BLK - Amundi: New Outlook Means We Should Be Careful Moving To 'HOLD' (Downgrade)

2023-04-18 14:04:14 ET

Summary

- Amundi S.A., like most financial companies, has had a bit of a negative time in early 2023. The company has somewhat underperformed.

- Amundi has a through-cyclic upside and safety that puts it high on the list in terms of appealing to global asset managers. What's more, it's cheaper than many peers.

- However, the updated forecast for the company in this new environment requires an adjustment of the share price target. This makes the thesis more difficult.

- I'm changing my rating to "HOLD".

Dear readers/followers,

In this article, we'll look at Amundi S.A. ( AMDUF ) again. The company does warrant an update here because the outlook for this company, as with many asset managers, has changed. This, coupled with the current macro environment, means that I am changing my thesis on Amundi to reflect this new reality and outlook.

We'll look at the updated results, and the updated upside and I'll explain why I'm now less positive about the upside here. Now, technically, the company still has an upside to a relatively conservative upside - but what's available next to Amundi makes this company, in context, less attractive than it was.

My previous PT was around €62/share. I would now go closer to €57/share.

Here is why.

Amundi - Careful, despite recent results

Many of the original positive upsides still remain. This is one of the best-growing asset managers around, with close to sector-leading EBITDA and NRI growth rates, as well as well-above-average ROE and other return KPIs. The dividend payout isn't right-sized necessarily for the new income environment, and the valuation isn't as "bottom" as some of its peers and other companies in the financial sector. That's part of the reason I'm going somewhat more cautious here - but there's still a lot to like about Amundi.

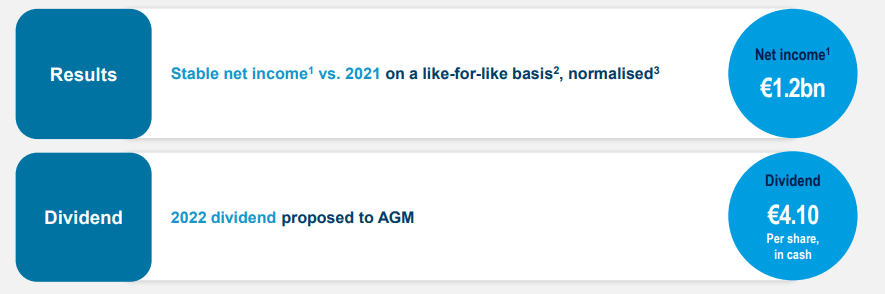

FY22 results confirm this. The company has managed outperformance in a bear market. That's usually the least we expect out of a manager like this, but the company also experienced positive inflows, as well as €1.2B in net profit, which for this environment is excellent. Customers voted with their wallets, and the company saw growth in high-margin segments and in expertise segments.

This caused the company to declare a high dividend for the 2022 fiscal year.

{kind=link}

This performance is nothing to take lightly in the context of the macro environment. The European asset management market saw outflows of close to €60B during the year, and including MLT assets, the outflows were over €130B. Considering equity market performance of negative 13%, and fixed income of -17%, the company's performance deserves highlighting. The new dividend means that as of right now, the company is yielding nearly 7%.

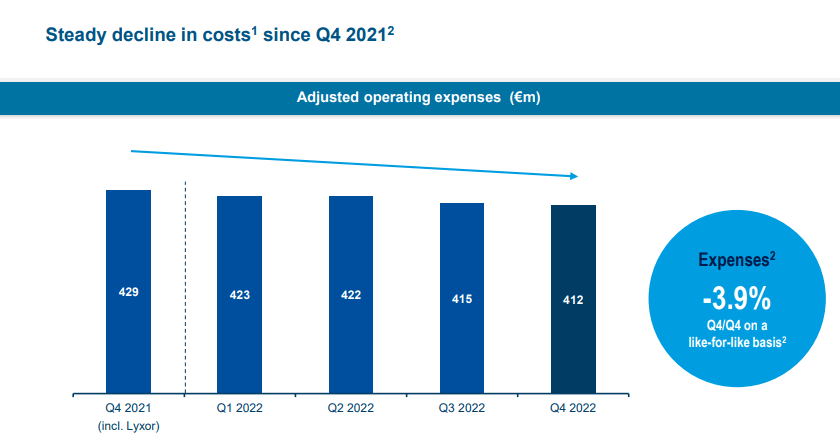

Equally impressive is Amundi's superb cost control.

