ASCJF - AMSC ASA: Revisiting The Thesis After 6 Months I'm Still 'Hold'

2023-09-27 07:51:08 ET

Summary

- AMSC ASA is a ship financing company with similarities to Ocean Yield, but it has a smaller market cap and fewer vessels.

- The company's move outside the Jones Act may have negative implications for its stability and investment thesis.

- AMSC ASA has a solid portfolio of modern vessels and offers a double-digit yield, but it carries significant risk due to macro factors and size concerns.

Dear readers/followers,

I've been in high-yield shipping stocks before - and it's one of the few areas and investments where I actually took realized losses in my investments. As a result of this, it's an area I'm very careful about. I've written two articles about AMSC ASA (ASCJF), to begin with, due to a subscriber request. The articles themselves garnered a surprisingly high like/comment ratio, which is something I look at. I'm happy to look at companies that readers seem to enjoy me looking at.

So with regards to AMSC ASA, I don't feel that I'm tooting my own horn too loudly when I say that I managed to avoid a negative RoR in this company. Even with dividends, the company is down 8.29% since March, which is much worse than the S&P500.

AMSC ASA RoR (Seeking Alpha)

But the time has come to revisit the company. Is it perhaps more attractive now? It should be unless something fundamental has changed.

The one thing I am sure about is that I am in no hurry to repeat my mistakes in the shipping sector. So this is an area where I cross my t's and dot my i's.

Revisiting AMSC ASA - Shipping with high-yield

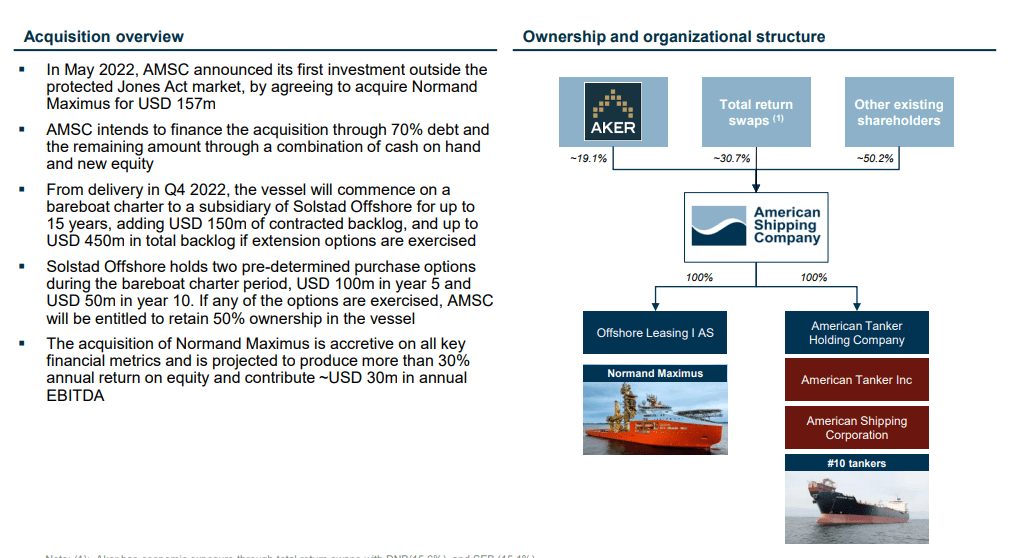

The similarities to Ocean Yield, a company that I've previously been invested in and actually lost money in, are numerous. This is a ship financing company, much like Ocean Yield was. This means that it owns so-called bareboat charters for maritime assets and leases them to various companies around the globe, in what can be compared to a triple-net lease structure for REITs.

Also, as perhaps the foremost risk - this is a minuscule company. On a global scale, it's barely worth the name. It was established back in -05 and is traded under the ticker AMSC natively in Oslo, and currently owns less than 20 vessels. You can consider it safer than your typical nano company because AMSC is actually owned in part by Aker ASA (AKAAF), a massive Norwegian conglomerate I appear to own - but this does not equate to a low risk or good returns.

$230M in market cap is what the company has. It's main argument for investing is the Jones Act. What on earth is the Jones Act?

The Jones Act is a 1920 law that limits how cargo is transported by sea. It requires any cargo shipped between U.S. ports to be carried by U.S. ships, with American crews. This is part of what gives the company its advantage. It's even right there in the name.

