CHTR - Altice: A Gameplan To Buyout Of Public Shareholders

2023-04-06 17:50:48 ET

Summary

- Stock is down over 90% from 2021 peak.

- Market cap is already a tiny sliver of the capital structure.

- Controlling shareholder Drahi could buy out public shareholders for less than half a turn of EBITDA.

- Drahi bought public shareholders in Europe two years ago under similar circumstances.

- Announcing my new Investment Group launch, Catalyst Hedge Investing, coming April 27th!

Basic Thesis

Let me start by saying I don't love the cable business. I think it's too leveraged in general, and many trends such as cord cutting and alternative broadband availability concern me. Technology changes can and will impact cable in ways that I find nearly impossible to predict. Taking that combination of factors into account, I have little appetite for long-term bets on really any cable company.

That said, I am never opposed to potential special situations with decent risk reward characteristics and I think I found one in Altice USA, Inc. ( ATUS ).

Altice US came public in 2017. It is the product of the combination of several US cable providers including Cablevision and Suddenlink that were bought by Patrick Drahi, a French entrepreneur who controls Altice Europe. Drahi is an interesting character. He stitched Altice US together in a similar fashion to the way he assembled cable assets in Europe, mostly through leveraged acquisitions.

The leverage from all of the US transactions makes ATUS a heavily leveraged entity. It has about $25 billion of net debt (after subtracting cash and hedged shares of Comcast) serviced by $3.6 billion of EBITDA, almost 7x. Servicing this debt and the capital expenditure required to maintain a cable system means free cash flow is only about $400 million.

