MBI - Ambac: Releasable Liquidity And SOTP Analysis Reveals Upside Potential

2024-01-10 13:10:46 ET

Summary

- Ambac is a complex company with a financial guarantees business and a new specialty P&C insurance business.

- We run a comparison with MBIA to compute releasable liquidity from the FG business that may be paid out as a special dividend.

- Ambac may benefit from a liquidity release or a sale, but the bulk of its value lies in its new businesses.

Ambac (AMBC) is a complex company with many activities, and we believe the market is failing to properly evaluate it. We think that comparing it with the only publicly listed “competitor” may be useful to shed some clarity over its financial guarantees business. MBIA Inc, indeed, recently paid a special dividend that was greater that its market cap, after the regulators allowed for the release of extra liquidity in their subsidiaries. Will this be the case for Ambac too? Let’s look closer.

The good and the ugly: Ambac's new and old business

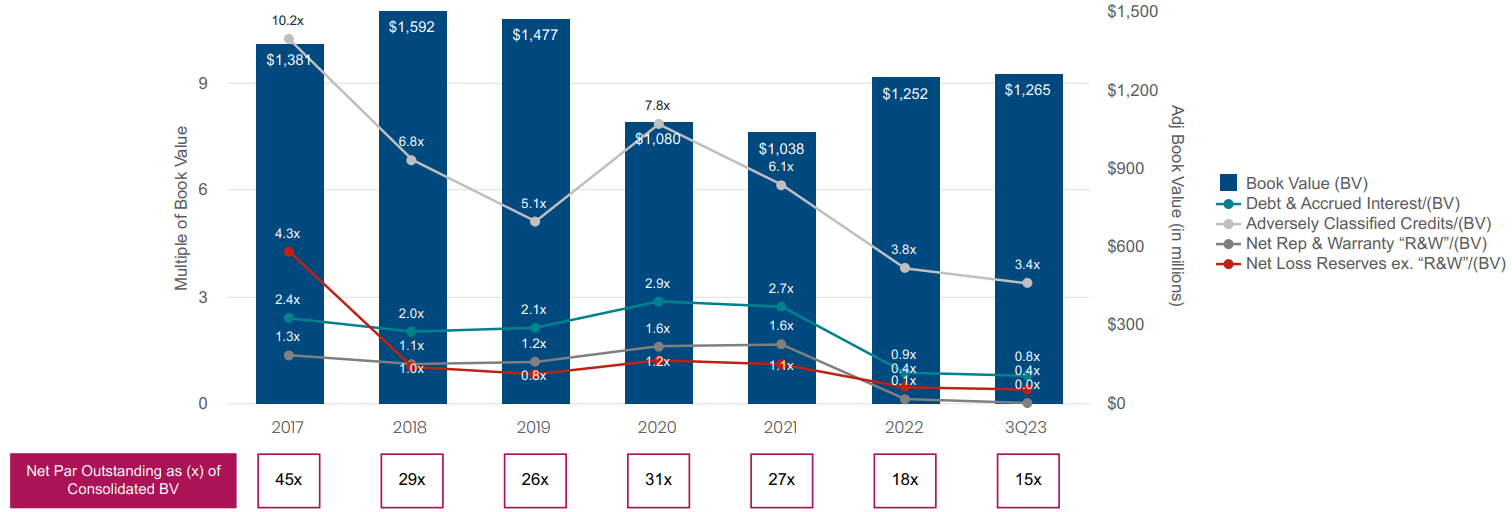

Ambac was very active in the years before the GFC selling generous financial guarantees in the form of insurance to bonds, structured products, and other financial instruments. Imagine AIG CDS business, but luckily much smaller. After the crisis hit they were left with a huge pile of problems that are hard to get rid of. Financial guarantees are serious obligations and even after Chapter 11 from which they emerged in 2013 (after 3 years) they still have this old division of the business as discontinued on their balance sheet. However, we can say that AMBC did a great job of de-risking the portfolio by restructuring many positions and engaging in reinsurance, helped also by the maturity of many obligations. Let’s have a look at the Financial Guarantees subsidiary’s position: book value stands at $1.2 billion with $29 billion of gross par (max exposure) outstanding. Adversely classified credit to BV is around 3.4x times. This is a big difference compared to the 10.2x times of only 5 years ago.

{kind=link}

But management is putting some effort into building something new. They found a niche in which they feel expert enough to operate efficiently, that is specialty P&C insurance. They are building a mixed business with both an underwriting and a brokerage segment that will take care of complex clients' needs.

Ambac Business Model (Latest Presentation)

This is a good summary of what the new platform looks like. A series of three different subsidiaries will deal with (1) underwriting risk, (2) providing special distribution channels (brokerage), and (3) acquiring strategic insurance-related stakes. We believe there is a genuine opportunity to build a strong company managed by expert insurers that can operate a profitable underwriting business and collect enough cash to scale. Let’s dive into both cases, the dying FC segment and the rising P&C insurer.

