AMX - America Movil: Unchallenging Valuation Capex Discipline And A Strong Peso Drive Shares

2023-03-11 03:30:28 ET

Summary

- Unchallenging valuation at 5.0x EV/EBITDA.

- Capex stability provides higher free cash flow.

- The stock is defensive while 5G rollout may accelerate EBITDA growth.

Summary

America Movil (AMX) has executed capex discipline while growing revenue and margins in a competitive environment. The stock, along with the global telecom sector, has derated as mobile became a commodity data infrastructure provider for the internet ecosystem i.e. dumb pipes. After near a decade of underperformance, AMX is now a good risk adjusted stock with a low valuation, rising free cash flow and dividends. The 5G rollout adds upside surprise when and if the LatAm internet ecosystem's increases the internet of things adoption.

History

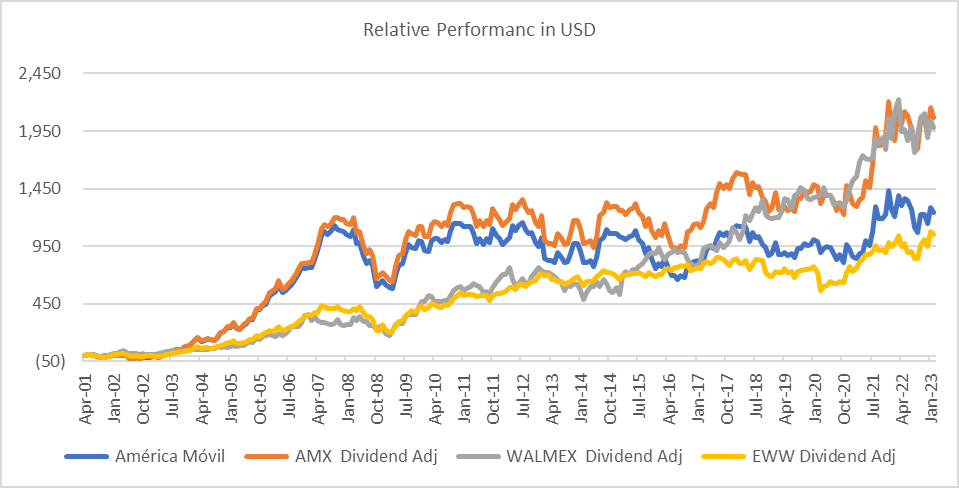

AMX went public in 2001 as a spin-off from Telmex; it initially greatly outperformed the Mexico Market up to 2010. However, it stagnated up to 2017 when it began to offset the Mexico anti-monopoly regulations. In addition, its expansion across Latin America, US and Europe via M&A stressed the balance sheet and ROIC as many assets were underperforming under competitive scenarios. Recent strength has come from a stronger MXN, RGU (revenue generating units) growth, capex discipline and increased dividend/buybacks.

AMX vs Mexico Market Performance (Created by author, data by Capital IQ)

{kind=link}

Capex Discipline

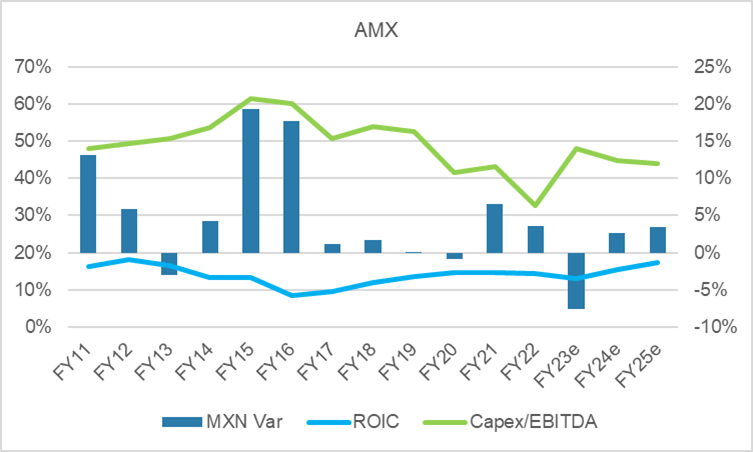

The Mexican peso devaluation and most LatAm currencies' weakness have been a headwinds for AMX since capex (wireless infrastructure, software etc.) is mostly imported or USD linked. This means that there is a mismatch between EBITDA and Capex that can dent ROIC and drive debt higher. Capex discipline became very important. In the chart below, one can see how capex as a percentage of EBITDA spiked to over 60% when the MXN devalued. Today the MXN has appreciated, and EBITDA is increasing faster than Capex, which drives free cash flow and ROIC.

