COLD - Americold Realty Trust: Still Too Hot For Me To Touch

2024-01-12 17:04:06 ET

Summary

- Americold Realty Trust, Inc. operates as a REIT that owns and leases temperature-controlled warehousing and provides transportation services.

- The company's financial performance has been mixed, with a decline in revenue and bottom line results due to multiple factors as of late.

- Despite its position as a major player in the temperature-controlled warehouse market, shares of Americold Realty Trust are expensive and not an attractive investment opportunity.

My constant search for interesting companies with interesting business models has led me to a wide variety of firms over the years. But few of them, operationally speaking, have been as interesting as Americold Realty Trust, Inc. ( COLD ). Those who follow the company closely understand that it operates as a real estate investment trust, or REIT, that owns and leases out temperature-controlled warehousing. It also engages in ancillary services like transportation for temperature-controlled products. However, as interesting as an investment opportunity it might be, it's important to keep our own interests separate from whether or not the firm in question makes for an attractive investment or not.

And that is where, unfortunately, my issue with Americold Realty Trust comes up. Back in September of last year, I decided to see whether or not the company made sense for investors to buy into. Although I found the business model interesting, and shares of the firm had risen significantly over the prior few months leading up to that point, financial performance had been mixed and shares looked rather pricey. This led me to rate the business a "hold" to reflect my view at the time that the stock would be unlikely to outperform the broader market for the foreseeable future.

So far, shares have actually performed a bit worse than I anticipated. Since the publication of that article, the stock has generated a loss for investors of 5.1%. By comparison, the S&P 500 (SP500) has popped up by 8.2%. Even with this decline, however, shares look quite pricey. Although relative to similar firms, units do look more or less fairly valued. But as a value investor at heart, this is not enough to get me optimistic enough to upgrade the firm just yet.

