AMX - America Movil: Triumph In Restructuring

2023-07-07 09:48:35 ET

Summary

- América Móvil recently completed a successful restructuring, resulting in increased profitability and operating margins.

- The restructuring plan included selling underperforming businesses and spinning off passive assets.

- América Móvil is now well positioned to compete against its rivals, as LILA and Millicom are still undergoing restructuring.

- Furthermore, América Móvil has the potential to expand further in Brazil, which contributed to its strong performance in Q1.

- Based on my assessment, I recommend a "buy" rating on AMX, as I believe it has a promising medium-term outlook.

Thesis

América Móvil, S.A.B. de C.V. ( AMX ) has successfully completed its restructuring phase, with improved free cash flow and operating margins. This positions América Móvil favorably to seize market share, compete, and expand while keeping its competitors at bay. By default, the Latin American telecoms market is expected to grow at a CAGR of 4.40%. I have projected this growth onto América Móvil's revenue for the future (2023-2028). Based on this valuation, the stock price is estimated to be $29.09, representing a 35.5% increase from the current price of $21.46. Furthermore, projecting the DCF implied stock price of $29.09 into 2028 suggests a target price of $51.30, indicating a substantial upside of 139% over a six-year period and an annual return of 23%.

Overview

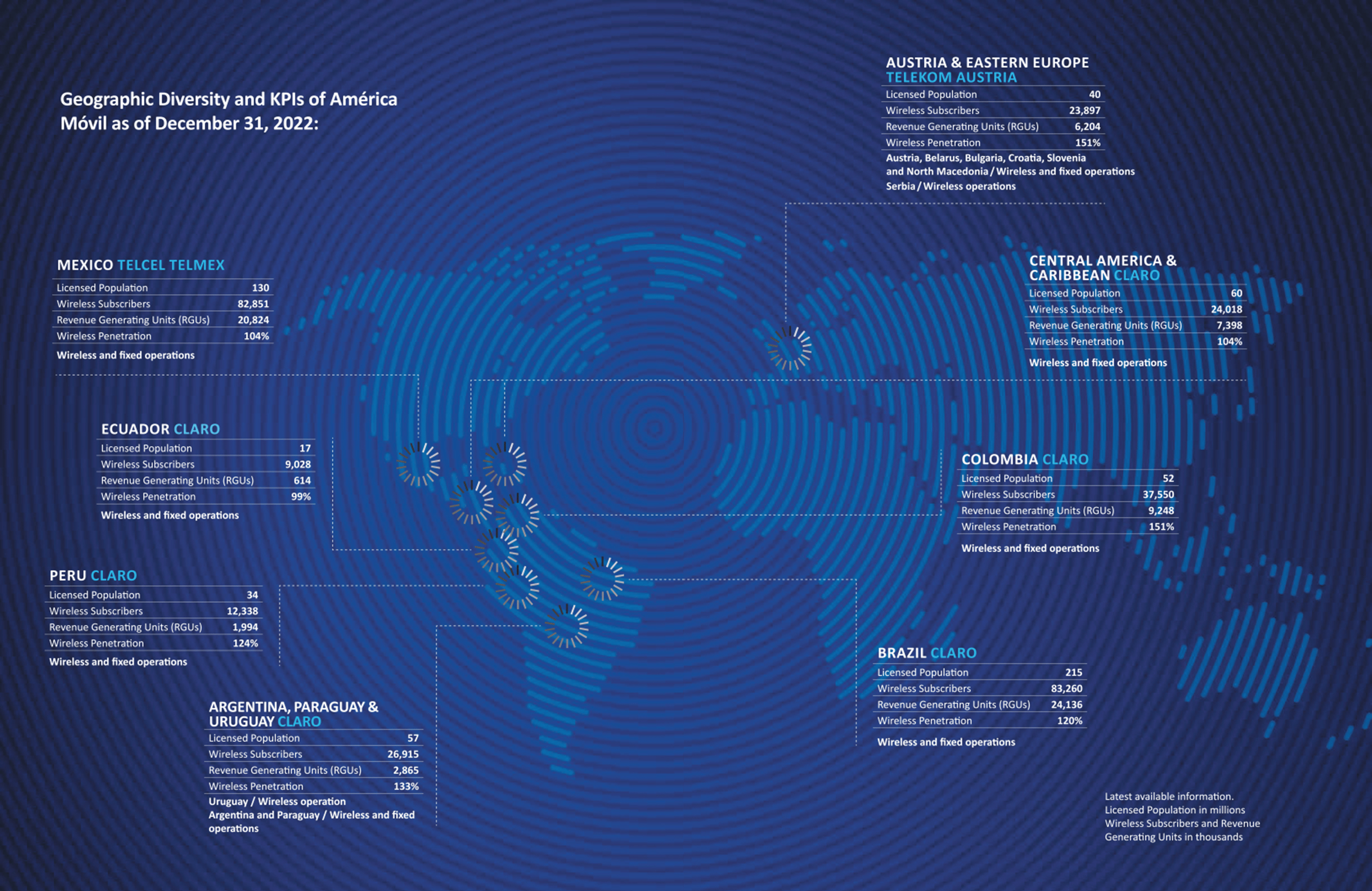

América Móvil is a leading Latin American telecommunications company with fixed operations that generated $15.1 billion in revenues in 2022, representing 30.6% of their total consolidated revenues. They provide a range of services including fixed voice, data centers, administration, and hosting. Residential broadband access is available through fiber-optic or hybrid fiber-coaxial cables. Their subsidiaries offer IT solutions, Pay TV services, and popular OTT services like ClaroVideo for on-demand streaming. With bundled packages and ClaroMúsica, an unlimited music streaming service in 15 countries, they cater to diverse customer needs. Notably, Mexico and Brazil serve as their primary markets, housing around half of their revenue-generating units.

