POWW - AMMO: A Complete Makeover Is Needed

2023-11-22 06:40:27 ET

Summary

- AMMO is undergoing some strategic changes.

- I do not believe these changes are enough to do the trick.

- The company will likely continue to bleed cash for a very long time on preferred stock dividends.

- Stock repurchase plan is hardly utilized.

- I now rate AMMO stock a sell.

AMMO, Inc. ( POWW ) ammunition sales plummeted by an astounding ~68% from Q1 of calendar year 2022 to Q3 of calendar year 2023. In the same period, the company's Gunbroker marketplace revenues plunged by ~30%. Based on the quarterly call for the period ended June 30, 2023 (company's Q1 of FY 2024) it seems as if the company is not in position to compete effectively in the ball ammunition space in the foreseeable future and it does not seem casing sales could grow to such an extent that would lead the company to meaningful profitability. Further, I doubt the improvements to the Gunbroker platform, after having been around for almost 25 years, could lead to a dramatic increase in revenues. In my opinion, without a complete makeover, POWW will find it very hard to generate any meaningful profit (if at all) in the foreseeable future. Therefore, I now rate POWW stock a sell.

AMMO, Inc. is involved in the design, production and marketing of bullets and bullets' components and, in addition, it owns and operates GunBroker.com, an online auction-based platform, for the sale of guns, ammunition, and related accessories.

According to the company's latest 10-Q , in the quarter ended September 30, 2023, compared to the same period in the previous year, revenues went down by a staggering ~29%. Albeit the substantial decline in revenues, operating expenses went up by ~28%.

Ammunition sales plummeted ~47%, and marketplace revenues declined by ~14%, while casing sales were moving in the opposite direction soaring ~47%. Casing sales, however, is still the smallest income segment, comprising in the quarter ended September 30, 2023 only ~18.5% of total revenues.

Preferred Stock Effect

Aa mentioned in the latest 10-K , the Company issued in May 2021 1,400,000 shares of Series A Cumulative Redeemable Perpetual Preferred Stock. The Company pays every year more than $3 million as dividends on these shares of Preferred Stock, reducing the cash available to the Company for buybacks, acquisitions or dividends to the common stockholders. The Company has a strong balance sheet but has yet to be able to exhibit an ability to generate sustainable profits and it seems as if the dividends on the Series A Preferred Stock are going to continue to be paid long into the future causing the Company to bleed cash.

The Suspended Spin-Off

On August 15, 2022 the Company notified of its plan to separate into two publicly traded companies through spin-off. The announcement of the planned spin-off triggered the initiation of a proxy contest , whereby Steven Urvan, the former owner of "Gunbroker", and the Company's largest shareholder, sent a letter to the Company offering a slate of directors for election to the Company's board of directors in the 2022 annual meeting of shareholders. Shortly thereafter, tensions continued between supporters of the spin-off and those opposing it.

These tensions ended up in a settlement agreement , which included, among other things, an agreement to suspend the spin-off plan and to increase the size of the Company's board of directors from 7 to 9 directors, where two nominees of Mr. Urvan will be added to the board; and the establishment of a special committee for the selection of a new CEO to the Company. Mr. Urvan agreed to have his proposal to replace board members withdrawn and to vote for a certain period of time defined in the settlement agreement in accordance with the board's recommendations with respect to certain matters (and subject to certain exceptions).

Gunbroker

Gunbroker was launched in 1999. Jared Smith, the new CEO of the Company provided, among other things, in a letter to shareholders dated July 31, 2023, details about the plans with respect to Gunbroker. I'm quite skeptic, however, with Gunbroker having been around for almost 25 years and with a very large subscriber pool, there is much room left for growth there.

That same letter, included the following:

Additionally, we will continue to create leaner and more efficient operations…

That begs the question - how small does the Company intend to go for the sake of increasing its margins?

