NVS - Ambrx: Next-Generation Antibody-Drug Conjugates Buying The Dip After ESMO Data

2023-10-24 11:23:00 ET

Summary

- Ambrx Biopharma Inc. common stock experienced an irrational selloff following the Phase 1/2 ESMO data release for its ADC candidate ARX517, presenting a buying opportunity.

- The company's technology for next-generation ADCs has shown safety benefits and potential efficacy, making it an attractive acquisition candidate.

- ARX788, an ADC candidate for metastatic breast cancer, alone has the potential to drive a significant upside for Ambrx stock.

- Rating Ambrx Biopharma Inc. Buy with a price target of $28 (120% upside) based on the discounted cash flow valuation method (model included).

Company logo

Bought the dip in Ambrx Biopharma Inc. (AMAM) following the irrational selloff following the release of Phase 2 data for its antibody-drug conjugate, ADC candidate ARX517 in treating metastatic castration-resistant prostate cancer, mCRPC in the ESMO conference abstracts.

Rating AMAM stock "Buy" with a price target of $28 (210% upside) using the discounted cash flow, DCF, valuation method. Just based on the HER2+ metastatic breast cancer, mBC indication, the stock has enough upside where ARX788, another ADC candidate, has shown efficacy in a post-Enhertu refractory setting. Phase 3 U.S. trial data is expected by year-end. The company is also an attractive acquisition candidate.

__________

The sell-off in AMAM stock due to ARX517 safety concerns is irrational

mCRPC is seen in 1.1% of all prostate cancers. The prevalence of mCRPC is 62 per 1000K men, and its annual incidence is 21 per 100K men (company data). Prostate-specific antigen, PSA, is used as a biomarker for monitoring the treatment response in this cancer.

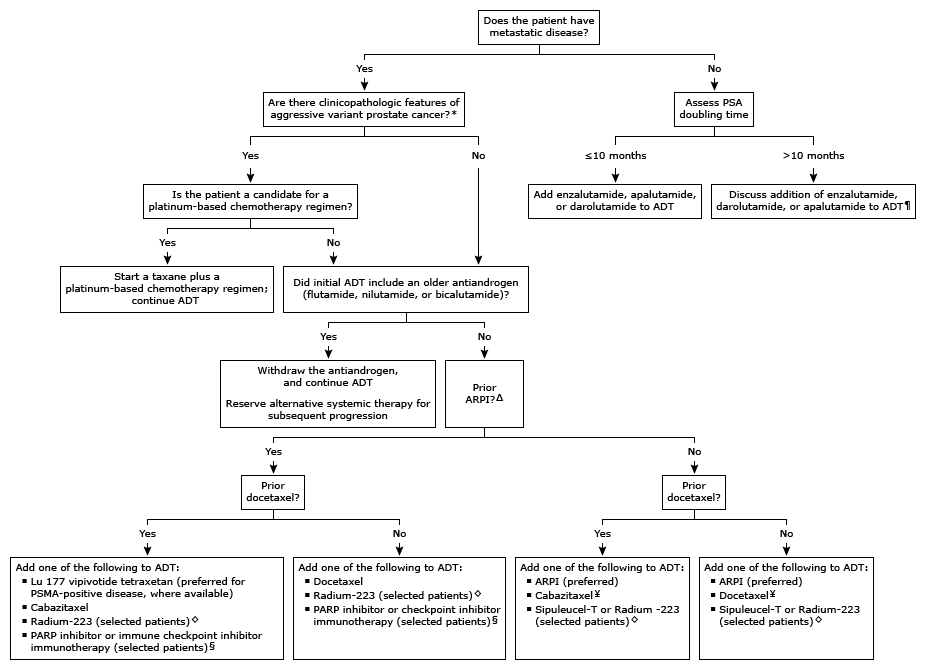

Systemic treatment algorithm for treatment of metastatic castration resistant prostate cancer (UpToDate)

{kind=link}

Recently, radioligand therapies like Novartis' (NVS) Pluvicto have been approved for this condition and have a peak sales estimate of $2 billion/year.

The company's technology (founded at the Scripps Institute) is based on next-generation ADCs, which are safer and more potent (due to a non-cleavable linker) than older-generation ADCs, which had significant side effects. Despite the side effects, big pharma has spent billions of dollars in acquiring ADC oncology companies ($43 billion acquisition of Seattle Genetics, $21 billion acquisition of Immunomedics).

