CRMT - America's Car-Mart: High Prices Continuing To Weigh On The Used Car Market

2023-11-09 18:25:51 ET

Summary

- America's Car-Mart shares have declined almost 35% since August as investors anticipate headwinds for the company.

- Consensus EPS estimates for fiscal 2024 have been revised downwards, indicating a lack of confidence in a swift turnaround.

- The high prices of used cars and the need to span out loan contracts to accommodate affordability pose challenges for CRMT's profitability and debt management.

Intro

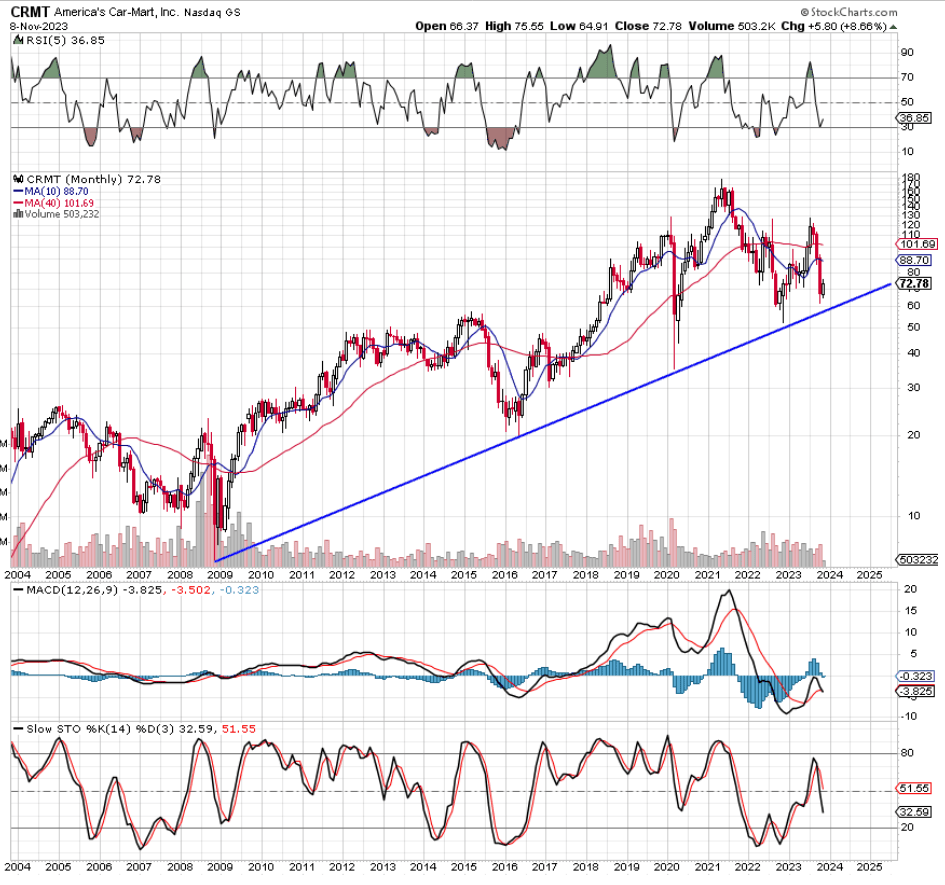

We wrote about America's Car-Mart , Inc. ( CRMT ) back in August of this year when shares were showing considerable strength. Earnings were improving and sustained investment taking place in the likes of the customer relationship management system meant that theoretically, (through extensive data analysis), CRMT would have more targeted prospects over time. However, given how shares were coming up against overhead resistance on the intermediate 5-year chart and how buying volume was beginning to taper off in a significant way (as seen on the daily 12-month chart), we refrained from issuing a 'Buy' rating at the time. Shares now find themselves almost 35% down from our most recent commentary in August as investors begin to price in significant headwinds for the company going forward. Furthermore, the biggest 'technical' test is yet to come for the automotive retailer as we see below.