Chilly times

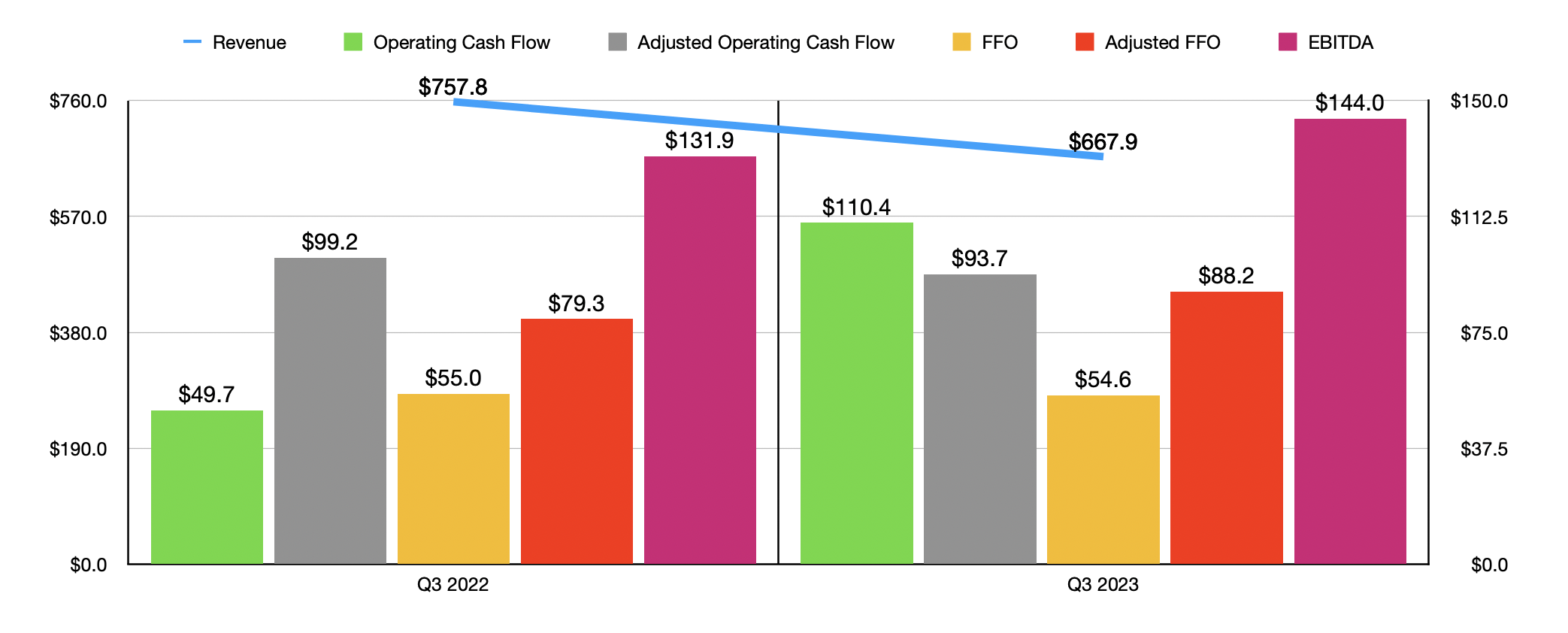

Every investor wants the investments that they make to sizzle, the sooner, the better. After all, we invest in order to make a profit. So when our investments turn cold, the end result is disappointing. This is especially true at times when the broader market takes a different route as I demonstrated to be the case since I last wrote about Americold Realty Trust in September 2023. A lot of the problems associated with Americold Realty Trust involve revenue. During the third quarter of the 2023 fiscal year, for instance, management reported revenue of $667.9 million. That's an 11.9% plunge compared to the $757.8 million the company reported the same time one year earlier.

{kind=link}

This increase in sales came about even as revenue associated with the Warehouse segment of the company expanded from $599 million to $602.6 million. Warehouse services revenue actually dropped about 4.3% during this window of time, though this was more than offset by a 7% rise in rent and storage revenue.

It is worth noting, however, that revenue would have grown even more, to $605.3 million, had it not been for foreign currency fluctuations. $2.8 million of the increase in revenue that the company achieved was driven by recently completed expansion and development activities, as well as an acquisition that the business made of a cold storage facility in Australia. This was offset to some extent by a decline in the number of non-same store sites from 21 to 19. On a same-store basis, the firm benefited from an increase in occupancy from 80.5% to 84% and from a rise in rent and storage revenue per 'average economic occupied pallet' from $59.45 to $61.52 on a constant currency basis.

Even though the Warehouse segment performed well, the company saw weakness elsewhere. For starters, the Transportation segment reported a plunge in revenue from $76.4 million to $55.6 million. This drop, amounting to roughly 30% year over year, was driven mostly by the company's decision to strategically transition to a third-party logistics model, as well as by weakening transportation demand because of macroeconomic issues. Even worse was the Third-Party Managed segment. Revenue plunged from $82.4 million to $9.7 million.

But this is not all that awful, since management made the conscious decision to exit a relationship that it had with its largest domestic customer during that time. I can only imagine that this decision was made because of a disagreement on what appropriate rates would be for the company's services moving forward.