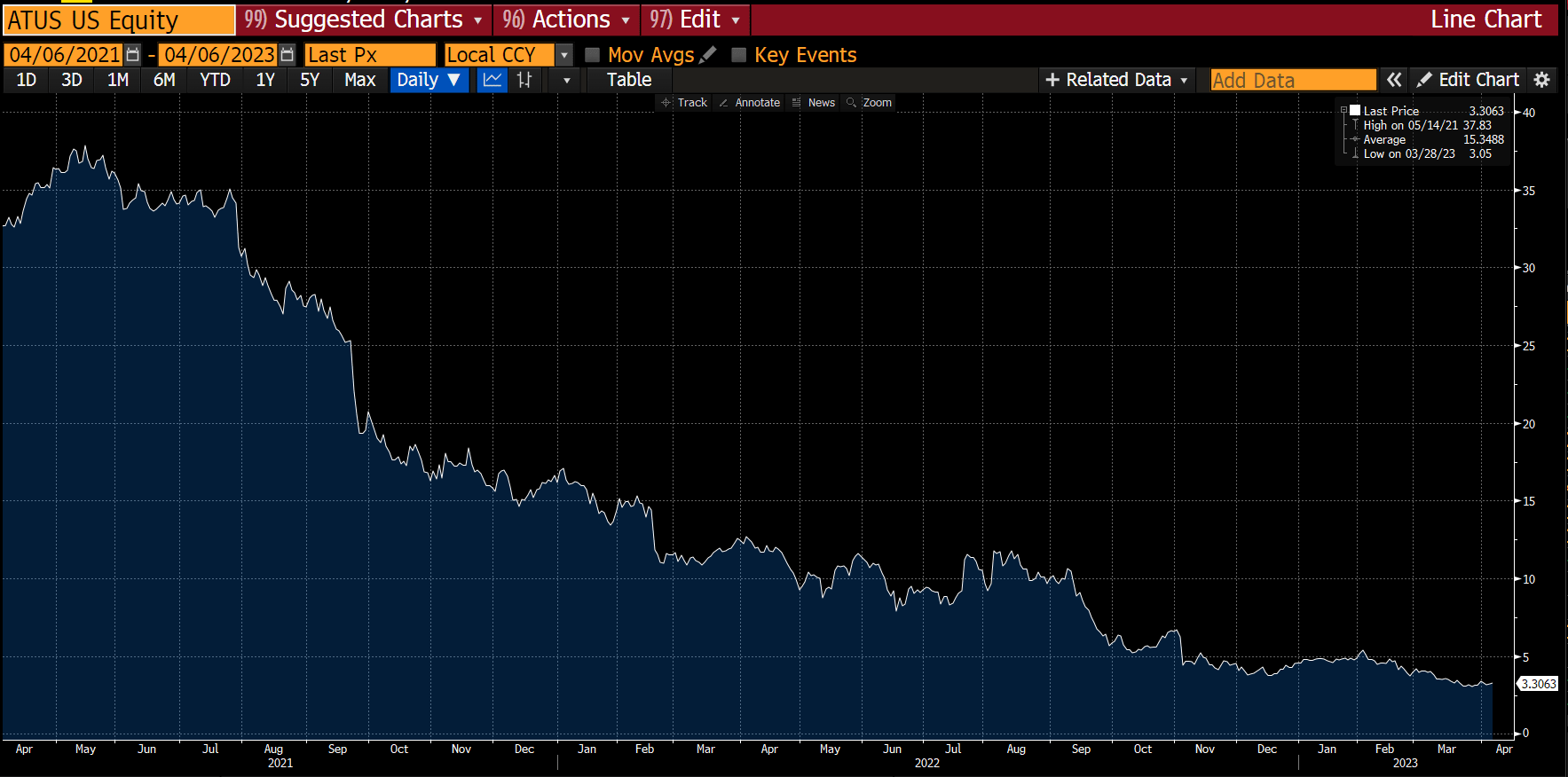

Apparently my hesitation towards the cable business and ATUS's leverage and skinny free cash flow is shared by others. The industry has had a rough few years. Pure cable carriers such as Charter ( CHTR ), WideOpenWest ( WOW ), and Liberty Broadband ( LBRDA ) have all seen their stocks perform miserably over the last two years. None has been as bad as ATUS tough. It peaked at almost $38/share in May 2021 and trades just above $3 as of this writing (April 6th).

Altice Stock Chart (Bloomberg)

{kind=link}

That >90% wipeout has left the company with just a $1.5 billion market cap on top of a $26.5 billion Enterprise Value. Drahi owns just under 50% of the company, which means the public float is less than $800 million right now.