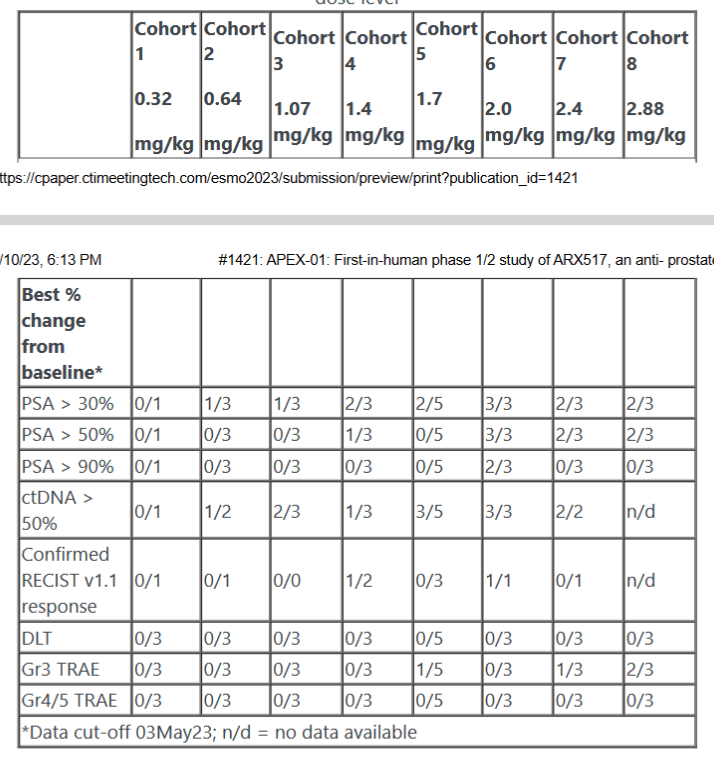

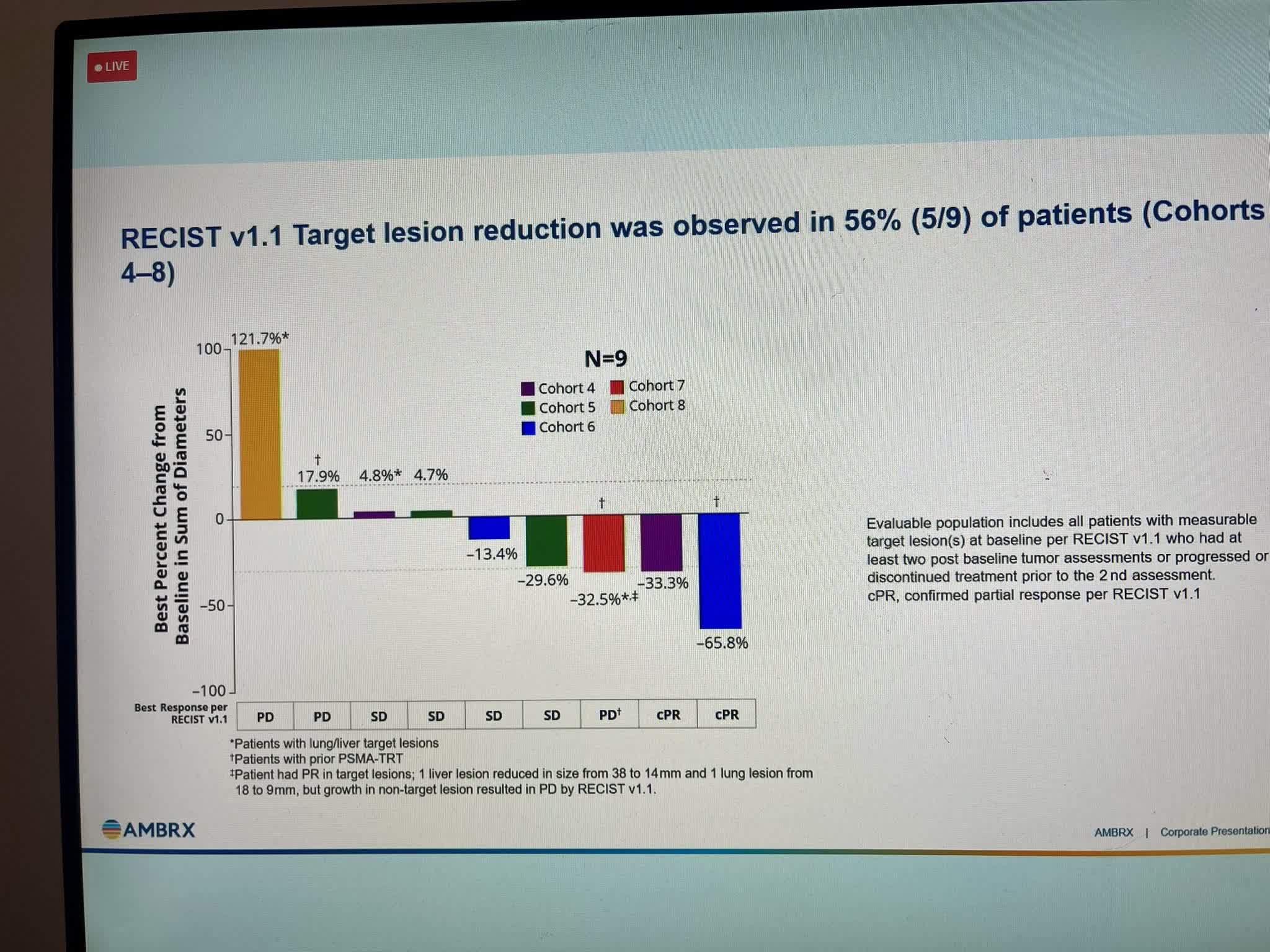

ARX517, a next-generation prostate-specific membrane antigen, PSMA-targeted ADC candidate, has shown safety benefits that were not present in earlier-generation ADCs (due to conjugation to a tubulin linker) and has Fast Track designation. Phase 2 data released at ESMO abstracts (in 24 patients with mCRCPC with >= two prior lines of therapy) is summarized in the table below:

{kind=link}

I listened to the company's KOL call this weekend at the ESMO, where the above data was discussed in detail. Notable is the fact that in Pluvicto-resistant patients, 2 out of 3 patients (65%) achieved a partial response (defined as >=30% tumor shrinkage).

Tumor shrinkage sen with ARX517. 2 out of 3 patients resistant to Pluvicto (Lum-PSMA) showed a partial response (OR = 65%) (KOL call at ESMO)

{kind=link}

The side effects were mild, like thrombocytopenia (transient) and leukopenia, and lower than that shown by Pluvicto (it has a very high incidence of hematological toxicity). The management is conducting further dose escalation, which may help to improve the efficacy further. Please note that these were dying patients who had exhausted all current treatment options, including Pluvicto, and ARX517 helped to shrink their tumors. Mild side effects seen in the study are easily manageable. Only 2 out of 54 patients discontinued the treatment due to side effects. PSA response (which was seen in these patients) correlates with survival benefit, so I expect ARX517 to show survival improvement as well (I expect the company to provide the survival data next year, likely at the ASCO conference in the summer).