The company recently underwent a corporate restructuring that followed a similar plan as Millicom International Cellular, S.A. ( TIGO ), involving a spin-off of passive assets, specifically telecommunication towers (a process that concluded on August 8, 2022), outside of Mexico, except for those in Colombia, Peru, and the Dominican Republic.

In addition to the spin-off of passive assets, América Móvil also restructured its business portfolio. This included the sale of TracFone to Verizon Communications, Inc. ( VZ ), the acquisition of Oi Group's mobile operation in Brazil, the sale of Claro Panama to Liberty Latin America, Ltd. ( LILA ), and a joint venture with LILA in Chile, merging their operations in a 50:50 joint venture. These events took place between 2020 and 2022, marking a period filled with accomplishments for América Móvil.

In Latin America, there is still significant work to be done regarding the adoption of 5G . The interest of governments and companies in this technology has led governments to be willing to assist the private sector in its adoption. It is projected that 5G subscriptions will increase from the current 19 million to 49 million. Additionally, fiber infrastructure is not yet widely available, but it is estimated to reach a 75% share by 2027.

The projections for 2025 indicate that the revenue of the Latin American telecom sector will reach $73.6 billion, representing a growth of 4.4% compared to the $65 billion in 2022.

América Móvil has extensive operations in Latin America and also operates in Eastern Europe through a joint venture with Telekom Austria. Currently, they hold a strong position as a major telecom player in Latin America, particularly considering the ongoing restructuring of competitors such as Millicom, LILA, and Telefonica, S.A. ( TEF ). Their primary competitor in Mexico is AT&T, Inc. ( T ).

Markets in which America Movil operates (2022 Annual Report)

{kind=link}

Currently, they are the best positioned major telecom player in Latin America, since Millicom is in the process of restructuring, as well as LILA, who was in a relatively bad shape compared to Millicom. The only formidable competitors are AT&T in Mexico, and Telefonica.