MXN variation impact on ROIC (Created by author, data by AMX)

{kind=link}

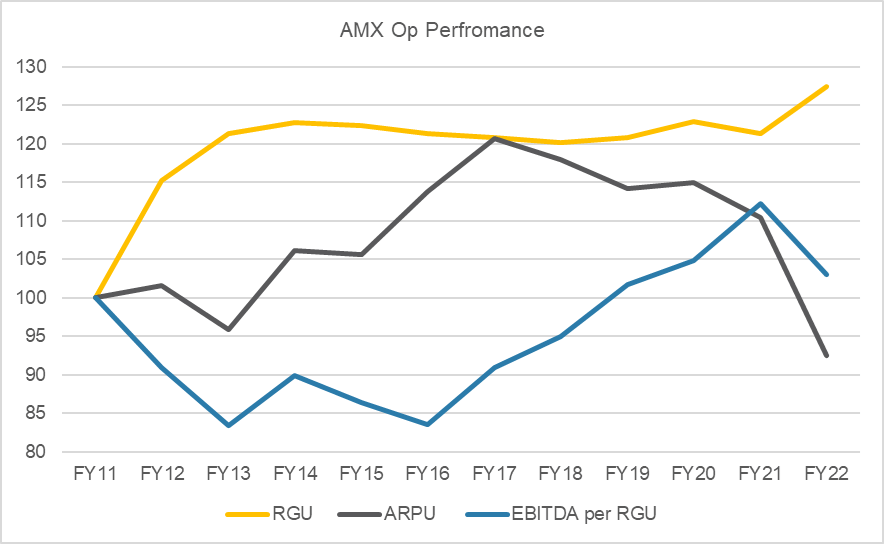

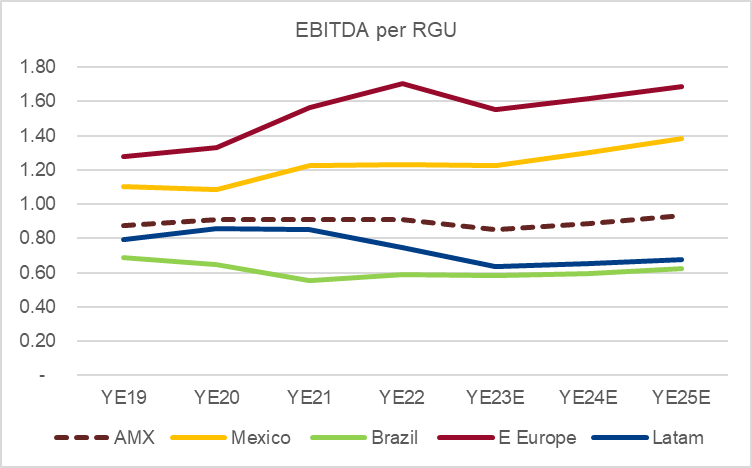

In the following chart one can see how stagnation in RGU offset by improved ARPU and a sharp recuperation of EBITDA per RGU in MXN. In 2022 that trend changed mostly due to the acquisition of a bankrupt Brazil operator that was dismembered and sold off to the three main players.

AMX operating data in MXN (Created by author, data by AMX)