Dr. John Shen, a medical oncologist at UCLA and an investigator on APEX-01, stated :

"The PSA results are very encouraging, especially in this heavily pre-treated patient population where eligible patients would have exhausted all available and appropriate treatment options prior to enrolling in this study."

I also looked at ESSA Pharma (EPIX) mCRPC data from ESMO. There is no monotherapy data (the data is in combination with Xtandi), so it is difficult to draw conclusions (remember NKTR). The FDA is also likely to raise questions over the lack of monotherapy data for (EPIX). AARX517 has shown monotherapy efficacy in >= four prior lines of therapy (including in Pluvicto-resistant patients), so I prefer to invest in it.

Pluvicto data was also released at ESMO. However, ARX517 is much safer than Pluvicto and has shown efficacy in patients who have even failed treatment with Pluvicto. There is a clear target market for ARX517 in refractory mCRPC.

Just ARX788, a late-stage metastatic breast cancer ADC candidate, is enough to justify a potential 4x upside in AMAM stock

Human epidermal growth factor, HER2 is expressed in ~20% of breast cancers. Approximately 5% of women diagnosed with breast cancer have metastatic disease at the time of diagnosis. HER2 targeting therapies in mBC had annual sales of $10 billion in 2020. AstraZeneca's (AZN) ADC drug, Enhertu, containing topoisomerase-1 payload (Breakthrough therapy designation) has a peak global sales estimate of ~$10 billion/year by 2028. A treatment algorithm for this cancer is given below:

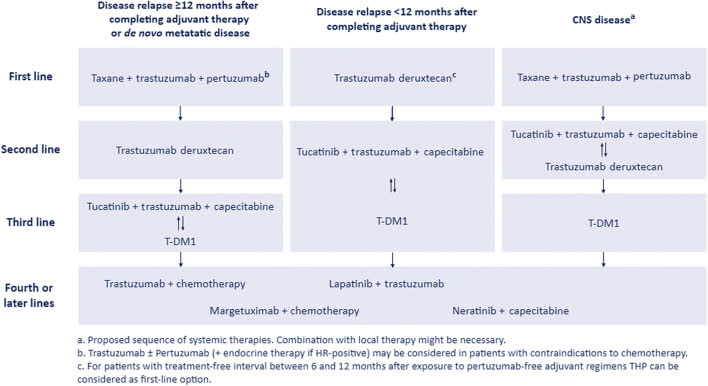

A treatment algorithm for metastatic HER2+ breast cancer (Nader-Marta et al., ESMO Open 2022; 7(10): 100343.))

