AFGB - American Financial Group: A Yield Of Over 5.00% On Debentures

2024-01-04 07:53:01 ET

Summary

- The 5.125% debentures issued by American Financial Group are a safe choice for investors with an attractive yield.

- The debentures are undervalued by 10%.

- American Financial Group is a strong and stable company with excellent creditworthiness and financial viability.

Thesis

The 5.125% debentures ( AFGC ) issued by American Financial Group, Inc. ( AFG ) are a safe choice for investors who want a dependable income security with an attractive yield. I believe they are currently undervalued by 10%.

About AFGC

This is one of four ‘baby bond’ debentures brought to market by American Financial (baby bonds are debt instruments that can be traded like stocks on major exchanges):

- 5.875% Subordinated Debentures due March 30, 2059 (AFGB)

- 5.125% Subordinated Debentures due December 15, 2059 (AFGC)

- 5.625% Subordinated Debentures due June 1, 2060 (AFGD)

- 4.50% Subordinated Debentures due September 15, 2060 (AFGE)

According to AFGC’s prospectus , filed November 21, 2019, it is a subordinated debenture with a maturity date of December 15, 2059, which is currently 36 years away. It was a $200 million issue and, as noted, pays 5.125% per year. Investors can buy them in units of $25.00.

Whether an investor should buy them depends mainly on three criteria: the interest rate, the underlying firm’s credit rating, and the maturity date. We’ll look at each of them in turn.

Interest rates

If you buy these long-term loans, you are locking in a 5.125% yield for up to 36 years. We can assess how this return compares with other current returns, but ultimately, what we decide about the future must be speculation.

One comparable income product is a 10-year Treasury Bond, which currently pays 3.94%. AFGC pays 30.0% more, but of course, the latter carries slightly more risk than the former.

Then there are the two baby bonds shown above with slightly higher yields, AFGD at 5.625% and AFGB at 5.875%. While these yields are higher, they are also more likely to be redeemed, as we will discuss below in the Maturity date section.

Alternatively, we might compare AFGC's yield with American Financial’s dividend, which is currently 2.38%, which is less than half the AFGC return. However, owning the stock rather than the debentures is also likely to generate capital gains.

The firm gets a B+ profitability grade from Seeking Alpha, and two components of that are the five-year Return on Common Equity or ROCE [TTM] of 15.42% and the five-year Return on Total Capital [ROTC] [TTM] of 9.76%.

Note that ROCE, is almost exactly triple the return from AFGC, which would tempt at least some investors to opt for the firm’s stock rather than its bonds. However, debenture holders are more likely to get their money back than shareholders in the very unlikely event American Financial Group suffers a major loss (on the operations side, the company uses reinsurance to cap its liabilities for catastrophic losses).