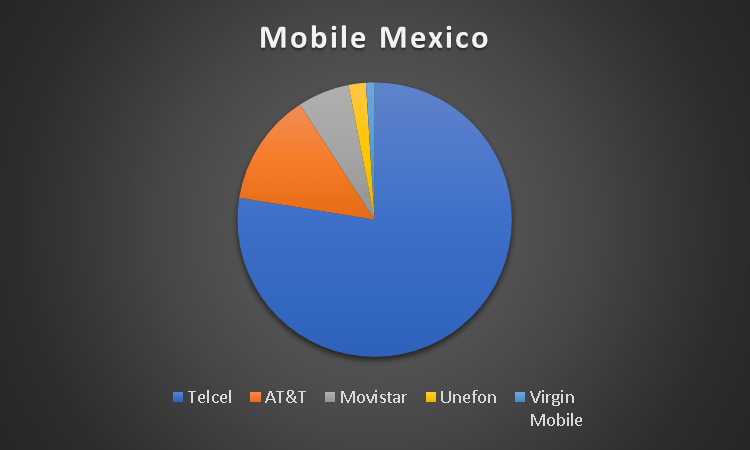

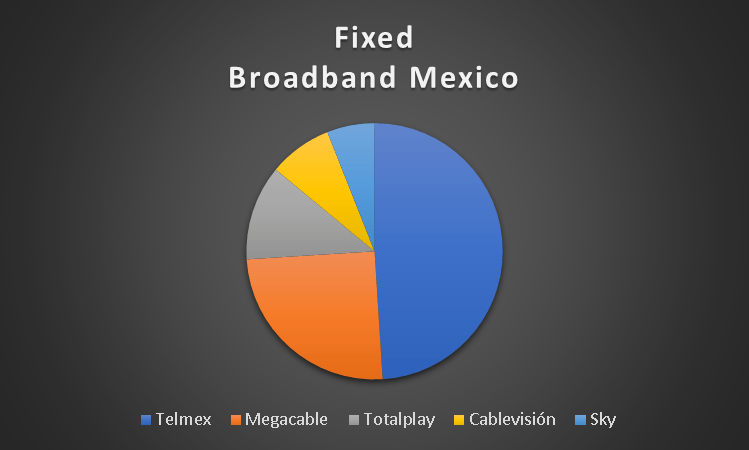

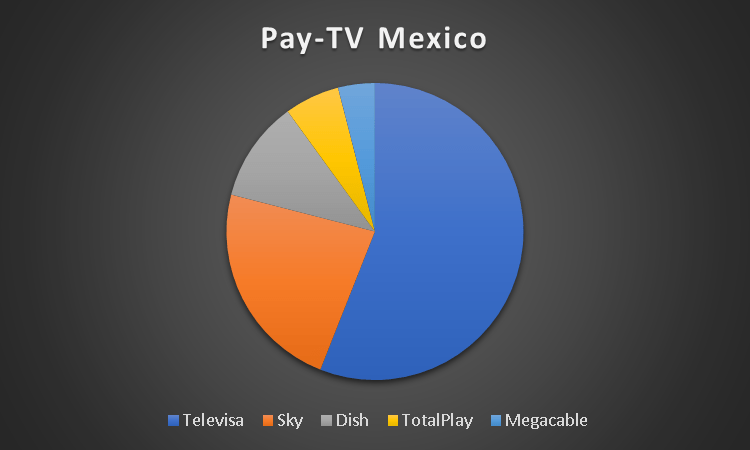

As mentioned earlier, Mexico and Brazil are their most significant markets, together accounting for half of their revenue-generating units [RGUs]. In Mexico, América Móvil holds a 76% market share in mobile and a 49% market share in fixed broadband. However, their market share in Pay-TV is minimal due to Televisa's dominance, with a 56.6% market share. Televisa, being the producer of numerous shows and owner of multiple channels, poses significant entry barriers, allowing them to potentially restrict access to their channels for any serious competitor. Consequently, growth opportunities in Mexico are limited, and América Móvil's focus lies in maintaining its market share through exceptional service.

Mobile Competitors in Mexico (Author's Calculations with base on Staatista) Fixed-Broadband competitors in Mexico (Author's Calculations with base on Staatista) Pay-TV Competitors in Mexico (Author's Calculations with base on Staatista)

{kind=link}

{kind=link}

{kind=link}

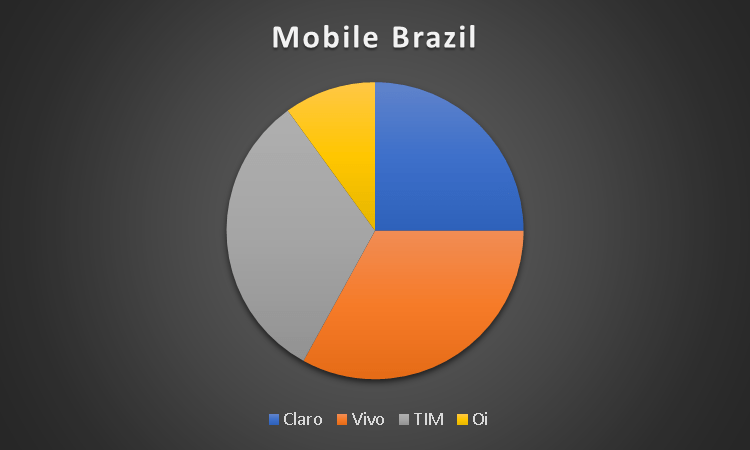

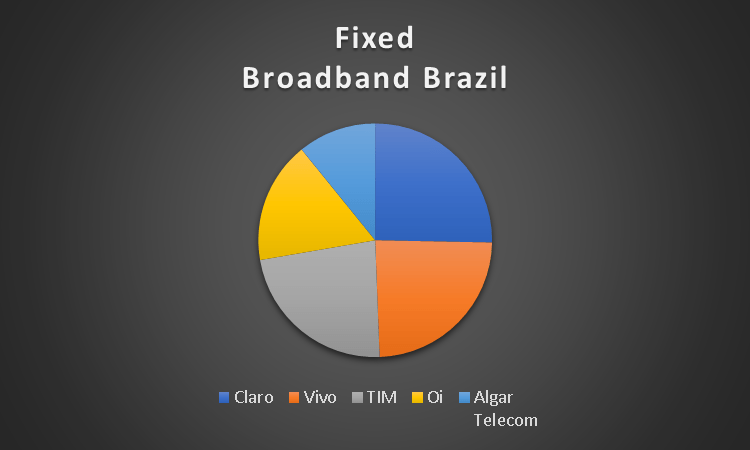

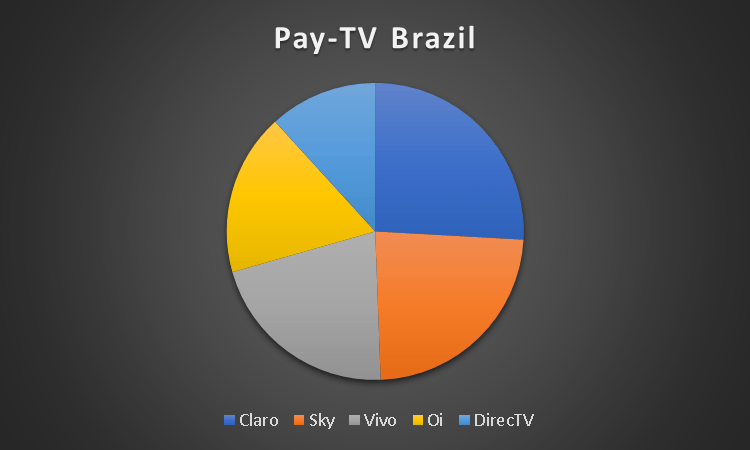

Brazil has been a promising market for América Móvil, with notable growth. In Brazil, Claro, their subsidiary, leads the market in Pay-TV and fixed broadband, but not in the mobile segment where their market share is nearly equal to that of their competitors' Vivo and TIM, since, as previously said, Oi's operations were bought by América Móvil.

