ASCJF - AMSC ASA: Solid Undercovered Stock 12% Yield Industry Tailwinds

2023-07-16 09:15:00 ET

Summary

- AMSC ASA is a Jones Act ship finance company with several industry tailwinds - no new vessels available until 2028 is supportive of higher rates.

- Revenue and EBITDA rose ~39% in Q1 '23.

- AMSC ASA receives very little media coverage in the U.S.

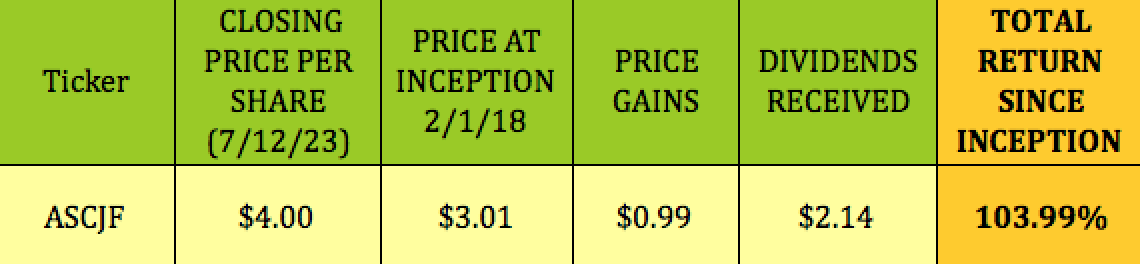

AMSC ASA ( ASCJF ) aka American Shipping Company is a core holding in the HDS+ portfolio. We added it on 2/1/18, nearly 5.5 years ago. Since then, it has delivered a total return from inception of 104.00%, two- thirds of which came from distributions.

{kind=link}

Company Profile:

