AYX - Alteryx: Optimism Returning At Last

2023-11-07 23:47:34 ET

Summary

- Alteryx, a data prep and integration software company, enjoyed a ~20% post-Q3 earnings rally, helping to offset sharp YTD declines.

- The company's strong position in automation, data-driven decision-making, and analytics, along with its broad applicability across industries, are all core pieces of its bullish story.

- It is also moving upmarket into enterprise clients, while sales rep productivity is also improving.

- Valuation is very cheap at ~3x FY24 revenue.

Especially with the alleviation of interest-rate fears and the rebound rally in tech stocks over the past week, most tech companies remain up year to date - some in a big way. When looking at what investment opportunities make sense for beating the market going forward in a high-rate environment, however, it's the laggards that I am keenly interested in - especially in a stock like Alteryx ( AYX ).

This data prep and integration software company, prior to Q3 earnings, was down ~40% on the year. After reporting Q3 results which showcased an acceleration in growth and a "beat and raise" message not commonly heard in the industry this year, Alteryx popped nearly 20%.

Beat and raise quarter solidifies the bull thesis

In my view, this is the beginning of renewed optimism and a rebound in this stock. I last wrote on Alteryx in August and recommended investors be patient for a rebound, especially given the stock's valuation. Today, after parsing through the company's Q3 results and in light of its latest valuation metrics, I remain solidly bullish on this name.

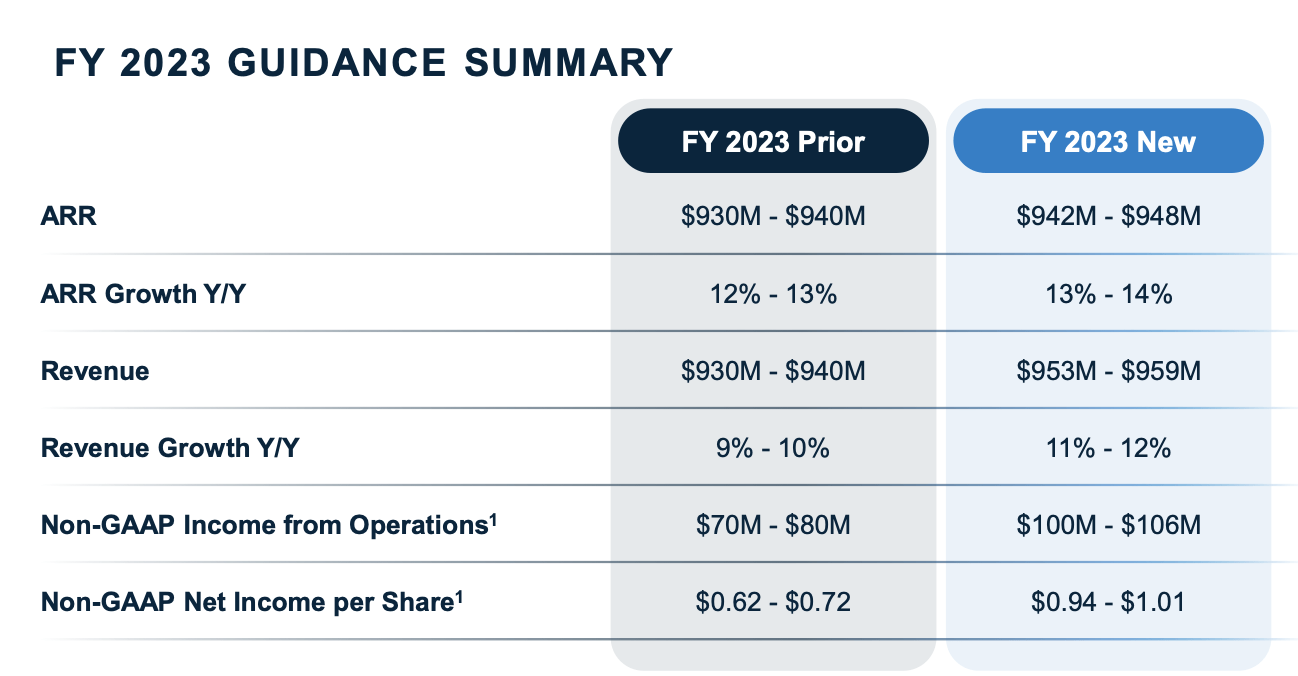

First, a cursory look at the beat-and-raise: the company took in bookings strength in Q3 which gave management confidence in raising the full-year revenue outlook to an 11-12% y/y growth range. At the same time, the company also significantly boosted its pro forma EPS expectations by 45% at the midpoint of the range, reflecting both stronger-than-expected top line momentum plus cost savings from the headcount reductions that the company has enacted since the start of the year.