Mobile Competitors in Brazil (Author's Calculation with base on Staatista) Fixed-Broadband competitors in Brazil (Author's Calculation with base on Staatista) Pay-TV Competitors in Brazil (Fixed-Broadband competitors in Brazil)

{kind=link}

{kind=link}

{kind=link}

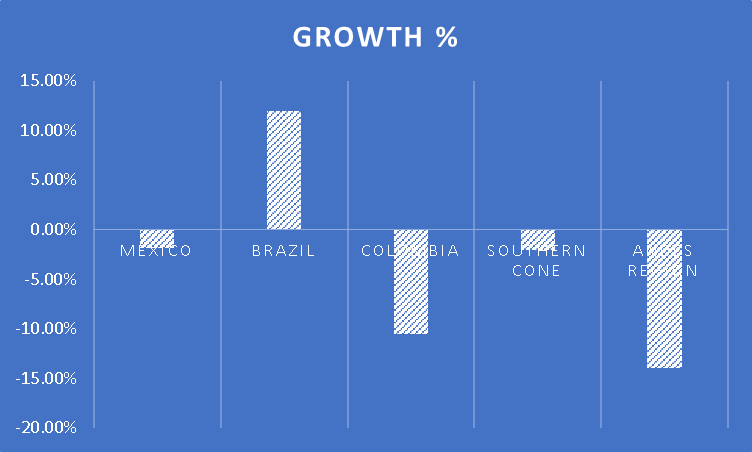

In Central America, América Móvil faces challenges with LILA and Millicom, the two major players in the region. This might explain their decision to sell Claro Panama to LILA. It is evident that growth discrepancies exist among their markets, with Brazil showing strong growth while other markets experienced negative revenue growth. Notably, Colombia and the Andes region have been particularly affected, possibly due to competition from Millicom (only in Colombia) and Telefónica (in Colombia and the Andes), respectively. In Colombia, both Telefónica and Claro are under government investigation for denying number portability to their users .

Growth in the different markets (2022 Annual Report)

{kind=link}

Considering the current landscape, it is likely that América Móvil will emerge as the winner in this competitive scenario. Millicom and LILA are still undergoing restructuring, and LILA specifically faces negative net income. Meanwhile, Telefónica is the only significant competitor in Latin America, except in Mexico where AT&T poses a serious threat. From a financial standpoint, América Móvil appears to be in the strongest position, while Telefónica has been plagued in the past by bureaucracy and poor financial decisions. For instance, their ill-advised overpayment for O2, followed by an attempted sale at a loss , which was vetoed by the EU. If the sale had proceeded, it would have resulted in a loss of EUR 12.5 billion ($13.6 billion).

Financials (In millions of USD unless Stated Otherwise)

In my opinion, América Móvil is currently experiencing one of its most prosperous periods. Profit margins have improved, and free cash flow has strengthened. Additionally, the company's debt is on a downward trajectory.

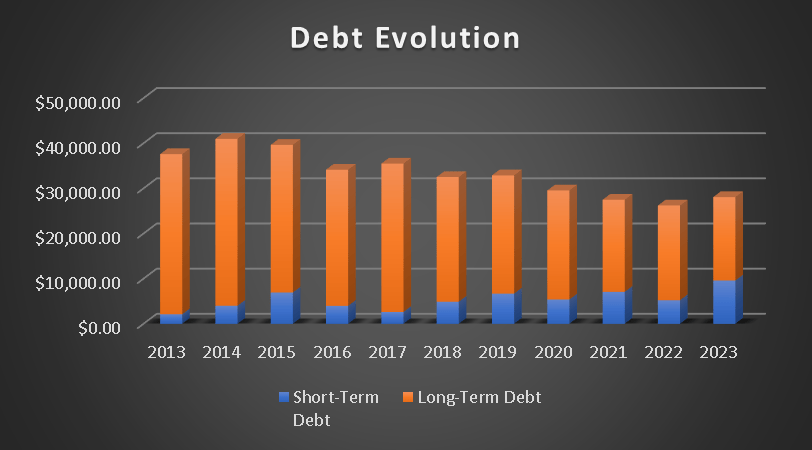

Since 2014, América Móvil has been steadily reducing its long-term debt. Back then, it stood at $36 billion, but now it has been reduced to approximately $18 billion. However, during the same period, short-term debt has increased from $4 billion to $9 billion. Nevertheless, the overall debt has been decreasing at an annual rate of 3.15% since 2014.

