CRMT - America's Car-Mart: When The Data Changes My Opinion Changes

Summary

- America's Car-Mart continues to generate strong sales, but bottom line results have become increasingly problematic.

- This has caused shares to become more expensive, but this should only last for as long as economic issues persist.

- Because of the uncertainty of how long that will be, though, a more cautious approach for this prospect is warranted.

Some of the most attractive companies I have seen from a valuation perspective over the past year or so operate in the automotive retail space. Concerns over the economy more broadly and the impact that high interest rates will have on the production and sale of cars has led to many of these companies being overlooked or underappreciated by market participants. But this is not to say that every player is being unjustly treated by the investment community. Due to a change in fundamental condition, some of the firms, such as America's Car-Mart ( CRMT ), likely deserved some downside. With additional pain potentially around the corner, this firm, which really should be treated more like a finance business than just a plain car dealership, could experience even more deterioration in its bottom line results. This is not to say that the company makes for a bad prospect for those who are willing to hold it for the long haul. But given where we are in what could be a continued downturn in the automotive retail space, there are far better prospects to consider at this point in time.

I underestimated this one

At this time, I run a very concentrated portfolio. In total, this portfolio consists of nine individual holdings. One of them, the third largest by asset value at this time, operates in the automotive retail space. So needless to say, I'm a huge fan of this market and I believe that, for the most part, it is drastically undervalued. But this is not to say that every player in the market should be looked upon in the same gleaming light. And that was a mistake that I made when I first wrote about America's Car-Mart in January of 2022. At that time, I called the company an intriguing business that had a history of attractive top line and bottom line growth. This is not to say that I was completely under its sway. After all, I acknowledged that it was a complicated firm that really should have been considered more a finance enterprise than just a car dealership. But despite those risks, I felt as though shares of the company were cheap and that the business would offer attractive upside for long-term investors. That ultimately led me to rate it a 'buy' to reflect my view that shares should outpace the broader market for the foreseeable future. So far, however, that call has been wrong. While the S&P 500 is down 16.3% since the publication of that article, shares of America's Car-Mart have experienced downside of 27.4%.