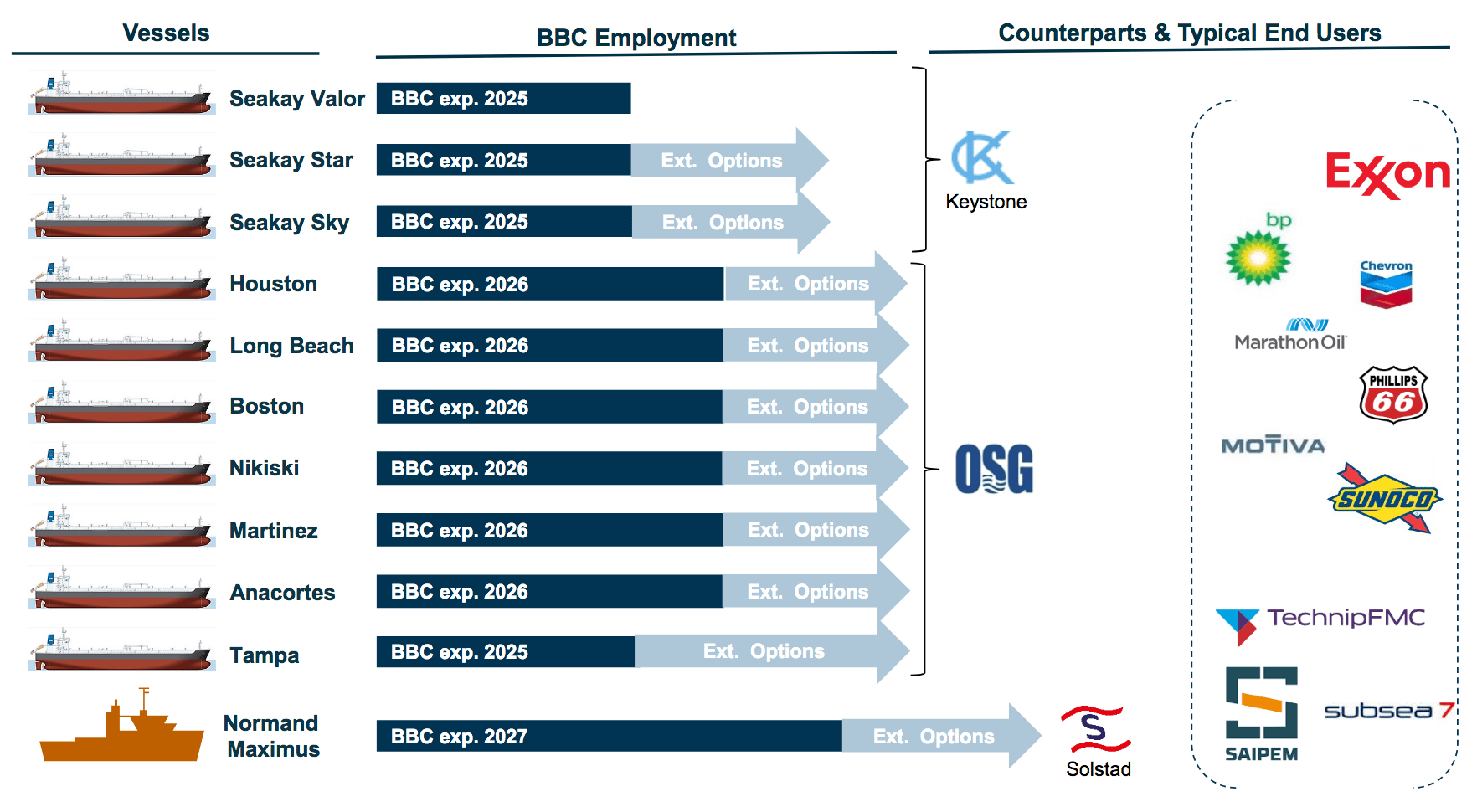

American Shipping Company owns a fleet of 9 modern handy size product tankers, one modern handy size shuttle tanker, and an international sub-sea construction vessel. Established in 2005, American Shipping Company is a ship finance company focused on the inter-coastal U.S. Jones Act shipping market.

Its modern handy size product tankers and its modern handy size shuttle tanker are on long term bareboat charters with Overseas Shipholding Group (OSG), a U.S.-based company.

Aker ASA is the largest shareholder with ~19% of the shares.

NOTE: We'll refer to American Shipping as AMSC or ASCJF in this article. AMSC's financial reports are in US $, with some figures also in Norwegian Krone, NOK.

The Company is listed on the Euronext Oslo Stock Exchange under the symbol "AMSC", with good volume, and also trades, with low volume, on the US OTC market, under the ticker "ASCJF".

Jones Act:

The Jones Act is a U.S. law that was passed in the 1920s, which stipulates that, "waterborne transportation of merchandise between two points in the United States must take place aboard a vessel that is U.S.-built, U.S.-owned, U.S.-flagged, and U.S.-crewed."

The Jones Act is an essential feature of U.S. national security policy, as it provides required capacity to support national security needs and avoid complete dependence on ships controlled by foreign nations. Since the U.S. maritime position in international trades has declined significantly in the last three decades, the Jones Act is the primary maritime market for U.S. shipyards and operators.

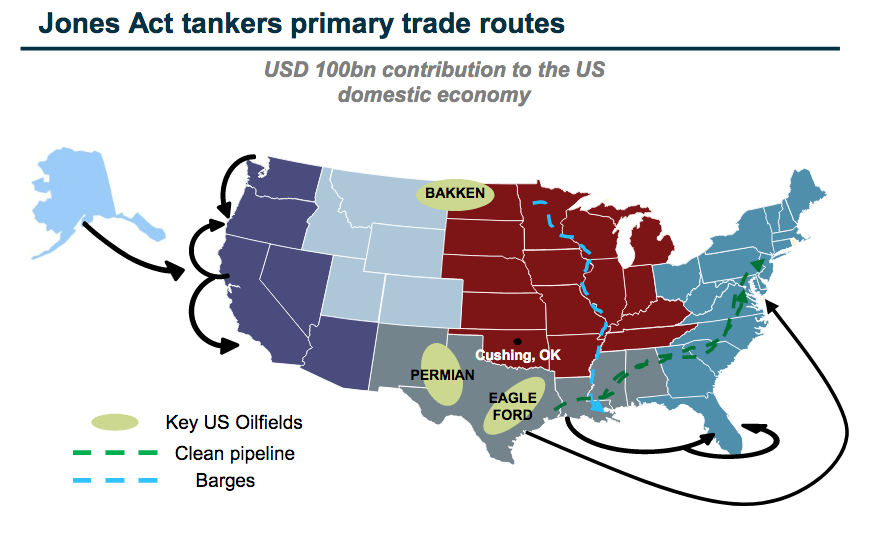

There is a lease finance exception in the Jones Act, which allows AMSC to lease vessels to Jones Act approved charterers, such as OSG, who, in turn, leases these vessels to various major oil companies, such as Exxon Mobil (XOM) and BP p.l.c. (BP).

