CRMT - America's Car-Mart: Economic Conditions Causing Profitability Issues

2023-11-14 09:00:39 ET

Summary

- CRMT’s revenue has grown at an impressive CAGR of 12%, driven by aggressive expansion, a focus on financing under-served markets, and industry tailwinds.

- Like many, the company has benefited from the post-pandemic bump but has seen a deep decline in profitability subsequently, illustrating the weakness of its business model.

- We believe the company is less compelling relative to others within the industry, primarily due to its excessive exposure to a single growth strategy and lack of diversification.

- With CRMT trading at a premium to its peers and historical average, we believe the stock is clearly overvalued.

Investment thesis

Our current investment thesis is:

- CRMT's business model has left the company highly cyclical, with its target demographic heavily exposed to a market downturn. Further, this is compounded by difficulties with underwriting loans, due to increased delinquencies and origination concerns.

- We do believe the automotive industry is experiencing tailwinds but investors may be better off considering other stocks such as Lithia and Asbury, owing to their more diversified business models.

- CRMT's quarterly results continue to look disappointing, with margins already at decade-low levels and the scope for improvement limited.

Company description

America's Car-Mart, Inc. (CRMT) is a publicly traded automotive retailer specializing in the sale of used vehicles primarily in the United States. The company operates a network of buy here, pay here dealerships, serving customers who have limited access to traditional financing. America's Car-Mart is headquartered in Rogers, Arkansas.

Share price

CRMT's share price performance has been respectable, returning over 100% to shareholders while the wider S&P slightly exceeded this. This has been driven by strong financial development and commercial improvement.

Financial analysis

America's Car-Mart financials (Capital IQ)

{kind=link}

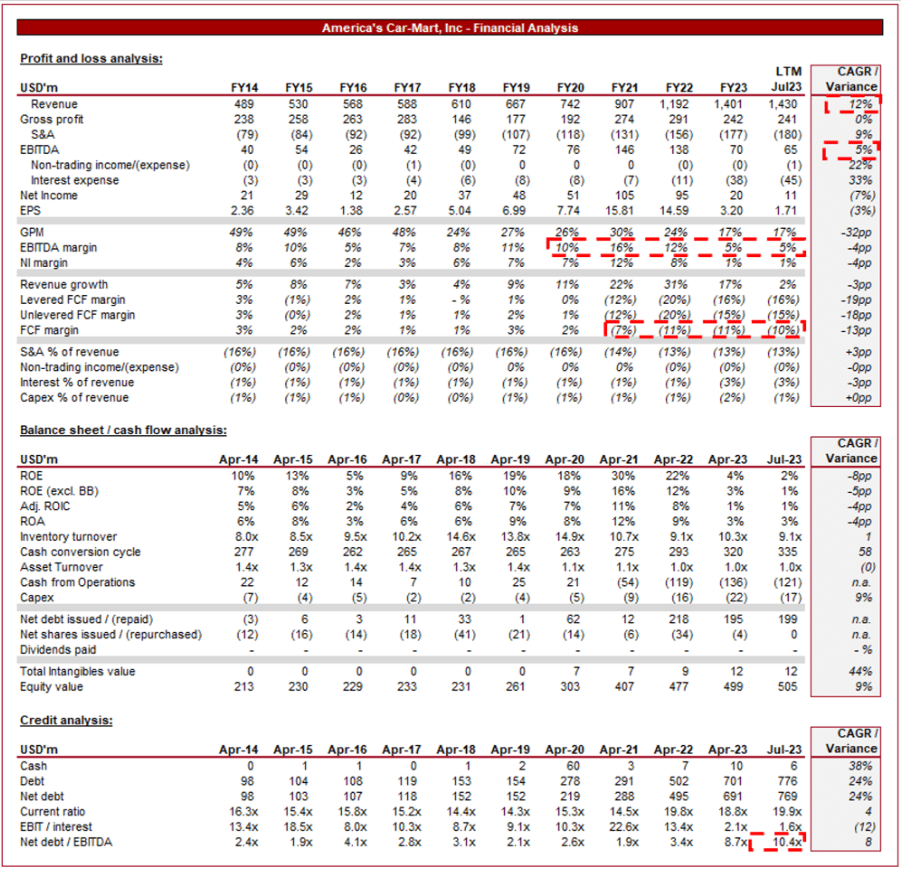

Presented above are CRMT's financial results.