A hard but necessary comparison: MBIA and Ambac

For some companies, it is really hard to find true comparables that present similar characteristics. In the case of Ambac it’s even harder because the practice of insuring complex structured products really diminished after 2008. Today there is one similar stock, that is MBIA Inc. (MBI). The news is very recent of a special dividend that MBIA paid to shareholders and that was greater than the actual market cap. This caused a surge of more than 100% in the stock price. Many speculated that Ambac could be next given that they announced a strategic review and appointed Moelis as special advisor in the last earnings release. This could increase the chances of a sale, a liquidity release, or other resolutions that may benefit shareholders. So let’s see if what happened at MBI could be replicated here.

First of all, we need to compare the exposures and book values, to be sure of using apples-to-apples metrics.

AMBC v. MBI Comparison (Author's estimates)

For liquidity sources, we use a non-GAAP metric called “Claims-paying-resources” (CPR). This is a measure that takes book value, adds back reserves and unearned premiums. This is because reserves are on the liability side but are unlocked when a loss occurs, and premiums that are due are subtracted from payables. The total amount at AMBC is $2.5 billion, and at MBI is $2.8 billion. National and MBI are the two insurance subsidiaries at MBIA, and the release came from National’s reserves.

Second, we want to assess exposure.

AMBC v. MBI Comparison (Author's estimates)

We take several metrics here as the two companies don’t provide exact disclosures in their filings. Gross Par represents the total par value of the insured assets and is useful to compute the maximum level of losses if defaults were to occur. We see that MBIA benefits from higher CPR but has gross par exposure 50% above Ambac’s. Then we want to look deeper and see how many of these insured assets have a high-quality rating (above IG). We notice that the below-A-rated to CPR is much higher for AMBC, which stands at 4.6x times compared to 2x of MBI.

Last but not least, we use an official metric of riskiness which is the watch list + Adversely Classified (ACC). This comprises a series of assets that are put under strict watch as default is believed imminent, occurred, or at least at high risk. The ratio is again higher for Ambac, particularly if compared to the pre-dividend MBI, which was only 1.7x times.

We conclude that no liquidity releases can be done at this time for Ambac, at least not by maintaining the same riskiness as its competitor, which is lower at this time. But not all hope is lost. We believe that value can still be unlocked under two conditions: (1) Ambac is allowed higher ratios, or (2) a buyer of the assets would pay a premium. While the latter is not impossible but unlikely given the current high rates, we believe that it is possible that insurance regulators allow for “higher risk”. This could be justified by the overall lower par, and the demonstrated ability of the company to slowly but effectively eliminate liabilities at very low cost through reinsurance/restructurings. The Puerto Rico case is an example of this, and Ambac got away with a much smaller obligation compared to MBI.

Let’s analyze how much can be released if the company is allowed a ratio of ACC+Watch list over CPR of 2.5x compared to the current 2.35.

AMBC Releasable Amount (Author's estimates)

The computation is simple. We take the difference in the two ratios and multiply by the CPR. We notice that this means releasing 15% of the current CPR, which is around $370 million of extra cash. If distributed to shareholders, it would translate into a special dividend of around $7.90 per share. But this is not all, because there is also the “new” business to evaluate.

A SOTP approach to Ambac’s aggregate valuation

Breaking their business into various pieces can be efficient if they feel they do not have significant synergy gains between subsidiaries. Plus it increases the quality of compliance. However, it makes the job of evaluating the company a bit harder. We will use a Sum-Of-The-Parts analysis to evaluate their various subsidiaries separately, and then sum them all together to derive the value of the group.

Let’s see a summary of what we will do.

AMBC Valuation Model (Author's estimates)

This table summarizes: (1) the segment evaluated, (2) the valuation method, and (3) the multiple/metric attached. For the P&C underwriting business we used a BV multiple, as it is the standard in the industry. We feel a 1.25x multiple is representative of their expertise and focus on a niche P&C, and the good results accomplished so far. For the broker we simply take an EBITDA multiple, since they are not a balance sheet business. The legacy FG division will be evaluated based on the current releasable amount that we previously computed. Last but not least, we take what’s left at the HoldCo level in terms of cash and the market value of the liquid assets, as reported in the filings.

The overall result is a fair value of around $800 million, which is already net of debt as the bulk of the obligations is already accounted for at the FG segment level. Nevertheless, this represents a fair value per share of around $17.5-18, and thus an upside potential of 15%.

Conclusion

Ambac is a complex insurance company with both an “old” and a new business division. In the last months, various speculations about the comparison with MBI and a strategic review tried to evaluate if something similar could happen at Ambac. We believe that the company may benefit from some form of release, but that the bulk of the value seems spread across their new businesses. The final aggregate value seems to be around $18 per share.

For further details see:

Ambac: Releasable Liquidity And SOTP Analysis Reveals Upside Potential