Insiders' Activity

When looking at insiders' activity it is important to see how shares were acquired. There is a big difference, for instance, between a director getting shares as part of his/her compensation package and a director buying shares in the open market or in a privately negotiated transaction - the former gives no indication as to that director's belief in the future of the company, while the latter, may give important indication in that regard, and the larger the size of the acquisition is, generally, the greater the sign of that director's belief in the future of the company.

Having said that, the only common stock acquisitions I find worth mentioning are the ones by the current CEO, Jared Smith, who acquired 50,000 shares at $2.04 per share on February 22, 2023 , another 55,000 shares around $1.60 per share on March 23, 2023 and another 5,000 shares at $1.97 on August 18, 2023 (110,000 shares altogether) for a total purchase price of around $200,000. However, to me it is quite discouraging that I found no reports of purchases of shares of the Company's common stock in the last year by any of the other directors and officers in the open market or in privately negotiated transactions. Moreover, the purchases by the Executive Chairman, Fred Wagenhals, of Series A Preferred Stock on August 24 & 25, 2023 is not a good sign in my book as the interests of common stockholders and Series A Preferred stockholders are not aligned. I would expect a director or officer who believes in the future of the Company to purchase shares of common stock rather than shares of Series A Preferred Stock.

Slow Pace Of Buybacks

On March 28, 2023 the Company issued a press release announcing that its share repurchase plan of up to $30M is extended until February 2024 (but may be suspended or discontinued at any time). The Company also noted in that press release that ~$29.7M is still available under the buyback program as disclosed in the Company's 10-Q filed on February 14, 2023. In its 10-Q filed on August 9, 2023 the Company reported that during the quarter ended June 30, 2023 it repurchased 738,831 shares of common stock. While this was a substantial increase compared to the meager scope of buybacks in the quarters ended March 31, 2023 (118,328 shares) and December 31, 2022 (150,000 shares), it still merely represents 0.6% of the outstanding shares of common stock as of August 4 (as indicated in the 10-Q filed on August 9, 2023).

As indicated in its latest 10-Q, the Company returned to an extremely slow pace of buybacks repurchasing only 197,798 shares. So, about a year and a half after the repurchase plan was launched, still more than 90% of the maximum dollar value under it (based on the closing price of the stock on September 29, 2023 as reported by Yahoo Finance ) has yet to be utilized. Therefore, thus far, buybacks have been made at a very slow pace.

Another way to illustrate how slow is the pace at which stock repurchases are made, is by looking at the amended and restated employment agreements of the Company's Executive Chairman and CEO, according to which they are entitled to an annual issuance of 720,000 and 133,333 shares of common stock, respectively, and, in addition, the Executive Chairman is entitled to a one-time issuance of 300,000 shares of common stock. Therefore, the scope of buybacks since the repurchase program was launched does not even cover the dilution caused to common shareholders by the foregoing issuances of shares.

As reported in the Company's 10-Q for the quarter ended December 31, 2021, as of February 11, 2022, just few days after the repurchase plan was first announced, the number of common shares outstanding was 115,526,404. As reported in the Company's latest 10-Q, as of November 8, 2023, the number of outstanding common shares was 118,460,743. So, since the stock repurchase plan was initiated, not only that the number of outstanding common shares was not reduced, but it even grew by ~2.5%.

Strong Balance Sheet, But What About Profitability?

The Company has a solid balance sheet, with little liabilities and a strong cash position. The problem is that the Company has yet to prove it has the ability to return a profit on a continuous basis. Now, that the Company is focused on implementing some changes aimed at improving its margins, I doubt that, given the much-reduced scope of revenues, it will be able to generate any meaningful profit (if at all) in the foreseeable future.