{kind=link}

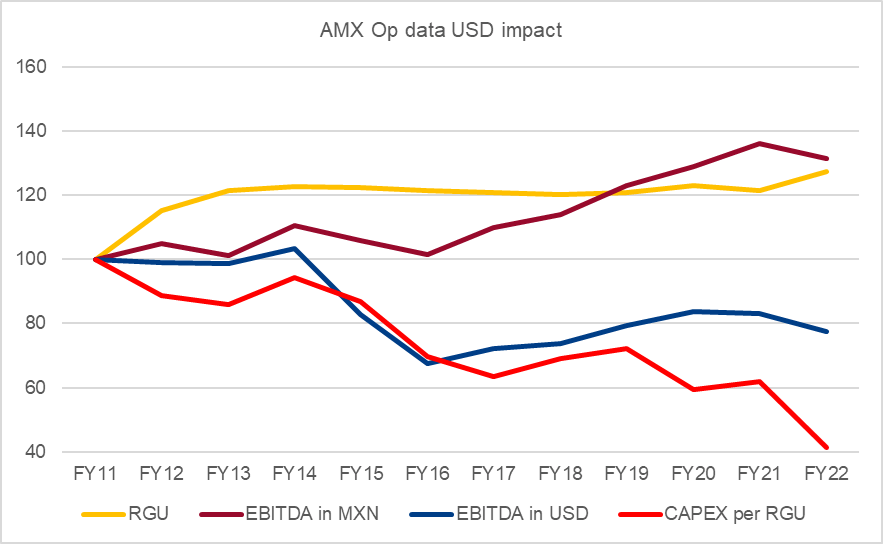

Contrary to the above chart in MXN, the operating drivers in USD are less favorable and demonstrate the risk of emerging markets. While EBITDA grew in MXN it declined in USD terms due to currency devaluation. However, and key to AMX investment case is that Capex per RGU has declined consistently, suggesting capital discipline and scale gains. As mentioned earlier, capex is key to the Telecom sector investment considerations.

AMX operating data in USD (Created by author, data by AMX)

{kind=link}

AMX Operating Overview

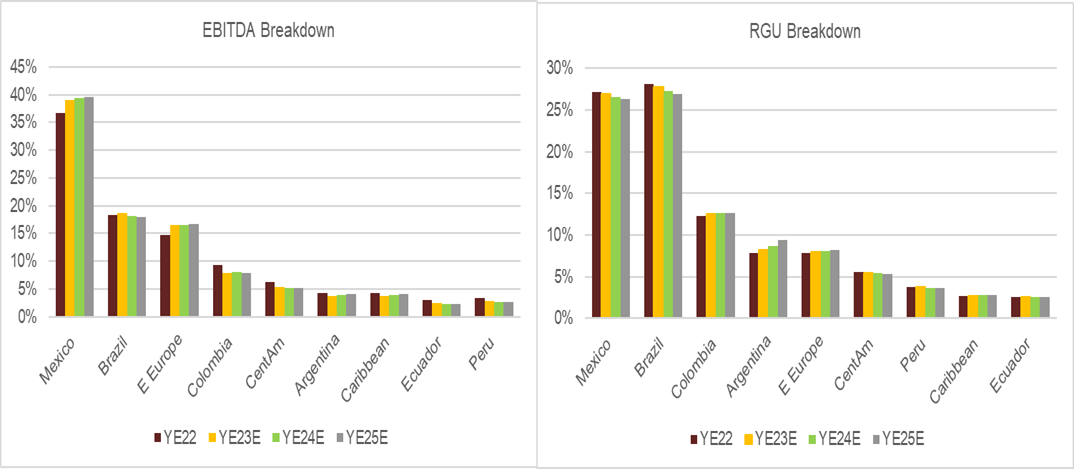

Mexico continues to dominate AMX with over 35% of EBITDA followed by Brazil with 18% of EBITDA. Brazil operations have the weakest dynamics due to FX devaluation, competition and recent M&A as seen in the ARPU (Average Revenue Per User). Austria and Eastern Europe operations provide strong currency EBITDA and contribute nearly double their RGU count. A principal driver for subpar results in LatAm (ex-Mexico) is that in many markets AMX is the 2nd and 3rd players in terms of market share with Telefonica (TEF) usually the top player across markets. This means it has lower scale and any increased competition causes expensive churn that drains margins. Churn is the amount of RGU that leaves your network and thus to grow companies typically enter into price promotions that increase sales cost and reduces ARPU.

5G roll out may provide RGU and revenue growth but adoption from advanced tech i.e. the Internet of things etc.. is still under development. I am assuming a very modest pickup in RGU and ARPU starting in 2024.

EBITDA and RGU Breakdown (Created by author, data by AMX)

{kind=link}

ARPU Breakdown in USD (Created by author, data by AMX)