{kind=link}

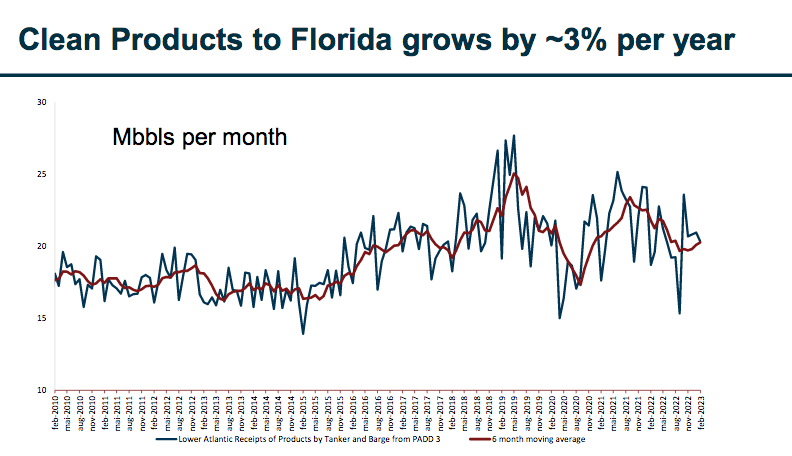

The Gulf of Mexico is a major shipping lane for Jones Act vessels. Since Florida has no pipeline connection nor any refineries, all clean products (Gasoline, diesel, and jet fuel) consumed are supplied by sea via Jones Act vessels - Florida alone represents 40% of demand.

Over the past 10 years, this trade has grown with a CAGR of about 3%. There's also demand for Gulf product in the Northeast, but that's dependent upon pricing vs. international alternatives such as Brent Crude. However, there's a shortage of available vessels for servicing the Northeast crude trade.

{kind=link}

Tailwinds:

Bio-fuels, which are produced in the U.S. Gulf, are expected to further demand for Jones Act vessels. There's only 1 vessel servicing the West Coast trade, but 8 more are planned to do so by the end of 2023. New bio diesel refining projects are also planned for the West Coast.

Refiners in the U.S. Northeast are experiencing a lack of available Jones Act tonnage to carry crude. The emergence of the Bio-Fuel will contribute to the shortage of vessels to the Northeast U.S. This is supportive for shipping rates and re-contracting rates for AMSC's fleet.

{kind=link}

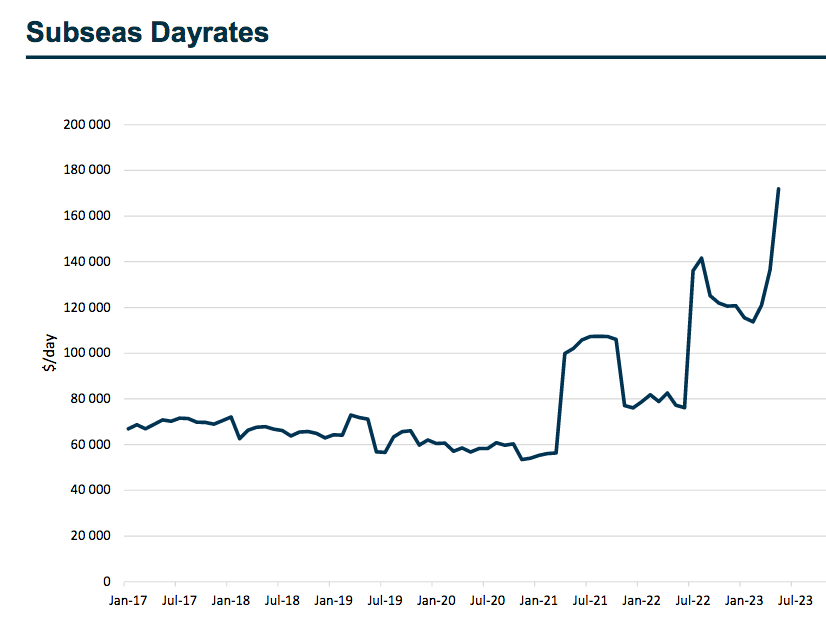

ASMC's newest vessel is the Normand Maximus, a sub-sea construction vessel. Day rates for Subsea Construction vessels has been rising since 2021, and is over $160K/day.