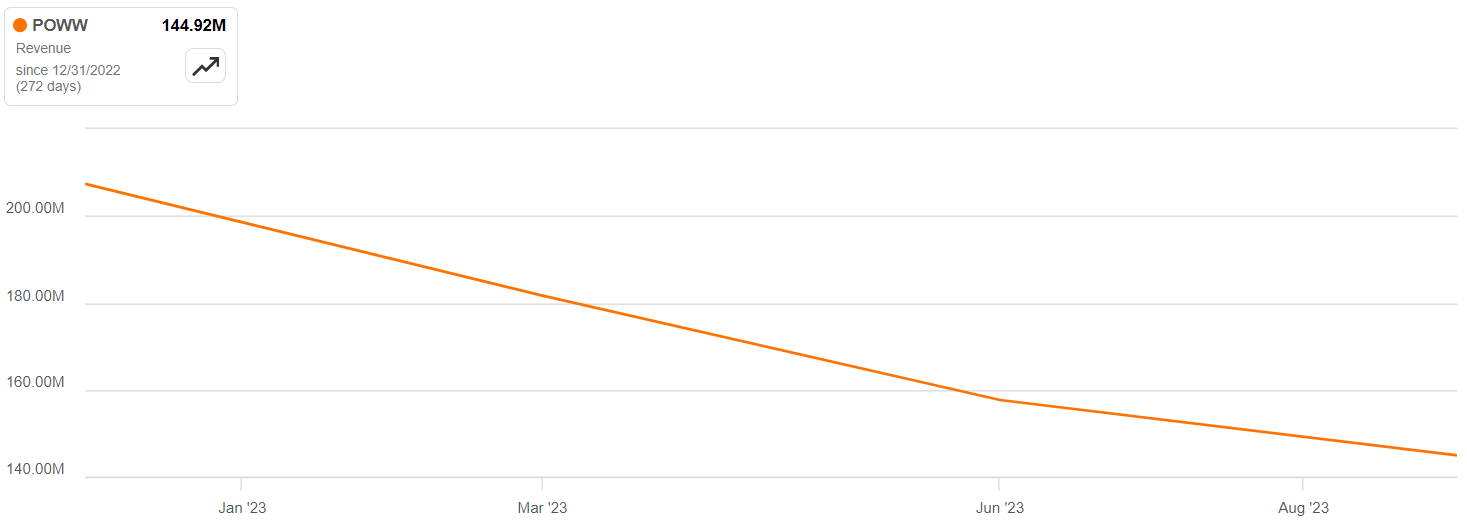

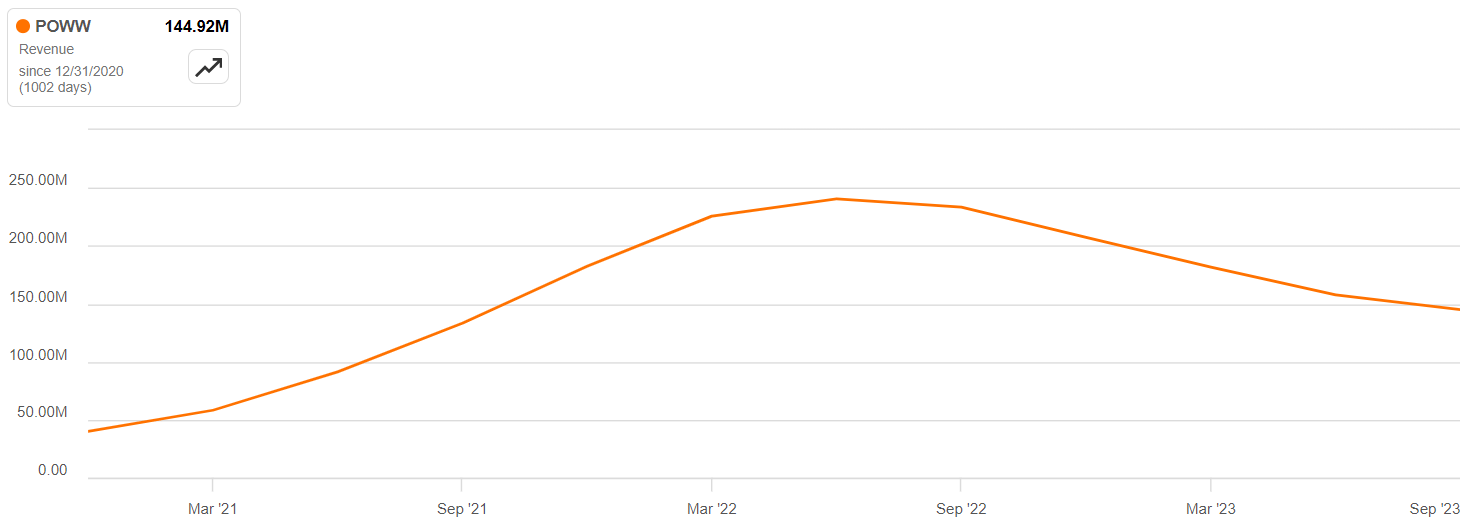

1 year revenues chart (SA 11-16-2023) 3 years revenues chart (SA 11-16-2023)

{kind=link}

{kind=link}

The Company may redeem the Series A Preferred Stock starting on May 18, 2026 (with an exception to a Change of Control allowing earlier redemption). According to the latest Q, there are 1,400,000 shares of Series A Preferred Stock outstanding as of September 30, 2023. Each share of Series A Preferred Stock is redeemable at $25. That means that in order to redeem the entire Series, the Company will need to spend $35 million, which is roughly 70% of its entire cash position as of September 30, 2023. So should the Company not be able to generate meaningful profits on a continuous basis until then, it is very unlikely it will redeem the Series A Preferred Stock and would need to keep paying more than $3 million each year to the Preferred Stock holders, which over time, again - if no way is found to generate meaningful profits on a continuous basis, will drag the Company down.

Performance In The Foreseeable Future

The Company's CEO, Jared Smith said in the Company's call regarding its Q1 2024 that:

The Ammunition division of AMMO Inc. created positive margins for the first time since June of 2022. We reported $20.3 million in revenue with a 9.5% gross margin, up from negative 8.6% in the previous quarter. While this is a major win, we anticipate strong headwinds for loaded ammunition sales for the next 2 quarters.

And, in addition, that:

…ammunition sales continued to decline and margin compresses across the board for the rest of the nonvertically-integrated players…today, our cost to produce ball ammo is somewhere between $2.20 to $2.40 per 1,000 and the price at retail was $2.05. We just can't play there...but we can sell the brass casing for a 20% to 35% margin.

The Company has dramatically lowered the scope of its ammunition sales in the last few quarters and, given the note above, it is reasonable to assume it may continue doing so, at least in the foreseeable future.

Below is a projection I prepared, which, in my opinion, depicts a very optimistic scenario for average P&L quarterly results for the next 4 quarters. Even in that scenario, the Company makes only a very modest profit. Such profit gives the Company a P/E ratio of ~41 (based on the closing price on November 17, 2023 as reported by Yahoo Finance and on 118,460,743 common shares as of November 8, 2023, as reported in the Company's latest Q), which is very high for what I believe lies ahead for it in the foreseeable future.

Following are the assumptions I used: casing sales: more than doubles, comprising 35% of overall revenue and having a gross margin of 35%; ammunition sales: go down by 20% and having a gross margin of -1.77%; marketplace sales: go up by 20% and having a gross margin of 86.92%. For operating expenses, I used the lowest quarterly number in the last 4 quarters; for other income (expenses) I used the last full fiscal year number and divided it by 4; for interest expense I used the one reported in the latest Q filed.

