AMX - América Móvil Struggling With Consistency

2023-07-06 09:47:34 ET

Summary

- América Móvil, a Mexican telecommunications corporation, has seen strong growth, with its stock price up 8% over the past year and 25% in the past five years.

- The company's strong Q1 performance was driven by growth in Brazil, but it faces inconsistency in performance across different countries and struggles to maintain ARPU with high churn rates.

- Despite the company's growth, investors should be cautious due to long-term telecom industry headwinds in Latin America and valuation multiples reflecting non-operating fluctuations.

América Móvil, S.A.B. de C.V. (AMX), a Mexican telecommunications corporation, was founded in 2000. Since its inception, the company has become a leading player in the global telecommunications industry. América Móvil operates in many countries, with a significant presence across Latin America and Eastern Europe. It provides a broad range of telecommunications services, including wireless voice, wireless data, and value-added services.

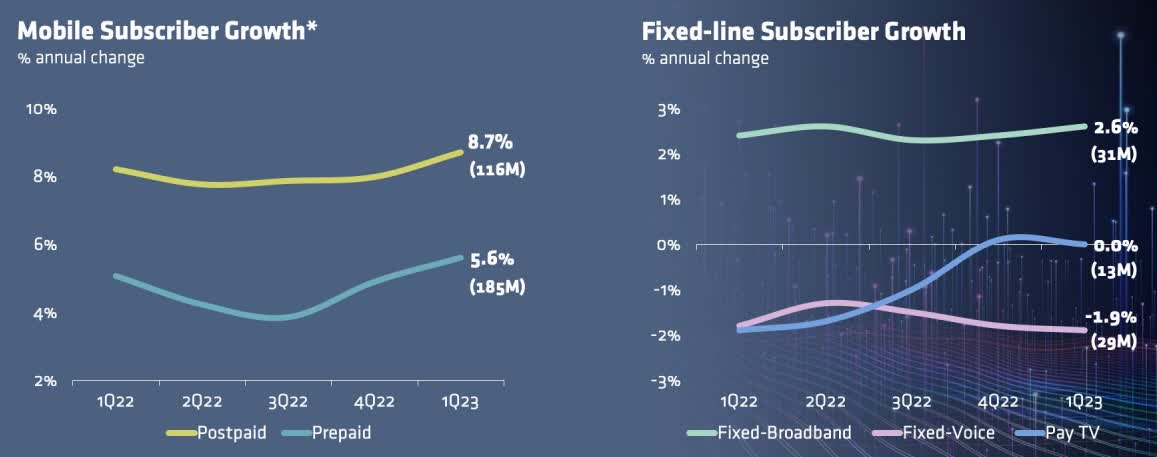

América Móvil has had a good run in the stock price, up 8% over the past year and 25% in the past five years. Q1 2023 results showed strong unit growth, and management put together a compelling narrative with 1.1 million new wireless subscribers, revenue growth, EBITDA growth, and a decreasing debt load.

Digging into the details, the story is not quite as compelling. América Móvil is experiencing materially different performance levels across countries and struggling to maintain ARPU, and net adds with high churn rates. In addition, the Latin American telecom market is facing long-term headwinds that will limit growth potential. I believe that the stock is priced fairly (if not a little high), given the risks, and investors should hold existing positions.

Brazil Drove Strong Q1 Performance

The bull case for América Móvil is that they are not only driving growth but accelerating it.

AMX Q1 2023 Growth (AMX Investor Relations)

{kind=link}

Exceptional Q1 performance in Brazil, as discussed in the Q1 earnings presentation , drove the business to new highs in subscriber growth. Based on industry analysis, Brazil is likely the best growth opportunity in Latin America, and América Móvil is capitalizing. The growth was also delivered efficiently, as Brazil had the highest EBITDA growth of any region, at 13.7%.

América Móvil has also shown great discipline in cost management, allowing them to navigate a high-inflation environment. Despite significant growth (and higher cost of sales), costs only grew 0.7% year-over-year.

