AMPL - Amplitude: Decades Of Growth And Evolution Ahead

2023-10-10 08:30:00 ET

Summary

- Amplitude is a fascinating company to me insofar as its size, profitability, and balance sheet poise it to generate quite exceptional returns in the decades ahead.

- Additionally, its management is young enough to continue to evolve the company aggressively for decades to come.

- That is, Amplitude's management has the stamina to add new lines of business atop its already large and growing lines of business.

- Out of all the companies on which I've produced research publicly, Amplitude is virtually the only one that has even the remote chance to create a 100x outcome.

- I explore this contention and much more with you today. In short, I like Amplitude at ~$11/share, and its solid free cash flow, pristine and well-capitalized balance sheet, and healthy growth poise it to perform well in the decades ahead.

100 Baggers

Within my private community, I would say there are really only 1 to 3 companies that have even the faintest chance of achieving the coveted 100 bagger return profile in the next 15-20 years (emphasis on the possibility of it requiring two decades).

For those unfamiliar with this term "100 Baggers," a popular investment writer and author, Chris Mayer, wrote about the concept in the fantastic and oft-cited book entitled, "100 Baggers." (I highly recommend reading it, as it offers timeless wisdom about investing as opposed to a narrow focus on capturing 100x returns from your investments, which is generally unnecessary for a successful investment practice over the long run and very, very rare).

At just $1.11B in enterprise value today ($11/share), Amplitude is one such company that I believe could produce 100 bagger returns in the next 15-20 years.

To be sure, I believe it will take at least 15-20 years, but, within my coverage universe, Amplitude is arguably my number one vote for the few candidates that could achieve this feat.

Why do I believe Amplitude could become a 100 bagger?

- Amplitude is a free cash flow (profitable) business. Since I originally partnered with the company (bought its stock), I've liked Amplitude because of its fundamentally profitable nature, despite being a very young company led by quite young technologists/leaders. Amplitude also has ~$320M in cash and no debt, and this cash-rich foundation provides Amplitude a fantastic platform to grow and evolve in the decades ahead. Having robust free cash flow generation will also allow Amplitude to make "revenue growth-accelerating acquisitions" in the future, which will invariably be necessary to create a 100x investment return outcome.

- Speaking of evolution, Amplitude will need to internally evolve its core platform substantially in the 15-20 years ahead in order to become a 100 bagger. Looking at Amplitude through our "third foundational investment framework" detailed here and in a recent podcast I shared, the business will need to layer on new lines of business that generate $100M to $1B to $10B in total sales each in order to generate 100x returns from its current level. Considering CEO Spenser Skates and his co-founders are quite young in their early to mid 30s, they have the stamina to continue to evolve the business for a sustained, multi-decade period of time, akin to Mr. Huang of Nvidia ( NVDA ) building and evolving his company over the last 30 years.

- Amplitude has already demonstrated its ability to evolve its platform and layer on new lines of business, while generating robust free cash flow. Atop its core analytics product, Amplitude has also released the following products: Experiment, Recommend, Amplitude CDP (customer data platform), and, most recently, Amplitude AI. Amplitude also released a "Snowflake-native" ( SNOW ) version of its platform via Snowpark, which is, as an aside, a platform about which I am very excited. You may learn more about Snowpark in this note . I am highly, highly incredulous that these young, dynamic technologists will stop here. There's likely much more to be built and offered to Amplitude's customers, present and future.

Here are a few data points substantiating the three points enumerated just above:

Amplitude Is A Highly Profitable Business

We generated record operating cash flow of $20.4 million and positive free cash flow of $19.3 million. With this result, we expect to be firmly in free cash flow positive territory as a company going forward.

Amplitude Has Demonstrated The Ability To Launch New, Attractive Products That Compound Top Line Sales Growth

Lastly, we had strong execution on our newer products with Experiment and CDP together now exceeding $20 million ARR.