{kind=link}

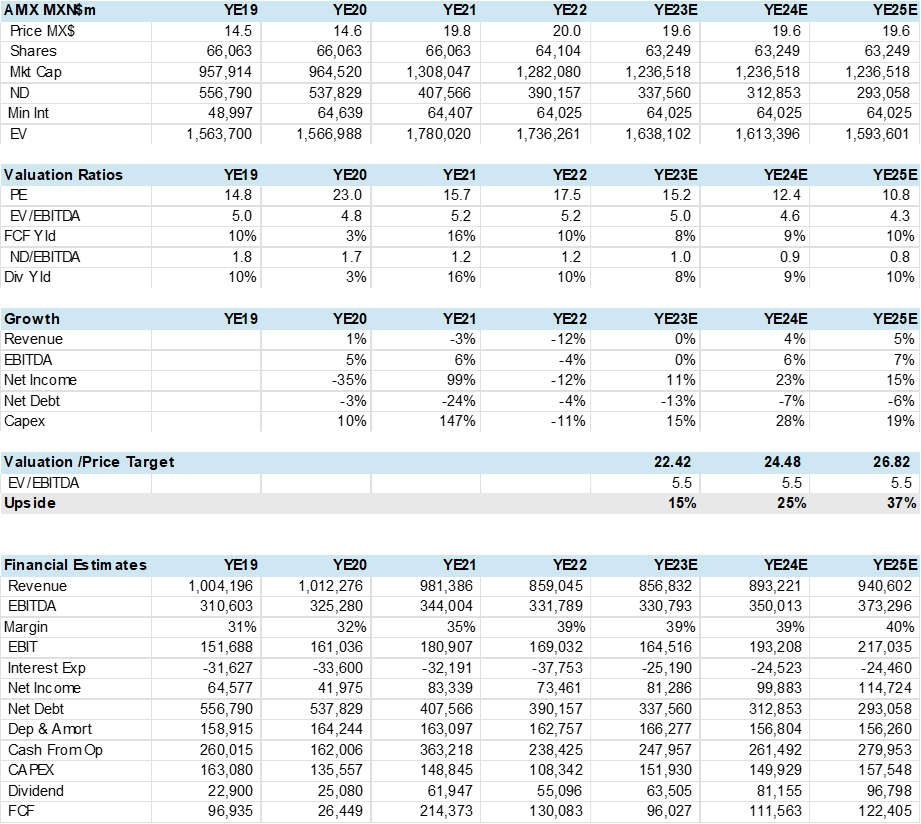

AMX Financial Estimates

Below a summary of key financial data and valuation in Mexican pesos. As can be seen the company has seen declining revenue and EBITDA but increased free cash flow, debt reduction and dividends/share buybacks. AMX is more like a mature utility than a consumer company.

I am valuing AMX stock at 5.5x EV/EBITDA on YE23 EBITDA estimates that provide a 15% upside potential plus 8% in dividends. This is not a growth stock and multiple may increase when the Mexico Central Bank begins to reduce interest rates, which is not likely until the Fed does.

AMX Financial and Valuation Summary (Created by author, data by AMX)

