AYX - Alteryx: Why It's Not A Core Portfolio Holding

2023-10-02 11:58:03 ET

Summary

- Alteryx's Q2 2023 results were below expectations and the management revised their full year guidance downwards, leading to a decline in stock price.

- The company's business model does not look scalable.

- There have been rumors of Alteryx exploring a potential sale, but even in the case of M&A, the company may not generate significant value for shareholders.

We think Alteryx's (AYX) analytics offering sits on top of the data pyramid, with unstructured data at the bottom and many levels of cleaned and standardized data in between. The company's Q2 2023 results and the management commentary around its business make us question the scalability of the standalone offering. We note that there have been some rumors on the M&A front, but find even in the case of M&A the company may not be able to generate significant value for shareholders. Thus, we would not want to have the stock in our portfolio.

Business

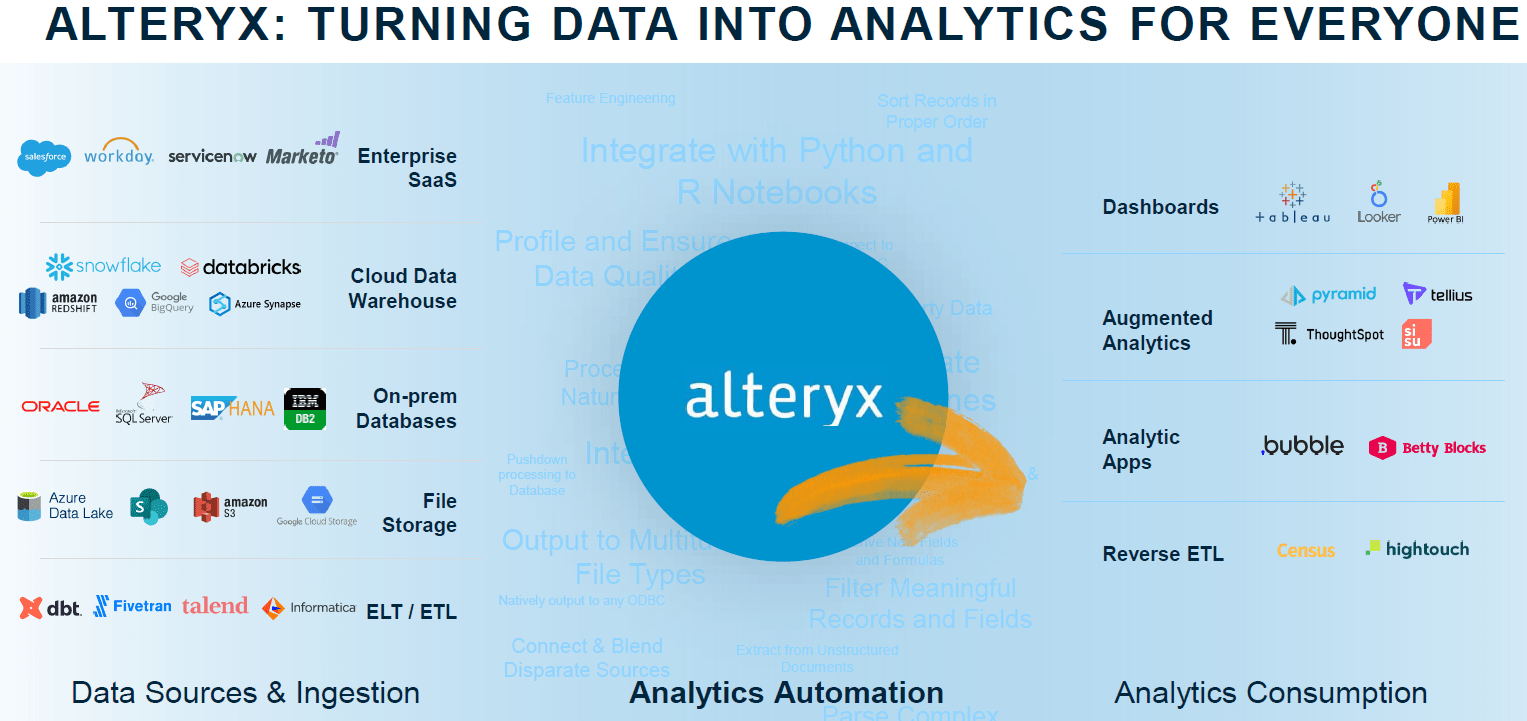

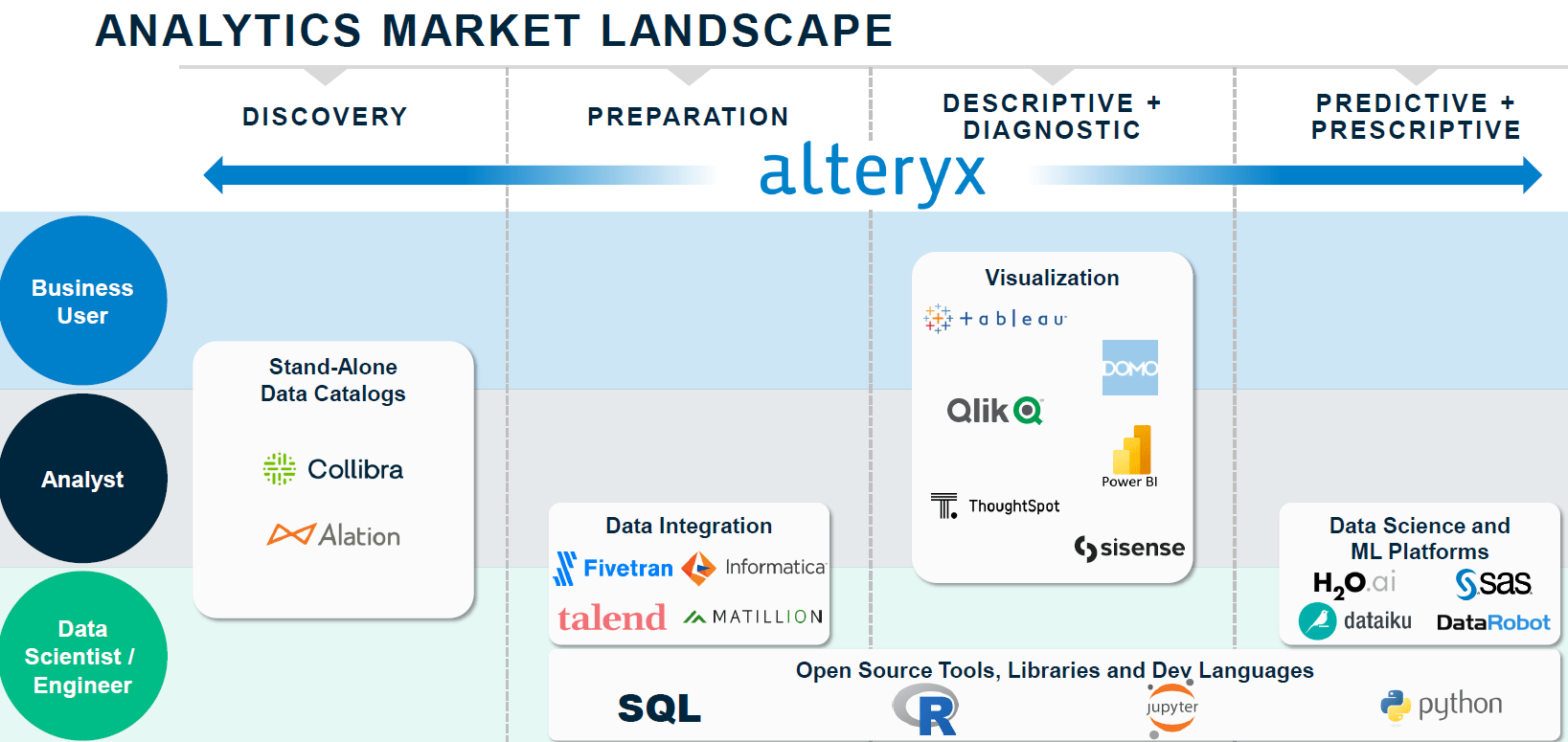

Alteryx is a provider of analytics software. The company claims that its software can collect information from disparate sources and transform them into insights. Alteryx defines itself as an orchestration layer technology (or a provider of abstraction) for the business user, who is presented tools to data synthesized from an environment with fragmented sources of data.

{kind=link}

The company's business model of data discovery, presentation, quality analysis and analytics pits it against a host of specialists in each area.

{kind=link}

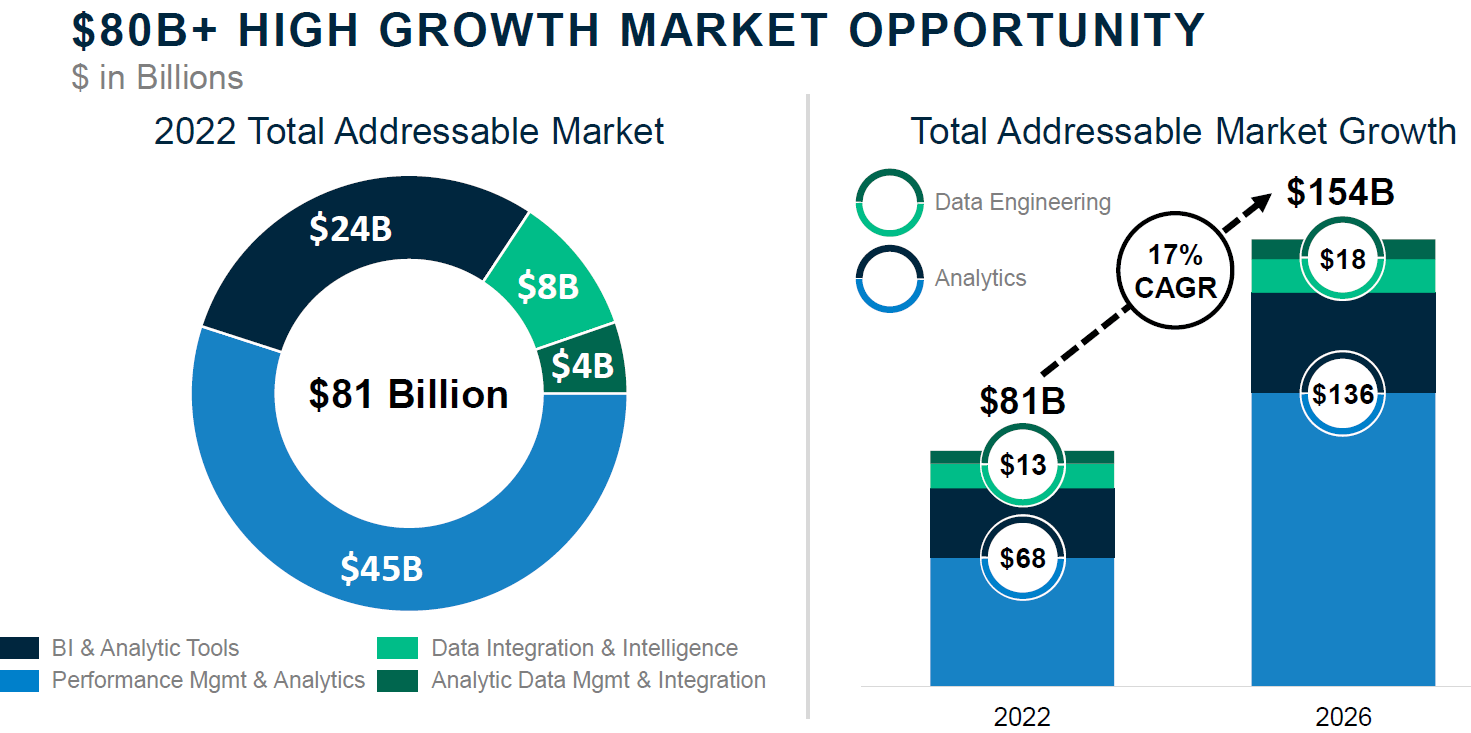

The breath of Alteryx's solution has led to the company targeting a large total addressable market or TAM.