{kind=link}

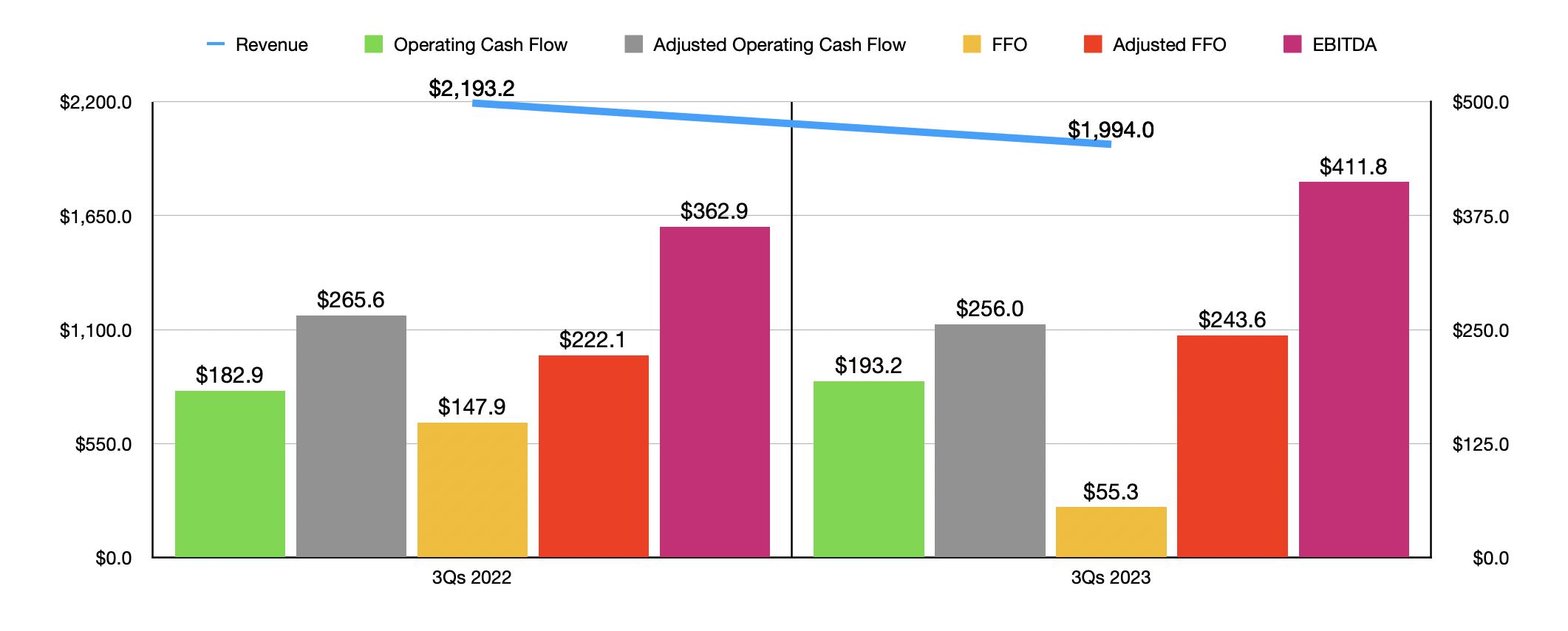

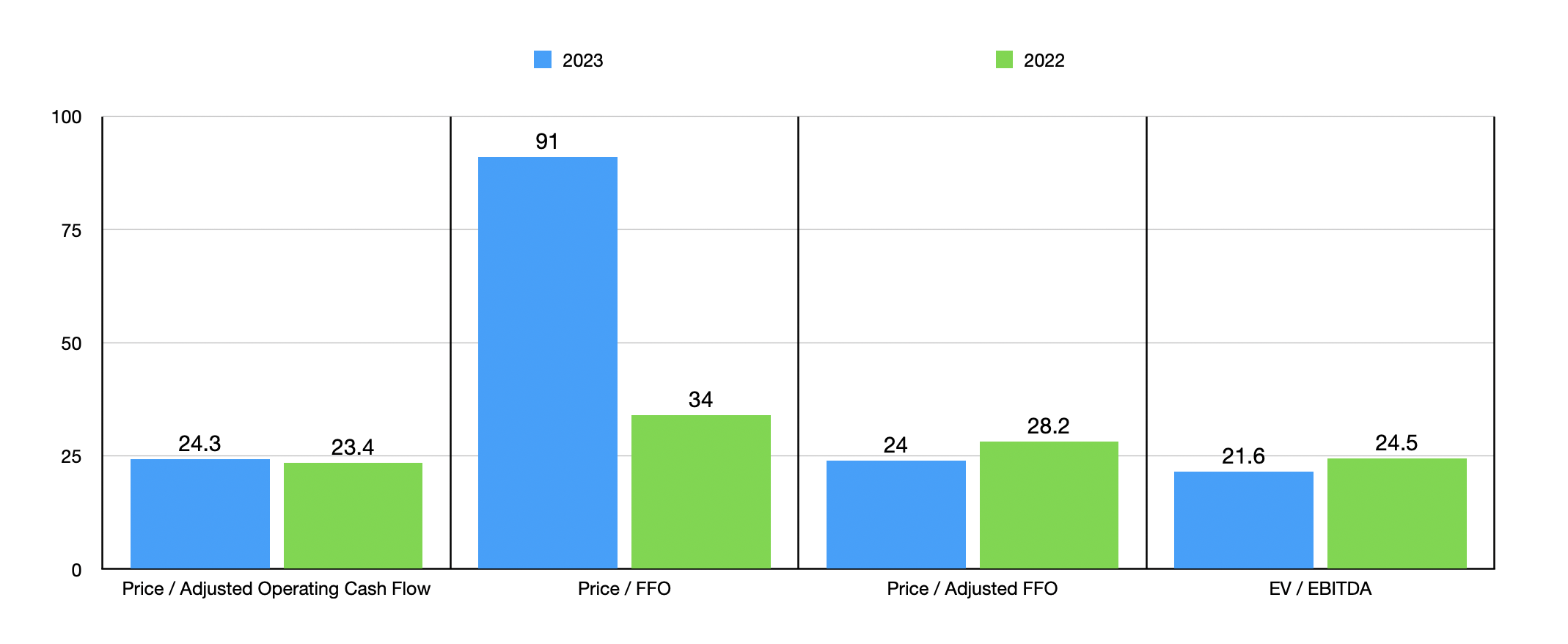

Even though revenue for the enterprise took a hit, operating cash flow shot up from $49.7 million to $110.4 million. If we adjust for changes in working capital, however, we would get a small decrease from $99.2 million ten $93.7 million. Other profitability metrics were rather mixed. For starters, FFO, or funds from operations, also declined, dropping from $55 million to $54.6 million. But on an adjusted basis, it increased from $79.3 million to $88.2 million. Meanwhile, EBITDA for the business expanded from $131.9 million to $144 million. As you can see in the chart above, the same kind of mixed financial performance seen in the third quarter of 2023 was very similar to what was seen for the first nine months of 2023 relative to the same time of 2022 as a whole.