{kind=link}

Assets under management ("AUM") remain stable at a high level, and as of late 2022, the company had an AUM of over €1.9T. This isn't as high as the end of 2021, but that also was one of the best years for asset management in the history of the stock market. Worth mentioning is the company's outflows in China given the environment in those areas - I expect we'll see more of that going forward.

What I want to focus on in these latest results is the appealing combination of cost control and excellent net income for the times. At the same time, we can't ignore the lower AUM and the overall environment. For the time being, Amundi is managing to keep management fees relatively high, even up over 7% YoY, and performance fees was impressive as well (given the current environment). The company also reports tangible equity of nearly €4B, with a CET-1 ratio of over 19%.

Amundi's credit rating of A+ remains one of the best ratings in the entire sector and actually makes Amundi a 7%-yielding A+ investment, which even at zero capital appreciation is better than many MMFs. The company refers its good results to its excellent management, good cost control, successful integration of Lyxor M&A in less than 9 months, its successful execution of the Ambition 2025 plan, and good development of its passive management, technology pushes, and superb profitability. The company remains one of the best on the block.

{kind=link}

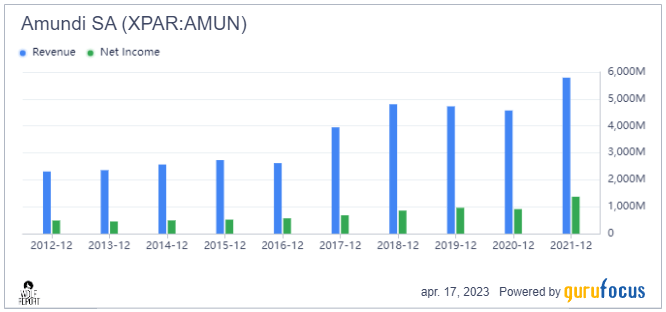

The same positives are true if we look at the net management fees, and the more granular overview of the overall inflows. It is broad-based, not one or a few segments. The company's revenues and earnings only, with a few exceptions, go in exactly the right direction.

Amundi rev/earnings (GuruFocus)

{kind=link}

Some instability, but not surprising.

No, where Amundi now fails is, at least I believe, in the comparative appeal for what's being offered here. Before I wrote my first article on Amundi, the company traded to close to €40/share, and that is some of the trough levels we've seen for the company before, representing a sub-10x P/E ratio. Sub-10x is where many asset managers are currently trading - Amundi is now closer to 11x.

What I'm looking at when I check asset management businesses, is how the company is handling the changed nature of expense management, or rather, the expenses themselves. Amundi is still impressive here, despite me expecting a downturn in 4Q22 - and all of this is in spite of a negative FX from the dollar and Euro.

Risks currently come primarily in the way the company is being priced on the market given what's happened in the finance sector over the past few months.

Amundi is in a sector where peers include massive giants. The obvious ones here include market leader BlackRock ( BLK ) - however, the yield isn't comparable for the two businesses. Bigger than Amundi in terms of sheer market cap are also businesses like Blackstone ( BX ), Investor AB ( IVSXF ), KKR & Co, T. Rowe Price Group ( TROW ), and a few more. While Amundi is far from the most expensive in this peer group, it's also far from the least expensive.

Let's look at the valuation for this company, so that I may clarify my problem somewhat.

Amundi - the valuation problem compared to broader finance peers

So, the problem for Amundi is that compared to where the company typically trades, and how close the stock is trading to that range of 11-13x, it's not even close to as undervalued as many BBB+ or similarly-rated finance businesses out there today. Granted, many of these peers or finance businesses might not be asset managers. They're found in insurance or large banking - but these companies will see less volatility associated with a downward trajectory market, which I believe we're moving into as we go forward here.

As I've mentioned in other articles, the right time to buy any asset manager is when there is a significant discount to its assets, but also to its peers, and to the historical valuation.

We did have that time in October of 2022, when Amundi was trading at around 6-7x P/E - a great discount for a qualitative, A+-rated asset manager such as this. That is no longer the case here. In my previous article, before the financial crash (or rather, the banks), I saw the company as appealing enough to "BUY" at just above €60/share. However, I can no longer justify that - not with the market in the shape it's currently in.