{kind=link}

Name, logo, and everything - it's clear what this company is. Its arguments are very similar to those once presented by Ocean Yield. Predictable EBITDA and dividends from in-demand assets with good, accretive acquisitions. Few maturities. Modern ships - I've heard most of this before.

A mix of things caused Ocean Yields' downfall, but a lack of diversification in subsectors in shipping was one of them. AMSC thankfully has a bit different structure, even if they have fewer vessels. (Source: 2Q23 Presentation)

Unfortunately, AMSC has recently decided that it's moving outside the Jones act.

{kind=link}

I don't have an issue with the financing solution. But I do believe the company moving outside Jones is a net negative for what was otherwise far more protected if a small sector. The asset of course has a contract, and I'm not prepared to say this is all-in-all a negative for the investment thesis. But it does not make things less complex. Yes, all of the fundamentals say that the Maximus M&A will be accretive - but it was exactly this sort of specialized vessel that in part caused trouble at Ocean Yield. The Maximus is an offshore construction vessel in the heavy-duty subsea sector - and while the contract, on the surface, looks safer, I know well that if things do take a downturn, there's very little safety to be had anywhere here. (Source: 2Q23 Presentation)

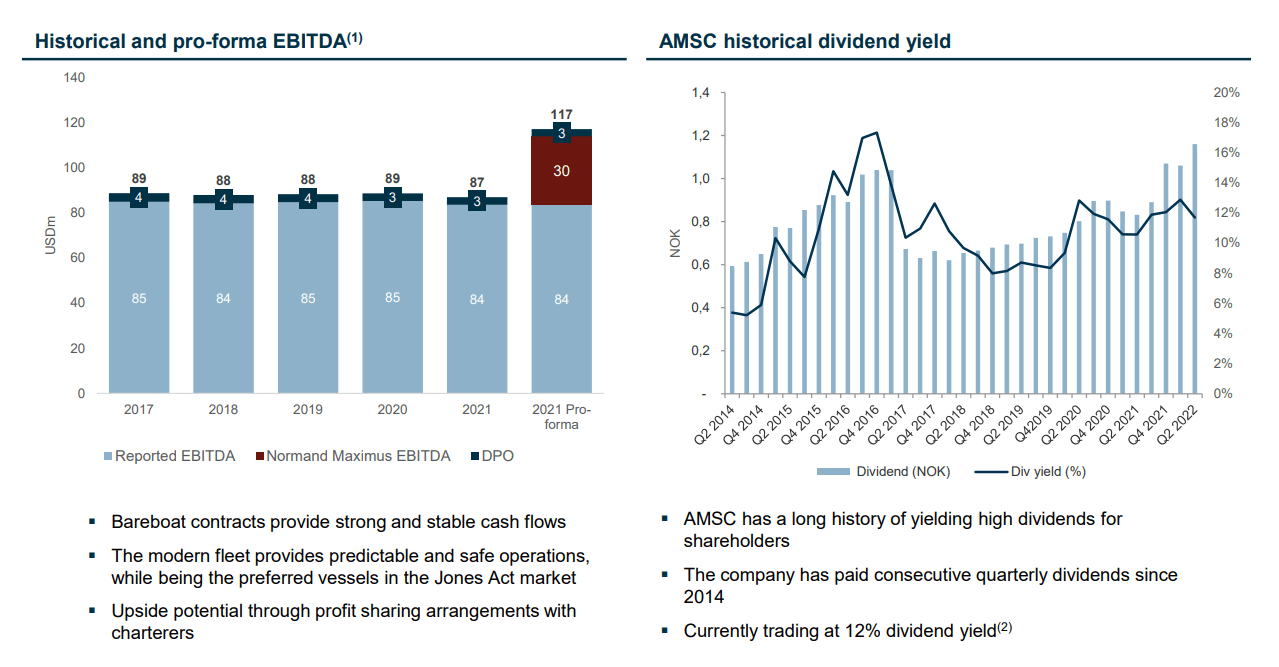

I like the company's portfolio of vessels otherwise. It's a very solid collection of Veteran-Class MT46'ers, type MR with not a single vessel older than 2007, or 15-16 years. It's a very "young" fleet, and the $84-$85M worth of EBITDA that we're getting annually seems safe. 52% LTV is good even now and would have been amazing two years back during ZIRP. (Source: 2Q23 Presentation)