{kind=link}

To cater to this diversified TAM, the company aims to cover multiple use cases through its product offerings.

{kind=link}

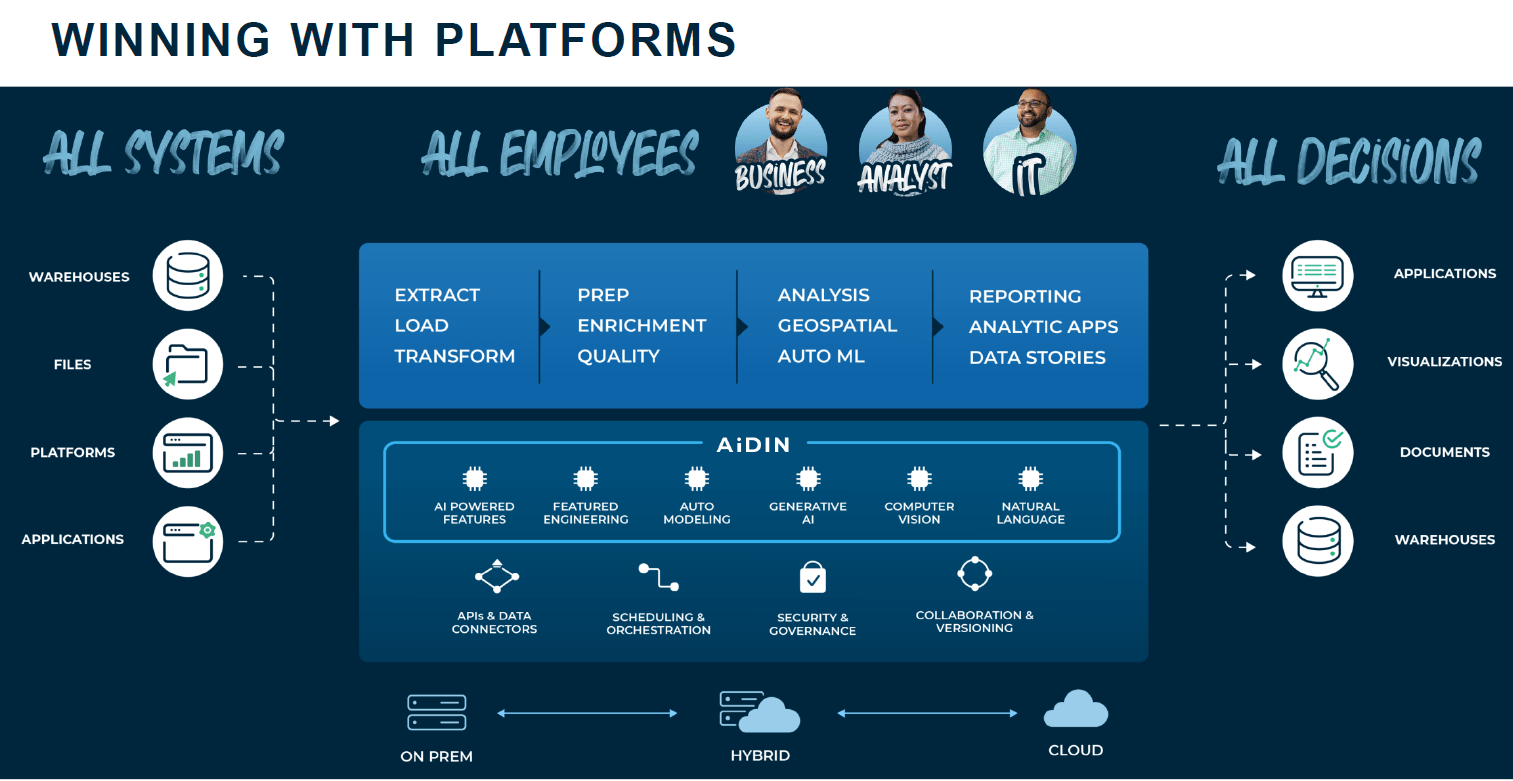

Considering the span of Alteryx's solutions, the company recently introduced 'multimodal,' a solution designed to allow coders to CXOs to collaborate on the same analytics problems.

... it's an environment that will allow different personas to interact with models in the way that's most comfortable for them.

So if you're a data scientist and you're comfortable in Jupyter notebook, we would have a representation of the model in Jupyter notebook for you. And so that data science can go review a model, interact with that model and then in effect, collaborate and share it back with another group of participants. If you're comfortable in a drag-and-drop environment, you'll continue to have the canvas experience. But if you're less sophisticated and you don't understand those things, we'll represent it to you in natural language so that you can interact with the model through basic query

Source: Alteryx, Inc. Management presents at Citi Global Technology Conference

Of course, multimodal is driven by generative AI and is among one of the company's generative AI projects to enhance growth and reach.