Amplitude's Latest Product Release: A Suite Of AI-Centric Products

Today, we're really excited to introduce Amplitude AI, a suite of AI-powered features. Here are 2 highlights. The first is ask Amplitude, which uses AI to shorten the learning curve for anyone getting started with Amplitude. Type in a question like how long does it take for new versus returning users to make a purchase and will show a chart with the answer you need.

The second is data assistant, which uses AI to make data governance effortless. It determines the most important ways to improve your data quality and automate certain updates. By improving data quality and trust, we're helping customers get value from Amplitude faster. We're also releasing functionality that automates formula creation and short naming. Teams can pick from a variety of suggestions so they can move fast and stay in control. These new features will help us accelerate time to value and expand the base of users we speak to, enabling us to win simple.

To more succinctly summarize what could make Amplitude a 100 Bagger:

- Robust free cash flow generation and massive cash hoard alongside no debt

- Young leadership that has the stamina and creativity to continue to evolve the platform, launching $100M, $1B, and $10B+ products over the next 15-20 years, creating compounding, explosive sales growth

- Its relatively diminutive size at just $1.1B in enterprise value

Turning To Q2 2023

Let's now review Amplitude's most recent quarter, including the key metric for investment in the business: customer growth. From the beginning of my ownership of Amplitude, customer growth has been central to my thesis, and, despite slowing sales growth, Amplitude's ability to capture new customers has sustained at elevated rates.

We see how our platform approach is resonating with customers, improving our competitive position against legacy and point solutions. Win rates remained robust in Q2 and we continue to win deals against as well as replace legacy players.

We continue to refine our integrated go-to-market efforts, get closer to our customers and build on the strong pipeline we saw in Q2. We are executing with urgency as a company. A lot is happening under the surface. New leaders are raising the bar. I'm pleased with the progress we're making here as a team.

