COLD - Americold: A Fairly Valued Promising Business

2023-12-12 22:21:03 ET

Summary

- Americold is in the business of providing temperature-controlled storage and value-added services.

- Though the prospects look good, and no significant headwinds appear to be present, the REIT is currently fairly valued.

- Due to the lack of a margin of safety and the relatively low dividend yield, investors may want to be patient with buying the stock.

Americold Realty Trust, Inc. ( COLD ) is a prominent global player in the cold storage industry, providing temperature-controlled storage and value-added services. This REIT mainly acquires, develops, and leases temperature-controlled warehouses that are designed for the storage of temperature-sensitive items, including pharmaceuticals and food products.

Though I am intrigued by the prospects here, as the title says, COLD shares are fairly valued. As I am reluctant to invest in a REIT that is not undervalued, I believe that interested investors should wait if they find comfort in a margin of safety as I do. On top of that, the dividend yield is too low for me and I suspect that it may be not high enough for many investors in the current environment. Regardless, I wanted to dive into the aspects that make Americold's business promising in case a discount is ever offered by the market. I'll also get into the specifics of valuation to help you understand where I'm coming from. Let's take things from the start.

Portfolio

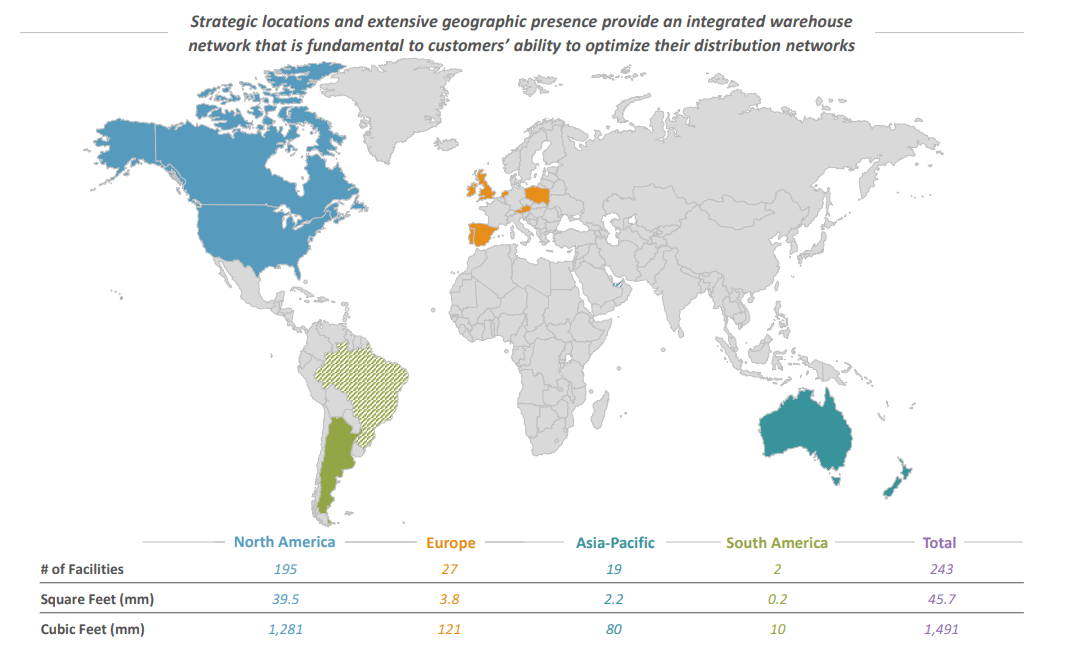

This self-managed REIT manages a global portfolio of 243 warehouses, totaling a volume of approximately 1.5 billion cubic feet. The portfolio includes 195 warehouses in North America, 27 in Europe, 19 in Asia-Pacific, and 2 in South America.

Obviously, if one were to seek exposure to a cold storage provider, Americold's portfolio seems exceptionally diversified from a geographical standpoint:

{kind=link}

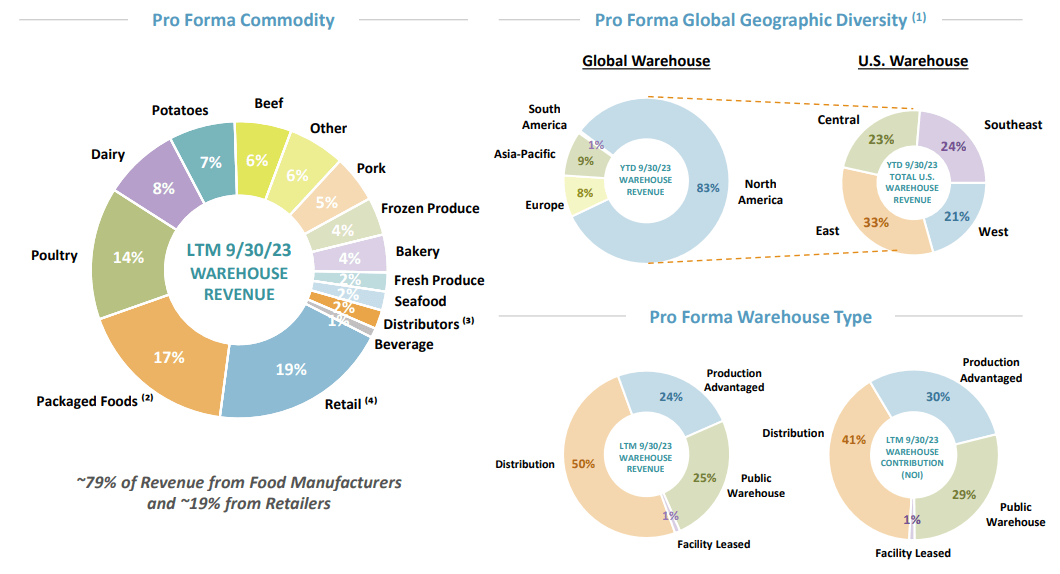

But diversification is also present in the type of clients the REIT serves; around 80% of its revenue comes from food manufacturers and almost 20% comes from retailers. At the same time, it's further diversified when it comes to the warehouse type:

{kind=link}

While I find that its 25 largest customers accounting for 48% of its customer base can seem risky, they have been with the company for an average of about 36 years. Moreover, 15 of them are investment grade.

Performance

First of all, Americold's economic occupancy for its same-property portfolio reached 84% during the three months ended on September 30, 2023, marking a growth of 345 basis points compared to the corresponding period in the previous year. Also, its average physical occupancy stood at 75.8%. For the same-store assets, these are very low rates so there's definitely a large margin for improvement here.

When it comes to operating performance, the REIT has experienced decent revenue growth in a relatively short period of time, but its operating income and FFO performance didn't follow:

However, more recent results are very good when compared to the recent past. Below, you are looking at the change between the most recent figures annualized and their corresponding average annual ones as reported in the REIT's last 3 fiscal years:

| Rental Revenue Growth |

| 21.79% |

| Same-Property Cash NOI Growth |

| 24.17% |

| AFFO Growth |

| 21.93% |

However, the fundamental growth hasn't yet been reflected in the price performance, with COLD's price still oscillating up and down after realizing a confident increase up until 2020:

Leverage

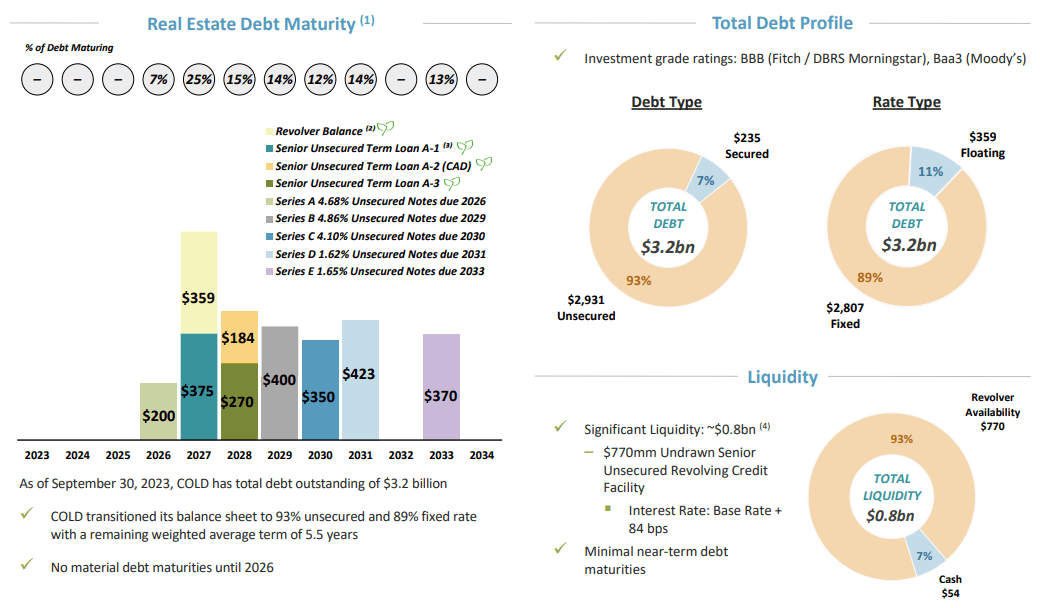

As for the use of leverage, Americold has decreased it from around 50% in 2019 to 36.44% today. Its debt-to-EBITDA ratio sits at 8.27 times, which I see as acceptable. However, its TTM interest coverage at 0.22x is concerning and something to keep an eye on:

Fortunately, its revolving credit facility, unsecured notes, and term loans cost a weighted average interest rate of 4.02%.