Debt Evolution (Author's Calculation)

{kind=link}

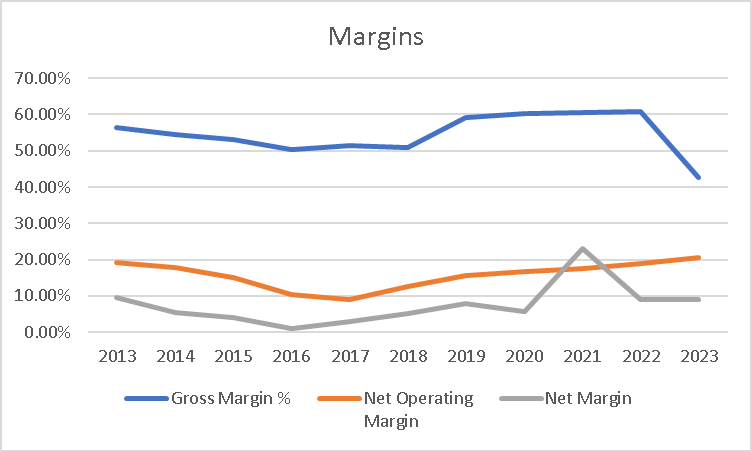

As mentioned earlier, América Móvil has reached near all-time high margins, with the exception of the gross margin, and net income margin. In the graph below, you can observe that the net operating margin has reached 20.61%, which is the highest it has been since 2013. However, the gross margin currently stands at 42.48%, a decrease from the 60.88% recorded in 2022.

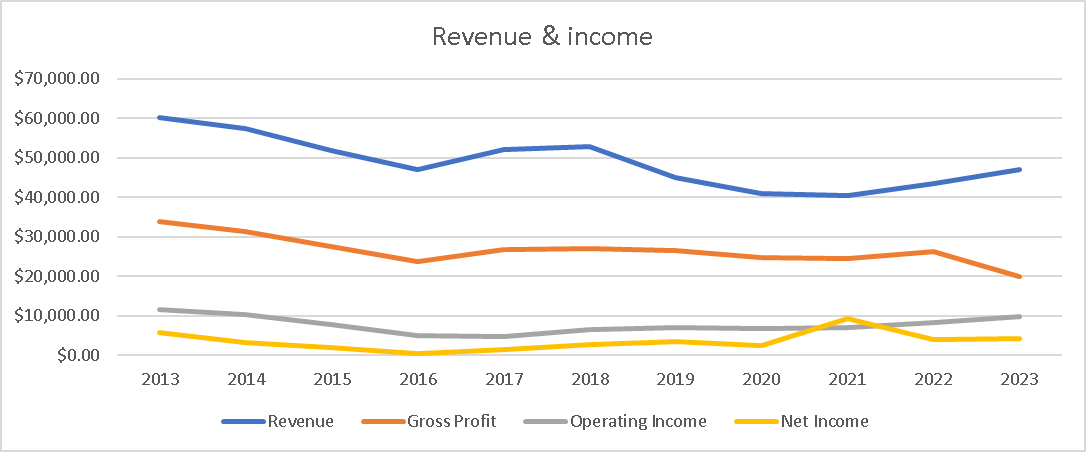

When analyzing the company's revenue evolution, we notice a decline of $13 billion since 2013. It is important to consider that this decrease in revenue may be attributed to América Móvil's strategic decision to sell underperforming units. As previously mentioned, their net margin has reached an all-time high of 20.61%. This indicates that the company has become more efficient over the years.

Revenue & Income (Author's Calculations)

{kind=link}

| Revenue |

| Gross Profit |

| Operating Income |

| Net Income |

| 2013 |

| $60,065.00 |

| $33,819.30 |

| $11,520.00 |

| 5702 |

| 2014 |

| $57,486.00 |

| $31,289.00 |

| $10,291.60 |

| 3126.1 |

| 2015 |

| $51,875.50 |

| $27,482.00 |

| $7,884.50 |

| 2034.7 |

| 2016 |

| $47,056.60 |

| $23,655.90 |

| $4,884.50 |

| 417.3 |

| 2017 |

| $51,961.10 |

| $26,717.10 |

| $4,657.10 |

| 1491.5 |

| 2018 |

| $52,836.30 |

| $26,941.40 |

| $6,628.80 |

| 2675.2 |

| 2019 |

| $45,034.90 |

| $26,588.10 |

| $7,010.10 |

| 3582.3 |

| 2020 |

| $41,005.30 |

| $24,738.50 |

| $6,837.50 |

| 2356.2 |

| 2021 |

| $40,479.30 |

| $24,471.00 |

| $7,130.70 |

| 9376.8 |

| 2022 |

| $43,335.30 |

| $26,374.20 |

| $8,181.10 |

| 3908.1 |

| 2023 |

| $47,049.00 |

| $20,034.80 |

| $9,698.00 |

| 4189.7 |

Margins (Author's Calculations)