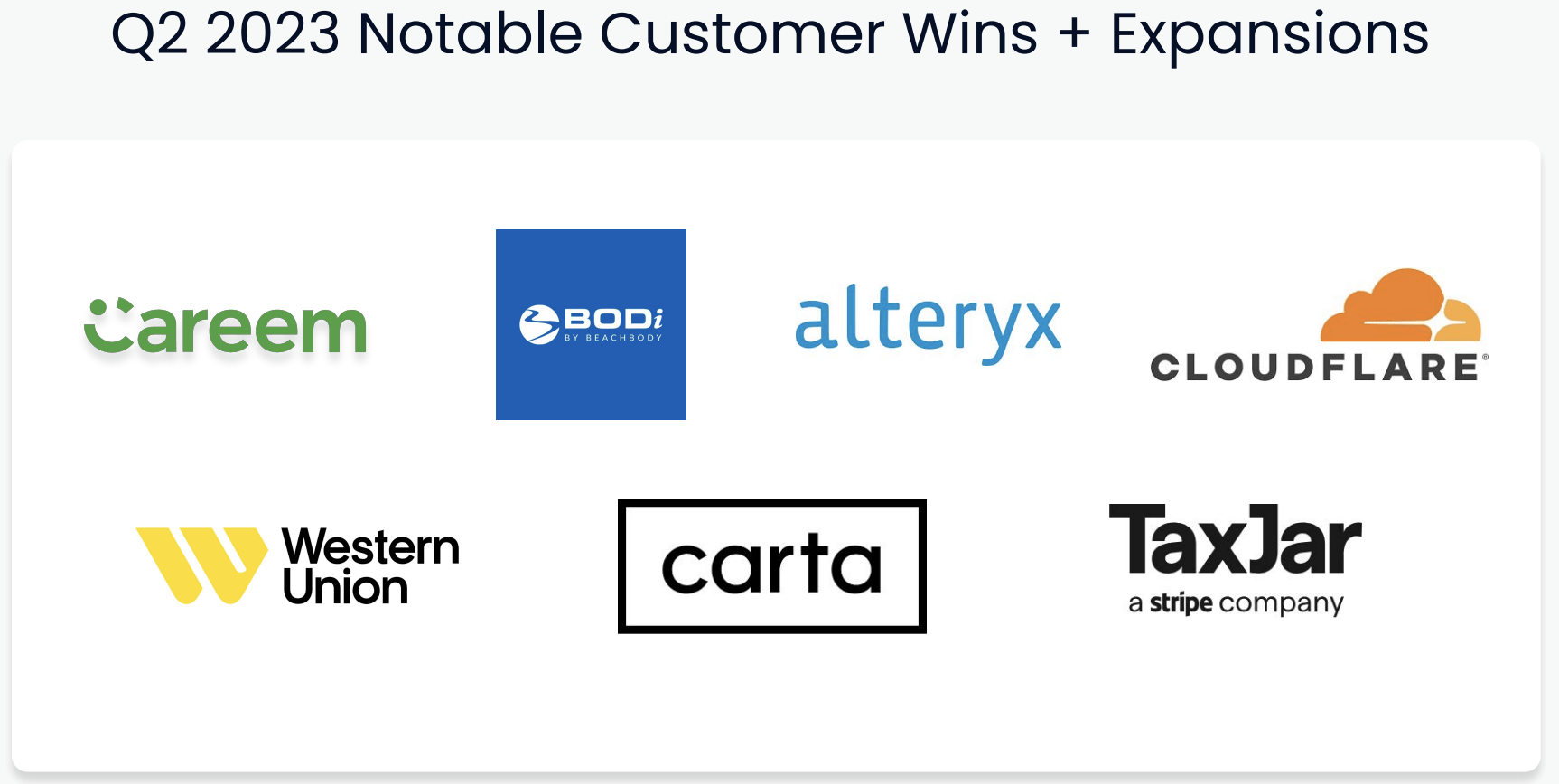

Amplitude Adds Some Of The Most Dynamic Businesses On Earth As Customers In Q2 2023

Amplitude Q2 2023 Earnings Presentation

{kind=link}

In Q2 2023, Amplitude brought Cloudflare ( NET ) on as a customer. Cloudflare is indisputably one of the best software businesses on earth. Similarly, Twilio ( TWLO ), Atlassian ( TEAM ), and Block ( SQ ), which are also some of the best and smartest software businesses on earth, have chosen to partner with Amplitude.

While certainly not the entirety of the Amplitude thesis, I believe it's noteworthy that some of the smartest, fastest growing software businesses on earth have chosen to partner with Amplitude.

Additionally, I found Careem to be a fantastic win, which illustrates the nature of the Amplitude platform. Careem is the "Uber ( UBER ) of the UAE" (Uber actually owns Careem). It's a dynamic, growing app that tens of millions of people use, and I believe this customer win is a great case study for understanding Amplitude's product, i.e., what the business sells to its customers.

Instead of "Microsoft," I would invite you to substitute "Careem" or "Uber" in the chart below:

Digital Customer Journey

Martech.org

Amplitude provides data and analytics to product development teams and marketers with which these teams can better understand how end consumers use their apps.

Product development teams and marketers can ask:

- Where is the customer getting stuck in the app?

- Why aren't they taking more rides?

- Why aren't they using our deliveries product?

- What features do they like most?

- What behaviors within the Careem or Uber app suggest that we will retain the user long term?

- What behaviors suggest that the user will churn early?

- When should we reach out to our users?

- What should we say to them?

- What features should we remove to create more simplicity?

- What features should we add to drive further engagement?

- What times of the day should we connect with users to create better retention?

And so on and so forth.

Amplitude provides the platform to answer all of these questions and more, and, based on the aforementioned customer wins, Amplitude's platform resonates with its customers and prospects as a source for reliable answers to these questions.