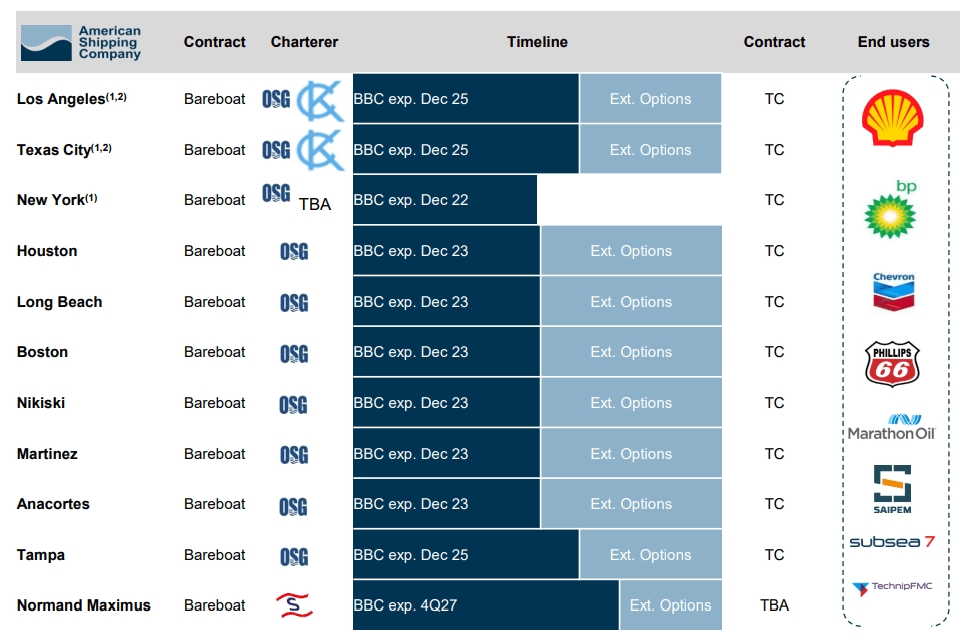

But the company suffers both from charter concentration as well as expiration concentration - and this is likely what has pushed the share price down quite a bit.

{kind=link}

So you can see, while the end users are diversified, the company's vessels are pretty much just chartered by OSG, with many expirations in 2023, lest options are used for extensions.

The Maximus will result in a significant increase in company EBITDA, around $30M more per year, which could enable either dividend growth or increased safety and debt downpayment. However, to call the company "stable" in terms of dividends would be wrong. AMSC adjusts its dividend where needed, and cut it as late as 2021.