As we see below, the sharp decline in CRMT's share price in recent months has resulted in shares coming up against long-term support which dates back to the Great Recession of 2008. Although CRMT has managed to successfully test support several times over the past 15 years or so, recent 'consensus EPS revision' trends do not foster confidence that a swift turnaround is around the corner any time soon.

For example, the bottom-line consensus estimate (less than 3 months ago) for fiscal 2024 (ending April 2024) was an EPS of $4.94 per share. This target has now been revised down to $4.15 per share and most likely will fall further when we consider the recent trends discussed below.

CRMT Technical Chart (Stockcharts.com)

{kind=link}

Worrying Q1 Trends

First, America's Car-Mart caters to a segment of the market the former CEO (Jeff Williams) stated is 'always in recession '. What this essentially means is that given this segment's continuous struggle to stay on the road through meeting consistent monthly payments, CRMT always has to balance the inventory it has on its books with what its customers can realistically afford. Therefore, when you see that used car prices have remained stubbornly high for a myriad of reasons (through the likes of lower stocks in general, inflation & chip shortages exacerbated by the pandemic), this puts more pressure on affordability over time which CRMT is acutely aware of.

CRMT's contract terms with customers have had to be spanned out to accommodate this 'new normal' but the real question is whether present trading conditions can do a 180 or whether current elevated inflation can finally present itself in wage growth (better affordability) in a meaningful way. If indeed, a significant change does not present itself in the present market, investors should be aware that those panned-out contracts essentially mean less income over time (per transaction) for the retailer. This trend (given the fact that CRMT's current net income trailing margin comes in below 1%) is worrying as it means CRMT will not generate profits as fast as prior times. Remember, in low-margin businesses, it is a prerequisite to be able to turn over capital as quickly as possible to ensure successful reinvestment can transpire.

Not being able to recoup as much profit as originally envisioned has led to repeated 'rolling-over' of the company's debt which is another worrying trend. Due to increasing long-term debt (now $710+ million), interest expense in Q1 of $14.3 million came in only $5.4 million short of the retailer's operating profit. Trailing net profit now comes in almost 70 times lower than the company's debt load. This certainly has ramifications for the company being able to meet this debt if indeed interest rates keep on trending higher.

Valuation

The lack of elevated earnings compared to CRMT's enterprise value can be seen clearly in the company's trailing EV/EBIT multiple which comes in at an ultra-high 21.07. CRMT's peers on average trade with a lower EV/EBIT multiple of 13.55 and have been reporting better growth rates to boot. Using the EV/EBIT multiple as opposed to the p/e ratio is advisable as it takes CRMT's balance sheet into account which is key considering the leverage the retailer is currently holding. Furthermore, given the almost $280 million of property, plant & equipment on CRMT's balance sheet & associated capital expenditure, using the EV/EBITDA multiple to value CRMT would also not be advisable as it would inflate the retailer's earnings so to speak.

Suffice it to say, slower expected growth coupled with an already overextended valuation is not a marriage made in Heaven. However, CRMT fully intends to keep on investing through the cycle. By picking up other dealerships which have run out of money, the retailer should continue to gain share but at what cost is the question.

Increasing market share in a down-market is all well and good but the market only wants to know one thing - when will affordability improve for the better? For example, used car prices (even if they decline over a monthly basis) remain much more expensive compared to pre-pandemic levels. The longer this trend remains in place, the more doubtful I become whether long-term support alluded to earlier in the technicals will hold.

Conclusion

To sum up, forward earnings expectations have pretty much collapsed over the past 3 months as investors read into tougher times for CRMT. With used car prices remaining elevated due to inflation and reduced inventory compounding the problem, CRMT has had to span out loan contracts to compensate. Whether this will have a long-term impact on the delinquency rate remains to be seen. We continue with our 'HOLD' rating but will be watching long-term support levels closely if indeed shares keep falling. We look forward to continued coverage.

For further details see:

America's Car-Mart: High Prices Continuing To Weigh On The Used Car Market