{kind=link}

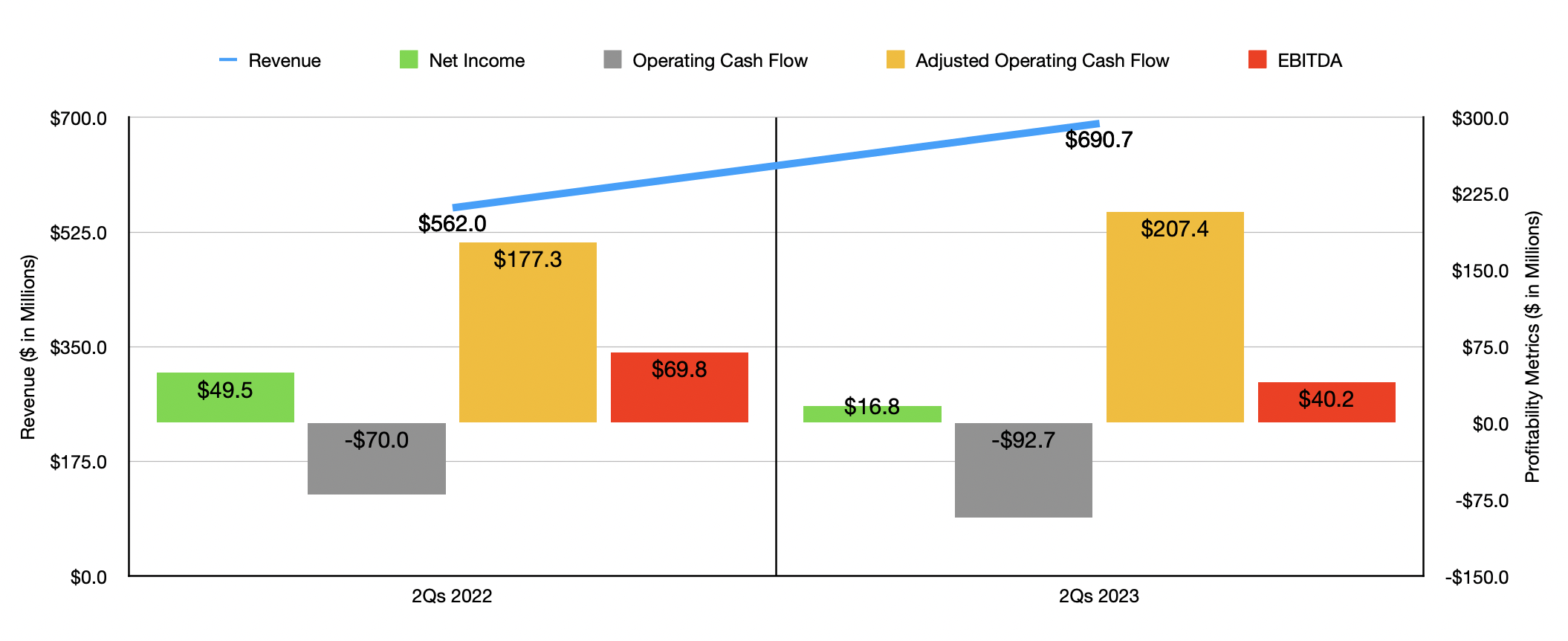

Interestingly, this return disparity exists even though sales growth for the company continues. Consider how the company fared during the first half of its 2023 fiscal year. Revenue during that time came in at $690.7 million. That's 22.9% higher than the $562 million generated the same time one year earlier. This increase was driven by a couple of factors. First and foremost, the number of stores that it had in operation grew from 152 to 154. A rise in the average units sold per store also benefited investors, with that number climbing from 33.2 to 34 in an average month. That translated to the number of retail units that the company sold climbing from 30,043 to 31,421. Also benefiting the firm was the fact that the average retail sales price of the cars in its portfolio increased from $15,567 to $18,045.

This is great in and of itself. But what's not great is that the company reported a decline in profitability. Net income dropped from $49.5 million in the first two quarters of 2022 to $16.8 million the same time of its 2023 fiscal year. There were three primary drivers behind this decline in profits. Although sales increased, the cost of sales for the company, excluding depreciation, jumped from 63.1% of sales to 66.8%. This increase, management said, was largely attributable to wholesale losses and inventory procurement challenges, the latter of which involved higher direct and indirect costs related to repair parts, transportation fees, fuel costs, and cost of sale expenses.

Also problematic was the fact that the provision for credit losses for the company jumped by 55.2%, climbing from 21.6% of sales to 27.6%. This, management said, was driven by an increase in both the frequency and severity of losses when it came to net charge-offs year over year. Total net charge-offs of finance receivables during the six-month window covered came out to 11%. That's up from 8.4% seen at the same time one year earlier. And finally, interest expense for the company increased from 0.9% of sales to 2.6%. Naturally, this stemmed from a general rise in interest rates, combined with the impact that they had on a rise in average borrowings made by the business. These challenges impacted other profitability metrics as well. Operating cash flow went from negative $70 million to negative $92.7 million. It is true that the adjusted figure for this, which ignores changes in working capital, improved from $177.3 million to $207.4 million. But offsetting this to some degree is the fact that EBITDA worsened from $69.8 million to $40.2 million.