Performance Across Countries Is Inconsistent

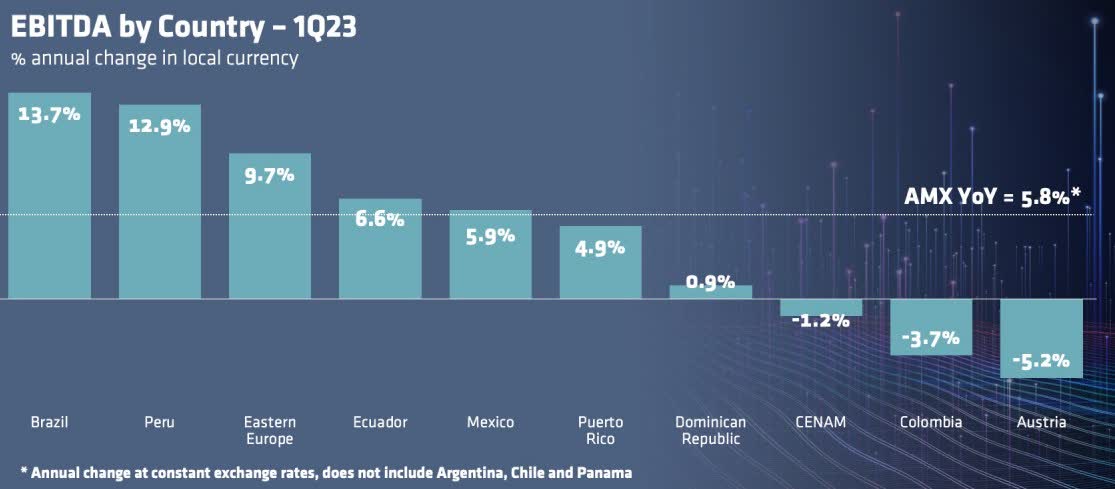

América Móvil has a problem with consistency across its operating region, and throughout the Q1 earnings call they avoided the topic, focusing on overall performance and the core markets of Brazil and Mexico. The Q1 earnings presentation provided the following EBITDA by country, which is telling:

Q1 2023 EBITDA By Region (AMX Investor Relations)

{kind=link}

EBITDA ranged from 13.7% in Brazil to -5.2% in Austria, while management's narrative focused largely on Brazil and Mexico.

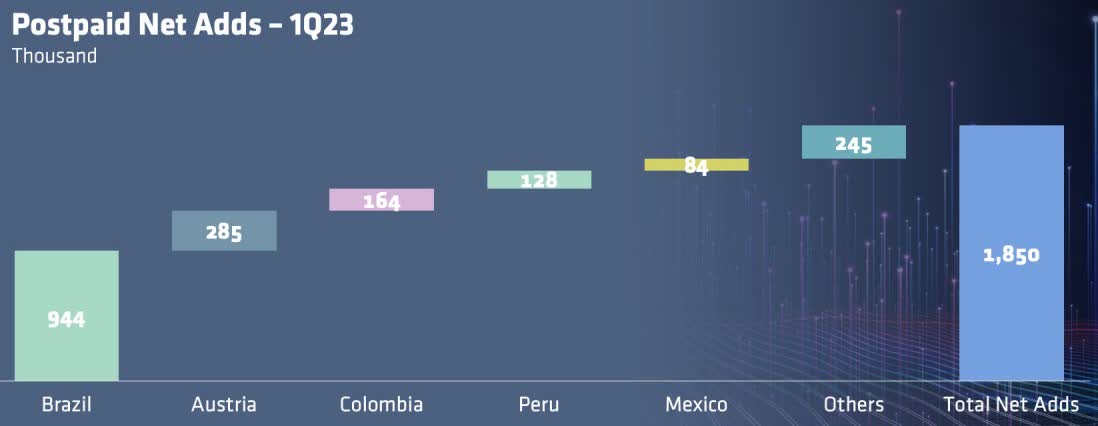

Q1 2023 Adds By Region (AMX Investor Relations)

{kind=link}

Looking at the volume side of the equation, net adds were equally inconsistent.

Management also quickly glossed over churn in the earnings call, noting that they were "putting resources behind it." I call this out because churn increased in both Brazil and Austria, the highest growth regions.

I have a similar concern on the rate side. América Móvil provides financials by region in their earnings release . ARPU was well below inflation in almost every region, if not declining. Using Brazil as an example, ARPU grew 4.2% year-over-year, while inflation has been running close to 6% over the last year.

I am concerned that management doesn't have a handle on running all regions. In addition, I do not believe they are focused on driving the right balance of rate and volume to offset inflationary pressure.

Long-Term Telecom Headwinds

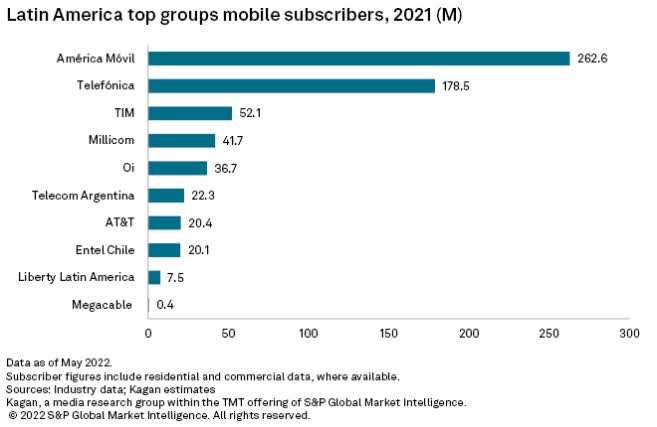

As América Móvil works to continue its current growth trajectory, it faces headwinds from the Latin America telecom market, as well as its own scale. They are the largest provider in Latin America by a clear margin.