{kind=link}

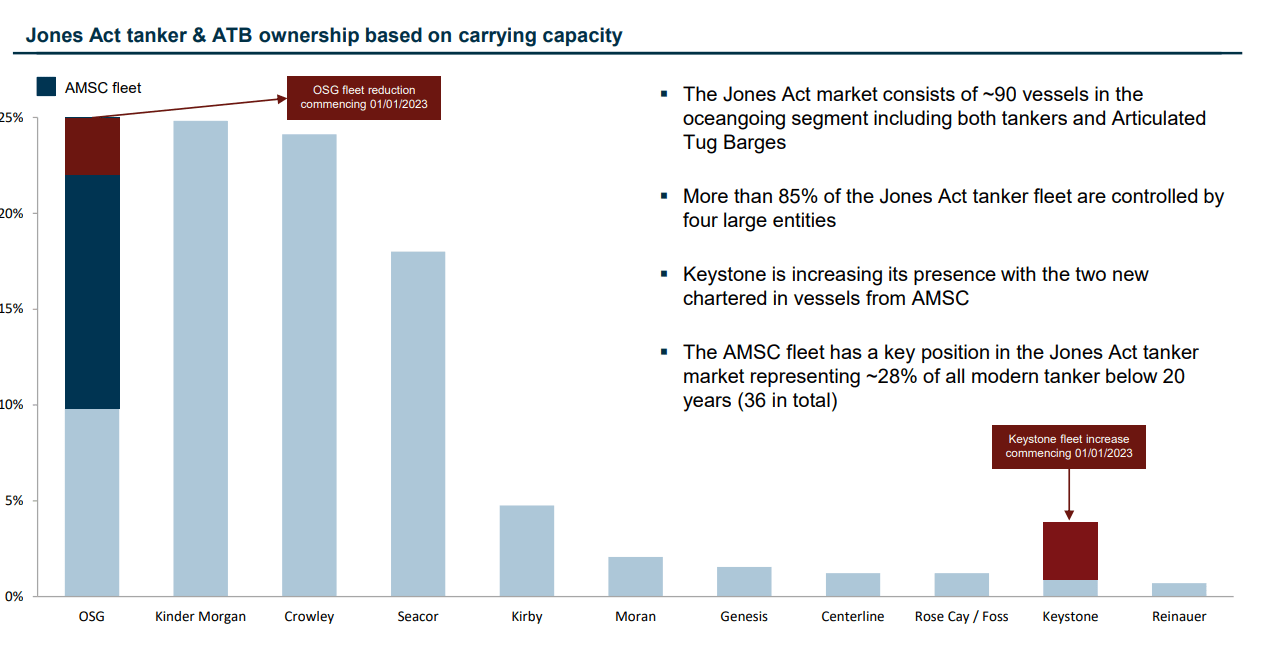

The company's fundamental advantages, and why I consider it a company worth at least looking at remain, even in 2Q23, its bareboat rates and competitive position. That the construction of new vessels is significantly higher than anything AMSC can offer the charter companies is clear. As an example, the company has a delivered cost at average $107M per vessel. The cheapest newbuild deliveries and transaction values for the years 2015-2017 were $130-134M, more than 25% above AMSC. The 2026E newbuild cost, inclusive of inflation, is estimated to be around $175M (Source: Philly/NASSCO, AMSC IR).

So for the foreseeable future, AMSC has a distinct advantage in the space. However, OSG has already communicated its intention to reduce its fleet size - and OSG is the largest player in the Jones Act. This is likely also the reason, or at least part of the logic behind the move outside the Jones Act. While the company has been able to move these assets to another Jones Act player, Keystone, any shift here is likely to bring about instability - as we're seeing at this time in the share price, down double digits. (Source: 2Q23 Presentation)

{kind=link}

The company's foundational appeal remains. It offers long-term lease solutions with significant financing advantages as well as ownership optionality at the end of the leasing term. It's an asymmetric risk/reward, just as it was with Ocean Yield. To be clear, Ocean Yield did not go bankrupt. It just went private at a price below my purchase price. And while the Jones Act continues to be a vital part of the US tanker economy, and the current refinery utilization and fossil fuel trends point in the right direction, I've been on the receiving end of the negative stick for a company like this for too long to be easily swayed by a 12% yield.

I have, as they say, been burned once.

Still, a case can be made for why AMSC ASA may be an interesting investment - and we shouldn't let one mistake make an entire sector unattractive.