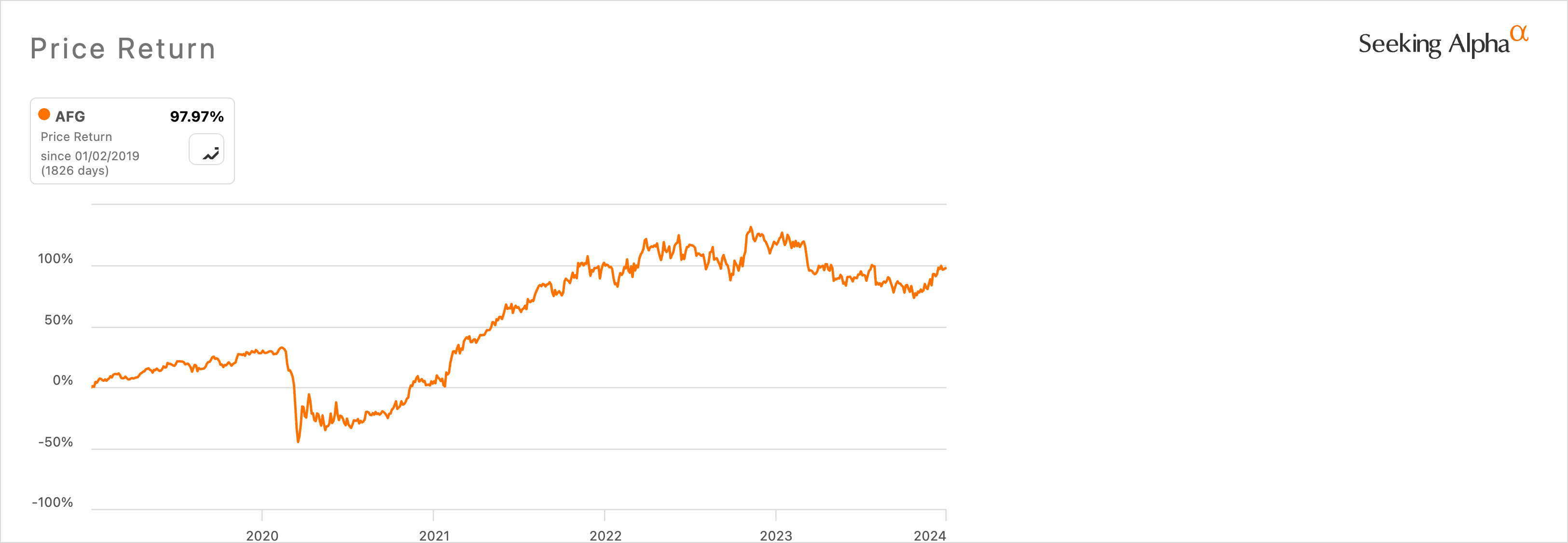

Thanks to results like these, investors in the parent company have seen a price return of nearly 100% over the same period:

{kind=link}

The other side of the interest rate coin is the prevailing economic interest rate. The state of the broader economic environment dictates the value of fixed-return securities. As interest rates rise, debentures and bonds decline in value and vice-versa. These gyrations help explain why the price of AFGC moves up and down (and mostly down for the past couple of years).

The underlying’s creditworthiness

This debenture is unsecured, which means it is not backed by any form of collateral; investors must rely on the creditworthiness and financial viability of the issuer.

American Financial is an insurance holding company, with subsidiaries in the property and casualty [P&C] insurance business, according to its 10-K for 2022. More specifically, it focuses on “specialized commercial products for businesses.”

{kind=link}

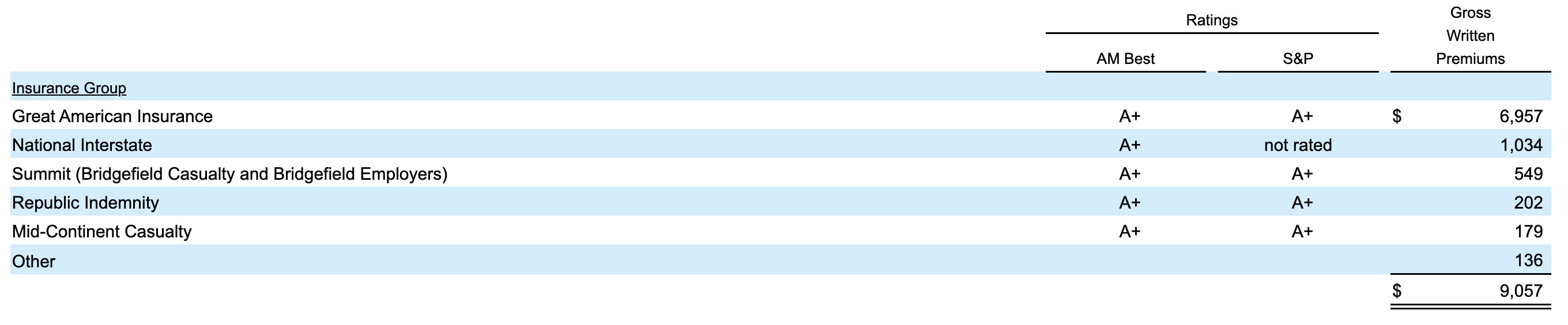

Some parts of the firm have been in business for more than 150 years. As this table from the 10-K shows, each of its subsidiaries has an excellent rating from A.M. Best, the leading name in assessing insurance companies and the S&P organization:

{kind=link}

With the highest possible rating for each of its subsidiaries, American Financial is considered strong and stable.