Latin America Telecom By Customers (S&P Global)

{kind=link}

Given the scale, I believe that their biggest challenge is regressing to the mean . América Móvil grew mobile service revenue by 9.3% during Q1 2023 . However, the entire Latin American market is only expected to grow by 2.9% from 2022 through 2027. The fight for market share will ramp up competition in key growth markets like Brazil ( growing at 6.1% over the same period) and likely drive down ARPU.

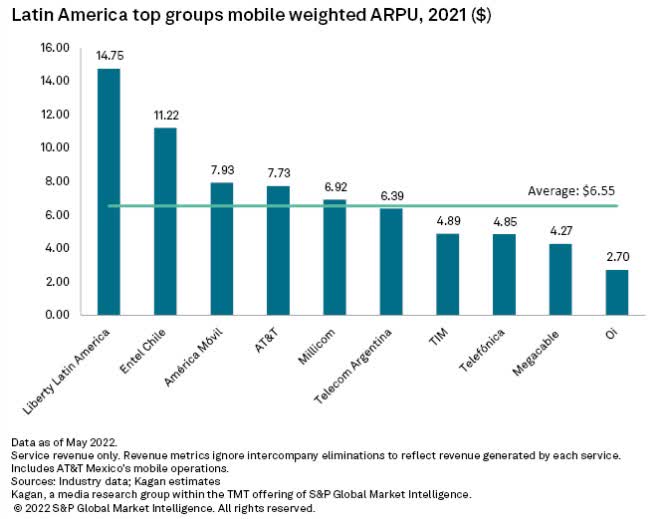

In fact, ARPU has already been on a downward trend for 10 years, despite high inflation. From 2011 thru 2021, ARPU across Latin America declined at a CAGR of 6.7%. Just as América Móvil is above average in size, they are above average in ARPU at $7.93 versus the industry average of $6.55.

Latin America ARPU (S&P Global)

{kind=link}

As growth opportunities become more limited, I feel that maintaining both market share and pricing while bucking industry trends is unlikely.

Valuation Multiples Reflect "Non-Operating" Noise

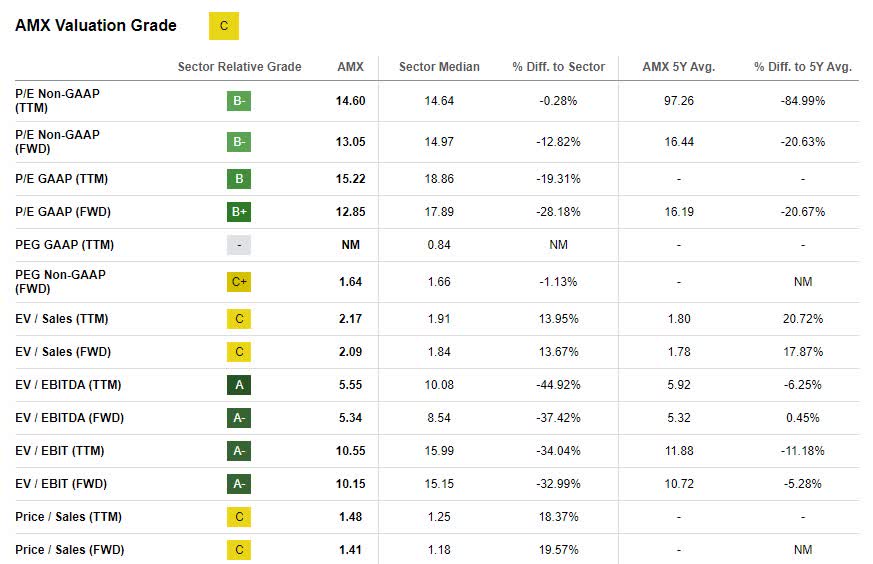

At first glance, the valuation multiples make AMX look like a compelling investment opportunity.

AMX Valuation Multiples (Seeking Alpha)

{kind=link}

However, the stronger buy (A and B) ratings are all in earnings and profitability ratios, while the hold ((C)) ratings are in revenue and sales ratios. This is critical because of the non-operating noise that positively influences earnings and profitability, as reported. There is a perfect example in the Q1 earnings release . EBITDA, as reported, was up 12.6% year-over-year. Adjusting for extraordinary items, EBITDA growth decreases to 5.8%. Adjusting for Fx, EBITDA growth decreases again to 3.2% year-over-year.

Q1 2023 EBITDA to Net Income (AMX Investor Relations)

Financing expenses, Fx, and equity participation for AMX are highly volatile and impact cash flow and earnings. In 2023, they were largely negative on profitability. However, their impact is not captured in the valuation ratios. The multiples quickly move closer to the hold range using adjusted EBITDA or EBIT.

Verdict

Despite strong Q1 performance, I believe investors should be cautious when it comes to investing in América Móvil stock. Management must show they can sustain growth across different countries and mitigate long-term telecom industry headwinds in Latin America. Valuation multiples reflect non-operating fluctuations from Fx and other business interests and are not as strong as they appear. I believe investors should hold existing positions and wait for a more compelling investment thesis to develop.

For further details see:

América Móvil Struggling With Consistency