{kind=link}

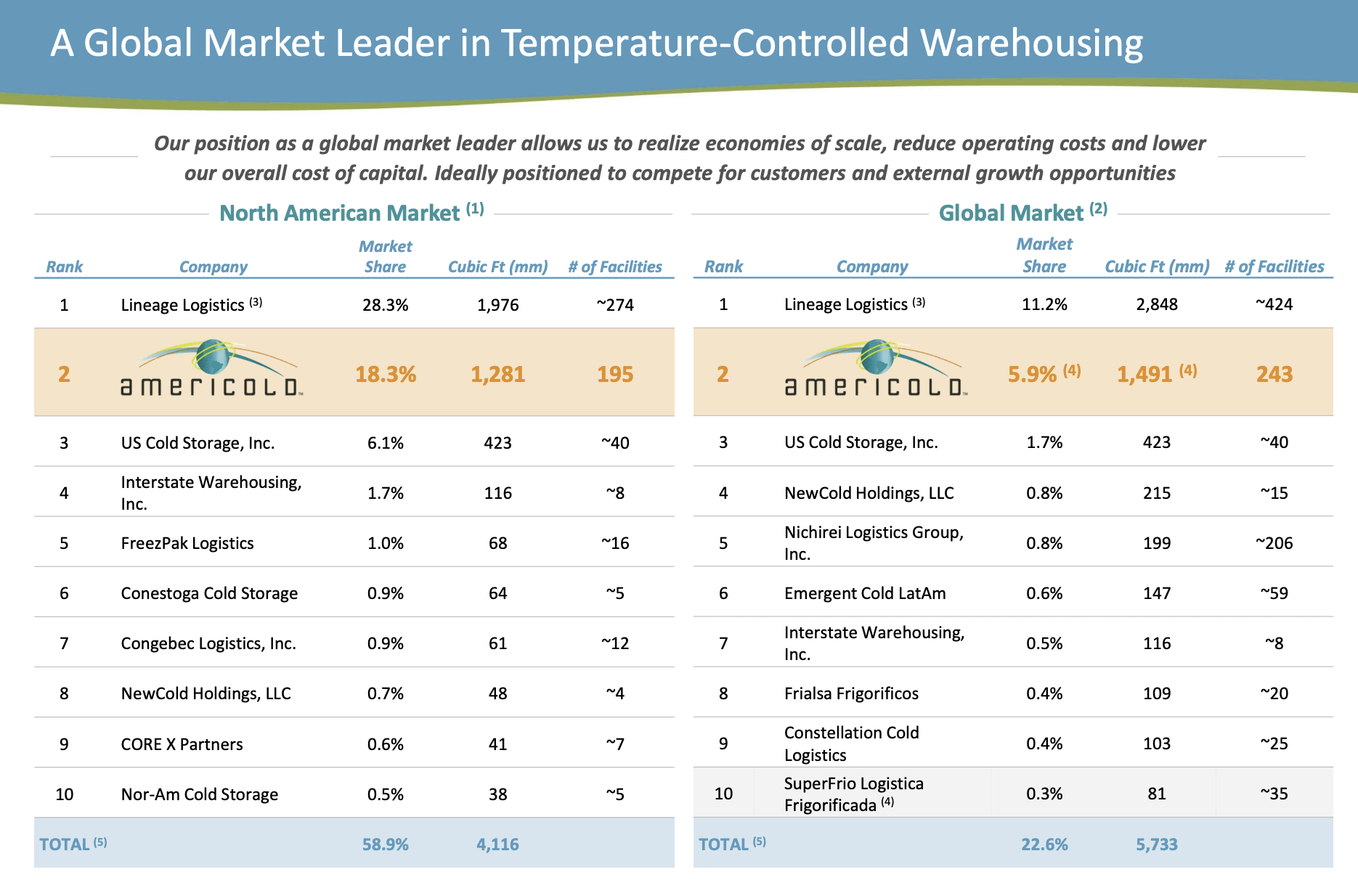

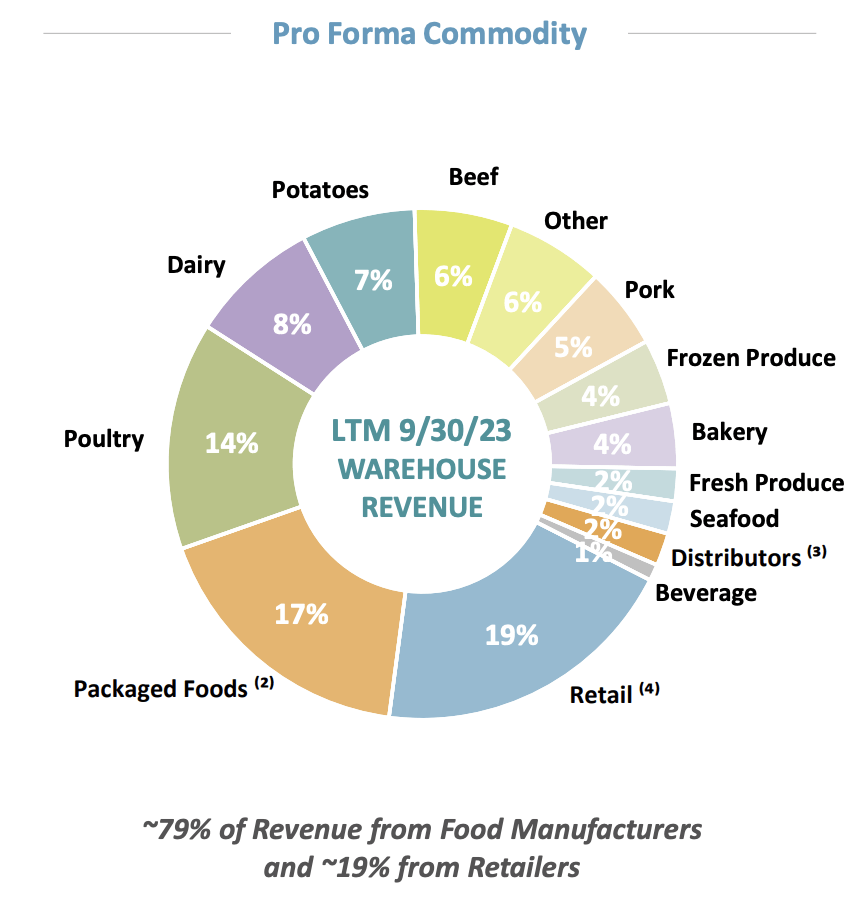

Despite the drop in revenue, much of which was driven by management's own choices, Americold Realty Trust continues to have its sights set on maintaining its position as a major player in the temperature-controlled warehouse market. Globally, the firm has 243 facilities that comprise 45.7 million square feet of space. It's the second-largest player in the North American market and the second-largest player globally that focuses on this particular niche. Its global market share is about 5.9%, while its market share in North America is an astounding 18.3%. And with almost all the products that are stored in its facilities being perishable goods like dairy, poultry, potatoes, beef, and more, with 79% of revenue in all coming from food manufacturers, it's clear that demand for its services will likely always exist.

{kind=link}

But this doesn't necessarily mean that shares make for an attractive opportunity at this time. Management forecasted that adjusted FFO per share should be between $1.24 and $1.30 for 2023. This would imply an adjusted FFO of around $353.2 million at the midpoint. That should translate to an FFO of around $93.1 million given the recent weakness that we have seen on that front covering the first nine months of 2023 relative to the same time of 2022. Adjusted operating cash flow should be much higher at about $348.7 million, while EBITDA should be somewhere around $536.3 million.

{kind=link}