Q2 2023 Results

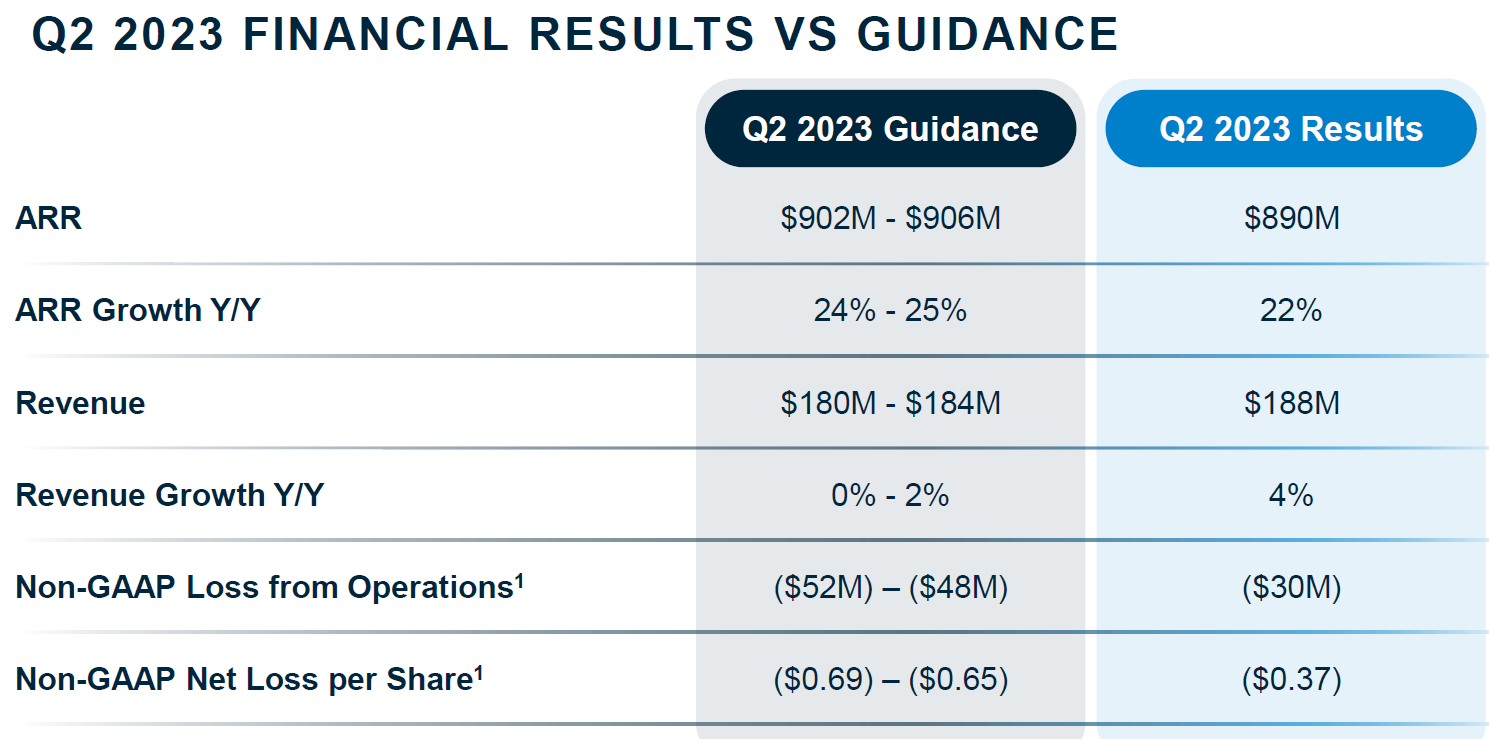

Alteryx's Q2 results were below the company's guidance.

{kind=link}

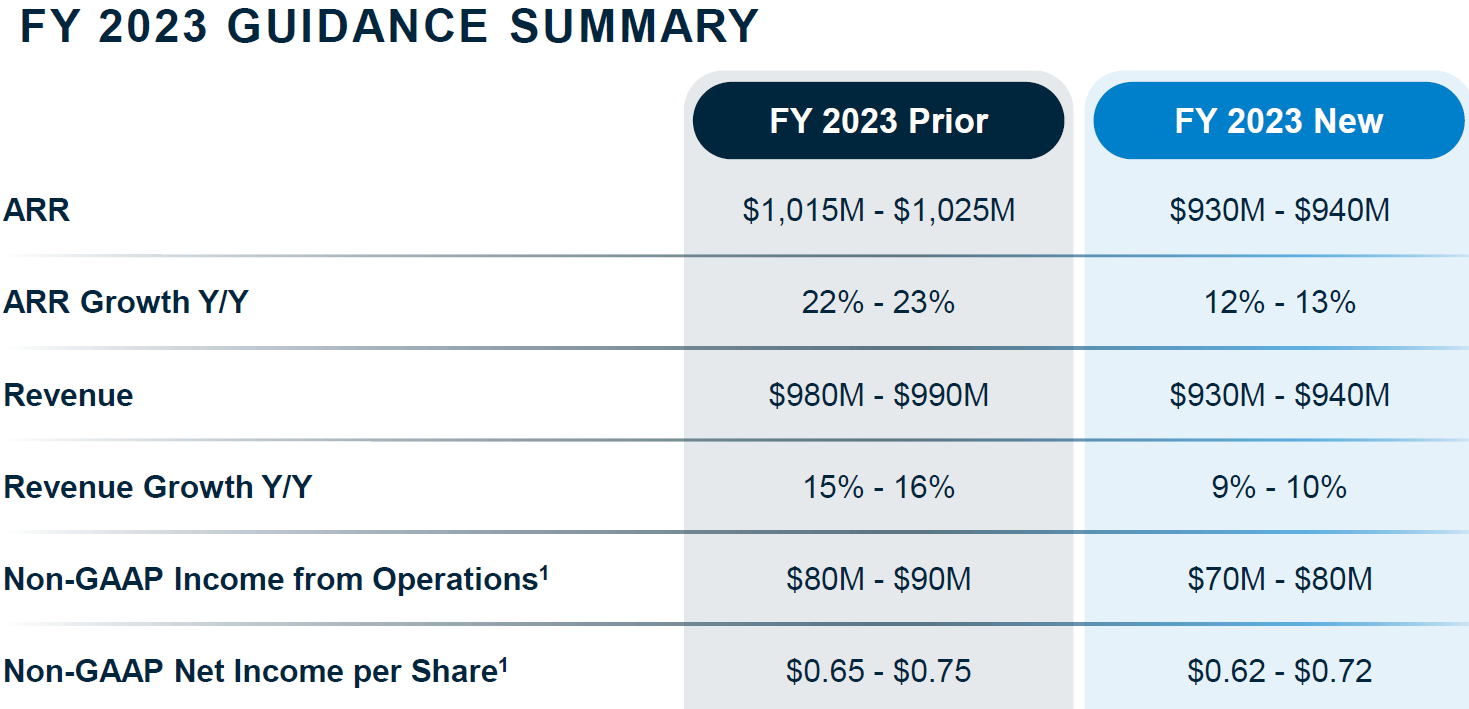

The management blamed macroeconomic issued and acknowledged execution challenges leading to the below expectation results. Consequent to a weak Q2, the management also revised the full year guidance, downwards.