{kind=link}

Beyond this outlook boost, here's a reminder of what I view to be the core bull case drivers for Alteryx:

- Automation, data-driven decision-making, and analytics are all powerful secular drivers for Alteryx. Companies want to use data to drive decisions. Unfortunately, data is sometimes locked in different formats and takes hours of manual work to untangle. Alteryx's technology helps with that process and automates one of the most labor-intensive pieces of adopting a "big data" strategy in the C-suite. Investing in technology like Alteryx may not have been a top priority during the pandemic, but it will become a much hotter-button topic as we look ahead.

- Large $113 billion 2025 TAM. Alteryx's current ~$1 billion annual revenue run rate is only a fraction of its estimated current $65 billion TAM, leaving plenty of room for growth. Alteryx additionally expects its TAM to expand to $113 billion by 2025.

- Truly horizontal software serving a wide variety of use cases across many industries - Alteryx's software is broadly applicable to clients in virtually any industry. An illustrative cross-section of Alteryx's customer base: Netflix ( NFLX ), Walgreens ( WBA ), Abbott Laboratories ( ABT ), Chevron ( CVX ), Wells Fargo ( WFC ), Visa ( V ), Marriott Hotels ( MAR ), and Facebook ( META ) are all among Alteryx's anchor clients, spanning every industry.

- Best-in-class gross margins of ~90% are among the highest in the software industry - Virtually every dollar of revenue for Alteryx flows through to the bottom line, justifying the efforts that Alteryx makes on the initial sale.

- Plans for significant profitability - Already, Alteryx has hit significant pro forma operating profits. Over the long run, it plans to generate pro forma operating margins in the 25-30% range, primarily by achieving economies of scale on sales and marketing. When a company like Alteryx has huge recurring revenue, over time the cost of sales support for that revenue base will eventually dwindle.

Stay long here: there are both short and long-term drivers for upside.

Valuation update

After earnings, Alteryx popped ~20% in after-hours trading to settle near $36. At that price level, the stock trades at a $2.58 billion market cap and a $3.13 billion enterprise value , after netting off the $682 million of cash and $1.24 billion of convertible debt on Alteryx's most recent balance sheet.

For next year FY24, Wall Street analysts are expecting Alteryx to generate $1.05 billion in revenue, representing 12% y/y growth. Consensus is also calling for $1.11 in pro forma EPS, which would be ~15% growth above the midpoint of this year's higher EPS range (estimates are likely to be revised upward following earnings). Taking today's consensus at face value, Alteryx trades at just:

- 3.0x EV/FY24 revenue

- 32x P/E

There's room for valuation expansion here, especially as Alteryx continues to chase upmarket deals while also refining its opex structure.

Q3 Results

Let's now go through Alteryx's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

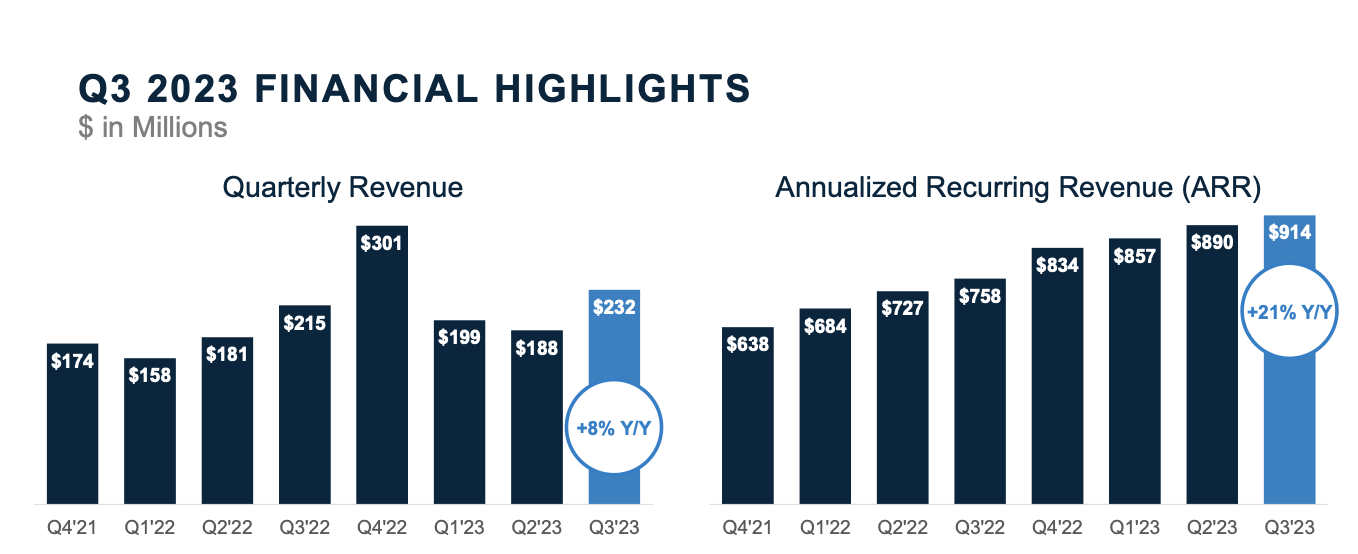

Alteryx's revenue grew 8% y/y to $232 million, accelerating over Q2's 4% y/y growth pace and decimating Wall Street's expectations of $210 million (-2% y/y) by a ten-point margin.