{kind=link}

ARX788, a next-generation ADC (anti-tubulin cytotoxic payload, AS269), has an FDA Fast track designation in treating HER2+ metastatic breast cancer, mBC. It showed proof of concept in a U.S./Australia-based PanTumor-01 study (n=3) where antitumor activity was seen in post-Enhertu patients (ORR of 67%, and disease control rate of 100% at 1.5 mg/kg dose). The objective response rate, ORR, in highly refractory patients with prior HER2+ targeted therapies like monoclonal antibodies, ADCs, and bispecific antibodies ranged from 65%-80%, higher than approved therapies.

In a pivotal study , ACE-Breast-02 trial (n=441) for the China market, it showed a progression-free survival, PFS of 17.02 months (higher than the control arm, lapatinib+cepcitabine) in highly refractory patients (n=69) (Breast-02), which was stopped earlier as the efficacy was reached. The side effects were significantly lower than Enhertu. The company's partner for China NovoCodex is planning to submit an approval application to the China FDA.

Data from a global Phase 2 randomized controlled study (ACE-BREAST-03) in this indication is expected at the annual San Antonio Breast Cancer Symposium, SABCS from December 5-9 this year, another near-term catalyst. The study has a treatment duration of 2 years (vs. four years for Enhertu). The primary endpoint is ORR. Survival endpoints like PFS and overall survival, OS are secondary endpoints. Based on the previous clinical data, this study has a high probability of showing a successful result. Due to a lower side effect profile and probable higher efficacy (due to a non-cleavable linker) than Enhertu, ARX788 has a shot at gaining market share in this large target market.