{kind=link}

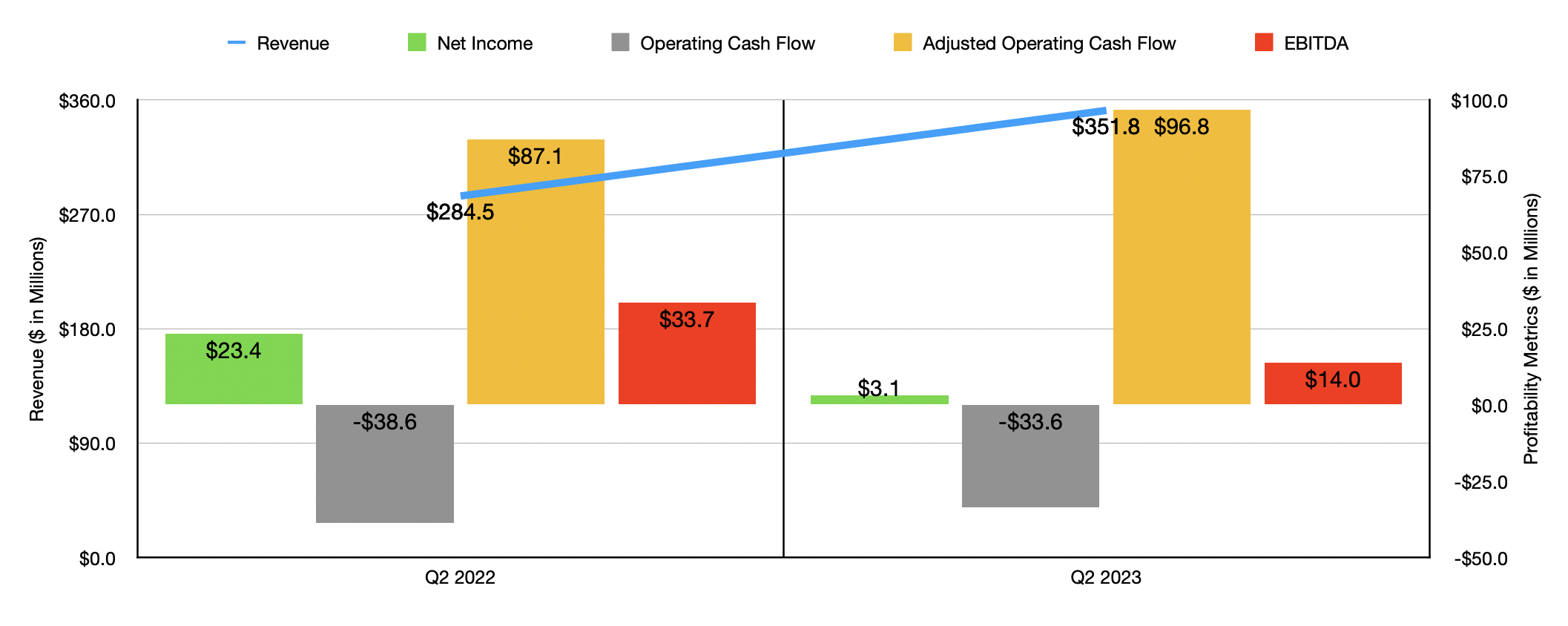

Problems for the company were present in both quarters. In the second quarter, for instance, sales were still strong, coming in at $351.8 million. That's 23.7% above the $284.5 million reported one year earlier. An increase in retail units sold and a rise in average retail sales prices were instrumental in the second quarter just as they were in the first half of the year in its entirety. But because of the same aforementioned factors, net income plunged from $23.4 million to $3.1 million. Operating cash flow went from negative $38.6 million to negative $33.6 million, while the adjusted figure for this went from $87.1 million to $96.8 million. Although the operating cash flow figures are great to see, I reiterate my point from my first article on the company that its exposure to the finance space makes operating cash flow a fairly poor metric to look at. Perhaps more appropriate would be EBITDA, which declined from $33.7 million to $14 million.