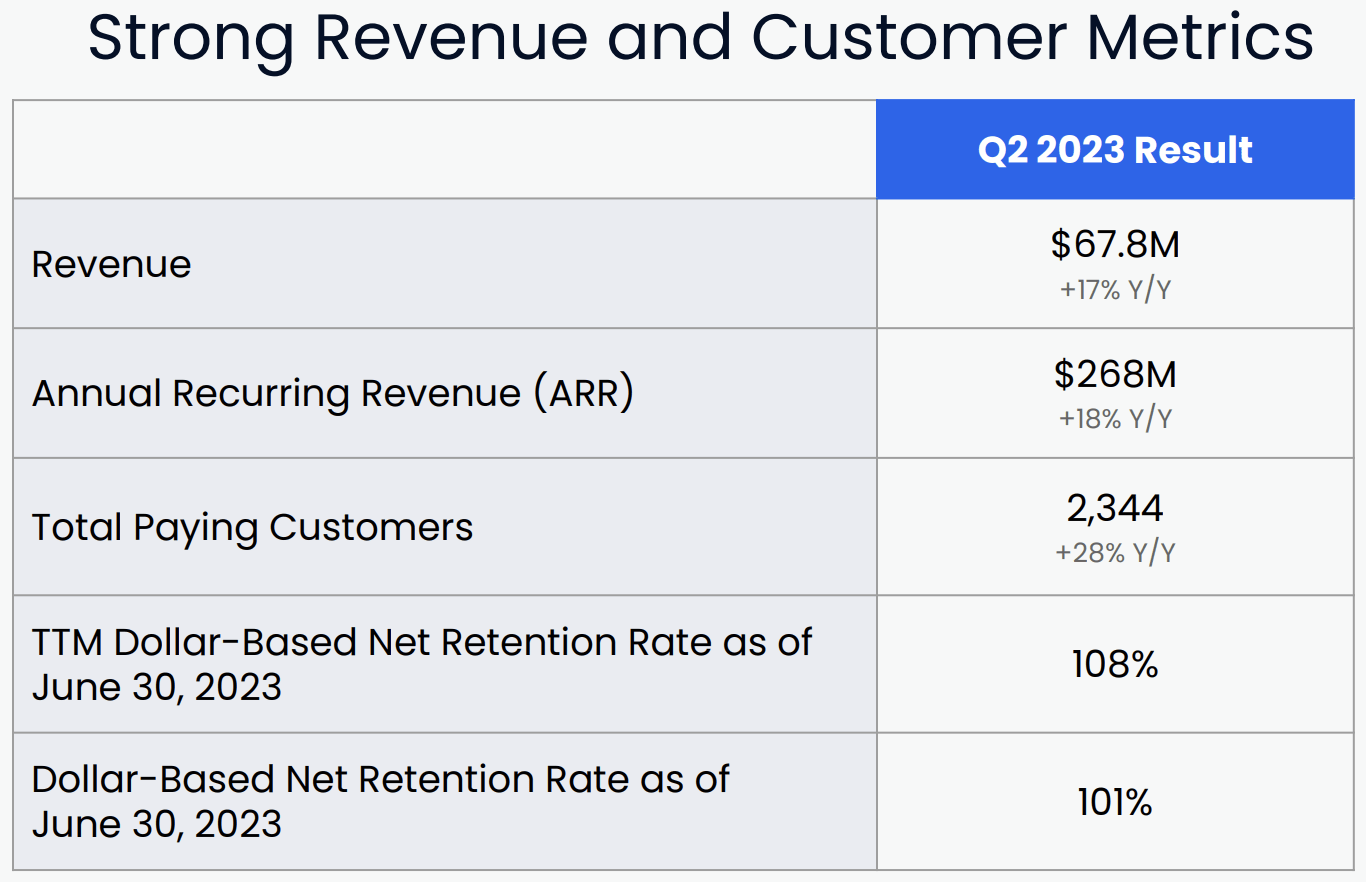

Amplitude Grew Customers At 28% Year Over Year In Q2 2023

Amplitude Q2 2023 Earnings Presentation

{kind=link}

We both landed and grew our relationship with customers around the world like Careem, Beachbody, Western Union, Alteryx, Cloudflare, Carta and TaxJar. Other customers this quarter included airlines and supermarket chains. It's clear that the need for Amplitude is a universal one.