Revenue & Commercial Factors

CRMT's revenue has grown impressively, with a CAGR of 12% into the LTM period. This growth has been incredibly consistent, with no single period of negative growth, even during the pandemic.

Business Model

CRMT operates on a "Buy Here, Pay Here" model, which means it not only sells vehicles but also provides financing directly to customers. This approach allows the company to serve individuals who may have difficulty obtaining financing from traditional lenders due to poor credit histories.

CRMT focuses on customers with limited credit options. This niche market includes individuals who may have had credit issues in the past or have limited credit histories. By supporting this underserved customer segment, the company has built a loyal customer base and a niche competitive advantage within the industry. Many of the traditional dealerships utilize third-party lenders/underwriters who are heavily weighted toward Prime debt only.

Providing financing in-house allows CRMT to have greater control over the lending process. It can tailor financing options to the specific needs of its customers, which can improve loan approval rates and customer satisfaction. This said, the company is responsible for all things risk management, involving exposure and financing.

The financing aspect of the business provides a steady stream of revenue through interest and finance charges. Even if economic conditions change, customers broadly prioritize their vehicle payments, which helps maintain a consistent revenue flow. Further, the margins associated with financing are significantly higher than the used car segment, which is known for its tight pricing.

CRMT has been expanding its dealership network, reaching more customers in different geographic regions. This expansion has contributed to the development of its business model, also, providing greater convenience and access.

Industry developments

CRMT's performance significantly improved between FY21 and FY23, following a rapid uptick in demand for used cars. This was due to supply constraints in the primary market, as semiconductor supply was insufficient and lockdown restrictions impacted production. With supply in the primary market lacking, consumers turned to used cars, driving up prices. This has slowly begun to unwind, contributing to margin pressures for many of the dealers. This is one of the primary reasons for CRMT's margins contracting to the degree it did in FY23.

Furthermore, the EV revolution is a broader trend that has impacted the industry positively, with Government legislation, running cost difference, and the sustainability movement encouraging a transition to EVs. We expect this to continually encourage greater demand for EVs in the lead-up to the phasing out of traditional ICE-powered cars.

Finally, the US vehicle fleet has reached a record age of 12.5 years , reflecting better quality vehicles and the relative affordability of households. This should ensure long-term health within the industry, as the need for a new vehicle statistically increases with age. Not only this but it further engrains the used car market as an attractive alternative to new cars.

Economic & External Consideration

Current economic conditions present a significant issue for CRMT. With high inflation and elevated interest rates, living costs are rising rapidly, with consumers naturally deferring or canceling large-ticket. The issue with CRMT is that the company is vastly more exposed than its peers. Firstly, the used car segment is far more exposed to a slowdown than the new. Secondly, CRMT targets a lower-earning demographic, who are generally harder hit by such conditions. Finally, with elevated interest rates, the financing segment is hit particularly hard, with greater delinquencies and difficulties with origination.

Key takeaways from the company's most recent quarter are:

- Revenue of $368m, representing growth of +8.6%. This is a strong performance but is primarily due to a disappointing result last year contributing to a reduced comparator. Revenue is down on a QoQ basis.

- Margins have improved, with GP per car up +3.7%. Again, this is partially due to a weak comparator but also an operational improvements and increased ancillary product sales to drive unit economics.

- An increase in the provision for loan losses from 25.9% of revenue to 30.9%, with net charge-offs up 0.7% to 5.8%. Management attributes this to the "post-stimulus normalization of charge-offs", as well as additional provisioning resulting from increased contract terms, and higher average interest rates on the portfolio. This is a concerning trend, particularly as consumers are not experiencing a material improvement in finances.

This has been a good quarter for the business relative to the prior year but remains below where CRMT wants to be. Significant improvement is required but also this reflects a key weakness with this company, that it is highly cyclical.