{kind=link}

In response, the stock tanked.

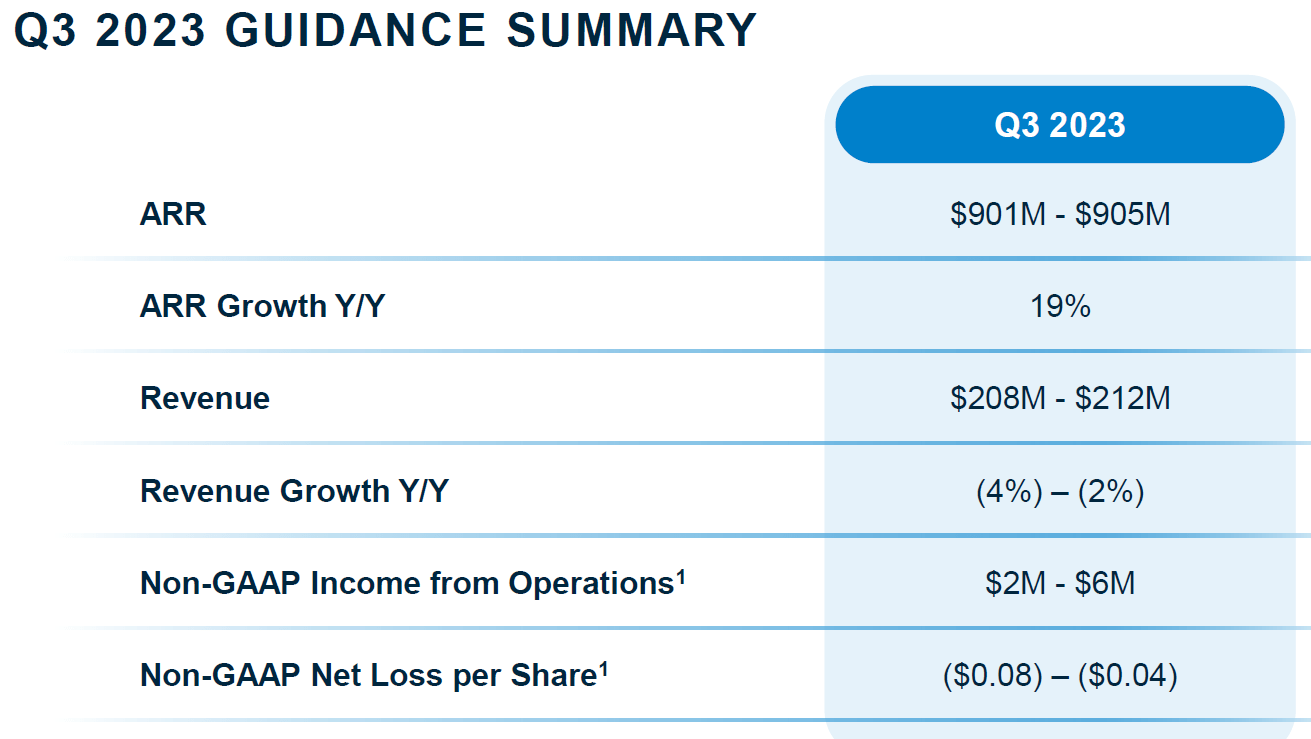

For Q3 2023, the management expects a revenue of $208-$212 million, a 2-4% decline and a 19% growth in ARR.