The core driver behind this outperformance is excellent sales execution. The company noted that it made big progress in pipeline management, with a more rigorous process for qualifying deals and managing the forecasting process - which has improved overall sales visibility. The company also fought back against a typical trend of backend-loading deals at the tail end of the quarter, helping prevent deals from pushing out of the period.

The company has also sold an increased number of ELA deals (enterprise license agreements). ELA bundles help to simplify pricing for customers, ultimately encouraging more cross-sell and helping net revenue retention rates. The company doubled the number of ELA sold in Q3 versus the prior-year period; meanwhile, net revenue retention rates clocked in at 119% for the company - indicating a 19% net upsell.

ARR, as shown in the chart below, also jumped 21% y/y to $914 million, adding $24 million of net-new ARR in the quarter. That's at roughly the same pace as Q2's 22% y/y ARR growth rate. The company exceeded its internal expectations for ARR growth by $9 million, and $15 million after adjusting for FX impacts that moved adversely since the company set its guidance in August.

{kind=link}

Per CFO Kevin Rubin's remarks on the Q3 earnings call regarding enterprise penetration and Alteryx's successful moves upmarket:

In recent years, we decided to up-level our go-to-market strategy to target the largest organizations in the world. In doing this, we hired experienced enterprise sales reps and leaders, enhanced our partner programs, and built out an enterprise-quality customer success team. Over the past year, we've seen progress on this strategy in our financial results, and that continued in Q3.

We're winning with larger organizations, as evidenced by our growing Global 2000 penetration, now at 49%. That's an increase of 10 points from two years ago.

We're winning larger deals. Our average deal size for Q3 expansion wins increased meaningfully year-over-year. And we're seeing our average customer size expand, as customers are increasing designer and server implementation, as well as exploring new use cases with our cloud-connected offerings."

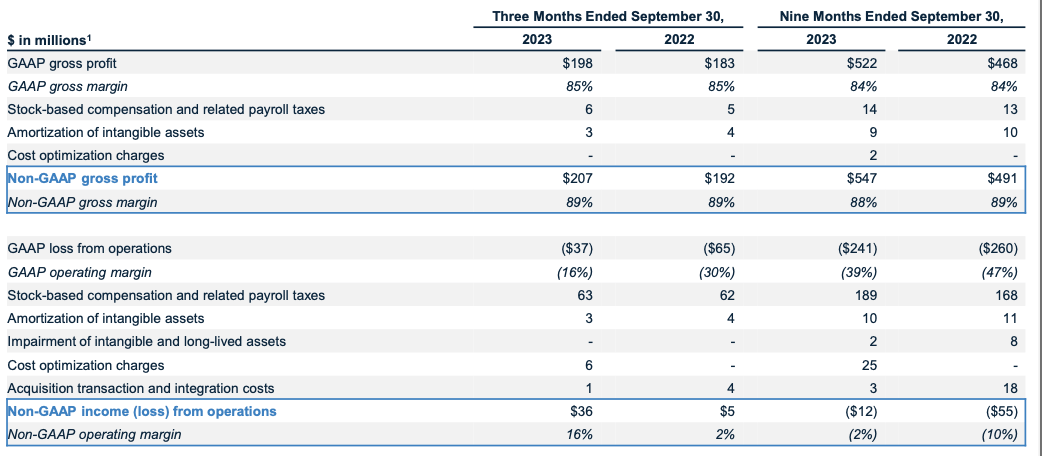

And, as shown in the chart below, driven by higher sales rep productivity as well as a reduction in pro forma expenses y/y across all of Alteryx's categories of spend, the company managed to surge pro forma operating margins to 16%, a 14 point improvement versus Q3 of last year:

Alteryx pro forma operating margins (Alteryx Q3 earnings deck)

{kind=link}

Key takeaways

With strong top-line momentum and tremendous cost discipline yielding significant profitability growth, there's a lot to like about Alteryx - especially at just a <3x forward revenue multiple. Stay long here and buy the earnings rally.

For further details see:

Alteryx: Optimism Returning At Last