{kind=link}

Consensus

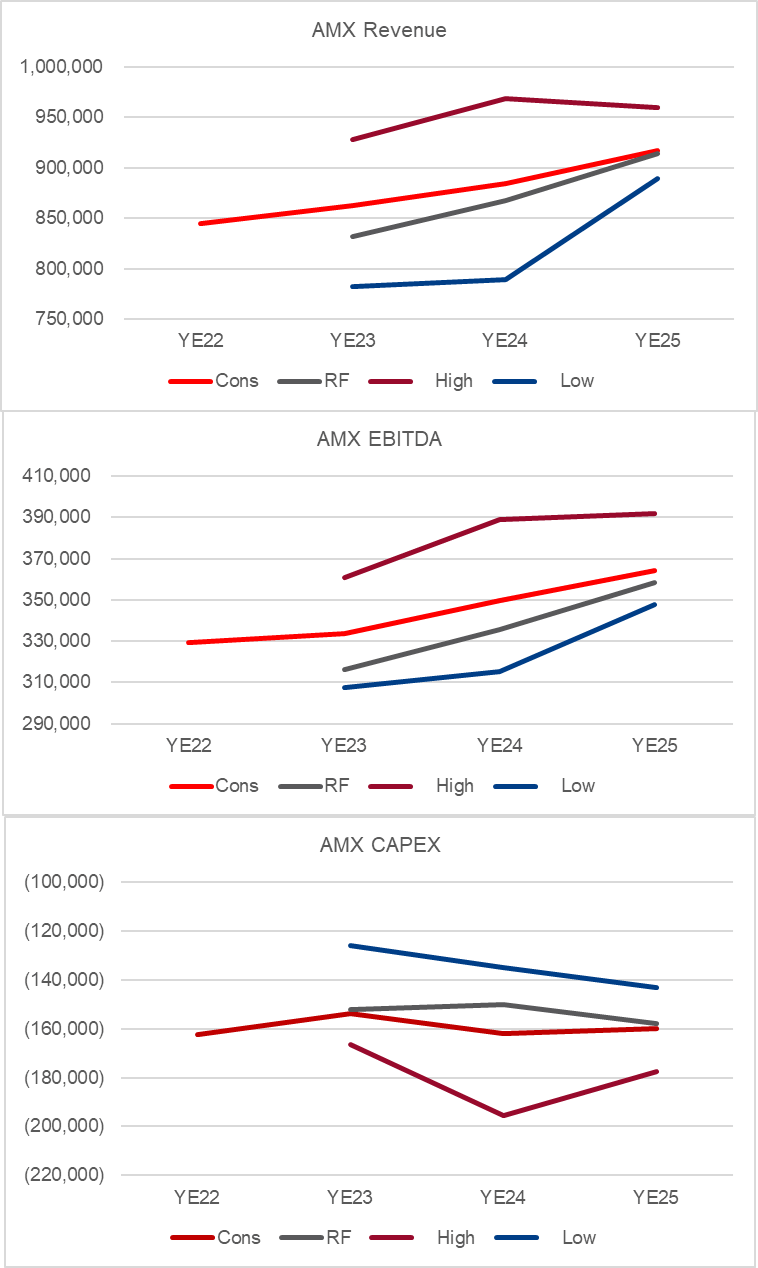

My estimates are below consensus on a more conservative RGU, ARPU and margin outlook vs the 16 sell-side analysts on Capital IQ. For 2024 and 2025 my estimates close the gap as 5G roll out may stimulate greater growth. All the estimates are in Mexico Pesos.

AMX Consensus Ranges in MXN (Created by author, data by Capital IQ)

{kind=link}

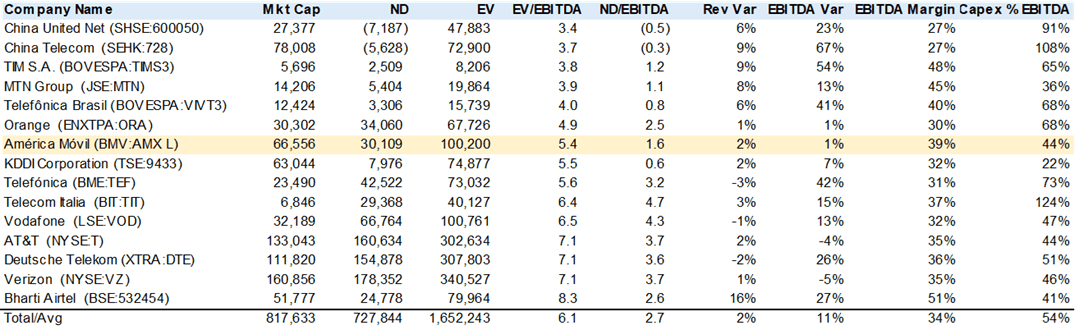

Peer Comps

AMX is in the middle of sector comps in terms of valuation. As can be expected higher growth names command greater multiples. The exception are the Chinese peers, which may be rebounding vs Covid restrictions. If AMX see better growth, perhaps driven by 5G or a stronger Mexico macro, the valuation may expand. For now, I would not count on it.

AMX Peer Comps (Created by Author, data from Capital IQ)

{kind=link}

What about 5G

5G provides vastly higher data speeds and increases potential new business uses and may/should increase RGU (revenue generating units). However, will the added revenue/EBITDA beat or provide a return on the capex, which includes spectrum?

5G has the potential to change the perception of cellular providers as "dumb pipes" of the internet and enable them to capture a larger share of the value in the internet ecosystem. Here are some ways that 5G could enable cellular providers to create new revenue streams:

Network Slicing: Designed to enable network slicing, which allows cellular providers to allocate different portions of their network to different applications or customers. This means that cellular providers can offer differentiated services with different quality-of-service levels and pricing models.

IoT Services: 5G supports the large-scale deployment of IoT devices, which can generate new revenue streams for cellular providers. This includes services such as asset tracking, remote monitoring, and predictive maintenance.

Edge Computing: This can enable new services such as real-time analytics, augmented reality, and virtual reality.

Content Delivery: Providers can offer high-quality video streaming and other content delivery services.

Conclusion

AMX has executed well through sector competition and macro headwinds in its 20-year track record. It is now a mature company in a far more stable telecom sector that looks to balance growth, capex, free cash flow generation and dividends to generate value. The risk reward equation is positive in my view for investors looking for Mexico and 5G exposure.

For further details see:

America Movil: Unchallenging Valuation, Capex Discipline And A Strong Peso Drive Shares