We expanded with a brand name global sports organization to help drive global fan acquisition growth. This is a fantastic case study of the opportunity ahead of us as traditional enterprises continue with their digital transformation. To succeed, they needed to unify user data to personalize the fan experience across digital and nondigital properties. Marketing and product managers needed a shared view of the customer journey in a way to test hypotheses, target relevant audiences and personalized content features.

The organization's direct-to-consumer arm was already using Amplitude, but other teams used a combination of legacy tooling and marketing technologies. They couldn't scale, which caused major delays in massive engineering requirements. Amplitude's digital analytics platform was the clear choice for the business and we're excited to help grow the subscriber base and in turn, increase the company's broadcast rights to the tune of billions a year.

Next, let's examine why Amplitude's business has struggled to sustain elevated sales growth over the last year or so.

Strong Customer Growth And Profitability But Weak Revenue Growth

At the outset, I think it's worth noting that:

- All software businesses have struggled over the last year. For instance, AWS' ( AMZN ) sales have collapsed from 40%+ to just 12% over the last couple years. Snowflake ( SNOW ) experienced 0% sales growth in the month of April 2023, and these two are just the tip of the iceberg. The macroeconomic environment has also been deteriorating at a very notable rate as of late.

- Hubspot circa 2015 would be a great comp (comparable company) for Amplitude, and I have discussed this with you and my community often in the past.

With these ideas as our platform, let's consider Amplitude's revenue growth over the last year or so.

I'm pleased with our revenue beat, especially given the persistent challenges in the macro environment. Let me touch on a couple of those for a moment. Larger companies continue to optimize for their current level of end customer activity.

[This is precisely what we've heard from Snowflake ( SNOW ), SentinelOne ( S ), and AWS ( AMZN ).]

We remain exposed to startups who are feeling that pressure more intensely. Continued cost cutting is causing churn to tick up as macro ripple effects work their way to that portion of our customer base. While difficult, we believe these short-term challenges are just a temporary part of this macro cycle. There are several areas that fuel our cautious optimism here.

Amplitude's Income Statement Depicting Revenue And Gross Profit Growth Flatlining In The Last Four Quarters

{kind=link}

It's natural to ask: If Amplitude is growing customers at ~30% consistently, how could growth be flatlining to this degree?

- Large customers have been "optimizing," i.e., reducing their spend on software and digital ads across the board in 2023. The macro has not gotten better throughout 2023. It has deteriorated further, while inflation has persisted, and the Fed appears intent on hiking rates further to combat this stagflationary dynamic.

- Amplitude had material exposure to startups in 2020/2021, and many of these startups have faltered/failed in the last 24 months, creating giant churn for Amplitude. Amplitude was especially exposed to crypto apps, which have been gutted over the last 24 months, and this has led to dramatic reductions in usage, as well as churn from these customers' businesses failing.

So, despite solid growth in new, stable, and quality customers, Amplitude has experienced immense headwinds from large customers reducing their spend and smaller customers simply failing as businesses, which has created churn.

We can see these realities in Amplitude's NRR, which hit 101% in the quarter.

Amplitude Q2 2023 Earnings Presentation

{kind=link}

101% net retention rate [NRR] is the lowest NRR a company has experienced within my coverage universe in the last 3-4 years or so.

As I mentioned in my review of S1's business recently, the software I share with you are among the best on earth, and, as such, their NRRs generally hover well above the average for all software businesses, which is about 100%.

So, relative to S1, Crowdstrike ( CRWD ), Monday ( MNDY ), Okta ( OKTA ), and Snowflake, Amplitude's NRR is quite bad.

But, when we contextualize the business via our study of Hubspot, which had an NRR of 83% when it was planning to go public, and when we contextualize the business via our study of the software industry at large where 100% NRR is about average in good times, and when we contextualize the business via a study of the macroeconomic environment, Amplitude's NRR is actually pretty great.