Using these figures, I was able to value the company as shown in the chart above. As you can see, the stock is rather expensive using almost any of the profitability metrics. Relative to similar firms, however, the stock is probably closer to being fairly valued. You can see what I mean by looking at the table below. In it, I compared Americold Realty Trust to five similar firms. On a price-to-operating cash flow basis, three of the five companies ended up being cheaper than our prospect. This number drops to two of the five if we look at the picture through the lens of the EV to EBITDA multiple.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Americold Realty Trust |

| 24.3 |

| 21.6 |

| EastGroup Properties, Inc. ( EGP ) |

| 23.8 |

| 25.7 |

| First Industrial Realty Trust, Inc. ( FR ) |

| 22.9 |

| 18.5 |

| Rexford Industrial Realty, Inc. ( REXR ) |

| 29.4 |

| 27.5 |

| STAG Industrial, Inc. ( STAG ) |

| 18.0 |

| 17.4 |

| Terreno Realty Corporation ( TRNO ) |

| 29.1 |

| 23.6 |

Takeaway

As much as I want to be a fan of Americold Realty Trust from an investment perspective, the picture just doesn't make sense to me. Shares are expensive on an absolute basis, even though they are closer to fairly valued relative to similar entities. As a value investor, my goal is not to buy shares of companies that look fairly valued. Rather, it's to buy them at an attractive discount. And unless something changes rather drastically, I just don't see that scenario playing out here. Because of that, I've decided to keep the company rated a "hold" for now.

For further details see:

Americold Realty Trust: Still Too Hot For Me To Touch