At a 10x P/E, the company's upside is close to below double-digits here. There is a margin of error here that I am somewhat uncomfortable with - if only simply because of the fact that other companies only have an upside at this time, as I see it.

Even in my last article, we did not really have a massive discount. While we're lower today, the market situation is also changed, which really means that the upside has not improved - only grown worse.

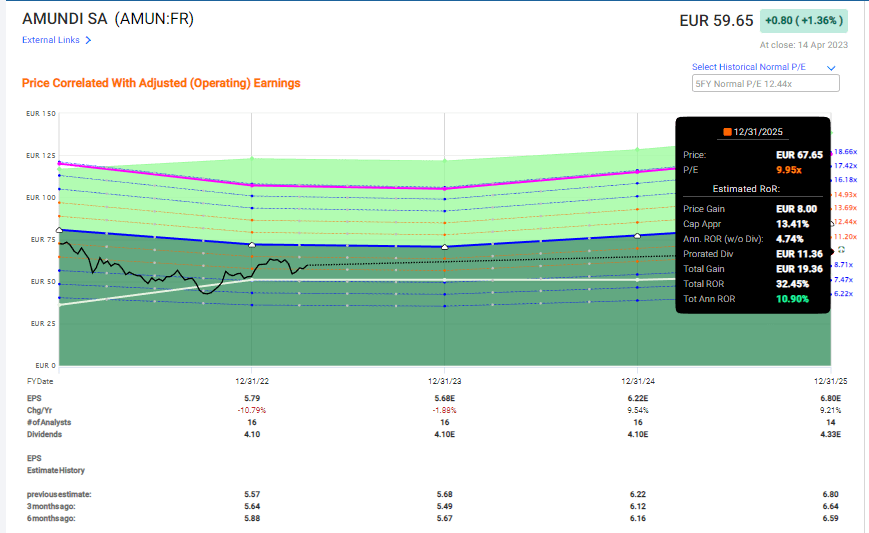

F.A.S.T graphs Upside (F.A.S.T graphs)

{kind=link}

This is the highest upside that I currently see is realistic for the company. Any higher than this would be based on what I consider to be doubtful at best. The S&P Global average currently comes to €62-€89 with an average of €71. While I understand some of these analysts taking the company's positives at essentially face value, despite this positive PT, only 8 out of 17 analysts are actually at a "BUY" here.

Furthermore, while I like Amundi fundamentally, I would caution anyone going "in" here that there are significantly better upsides available - which have much fewer downsides. If you consider that we've seen 7.5x P/E, that P/E on a forward basis means a total annual RoR of less than 1.5% - or 4.1% until 2025%. Annual RoR without the company's high dividend here is negative 6% until that 2025E.

That's the potential I see - not the positive double-digit that some see here. Going by peer appeal is hard because the spread between these valuations is too high. BlackRock is almost twice that of Amundi, but that doesn't make Amundi automatically attractive - BLK is almost 10x the size and has other appeal as well. Amundi is still trading at around 10-11x P/E normalized, which is close to its historical average of 11x. The expected forecasted average growth in the next 3-4 years is around 5-6% per year for EPS and 5-9% for the dividend.

The one clear advantage Amundi does have, aside from its qualities described above, is the yield. It's more than twice that of BlackRock, and significantly above most other asset managers.

However, we have little data on Amundi S.A.'s forecast accuracy - only that analysts are perhaps a bit too exuberant about the targets, as they tend to be. And for those reasons, and the reasons of the broader market, I'm not really willing to go higher. As an example, you could easily invest in something like Truist ( TFC ) or Lincoln National ( LNC ) with relatively similar yields, but much different upsides and downside trends.

This brings me to my current thesis for Amundi.

Thesis

- Amundi is a French, world-class asset manager with over €1.9T in AUM, A+ rated with a yield of over 6.7% at a good valuation. The company, like any qualitative asset manager, is a play on overall market development and should be bought at a significant undervaluation.

- A valuation that would consider being relevant for the company here in order to increase my position is below €57/share. However, this must also be put into context with other investment opportunities available on the market today - and that is why I now am lowering my target to that €57, from over €60/share.

- I start coverage on Amundi with a "BUY," albeit one with a very limited overall upside.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Now, I'm only at 3 out of 5 targets, which means I'm at a "HOLD" at this time.

For further details see:

Amundi: New Outlook Means We Should Be Careful, Moving To 'HOLD' (Downgrade)