On top of that, there are no significant maturities until 2026, only 11% of its debt has floating rates, and just 7% of it is secured, providing a lot of flexibility.

{kind=link}

Prospects

It's good to know that the market Americold is in has significant growth potential. The cold chain logistics market was valued at $280.23 billion in 2022 and is expected to grow at a CAGR of 15.5% until 2031 when it's expected to reach ~$1 trillion.

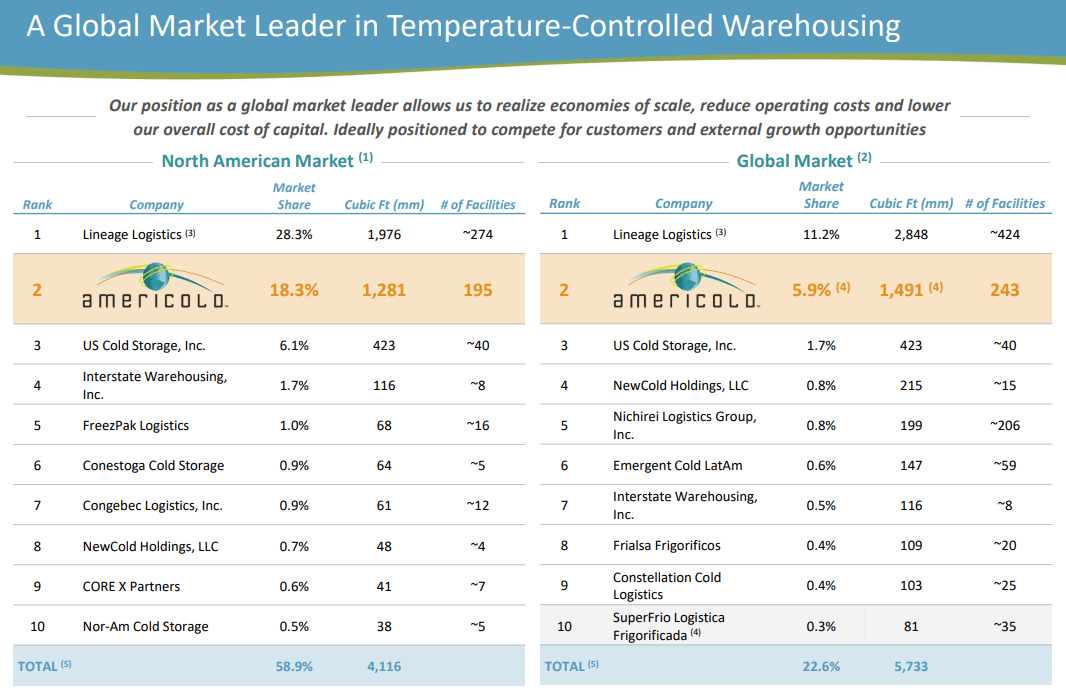

COLD seems like the right vehicle to position oneself for such growth since, based on market share, it's ranked second place in both the North American market and globally when it comes to temperature-controlled warehousing:

{kind=link}

That's the long term though. In the near term, I believe that any alleged price pressure that may have been applied by the aggressive Fed hikes in the recent past on COLD could be alleviated. We have already seen the likely reaction by the market when the rate was held steady recently:

And it's very likely that rates will remain unchanged in the next meeting on December 13, potentially providing further support for the recent COLD shares' repricing.

Management

Before we go into valuation, I'd like to briefly note some things you should be aware of related to management:

-

Americold's CEO, George F. Chappelle Jr. was paid $7,689,546 in 2022 (also accounting for stock awards); the highest compensation within the company

-

As of the end of the fiscal year 2022, 0.24% of COLD stock was held by executives

-

There have been no recent COLD share acquisitions by insiders; just sales and stock awards

In my view, a compensation scheme that allows for such potentially high figures, very low insider equity, and just share dispositions most likely enabled by stock awards, are not obvious red flags. But they fail to paint a great picture of management quality.

Many more factors should be considered when assessing that quality, but I think that quickly observing some key shareholder-interest alignment indicators like the above can give an investor the ability to see if they would like to be "in business" with a company. You be the judge.