{kind=link}

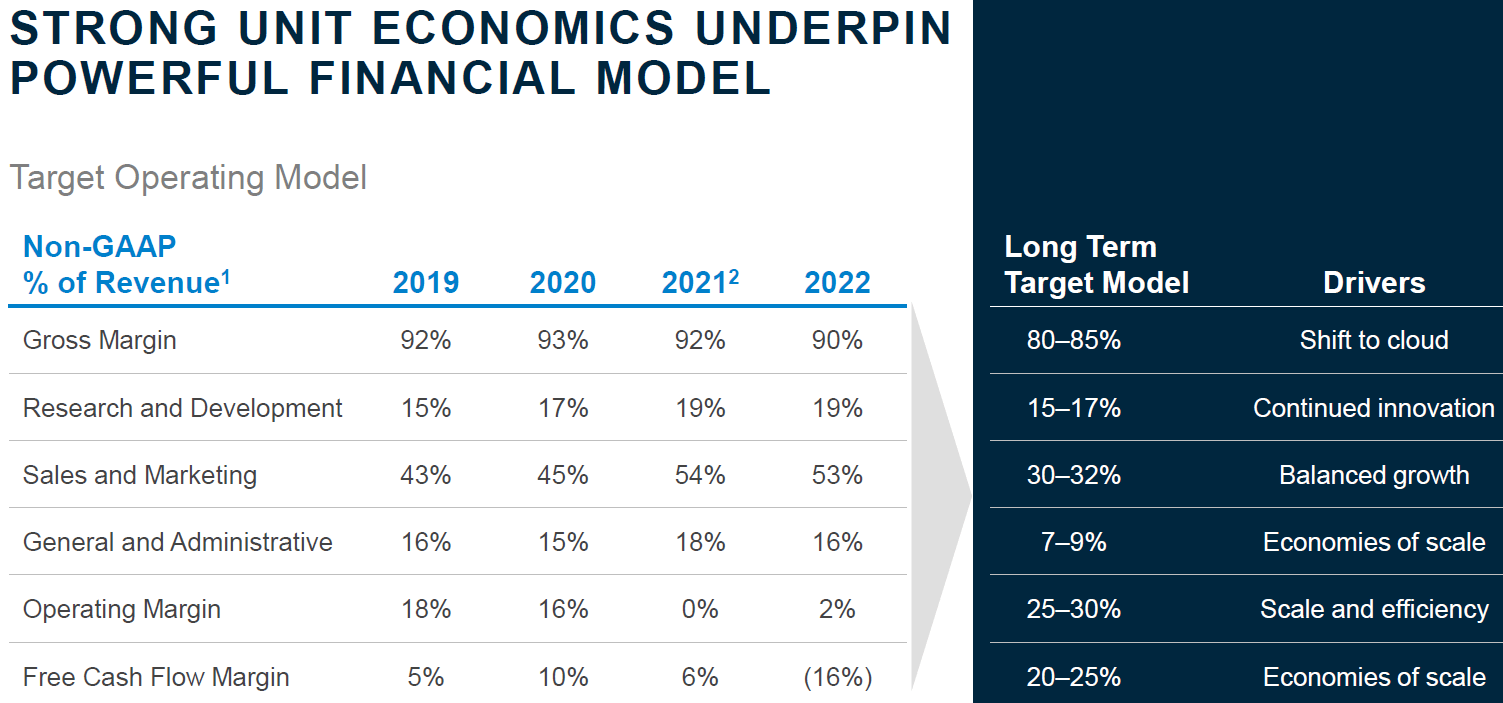

From a longer-term perspective, the management has some ambitious targets.

{kind=link}

The performance in Q2 makes the achievement of the drivers of the shift to cloud, innovation, sales organization restructuring and operating leverage difficult to envision.

Investment Thesis

Q2 2023 Results

The markets have punished Alteryx's stock on the back of results. We look at the key themes from the Q2 results.

Macroeconomic Weakness

The management called out change in customer buying behavior due to which Q2 was hit.

... While we had incorporated a tougher macro into our Q2 guidance, we encountered a pronounced change in customer buying behavior in the last two weeks of the quarter. This was especially apparent with larger customer expansion projects outside of the normal renewal cycle. As a result, many large customer upsell opportunities to which we thought we had clear line of sight ultimately pushed out of the quarter or closed with a reduced size.

… In the last two weeks of the quarter, we saw a significant divergence from historical conversion rates in which customers opted to delay or meaningfully reduce new initiatives until the time of renewal.

Source: Alteryx, Inc. Q2 2023 Earnings Call Transcript .

Execution Issues

Alteryx management also called out execution issues for not being able to close off the deals in the environment and vowed to make amends to the go-to-market strategy to better navigate the macro.

Renewal Event/Expansion/Enterprise License Agreements or ELAs

… Customer renewals, expansion upsells at the time of renewal and independent expansions outside of the renewal cycle. We saw healthy trends in both renewals and corresponding upsells. But it was the third element, expansion deals independent of a renewal event where we encountered challenges.

… we've seen our renewal base year-on-year continue to shift into the second half. So we have 72% of our renewal base for this year in the second half.

Source: Alteryx, Inc. Q2 2023 Earnings Call Transcript.

we introduced these two years ago, Q4 of 2022 was the largest dollar amount sold to-date at that point and so we have a large volume of those coming up for renewal in Q4 of this year. Q2 that just -- that we just closed was the second largest quarter of ELAs sold

Source: Alteryx, Inc. Piper Sandler Growth Frontiers Conference .

The management believes that while its consumption model remains robust, the weakness in the macro and tighter customer budgets (especially at the end of Q2) caused a lot of the pain. In the same breath Alteryx continued to see strong customer engagement.

This elevated level of engagement with our customers gives me confidence that the recent up-sell moderation is cyclical and not structural and that Alteryx remains well positioned for durable, profitable long-term growth.

Source: Alteryx, Inc. Q2 2023 Earnings Call Transcript.

On putting together the above data points, we observe the following: Q4 / H2 will be a loaded period for Alteryx from the perspective of renewal of ELAs and contracts, which poses a major risk - ELAs are one or three year and from the commentary above, despite having sold a bunch of these through the two years from Q4 2020 to Q4 2022, most of them are one year (coming up for renewals in Q4 2023).

Hence, a key aspect for us to watch out for will be if the customer engagement translates into longer-term ELAs - one-year renewals would not give us the confidence needed to invest in a very broad, horizontal (analytics) technology company.

The renewal rates will also cut across the macro and execution risks highlighted above - if there is an actual strong demand for the product, we should see deferred revenue growth along with gross margin strength (we can give a bit of a discount on this aspect due to the mix of cloud versus on-premise).

Hybrid Delivery Through A Mix Of Cloud And On-Premise

Alteryx continues to invest in both of its delivery modes, with no clear timeline of when they transition completely to the cloud.

Users of the Designer Desktop product, it's a rich experience, and it is -- it's kind of like trying to take candy from a baby. I mean the customers love that experience. So we're really trying to focus the initial cloud opportunities on different personas and different use cases, and we've had success in doing that.

…We don't have an intention to just simply replicate the Designer Desktop product in the cloud.

…as the cloud becomes more feature-rich and there are more capabilities in it, it will cover off on many of the things that the desktop product does, but that alone isn't necessarily what's going to make the customer's decision as to whether they deploy on-prem or in the cloud. I think there's other factors, governance, where does the data reside, what are they comfortable exposing outside the firewall versus inside the firewall.

…we've continued to innovate and develop on both sides, if you will. The on-premise is the vast majority of our ARR base today.

Source: Alteryx, Inc. Management presents at Citi Global Technology Conference.