{kind=link}

| Gross Margin % |

| Net Operating Margin |

| Net Margin |

| 2013 |

| 56.30% |

| 19.18% |

| 9.49% |

| 2014 |

| 54.43% |

| 17.90% |

| 5.44% |

| 2015 |

| 52.98% |

| 15.20% |

| 3.92% |

| 2016 |

| 50.27% |

| 10.38% |

| 0.89% |

| 2017 |

| 51.42% |

| 8.96% |

| 2.87% |

| 2018 |

| 50.99% |

| 12.55% |

| 5.06% |

| 2019 |

| 59.04% |

| 15.57% |

| 7.95% |

| 2020 |

| 60.33% |

| 16.67% |

| 5.75% |

| 2021 |

| 60.45% |

| 17.62% |

| 23.16% |

| 2022 |

| 60.86% |

| 18.88% |

| 9.02% |

| 2023 |

| 42.58% |

| 20.61% |

| 8.90% |

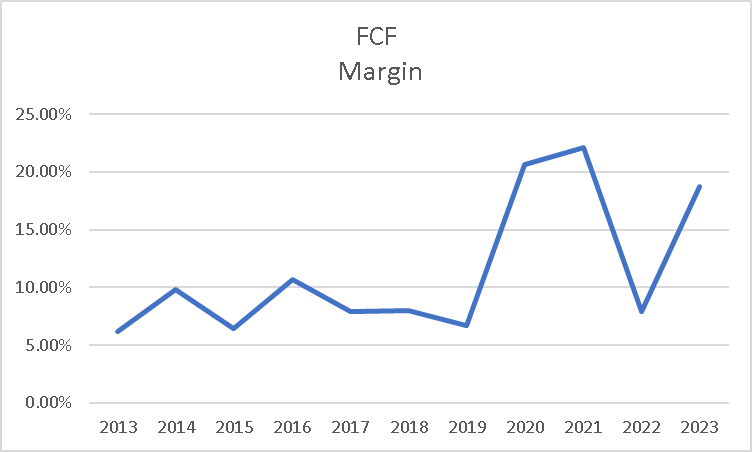

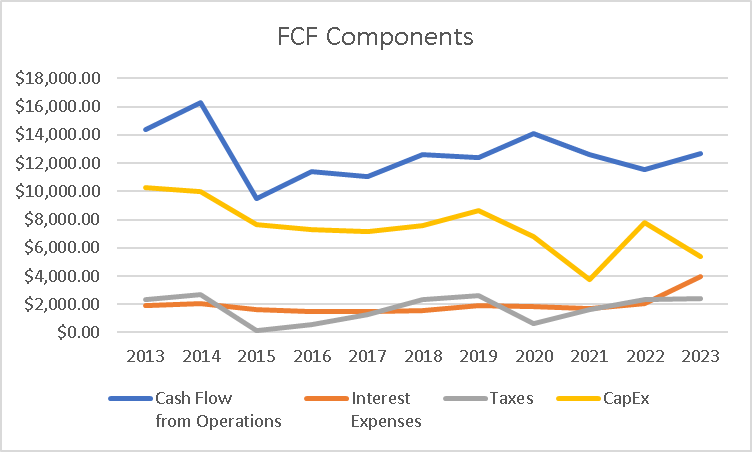

Another aspect that is at its all-time high is free cash flow, which currently sits at $8.8 billion, which is a 138% improvement from 2013's $3.7 billion. Its FCF margin is also good, currently it is at 18.7%, which is slightly less than 2021's 22.08%.

Free Cash Flow Margin (Author's Calculations) Free Cash Flow Components (Author's Calculations)

{kind=link}

{kind=link}

As depicted in the graph above, the improvement in free cash flow can be attributed primarily to a reduction in capital expenditures. In 2013, capital expenditures amounted to $10.2 billion, whereas in the current period, they stand at $5.3 billion, representing a significant 50% decrease. Interestingly, despite the company's debt being at an all-time low, the interest expenses have reached an all-time high, indicating a potentially higher cost of debt.

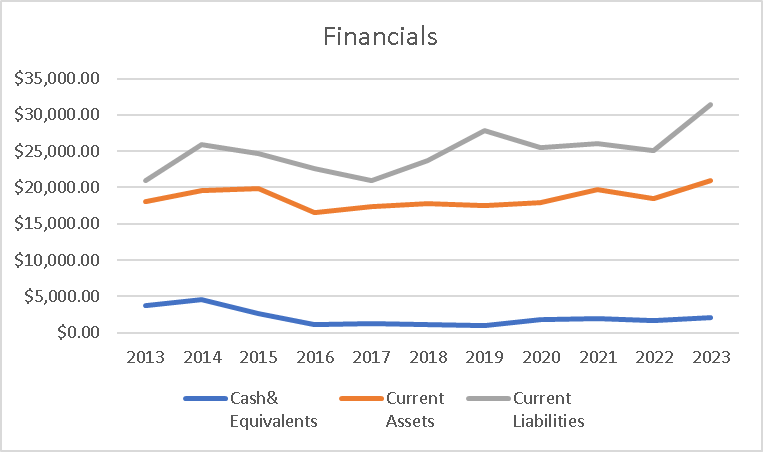

Moving on to the balance sheet, the notable observation is the climb in current liabilities, which is primarily a result of the increase in short-term debt. However, aside from that, the cash balance has remained relatively stable since 2016, with the current standing at $2 billion. Overall, there are no significant highlights on the balance sheet apart from the debt ratios.

Financials (Author's Calculations)

{kind=link}

As mentioned earlier, América Móvil has already undergone restructuring, and upon examining the financials section, you will notice that despite the decline in revenue, net income has remained steady while the net margin has improved. Furthermore, both free cash flow and the FCF margin have reached all-time highs, all of which have been achieved alongside a reduction in debt.