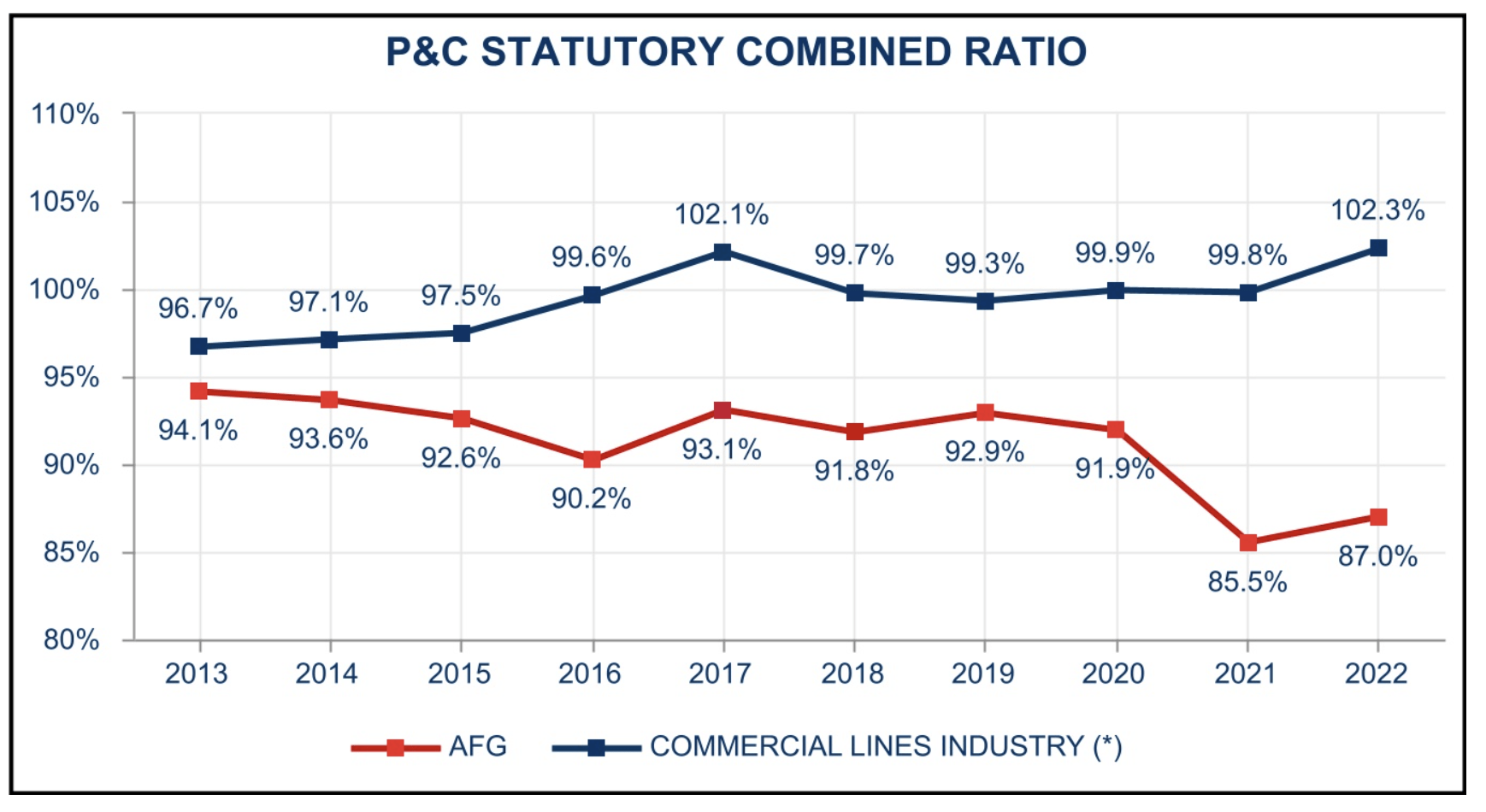

Another useful tool for rating P&C companies is the combined ratio, which provides a measure of operational performance. A ratio of less than 100 indicates a company is earning profits, while a rating of more than 100 indicates it is suffering losses.

For the third quarter of 2023 , American Financial reported that its combined ratio was 92.2%, meaning it was profitable. That’s consistent with its statutory 10-year average, as reported in the 10-K (in this case, lower is better):

{kind=link}

The chart above measures statutory combined ratios, which take in an insurer’s overall results (operations plus investment performance).

Above, we touched on the company’s performance from a returns perspective, and its B+ profitability grade. To consider this from a financial viability perspective, we can look at five-year profitability returns for ROCE and ROTC:

- Return on common equity: 15.42%, which is 41.79% higher than the financials sector median.

- Return on total capital: 9.76%, which is 34.90% more than the sector median.

Taken together, the data indicate American Financial is a strong financial performer and that it has outperformed the financials sector for the past five and 10 years. Investors can assume the underlying is a creditworthy and financially viable firm.

Maturity date

When the debenture was first issued, its maturity date was 40 years away: December 15, 2059. Now, of course, that’s down to 36 years, which is how long investors can expect to receive this rate if they keep the stock.

However, there is a chance that the issuer, American Financial, might opt for redemption. Should interest rates drop significantly, a redemption becomes increasingly likely. For example, the company explained in its AFGC prospectus that it would use a portion of the net proceeds from this issuance to redeem its 6.25% debentures maturing in September 2054.

Given the current trend of interest rates, the company may decide to refinance by taking out one or more of the higher-yielding baby bonds. So, while AFGC yields less than AFGB and AFGD, it is less likely to be redeemed.