Dividend & Valuation

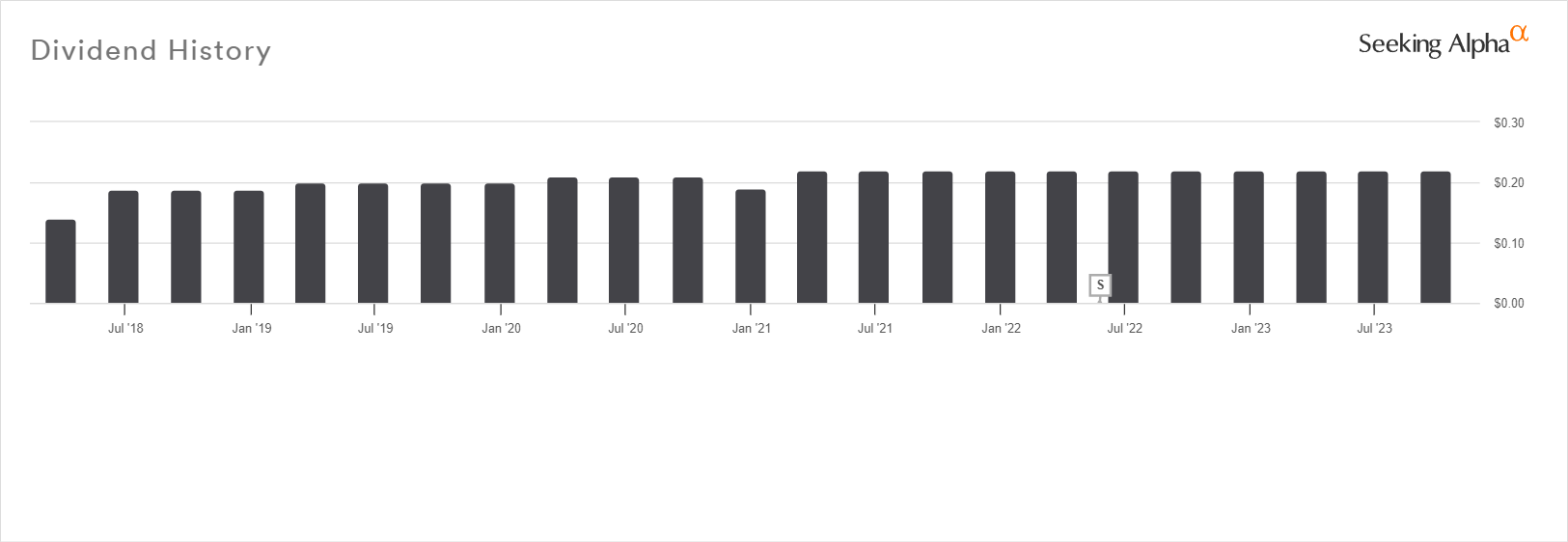

The REIT pays a quarterly dividend of $0.22 per share, which results in a forward yield of 3.07%. For what is worth, the dividend is relatively safe. Although we don't have a long track record of payments or a definite growth trend, the payout ratio based on the last AFFO figure annualized is 70.75%.

{kind=link}

Obviously, when other less risky options offer a significantly higher yield like the 1-Year Treasury Bill bond, one needs to consider what else COLD may have to offer here.

If it's a further increase in the price of COLD you seek, I believe that there are better opportunities elsewhere. The shares are currently trading at an implied cap rate of 6.17%, which suggests a more or less fair valuation.

Even if we assume that potential buyers of cold-storage warehouses currently don't demand a cap rate premium in regards to the broader industrial real estate market averages, we would still need to use a ~6% cap rate as the appropriate one here; remember that debt financing is still expensive so anything below 6% would be unreasonable.

Risks

In consequence, the potential narrow margin of safety at best and its non-existence at worst here may realize an opportunity cost. Remember that the dividend yield is too low to offset a potential missed opportunity.

Speaking of dividends, the distribution record doesn't make a dividend cut unlikely as I would personally have it when it comes to investing in REITs. On the one hand, I can appreciate a prudent allocation of capital, but the reluctance to increase the dividend doesn't exhibit confidence.

Verdict

For these reasons, I assign a HOLD rating and would reconsider COLD if it reaches anywhere close to $20 per share. Such a price point would still imply a low yield, but a nearly 20% discount to NAV based on a conservative assumption of a 7% cap rate as the appropriate one.

What are your thoughts? Do you own COLD or intend to? Feel free to let me know below in the comments. Thank you for reading.

For further details see:

Americold: A Fairly Valued Promising Business