Valuation (In millions of USD Unless Stated Otherwise)

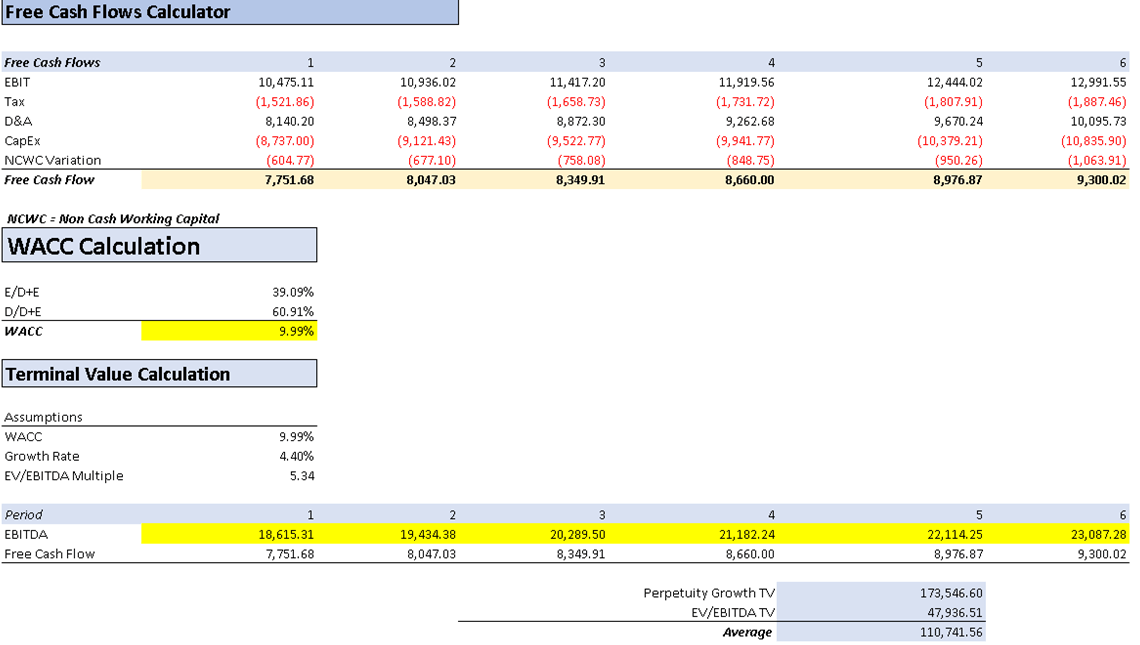

To value América Móvil, I will utilize a discounted cash flow [DCF] model that considers the Latin American telecoms market projected revenue growth rate of 4.40% annually. Additionally, I need to factor in the capital expenditures, which the company anticipates returning to 2019 levels. During that time, América Móvil allocated 18% of its revenue towards capital expenditures, resulting in expenses of $8.6 billion, significantly higher than the current $5.3 billion.

The first step in the valuation process is to project the 4.40% growth on América Móvil's revenue. This projection can be represented as follows:

| Revenue |

| 2023 |

| 47,049 |

| 2024 |

| 49,119 |

| 2025 |

| 51,280 |

| 2026 |

| 53,537 |

| 2027 |

| 55,892 |

| 2028 |

| 58,352 |

Next, I will calculate the net income after taxes, utilizing the net income margin of 8.90%.

| Revenue |

| Net Income |

| 2023 |

| $47,049.00 |

| $4,187.36 |

| 2024 |

| $49,119.16 |

| $4,371.60 |

| 2025 |

| $51,280.40 |

| $4,563.96 |

| 2026 |

| $53,536.74 |

| $4,764.77 |

| 2027 |

| $55,892.35 |

| $4,974.42 |

| 2028 |

| $58,351.62 |

| $5,193.29 |

Next, I will calculate the taxes by utilizing a tax rate based on revenue, as it provides simplicity. This tax rate will be set at 5% of revenues. I derived this tax rate by dividing the income tax expenses by the revenue.

Furthermore, I will determine the depreciation and amortization (D&A) expenses and interest expenses, again relating them to revenue. By performing the same division, D&A/Revenue and Interest/Revenue, I obtained a D&A margin of 17.30% and an interest expense margin of 8.36%.

| D&A Projection |

| Interest Projection |

| 2023 |

| 8,140.200 |

| 3,935.30 |

| 2024 |

| 8,498.369 |

| 4,108.45 |

| 2025 |

| 8,872.297 |

| 4,289.23 |

| 2026 |

| 9,262.678 |

| 4,477.95 |

| 2027 |

| 9,670.236 |

| 4,674.98 |

| 2028 |

| 10,095.726 |

| 4,880.68 |

| Revenue |

| Net Income |

| Plus Taxes |

| Plus D&A |

| Plus Interest |

| 2023 |

| $47,049.00 |

| $4,187.36 |

| $6,539.81 |

| $14,680.01 |

| $18,615.31 |

| 2024 |

| $49,119.16 |

| $4,371.60 |

| $6,827.56 |

| $15,325.93 |

| $19,434.38 |

| 2025 |

| $51,280.40 |

| $4,563.96 |

| $7,127.98 |

| $16,000.27 |

| $20,289.50 |

| 2026 |

| $53,536.74 |

| $4,764.77 |

| $7,441.61 |

| $16,704.28 |

| $21,182.24 |

| 2027 |

| $55,892.35 |

| $4,974.42 |

| $7,769.04 |

| $17,439.27 |

| $22,114.25 |

| 2028 |

| $58,351.62 |

| $5,193.29 |

| $8,110.87 |

| $18,206.60 |

| $23,087.28 |

| ^Final EBITA^ |

As shown in the table above, these are the projected EBITDAS for the next six years. Following this, I will fill the assumptions table, which you can also find below, along with the complete DCF model:

Table of Assumptions (Author's Calculations) DCF part 1 (Author's Calculations) DCF part 2 (Author's Calculations)

{kind=link}

{kind=link}

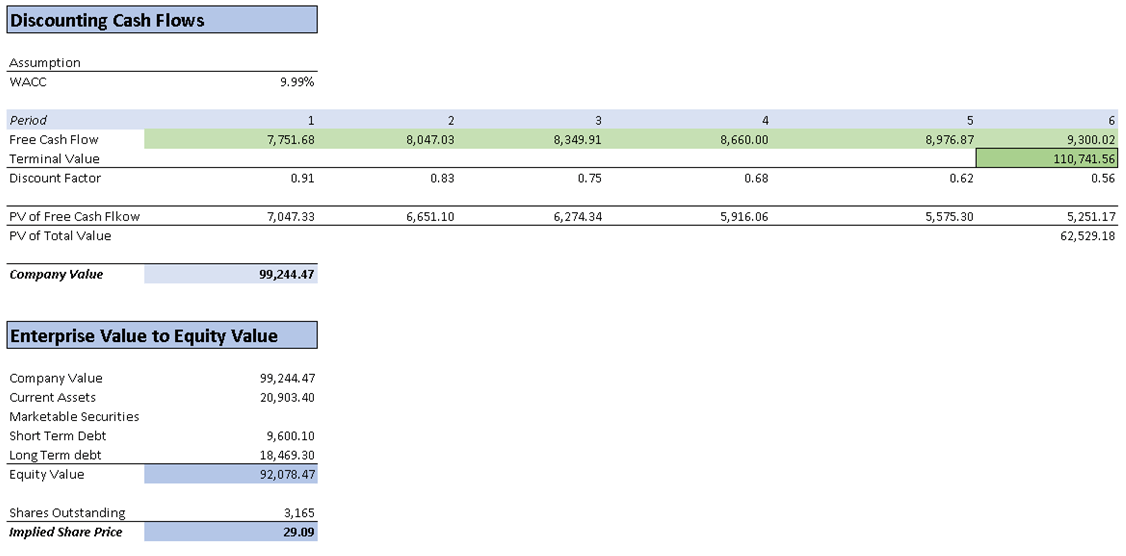

The DCF model indicates a stock price of $29.09, representing a 35.5% upside from the current price of $21.46. However, considering the current market sentiment, it may be advisable to wait for a better entry point, as the sentiment may not be conducive to supporting a significant increase in the stock price.

Additionally, projecting the DCF implied stock price of $29.09 into 2028 suggests a target price of $51.30. This implies a substantial upside of 139% over a six-year period, resulting in an annual return of 23%.

While I have set a target of $51.30 for 2028, with a medium-long term investment horizon, it is important to note that achieving this target would require favorable market sentiment. As a medium-long term investor, I am inclined to tolerate short-term risks. However, for short-term investors, it may be preferable to adopt a "hold" strategy. Regardless, given my investment horizon, I would assign a "buy" rating.

Risks to Thesis

As deduced, the primary risk to my thesis is competition. If rivals such as Millicom and LILA successfully complete their restructuring, they will emerge as formidable competitors to América Móvil in Colombia and Central America. Furthermore, Telefonica poses a significant threat primarily in Brazil, the market that has recently fueled the company's strong Q1 earnings performance. Additionally, there is the risk of currency devaluation in Latin American countries, as the region tends to exhibit higher volatility due to political decisions.

Currently, I perceive minimal business risks, as América Móvil has successfully concluded its restructuring process, resulting in improved margins and, most notably, stronger free cash flow, surpassing even that of Telefonica. This provides América Móvil with a competitive advantage over its rivals. However, there remains a risk of potential setbacks if an acquisition does not unfold as planned, which could potentially leave the company in a situation reminiscent of Telefonica's challenges from a few years ago. For instance, difficulties arising from an unsuccessful expansion into Eastern Europe.

Overall, I believe that América Móvil faces few risks in the medium term. However, in the short term, it is worth noting that the stock price may struggle to deliver returns without a catalyst. Even if the company surpasses market expectations in its upcoming earnings report on July 11, a positive market sentiment is necessary, which may not be the prevailing situation at present.

Conclusion

In conclusion, América Móvil, a leading Latin American telecommunications company, has been experiencing positive developments in recent years. The company has undergone a successful restructuring process, resulting in improved margins and strengthened free cash flow. Despite facing competition from rivals like Millicom, LILA, and Telefonica, América Móvil has positioned itself favorably in key markets such as Mexico and Brazil.

Investors should consider the medium to long-term potential of América Móvil, recognizing that short-term market sentiment may impact stock performance. Furthermore, the company's disciplined approach to acquisitions and its ability to execute successful expansion strategies will be critical factors in its future success.

Overall, with improved financials, a solid market presence, and a focus on growth, América Móvil appears well-positioned to capitalize on opportunities in the Latin American telecommunications sector.

For further details see:

America Movil: Triumph In Restructuring