{kind=link}

There has been a lot of vessel scrapping of Jones Act vessels over the past several years - vessels are considered ready for scrapping when they're between 35 - 50 years old. This has decreased the Jones Act fleet's capacity, which is supportive for charter rates. AMSC has one of the youngest fleets in the industry.

The other ongoing industry tailwind is that there are only 2 shipyards, which have big enough dry docks to build Jones Act MR tankers, and they're both tied up with other projects for several years.

The likely delivered cost for a newbuild is now around USD185M, with the first available delivery slot in 2028, which would require charter rates of over USD $90,000 per day to justify the higher expense. (AMSC site)

Fleet:

The Normand Maximus, a sub-sea construction vessel, began a long-term bareboat charter in October 2022 between a subsidiary of AMSC, and a single purpose subsidiary of Solstad, a major Norwegian shipping firm.

Solstad has chartered the Normand Maximus until 2027, and also has extension options. Solstad announced in late December that the Normand Maximus received Letters of Award from various sub-sea contractors for hire of the Normand Maximus for execution of projects in 2023. The projects have a combined duration of minimum 200 days plus additional option periods, with a minimum value of approximately NOK 500 million, which translates to ~$51M USD.

AMSC's main charterer, OSG, used its 3-year options in December 2022 to extend the chartering of 6 vessels to December 2026. That increased AMSC’s bareboat charter backlog by a total of 18 vessel years and more than USD $ 163M.

OSG also redelivered 3 vessels earlier in 2022 to AMSC, and management diversified AMSC's customer exposure, via leasing them to Keystone Shipping Co. on 3-year charters which expire in 2025.

AMSC had a contracted backlog of Offshore bareboat revenue of USD $137.9M with a 4.6 years tenor, as of 3/31/23.

{kind=link}

Earnings:

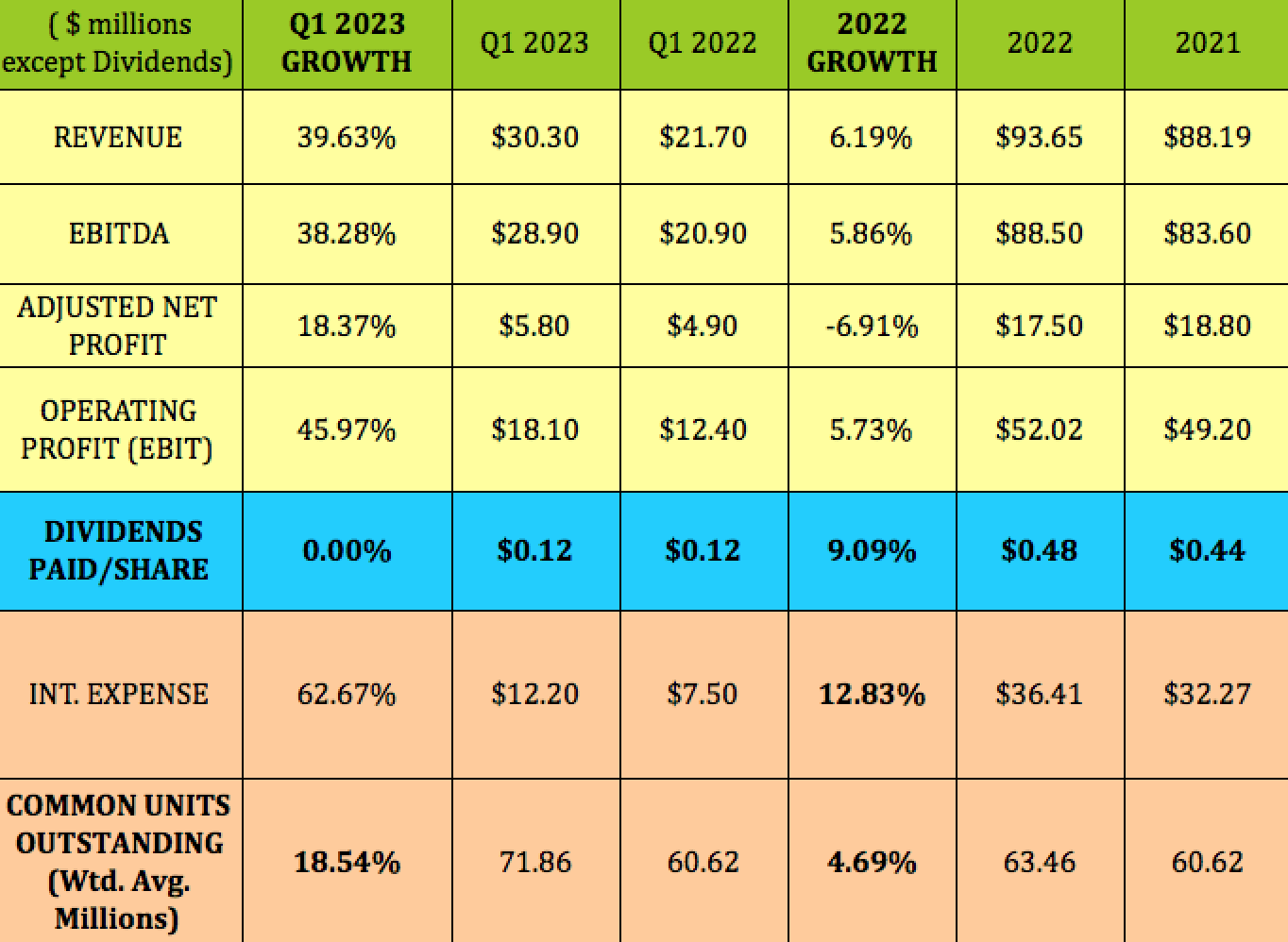

Q1 '23 had robust growth, with Revenue up 40%, EBITDA up 38%, Operating Profit up 46%, and Adjusted Net Profit up 18%. Interest expense was way up, partly due to additional debt taken on for the Normand Maximus purchase.

The unit count was up 18.5%, due to a private placement that mgt. did in 2022 to raise additional capital for the Normand vessel purchase.

2022: AMSC had mid-single digit revenue EBITDA and Operating Profit growth, with Adjusted Net Profit down ~7%. Dividend growth was 9%, as mgt. raised the quarterly payout from $.10 to $.12 in Q4 '21.

{kind=link}

AMSC also has a profit-sharing agreement with OSG, which could drop to its bottom line. In addition, it has a Deferred Principal Obligation, DPO, via which OSG repays principal and interest, up to $7M/vessel, over a period of 18 years. However, if the vessel's charter is terminated, the balance becomes due immediately. This gives AMSC good leverage with OSG in rechartering negotiations.

"During the redelivery process of three Jones Act tankers in December 2022, OSG withheld a DPO amount of USD $3.9M owed to AMSC for one of the redelivered vessels, claiming a breach of quiet enjoyment of the vessel as a result of a third-party inspection authorized by AMSC in August 2022.

AMSC filed a complaint against OSG in U.S District Court for the Southern District of New York in December 2022 for USD $4.5M. On 27 December 2022, AMSC was granted an order for the Process of Maritime Attachment and Garnishment which has subsequently frozen three of OSG’s accounts up to a total of USD 4.5 million. OSG fully repaid DPO amounts for the other two vessels." (AMSC site)

All 3 vessels were rechartered to Keystone.