The approach of continuing to invest in on-prem, when cloud should clearly be the way forward implies the following:

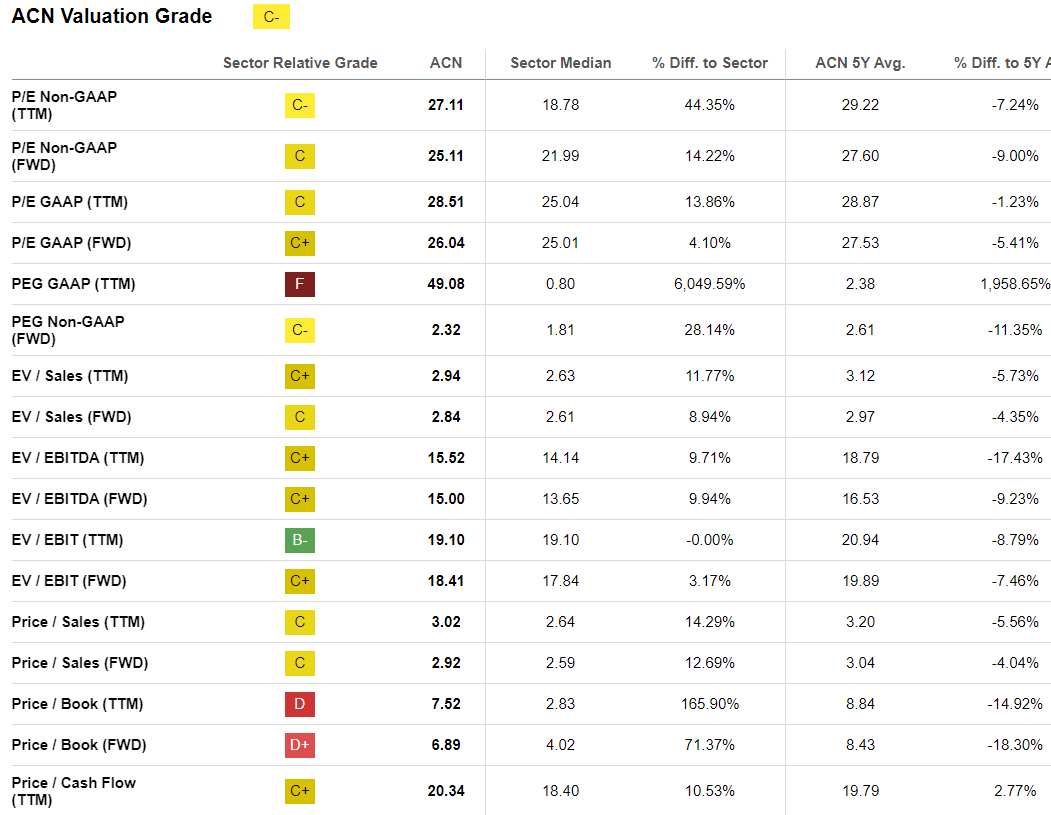

- While the software itself may be high margin, on-prem needs significant human support and hence at an EBITDA level it may not be a very pretty picture. The services approach to software then puts Alteryx in competition with the likes of Accenture (ACN), which fell after a revenue miss and soft guidance.

- Furthermore, we note the 'firewall comment' that implies that customers still need time to build trust with Alteryx orchestrating their data. This strengthens our doubt that the self-serve nature (and hence scalability) of the company's platform may ultimately be dependent on consultative (people-based) solutions. While the software itself does not need people to run, the system configuration may be needing a lot more support from Alteryx.

We innovate on the cloud in two-week cycles. So if you're a cloud customer, you are seeing rapid innovation being introduced to the environment on a regular basis. We have updates to the desktop products and the server products as well, but you just can't innovate and provide that to customers in the same friction-free way as you can on the cloud.

Source: Alteryx, Inc. Management presents at Citi Global Technology Conference.

While the obviousness of this comment is not lost on us, the management reluctance to fully commit to the cloud with such reasoning makes us seriously doubt 'economies of scale' as a credible driver of Alteryx's long-term plan.