Margins

{kind=link}

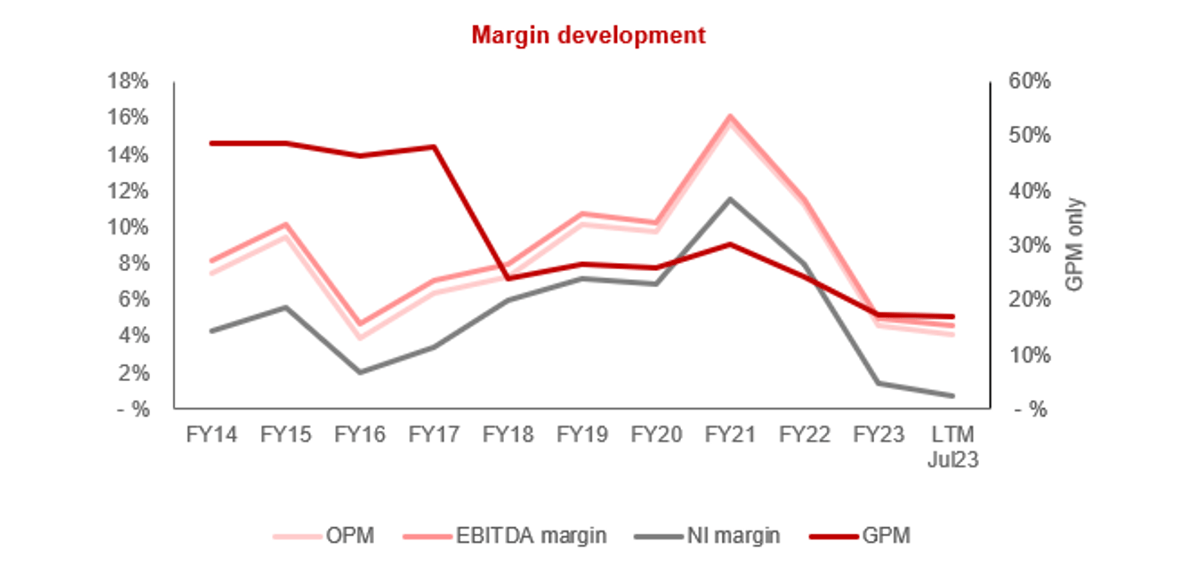

CRMT's margins had been improving prior to the recent downturn, with the company now at a decade-low on an EBITDA basis. This further illustrates the weakness of its business model, as CRMT is far too cyclically linked, and lacks to the scale necessary to offset the fluctuations in provisions required and the demand for used cars.

We expect margins to improve in the medium term, as provisions unwind once market conditions improve. Realistically, however, this means an EBITDA-M of c.8%.

Balance Sheet & Cash Flows

The decline in CRMT's cash flows is a reflection of an aggressive origination strategy in recent years, contributing to a growing delta to cash collections. CRMT has balanced this aggressive strategy by laddering up its financing balance, reaching a ND/EBITDA balance of 10x. With interest payments now at 3% of revenue and interest coverage at 1.6x, Management is towing a fine line with profitability.

Industry analysis

Automotive Retail Stocks (Seeking Alpha)

{kind=link}

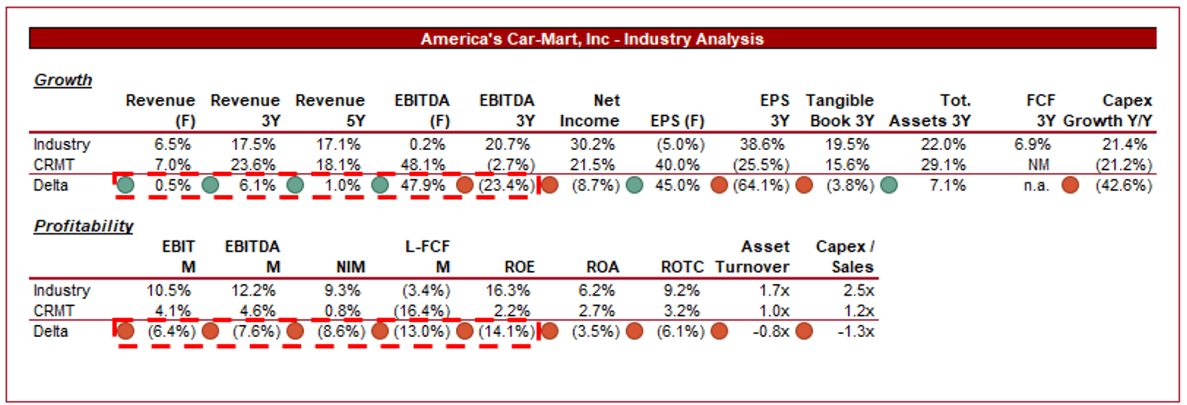

Presented above is a comparison of CRMT's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