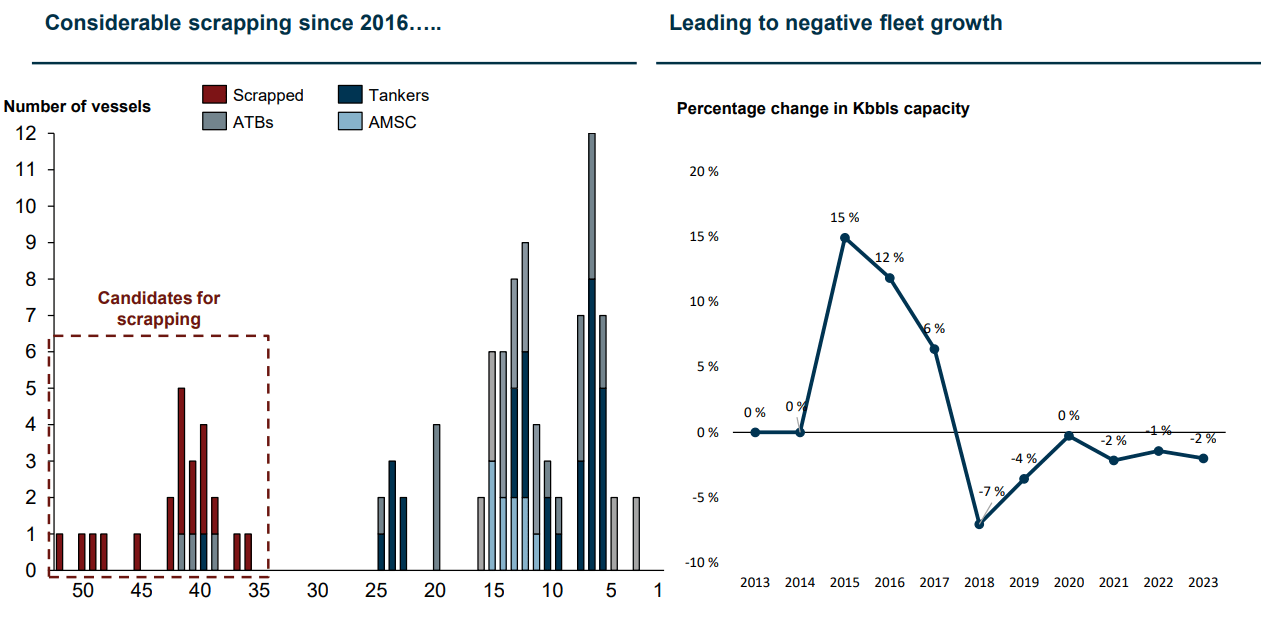

Furthermore, the availability of vessels and fleet in terms of fleet growth is actually forecasted to be negative. So on the macro side, plenty of things talk in favor of AMSC ASA. A significant amount of vessels are either already scrapped, or in the process of being scrapped, or candidates for scrapping.

{kind=link}

Let's see what this means for valuation, and how we should view the company here in September of 2023.

AMCS ASA - The upside is there, but it's risky

When I previously covered AMCS, I considered the company a "HOLD", fulfilling only 2 out of 5 of my investment criteria despite a significant, 12%+ yield. The native P/E at the time was over 15x, which I did not consider cheap or even appealing. There were cheaper and better shipping companies out there, and opportunities to get in on a high yield.

Because that's what we need to be clear about. Usually, investors want AMSC for an income investment.

But the thing about income investments today, due to increasing interest rates, there are plenty of them out there, and they are no longer hard to find - not even high-yielding ones. It's fairly easy finding 7-8% yielding debt instruments or pref stocks, which I would view as somewhat comparable to a risky, 12%-yielding shipping business.

I remain well beyond the state of being able to be tantalized by a double-digit yield and nothing else. The fact was that in my last article, and at over 43 NOK per share for the native listing, the downward potential of this company in the case the market turns, even with that relatively well-covered yield for the next 2 years, far outstrips the return potential of that yield.

That is now a different case.

While 2 analysts follow the company, these analysts have remained fairly steady at a 45-48 NOK, and the company has actually underperformed this for as long as I can see the history (Source: TIKR.com/S&P Global). In my previous article, I reiterated 30 NOK per share - and I'm fully cognizant that such a target may indeed never materialize, or at least not in the near term. But I remain firmly opposed to buying this company above anything with a "4" as the first number due to the significant risk of "just shipping".

I believe income investments yielding 7-9% are far easier to find out there, with more stability and safety and payouts in roughly the same size, and not asking you to invest in a sub-$250M market cap business.

However, as before, I can't justify going negative on the stock. The macro circumstances to enable such a downturn just aren't there. A flat development - yes - in fact, I believe energy prices will remain at these prices/relatively flat, and I don't expect a massive improvement in the sector from here on out.

This makes AMSC "speculative" in every case I look at. If you're fine with speculative investments, this may be one for you if you're sold on those high-income returns/yields.

For me though, the only circumstance where I could see myself buying AMSC is if the company was where I could consider "cheap" while at the same time being favorable from a risk perspective. While you could argue for the latter, I do not believe you, even now, can argue for the former.

Thus, here is my updated thesis for 2023E.

Thesis

- AMSC is an interesting company in the shipping sector with a solid portfolio of 11 (12 soon) modern vessels leased to relatively safe counterparties. The company sports a double-digit yield and attractive financials but is a small business with a decent amount of risk if due to macro and contract expiration.

- For that reason, I'm careful here. I wouldn't buy the company at today's valuation but would wait, if interested, for a bit of a drop.

- My PT for the company comes closer to the historical norm of 30 NOK/share, which is where I initiate coverage here. I'm not changing this for 2023 - it's still 30 NOK/share.

- The likelihood of the company dropping to this level without macro impacts is low - but this signifies just what I'm looking for before I would be willing to "BUY" a spec stock like this here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills 2 out of my 5 criteria, making it a "Hold" here.

For further details see:

AMSC ASA: Revisiting The Thesis After 6 Months, I'm Still 'Hold'