Dividends:

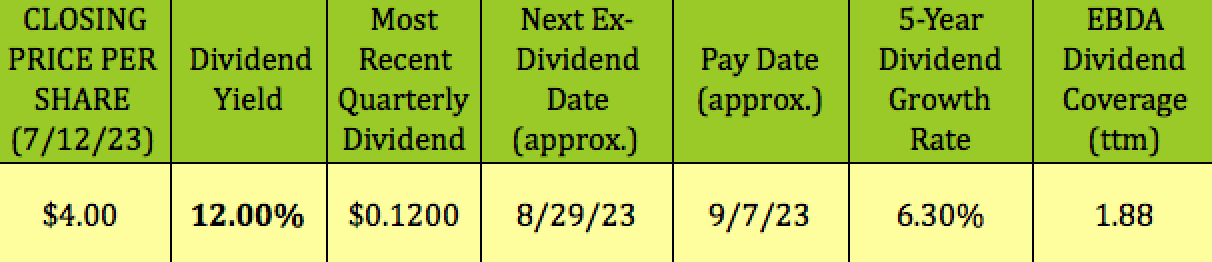

At its 7/12/23 closing price of $4.00, ASCJF yielded 12%. It should go ex-dividend next on ~8/29/23, with a ~9/7/23 pay date. It has a good 6.3% 5-year dividend growth rate.

{kind=link}

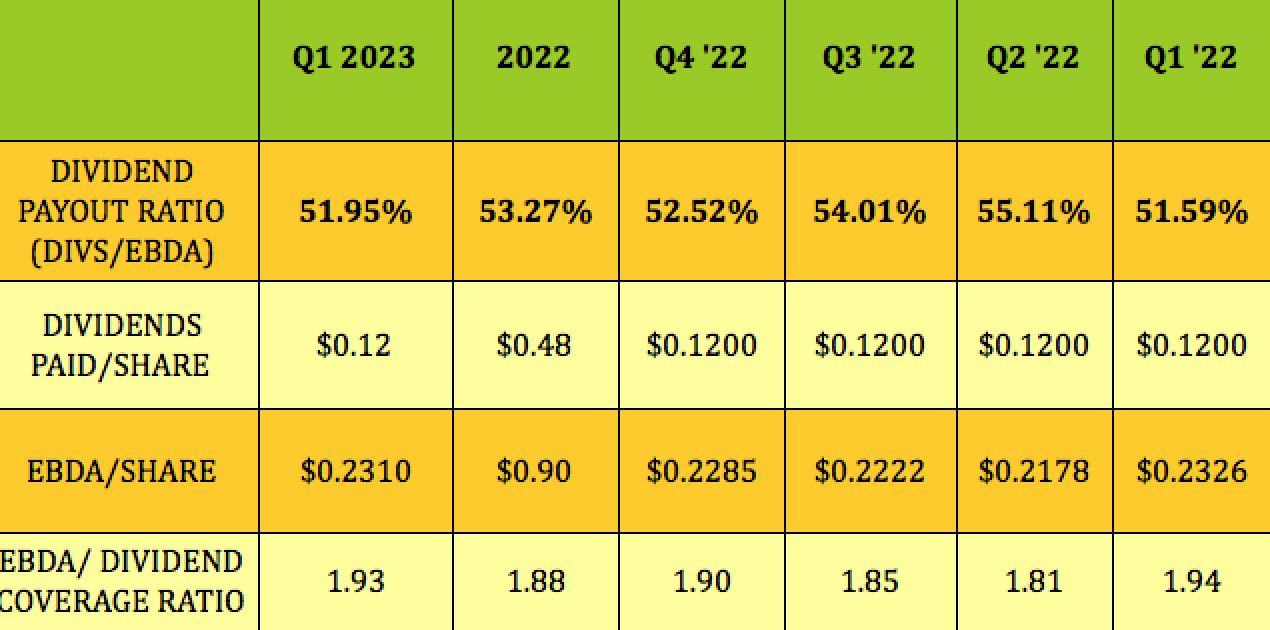

Dividends were covered by Earnings Before Depreciation & Amortization, EBDA, by a 1.88X factor in 2022, which improved to 1.93X in Q1 '23.

{kind=link}

Taxes:

AMSC had federal net operating losses carryforward (NOL's) as of 31 December 2022 of USD $413.6M in the U.S. and USD $62.7M in Norway. These NOL's have been generated since inception from the tax losses of the Company, which in the U.S. are mostly due to the accelerated depreciation of the vessels for tax purposes (10 years) and in Norway are mainly due to the interest cost on the original 2007 bond loan and tax depreciation. (AMSC site.)