I have no issues with it whatsoever, and I believe we will actually see it hit 120% at some point in the next 5-10 years, and there's a good chance it stabilizes there, as Amplitude continues to innovate and release new products, with which it can upsell its customers, driving NRR higher.

To close this review of Amplitude's financials, I'd like to end on a high note.

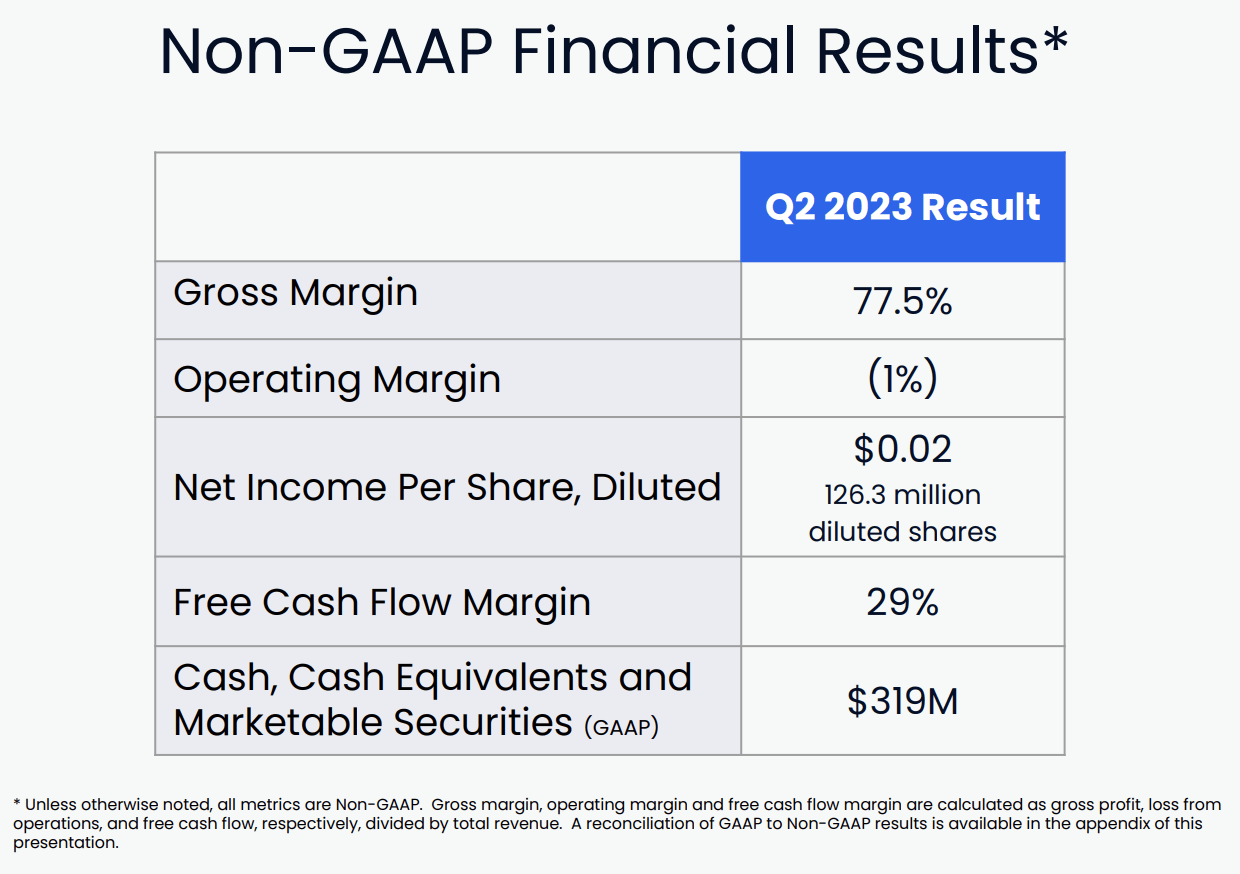

Below, we can see that Amplitude has ~$320M in cash and no debt. It has robust 77% gross margins and extremely robust 29% free cash flow margins.