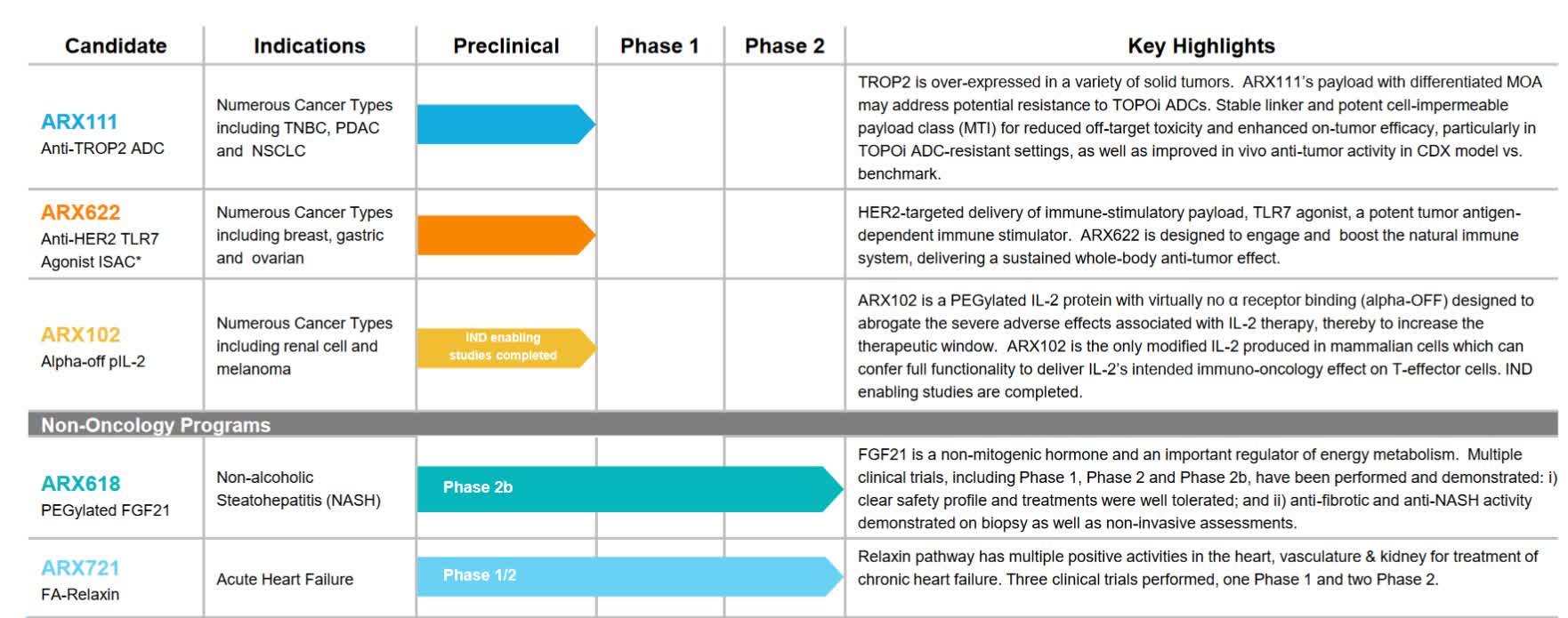

The company has a partnership with BeiGene (BGNE) for multiple projects. It is also developing Bio-conjugates for Animal Health. Another ADC program is ARX-305, anti-CD70 ADC (the only anti-CD70 in development to target CD70 expressed in several solid and hematological tumors), which is in a Phase 1 trial. It is licensed to NovoCodex for the China market.

The CEO, O'Conner, served as the CEO of two immuno-oncology companies, Advaxis (ADXS) and Oncosec (ONCS). He also co-founded Larkspur Health, which merged with Zyversa Therapeutics. He also served as a Senior Vice President of ImClone.

{kind=link}

The company's stock is a good Buy on the dip and a potential acquisition candidate

Cash reserves are estimated at $235 million and are enough till 2026. There is no long-term debt.

Valuation:

ARX517 in mCRPC:

Using input average wholesale price, AWP price of $250,000/year (similar to Lu-PSMA), average sales price, ASP=185,000, annual ASP price increase of 3%, target market - 34,700 (U.S.), probability = 65%, peak market share = 25%, U.S. launch in 2027, I modeled peak $1.2 billion/year peak U.S. risk-adjusted revenue in 2032. For the E.U. market, I input ASP=50% of U.S. ASP, target market= 35,000, and probability of 65%. Using these inputs, I modeled $628M/year of peak risk-adjusted E.U. revenue. Please note that I have modeled only 25% market share conservatively, though I expect ARX517 to gain >50% market share based on the ESMO data.

ARX788 in HER2+ mBC:

My input for the U.S. market was: AWP=230K/year (same as Enhertu), ASP=170,200/year, annual ASP increase = 3%, target U.S. market = 15,500, peak market share = 25%, probability of 75%, U.S. launch in 2025 (modeling peak risk-adjusted U.S. revenue of $574M in 2030). For the E.U. market, I used ASP=50% of the U.S. market, target market=15,000, peak market share of 25%, probability of 75%, launch in 2026, modeling peak risk-adjusted revenue of $286M in 2031. For the China market (licensed to NovoCodex), I input ASP = 25% of U.S. ASP, target market = 65K, and other assumptions same as E.U. market, modeling peak risk-adjusted revenue of $56.5M for NovoCodex and peak risk-adjusted royalty revenue of $9M for Ambrx.

The above estimates are in line with the guidelines from the Pharmagellen guide for biotech valuation.

| Product candidate |

| Markets |

| Peak risk-adjusted revenue |

| ARX517 in highly refractory mCRPC |

| U.S., E.U. |

| $1.9 billion (2033), $3B |

| ARX788 in HER2+ mBC |

| U.S., E.U., China |

| $950 million (2031) |

After discounting (discount rate of 15%, decreasing to 10% at maturity), I calculated the value of operations = $1.47 billion. After adjusting for the assets and liabilities, and using the diluted share count, my estimate for the fair value per share is $28.

Please feel free to use your own inputs in the above model and test out your assumptions.

Sell-side targets after ESMO data:

- Median PT = $22 (range = $15 to $26 from 3 analysts)

- JMP Securities= $15

- B. Riley Financial = $26

- BTIG = $26

Institutional holders include Cormorant Asset Management (17% stake), Venrock (10% stake), and Adage (2.6% stake). After the ESMO data, Cormorant Asset Management added 2.15 million shares to its stake.

Catalysts

- Phase 3 data for ARX788 in mBC at the SABCC conference in early December.

- China approval and launch for ARX788 in HER2+ mBC expected in 2024.

- Interim survival data from Phase 2 study of ARX517 in refractory mCRPC at ASCO conference in June 2024.

In conclusion, AMAM stock is undervalued, and the dip in the stock price is a good buying opportunity.

Rating Ambrx Biopharma Inc. Buy with a price target of $28 (210% upside). AMAM stock is also an attractive acquisition candidate.

Disclaimer:

Risks in this investment include underwhelming data, unexpected side effects, unfavorable FDA decision, further capital raise resulting in dilution, increasing competition from new entrants, etc., which may cause the stock price to fall.

For further details see:

Ambrx: Next-Generation Antibody-Drug Conjugates, Buying The Dip After ESMO Data