Its 2022 distributions were classified as Return of Capital, which offers you a deferred tax advantage, but also decreases your tax basis, so there's recapture if you sell.

Profitability & Leverage:

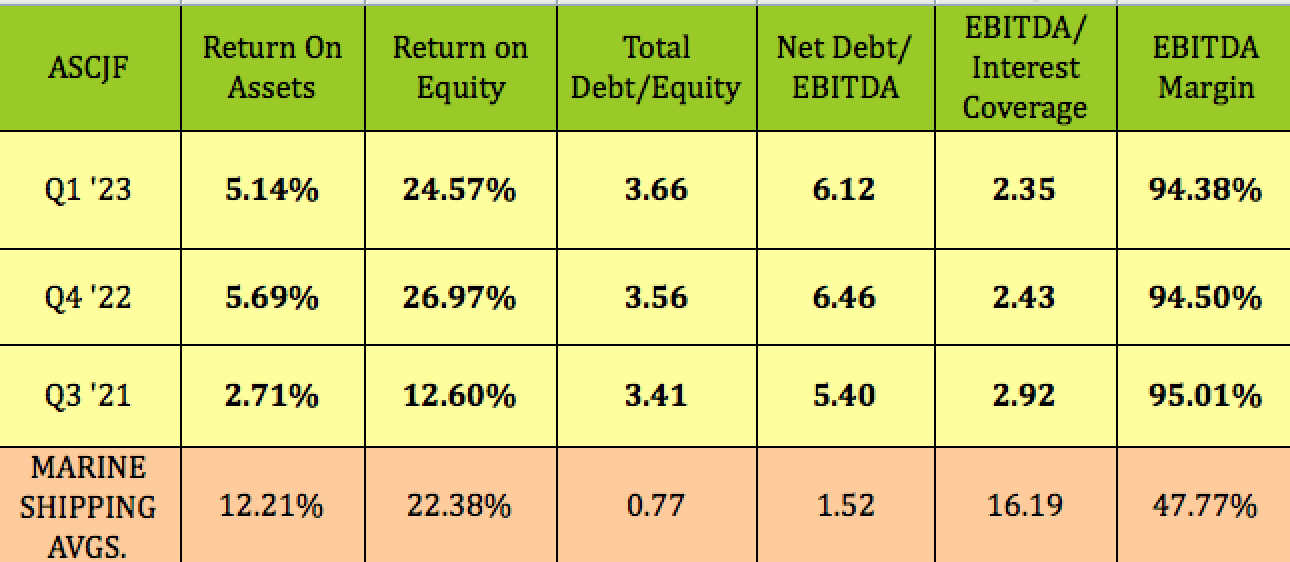

ROA and ROE have improved considerably since Q3 '21, with ROE slightly higher than the industry average. As a ship financing company, AMSC's EBITDA Margin is much higher than the industry average. Net Debt/EBITDA improved sequentially in Q1 '23, but was at a higher level than in Q3 '21, due to debt taken on to finance the Normand vessel acquisition.

Surprisingly, the overall marine shipping industry doesn't carry huge debt leverage. AMSC's situation differs in that it's a ship finance company, which uses capital to acquire and lease out bareback vessels, with the charterer paying for all vessel operating expenses plus charter rates to AMSC, but not having to finance the vessels.

{kind=link}

Debt & Liquidity:

"Interest bearing debt as of 31 March 2023 was USD $621.1M, net of USD $5.4M in capitalized fees vs. USD $633.2M as of 31 December 2022. This debt relates to the bank financing for the Company’s 10 U. S. Jones Act vessels of USD $291.9M, bank financing for the Normand Maximus of USD $108.7M, the unsecured bond of USD $220.0M, and accrued financial costs of USD $5.9M. AMSC was in compliance with all of its debt covenants as of 31 March 2023."

AMSC has $35M in debt coming due in Q4, 2023, with the balance of its debt maturing in 2025.