Valuation

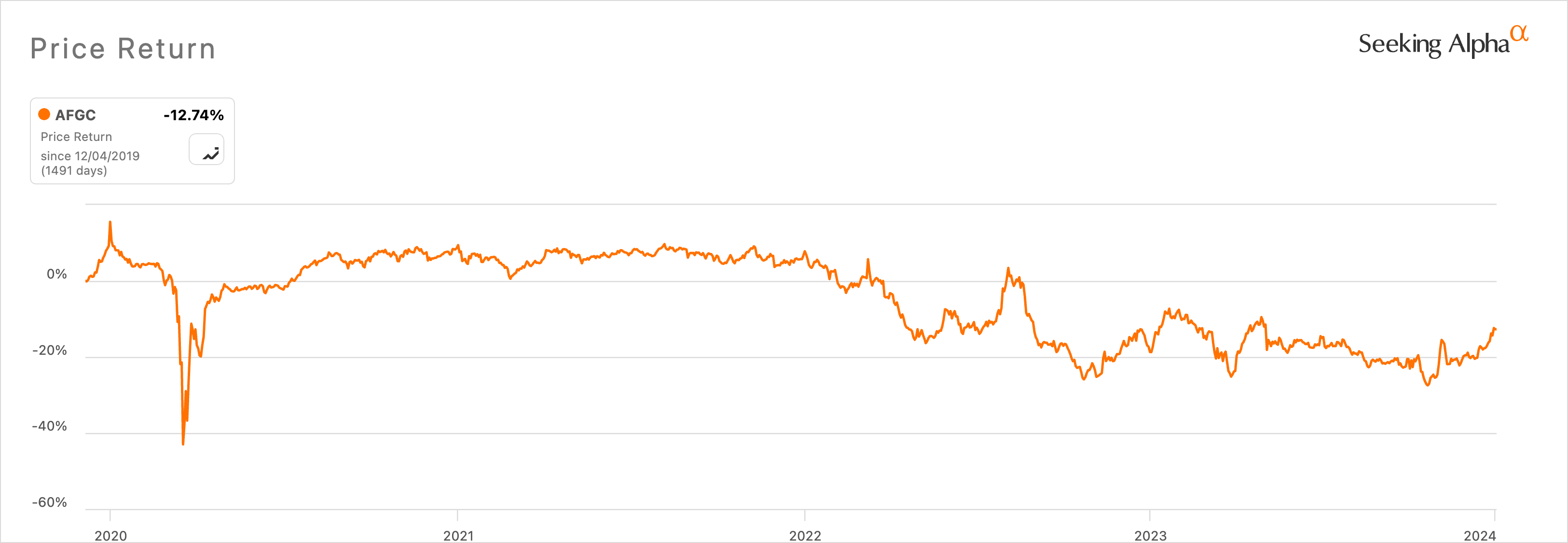

The following price chart illustrates recent economic history. AFGC traded in the $22.00 to $24.00 range soon after going public in December 2019. Not long after that, COVID-19 hit, pushing down all stock markets (and AFGC). However, value investors rushed back into the market when prices stumbled deeply and markets, along with AFGC, recovered much of their lost value. Just as we thought economic conditions were getting back to normal as COVID faded, interest rates began rising sharply, thanks to supply chain woes, Russia’s invasion of Ukraine, and other factors. That depressed the prices of many securities, but as aggressive anti-inflation measures took hold, stocks and other securities recovered too:

{kind=link}

At the close of trading on January 2, 2024, the price of AFGC units stood at $22.12, near the bottom of the range established earlier. While there have been significant gains recently, a basic technical indicator (the 50-day simple moving average has crossed above the 200-day simple moving average) suggests further gains may be possible.

The fundamentals indicate the same trajectory:

- P/E GAAP [TTM]: 11.69, which is 7.10% higher than the sector (financials) median.

- EV/EBITDA [TTM]: 8.21, which is 28.69% lower than the sector median.

- Price/Sales [TTM]: 1.39, which is 49.19% below the sector median.

- Price/Sales [FWD]: 1.54, which is 43.13% lower than the sector median.

Three of these four metrics indicate AFGC is undervalued, and undervalued by significant margins.

Based on this information and data, I would estimate the debentures are worth 10% more than $22.12. This would make AFGC worth $24.33 per share, which I consider reasonable given its price history over the past four years.

Conclusion

Income investors are likely to find the AFGC 5.125% debentures attractive. At its current yield of 5.77%, it is more than double the financial sector’s median yield of 3.32%. Its creditworthiness and financial viability are both strong, thanks to its ongoing profitability. It has a long runway, unless American Financial decides to replace it with something that costs it less. And, I estimate AFGC is currently undervalued by 10%.

For further details see:

American Financial Group: A Yield Of Over 5.00% On Debentures