Valuation

| Public Float of Stock (using ~237mm shares @ $3.30/share |

| $784 mm |

| Drahi's Shares (using ~216mm shares @ $3.30/share) |

| $713 mm |

| Total Market Cap |

| $1.497 billion |

| Cash |

| $305 million |

| Shares in Comcast (hedged with derivatives) |

| $1.5 billion |

| Debt |

| $26.887 billion |

| Enterprise Value |

| $26.556 billion |

| EV/2023 EBITDA (Using $3.6 billion) |

| 7.28x |

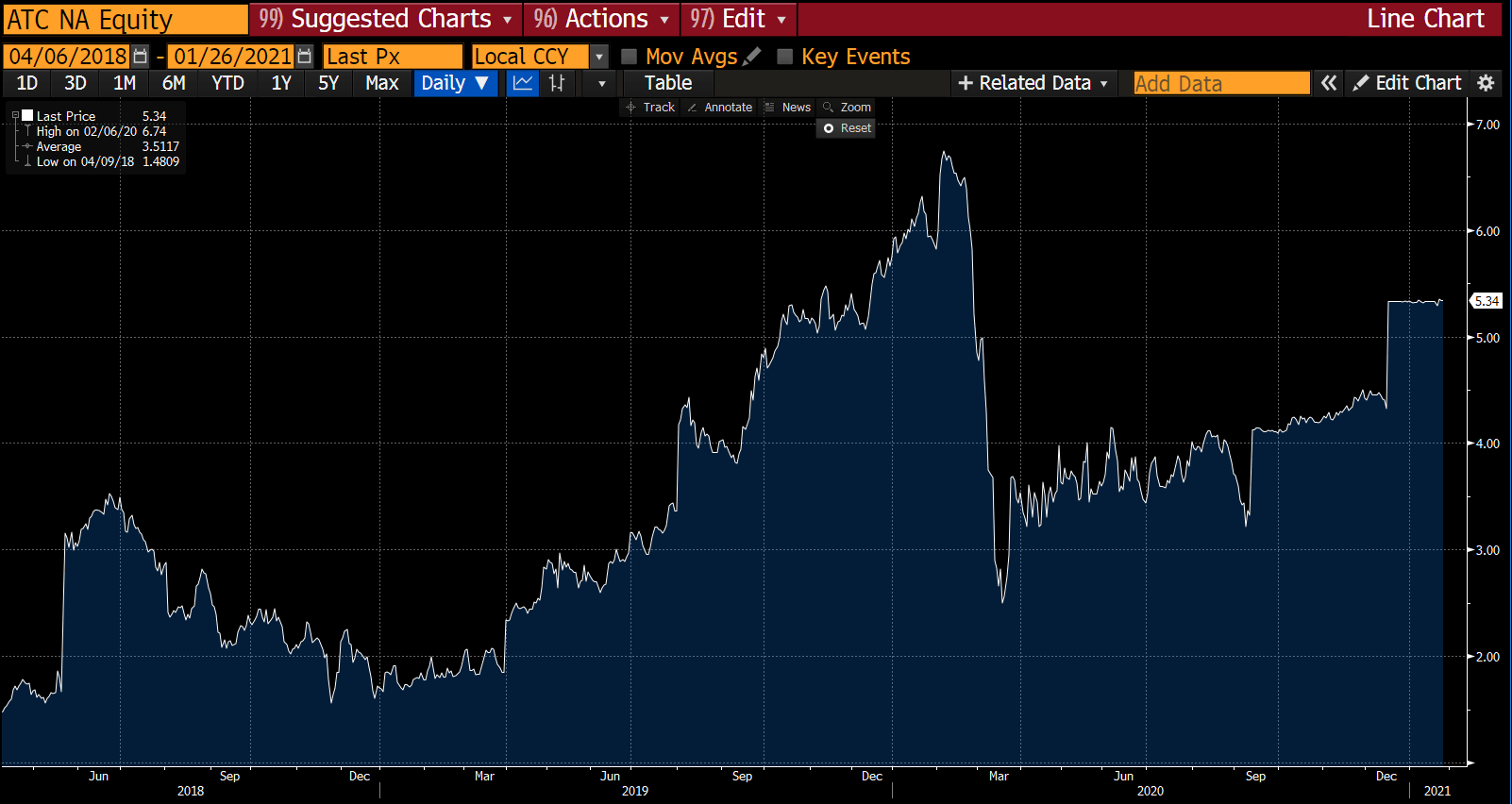

Here's where things get interesting. Altice Europe had a similarly poorly acting stock (which Drahi owned a lot of) on top of a leveraged capital structure. After a particularly nasty drop, Drahi bought out the public shareholders for a nice premium (compared to where the stock had fallen). The chart below shows the picture of 2020 drop and the deals that were agreed to later that year.

Altice Europe Stock Chart (Bloomberg)

{kind=link}

ATUS is lining up in a similar fashion in my mind. Drahi could offer public shareholders $5/share and own the entire company for just $1.2 billion. To put that into perspective, he raised over $2.1 billion when he IPO'd these US assets in 2017.

While Altice needs more leverage like another hole in the head, there are pockets of liquidity within the Altice US universe. The company sold a 49.99% in a fiber subsidiary called Lightpath two years ago at a $3.2 billion valuation (which corresponded to 14.6x $219 million of EBITDA. I estimate those assets conservatively throw off about $240 million of EBITDA now. Let's say multiples have compressed to 12x. The business is still worth about $3 billion. Back out $1.45 billion of debt and ATUS stake is worth about $750 million.

That's just one example of ways Drahi could find pockets of money to buyout public shareholders. I believe there are others.

For most people, $1.50 gain or so on a stock is peanuts. But in this case it's almost a 50% gain. Despite all of the leverage, Drahi has plenty of runway to operate the business given the $1.8 billion of cash and securities, a benign maturity profile on the debt, and the (albeit) small cash generation. Essentially, the stock is an option right now and there's little impending risk of financial stress, at least none that I see.

Risks

The main risk is that Drahi doesn't decide to follow the European game plan and leaves the US float outstanding. Then you just own a small market cap cable stock with too much leverage. Furthermore, a major and quick deterioration in cable performance would then pressure the company. There's so much debt here, a bankruptcy would mean little equity recovery. I don't think that's likely any time soon, but the bonds trade at a pretty high yield (over 10%) so it's a risk that has to be mentioned.

Conclusion

I like this setup is a classic catalyst-driven special situation for an acquisition of public shareholders in ATUS by Drahi. I think one could come fairly quickly if the European playbook is rolled out here. There is certainly downside given the leverage, but the leverage is partly why the stock has traded so poorly this year. This company though has time to change its structure and capitalization. The question is whether Drahi wants to bring public investors along for the ride. He didn't in Europe.

Announcing my new Investment Group!

My new investment group, Catalyst Hedge Investing , is launching on April 27. Please mark your calendars or PM me so you can reserve your spot as a Legacy Discount Member. There will be generous introductory prices for early subscribers that will continue for the life of your subscription. Keep reading my articles for more details, and thank you for following my work.

For further details see:

Altice: A Gameplan To Buyout Of Public Shareholders