Analysts' Targets:

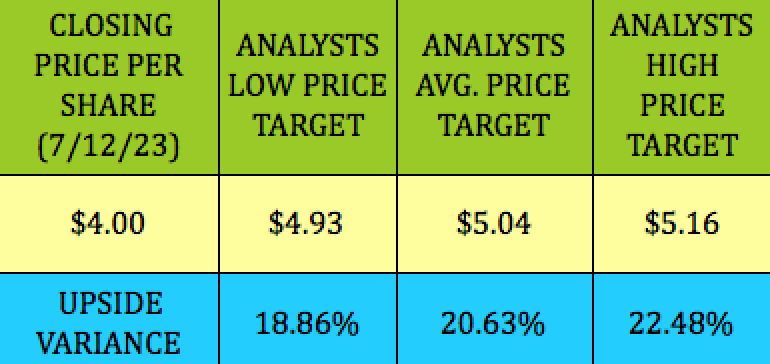

At its 7/12/23 closing price of $4.00, ASCJF was 19% below analysts' lowest price target of $4.93, and 20.6% below the $5.04 average price target.

{kind=link}

Valuations:

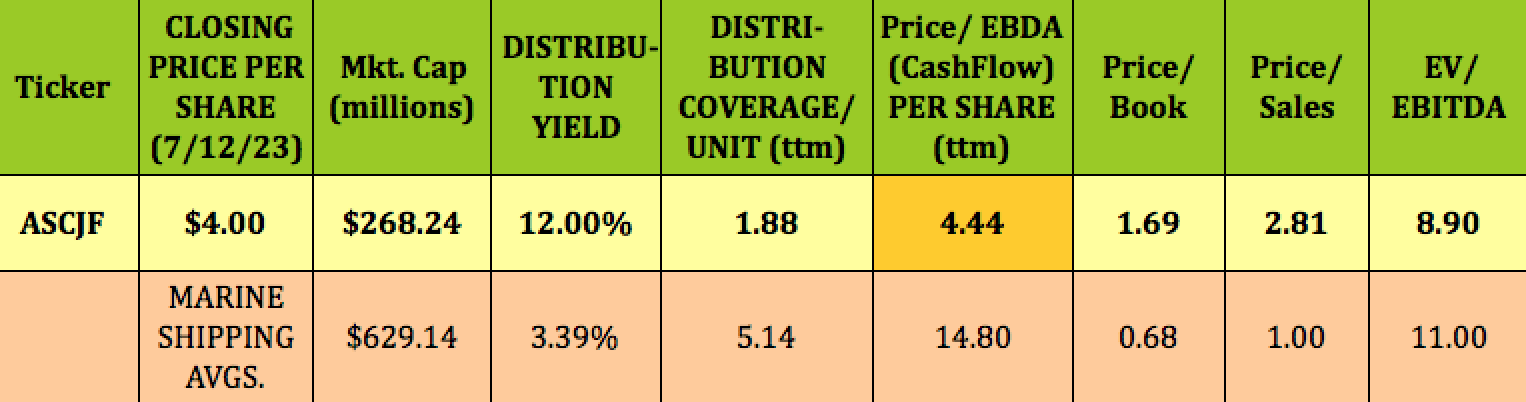

AMSC's Price/EBDA of 4.44X is much cheaper than the marine shipping industry's 14.8X ratio. Its EV/EBITDA of 8.9X is also below average, while its P/Book and P/Sales are both above average.

Its 12% dividend yield is 3.5X higher than the industry average. Although AMSC's dividend coverage is solid and consistent, it's much lower than the industry average, as the industry, on the whole, doesn't pay out very high dividends. AMSC's situation differs in that it's a ship finance company, which uses capital to acquire and lease out bareback vessels, which uses capital to acquire and lease out bareback vessels.

{kind=link}

Parting Thoughts:

ASCJF is thinly traded, and can sometimes be volatile - it jumped $.50/share, up over 14% on 7/12/23, on volume of 7K shares. It pays to check the Oslo price with your broker - you may be able to get a lower entry price.

We rate AMSC ASA stock a long term BUY, based upon its expanded earnings base, its well-covered dividend, its very attractive dividend yield, and its industry tailwinds.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted

For further details see:

AMSC ASA: Solid Undercovered Stock, 12% Yield, Industry Tailwinds