{kind=link}

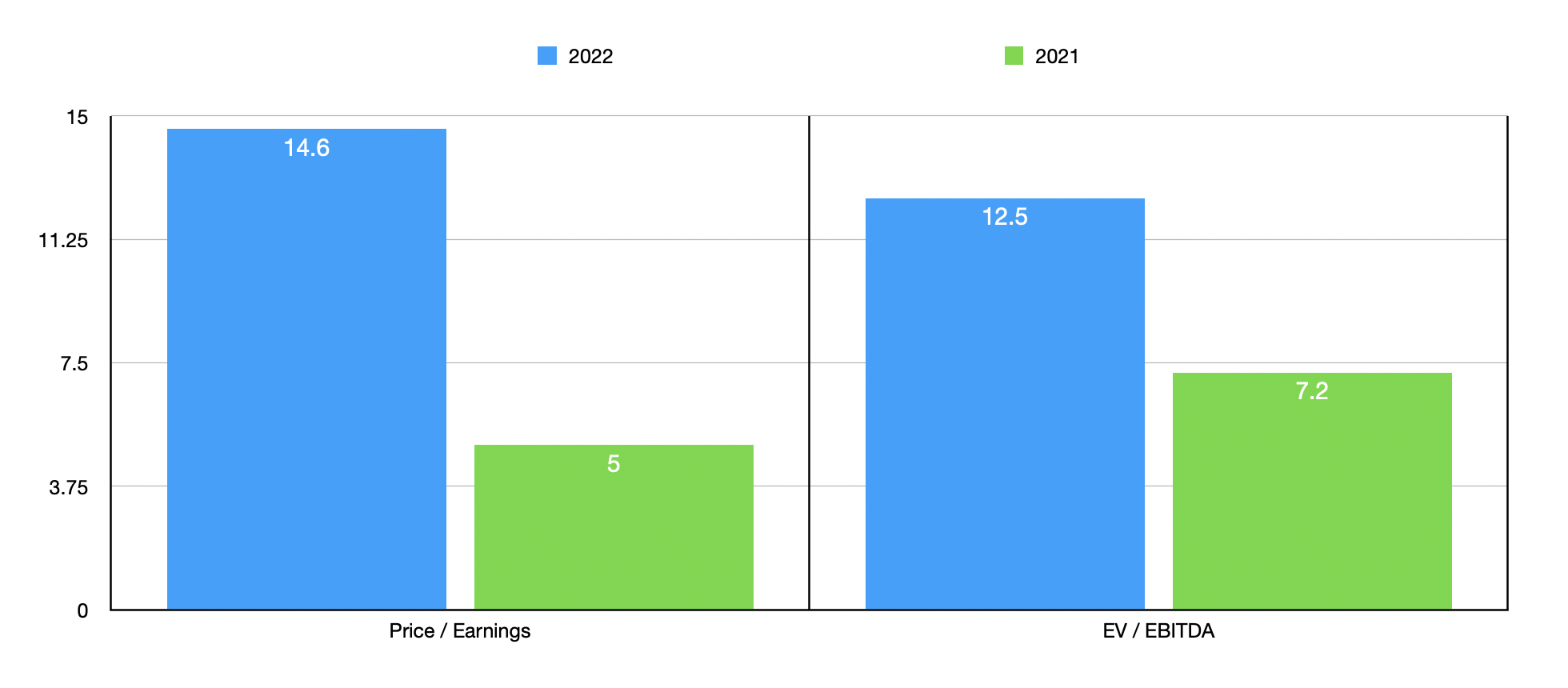

Truth be told, we really don't know what to expect for the rest of the 2023 fiscal year. If we simply annualize the results experienced so far, we would get net income of $31.7 million and EBITDA of $78 million. This would imply a forward price-to-earnings multiple for the company of 14.6 and a forward EV to EBITDA multiple of 12.5. To put this in perspective, if we were to use the data from 2022, these multiples would be considerably lower at 5 and 7.2, respectively. As part of my analysis, I did also compare America's Car-Mart to five other players in this market. On a price-to-earnings basis, these companies ranged from a low of 4.5 to a high of 18.4. Only one of the five was more expensive than our prospect. Meanwhile, using the EV to EBITDA approach, the range was from 4.4 to 20. In this scenario, once again, only one of the five companies was more expensive than America's Car-Mart.

| Company |

| Price / Earnings |

| EV / EBITDA |

| America's Car-Mart |

| 14.6 |

| 12.5 |

| CarMax ( KMX ) |

| 18.4 |

| 20.0 |

| AutoNation ( AN ) |

| 4.5 |

| 4.4 |

| Penske Automotive Group ( PAG ) |

| 6.4 |

| 5.9 |

| Group 1 Automotive ( GPI ) |

| 4.5 |

| 4.6 |

| Asbury Automotive Group ( ABG ) |

| 5.2 |

| 5.7 |

Takeaway

From what I can see in the data, I do find it interesting that the company continues to increase its sales. This on its own is a great thing. If we knew for sure that the interest rate environment would not worsen materially from here, I would even be willing to still rate it a 'buy' since I would believe that a return to normalcy would be soon coming. But because we have uncertainty in that regard and because bottom line results continue to deteriorate, I believe that a downgrade to a 'hold' rating is appropriate at this time.

For further details see:

America's Car-Mart: When The Data Changes, My Opinion Changes