CRMT underwhelms relative to its peers in our view. The company's margins are noticeably below the average, implying its deterioration following a softening of demand has been above average. This is due to its target demographic being overly exposed to the slowdown, as well as its used car focus.

CRMT does make up for this partially with growth, slightly outperforming the average. This said, the delta is not significant enough in our view, with the business normalizing to the average on a forward revenue basis.

Valuation

{kind=link}

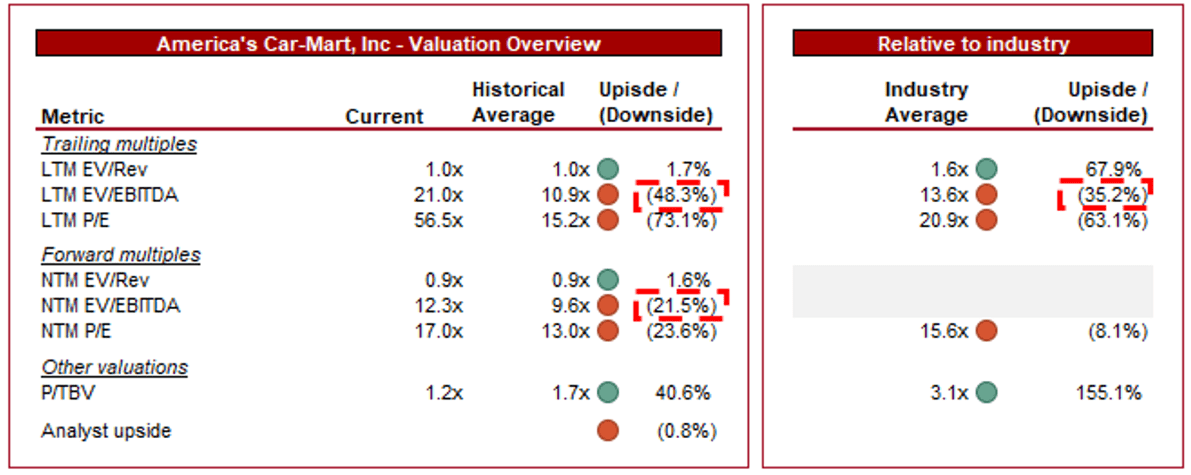

CRMT is currently trading at 21x LTM EBITDA and 12x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average appears unreasonable in our view, with an overweight expectation for future improvement. The business has progressed well and its strategy does allow for outsized growth during "the good times" but we do not consider this compelling enough to suggest a c.20% premium on a NTM basis is reasonable, particularly during a downturn.

Further, the company is trading at a premium to its peer group, both on a LTM EBITDA basis and NTM P/E. This again is unjustifiable in our view. Peers such as Lithia ( LAD ) and Asbury ( ABG ) are investing heavily in ancillary services, such as parts and financing (without underwriting), while operating a diversified national used/new segment. This creates a far more sustainable trajectory.

Based on this, we believe CRMT is currently overvalued, which is supported by Wall St. analysts.

Final thoughts

CRMT has done well to carve out a niche through its focus on the sub-prime segment, with an aggressive financial strategy allowing it to achieve strong growth and scope for consistent, profitable returns. The issue is that we are within a bear market, with the downside risks now playing out. We do not think solvency is a concern (yet) but a continuation of its current struggles is inevitable.

With CRMT trading at a premium to its historical average and peer group without significant growth or margin improvement in sight, we consider this stock overvalued.

For further details see:

America's Car-Mart: Economic Conditions Causing Profitability Issues