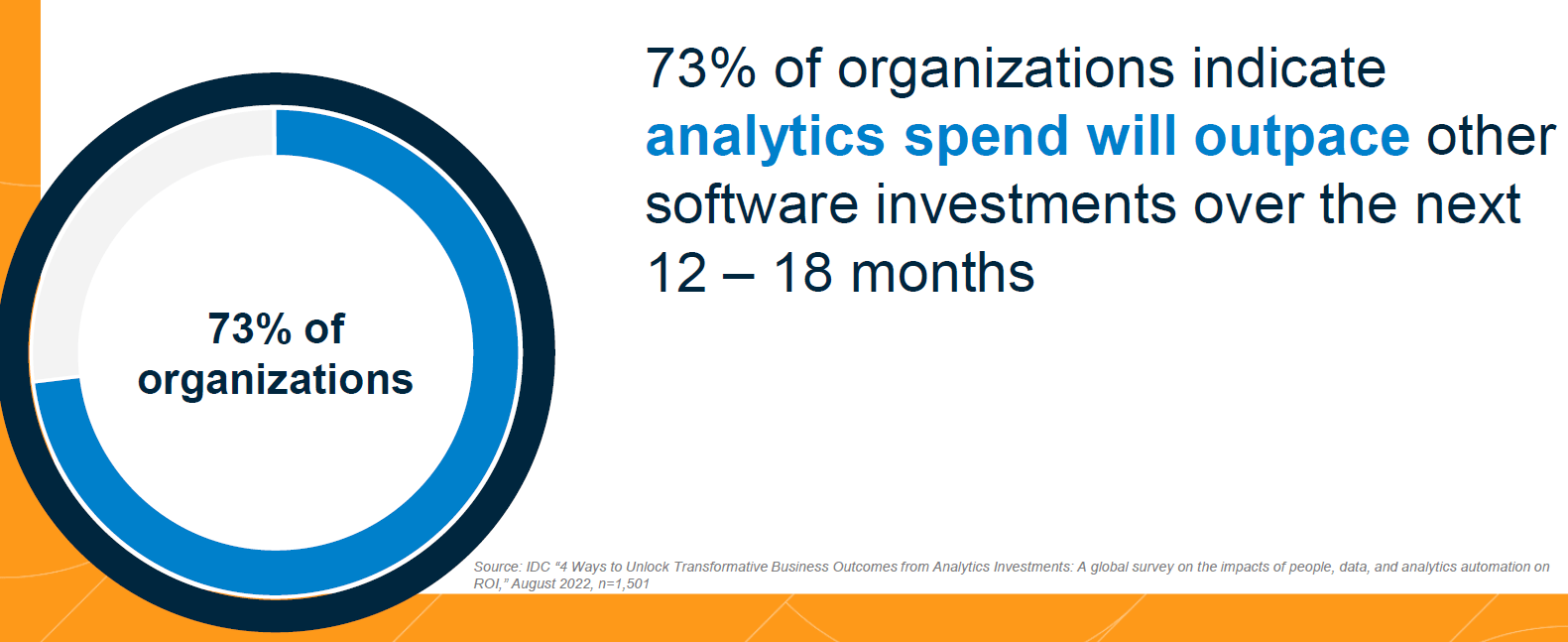

Lastly, we note that the company expects analytics spend to outpace other software investments over the next few quarters.

{kind=link}

This is in direct conflict with our findings. To set some context, as already mentioned, the company operates across the data to analytics value chain where analytics is the tip of the pyramid. In Gartner's Worldwide IT Spending July 2023 report , the research firm states:

"Generative AI's best channel to market is through the software, hardware and services that organizations are already using," said Lovelock. "Every year, new features are added to tech products and services as add-ons or upgrades. Most enterprises will incorporate generative AI in a slow and controlled manner through upgrades to tools that are already built into IT budgets.

When it comes to AI this year, organizations can thrive without having AI in production but they cannot be without a story and a strategy,"

We do not see Alteryx's approach aligned with any of Gartner's findings, which may have manifested in the Q2 2023 results.

M&A Talks

In early September 2023 , Reuters reported Alteryx was exploring a potential sale of the business.

While the management has not commented on rumors, we commend the logic. The company's standalone business has a discretionary element to it. As a horizontal Alteryx can possibly fit with the likes of Microsoft's (MSFT) Power BI or Informatica among others.

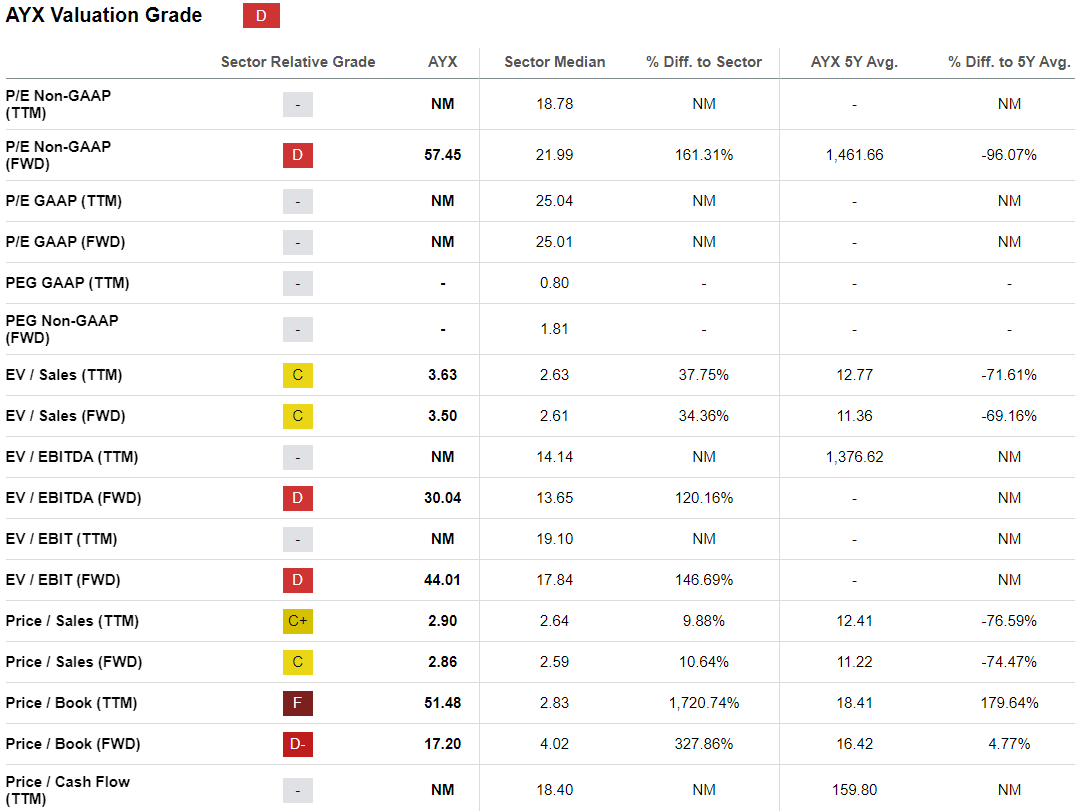

From a valuation standpoint, our business model assessment puts it closer to Accenture.

{kind=link}

Considering the sector median EV/Sales ('TTM') is at 2.6x, an M&A 30% premium would result in an EV/Sales of 3.4x.

{kind=link}

Given Alteryx already trades at 3.6x, the price uptick in case of M&A (with the Q2 2023 reported financials and expectations) is likely limited.

Conclusion

We think Alteryx is a strong application layer offering, which needs to have a dedicated database partnership. The standalone sale of analytics offerings poses a challenge in a world constrained by cost of money. Hence, we would not want to own the Alteryx stock.

For further details see:

Alteryx: Why It's Not A Core Portfolio Holding