| Q ended Sep-2023 |

| Future Q |

| Ammunition sales |

| $15,516,589 |

| $12,413,271 |

| Marketplace sales |

| $12,474,716 |

| $14,969,659 |

| Casing sales |

| $6,381,081 |

| $14,744,655 |

| Revenues |

| $34,372,386 |

| $42,127,585 |

| Cost of revenues¹ |

| $26,084,120 |

| $24,175,550 |

| Gross profit |

| $8,288,266 |

| $17,952,035 |

| Gross profit % |

| 24.11% |

| 42.61% |

| Operating expenses |

| $17,107,413 |

| $15,394,919 |

| Other income (expense) |

| -$321,341 |

| $6,295 |

| Interest expense |

| $212,314 |

| $212,314 |

| Preferred stock dividend |

| $782,639 |

| $782,639 |

| Net income (to common shares) |

| -$8,277,936 |

| $1,568,458 |

1 Future Q cost of revenues ((COR)) breakdown:

| Ammunition (101.77%) |

| $12,632,986 |

| Marketplace (13.08%) |

| $1,958,539 |

| Casing sales (65%) |

| $9,584,026 |

| Total COR |

| $24,175,550 |

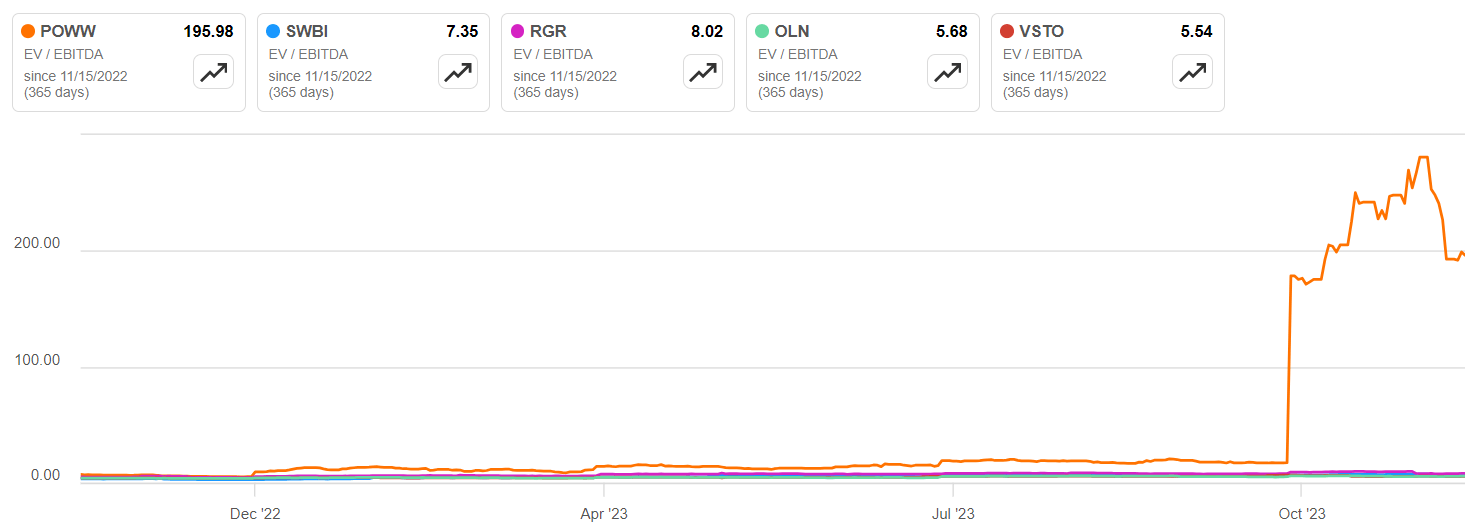

Also, the Company's current EV-to-EBITDA ratio (backward looking) is extremely high. See in the chart below how it compares with some other publicly-traded companies in the ammunition and gun industry.

{kind=link}

Risks To My Thesis

The main risk I see to my thesis is if the Company will manage to use its significant cash position to make acquisition(s) of highly profitable businesses. Two additional risks to my thesis are a dramatic cut in the Company's operating expenses; and a significant (and sustainable) rise in market price for the types of ammunition the Company manufactures.

Conclusion

I am highly skeptical about the Company's ability to generate any meaningful profit (if at all) in the foreseeable future. The Company will likely continue to bleed cash on dividends to the Series A Preferred Stock for a very long time. Insiders' activity, as a whole, in the past year demonstrates very little faith in the Company's future. The extremely slow pace at which the repurchase plan is utilized is discouraging. P/E ratio of ~41 (as discussed above) seems overblown for what, in my opinion, lies ahead for the Company as far as I can now see. Therefore, I rate POWW a sell.

For further details see:

AMMO: A Complete Makeover Is Needed