{kind=link}

These metrics are simply stellar; almost unbelievable really.

I understand why Amplitude's NRR and gross retention rates have struggled, and, with Hubspot's comparability and success in mind, as well as the caliber of the Amplitude team and its product-market-fit/customers, I believe NRR and GRR [currently about mid 80%] will improve materially once we emerge from this challenging economic environment.

Amplitude On Snowflake

Before we close, I'd like to take a moment to highlight Amplitude's Snowflake business, which I discussed with you in our recent review of Snowflake's business.

We announced warehouse native Amplitude at Snowflake summit in June. Our warehouse native approach is all about extending what has made Amplitude successful: being the most open, agnostic, and trusted way to access and find insights from our customers' data. By providing access to Amplitude product insights directly from the data warehouse, we're making it easier for data teams to manage data and for product teams to use those insights confidently.

Companies are taking deferring approaches as it relates to governance and storage of their data. We want to be wherever our customers are along their journey. We believe this warehouse native option will be a natural on-ramp for many enterprise customers who have already made significant investments in their warehouse strategy.

While early, we also believe this can be additive to our core amplitude value proposition in many ways, including potential new personas and workloads. AI developments are an exciting opportunity for us to evolve how users engage with and find value from our platform. Product teams follow and iteratively build, ship, use, learn. Companies like GitHub and Figma have made massive improvements to the build and ship phases with AI that made it possible for developers to go from prototype to production in record time.

This has been a very fascinating development within my coverage universe, and I believe it's noteworthy that my entire research process is augmented by cross-sectionally studying software, FinTech, and consumer discretionary businesses.

My two key takeaways here are:

- Snowflake's growth will benefit materially from the growth of native apps built on Snowflake such as Amplitude.

- Amplitude is proactively finding distribution of its product, and this should help accelerate growth post the dynamics discussed a moment ago.

Mr. Skates echoed this second point in stating,

So the key thing -- so let me explain what it is and I'll explain why we've done it and how it fits in the strategy. The key thing with warehouse native is that -- there's been a lot of companies that have decided to use the cloud data warehouse as their source of truth for product behavioral data. And so in that world, it's much easier if you have an application that already runs natively on top of Snowflake and that plugs in directly to that data set without having to send the data over to Amplitude. So we just have a native application running within a Snowflake instance directly on top of that data, and that allows you to get all of the -- a lot of the digital analytics functionality that we have right out of the box. And so it's -- think of it as it takes 10% of the time to get set up if you already have the data, data warehouse than with the traditional process of Amplitude implementation.

Strategically in terms of why we're doing it. I think there's 2 big things. The first is that our expectation is that data is just going to live in lots of different places. Cloud data warehouse is going to be one of them. So the more prolific we are with the data sources that we work with, the more we're going to win the overall space and easier it is going to be to get on Amplitude. So it's all about meeting customer where they're at.

The second thing is that warehouse native, and I want to make this clear because there's been a little confusion on this is that it's an on-ramp to the more advanced capabilities. You can think of it like a light version of Amplitude. And then over time, as you want more speed, as you want more functionality and flexibility, you upgrade to the more sophisticated versions of Amplitude over time. And so really, it's a distribution play to tap into currently Snowflake's customer base, but we'll get to more of the cloud data warehouses over time. And that will, again, enable us to work with whatever your data sources, warehouse CDP, et cetera.

I am very happy to own both businesses, and their cooperation, in my eyes, will surely bring revenue-growth-accelerating synergies in the years ahead.

Bringing In Reinforcements

Over the last six months, I've highlighted that Amplitude has brought in a new, older executive team from Microsoft ( MSFT ). I noted that these individuals likely have expansive rolodexes that would serve to accelerate sales growth for Amplitude via large enterprise deals.

For further details see:

Amplitude: Decades Of Growth And Evolution Ahead