AMDUF - Amundi: The Market's Expectations Are Acceptably Conservative

2023-09-08 03:21:11 ET

Summary

- Europe's largest asset manager, Amundi, operates a diversified distribution network and product offering, supporting relative through-the-cycle stability.

- Past AUM growth has been robust, with positive inflows in each year since IPO.

- Headwinds from fee margin pressure and market effect are the main risks here, but at a 10x P/E, that's already baked in to the stock price.

Asset management stocks have faced no shortage of headwinds recently. The stalling of the long-running bull market in equities and bonds, which has helped prop up industry AUM and fees, and the rise in passive solutions and their negative effect on margins are chief among them. Smaller players not diversified in their products and/or distribution channels can make for particularly volatile investments.

French giant Amundi (AMDUF) measures up well on the second point. Europe's largest asset manager, its relationship with parent firm Crédit Agricole (CRARF)(CRARY) contributes to a significant distribution network, while being diversified in terms of product lines makes it a fairly stodgy player in the industry.

While the firm faces the same headwinds on margins as peers, I do think that is largely reflected in the valuation here, and at just under 10x FY22 EPS these shares look reasonable value for the long-term investor.

Company Overview

Amundi is the largest asset manager in Europe with €1.96T (~$2.1T) in AUM. By client segment, AUM is split between Retail (~30%), Institutional (~55%) and Joint Ventures (~15%), with the latter basically encompassing its burgeoning Asian operations.

On a broad level I like Amundi for a few reasons. For one, Retail benefits from the nature of its relationship with majority-owner Crédit Agricole ("CA"), one of the largest banks in France, with products distributed to customers via thousands of CA bank branches in the country. Amundi is also partnered with fellow French bank Société Générale (SCGLY)(SCGLF) to similar effect, while in certain European markets it has supply agreements with the likes of Italian banking giant UniCredit (UNCRY)(UNCFF). French partner distribution networks account for around 21% of Retail AUM, with international partner distribution networks (28%) and third-party distributors (51%) accounting for the rest.

Further, institutional clients account for the majority of Amundi's AUM. These are typically stickier compared to retail, therefore supporting earnings stability through the cycle. The Institutional segment encompasses central banks, pension funds, corporates and employee savings plans among others. Around 40% of Institutional AUM is tied up in the insurance mandates from Crédit Agricole & Société Générale. This is admittedly a relatively very low margin business (~3.7bps or so), but it is also very stable source of recurring management fees, thereby further adding stability to through-the-cycle revenues and earnings.

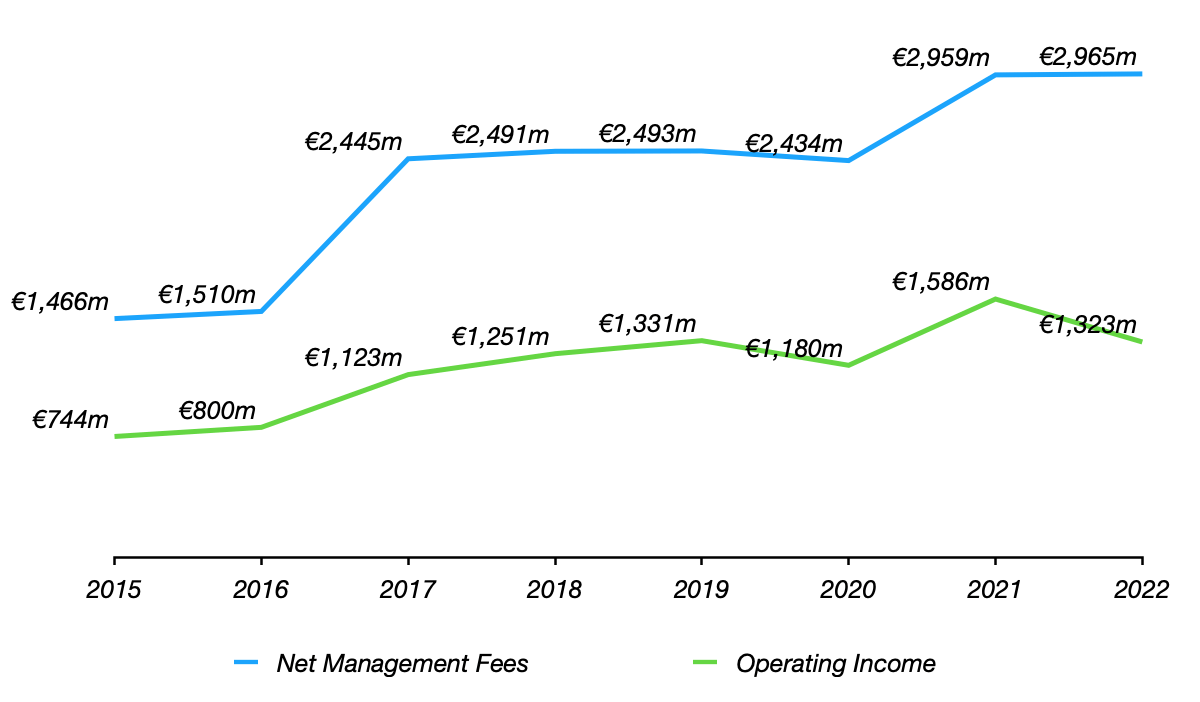

Amundi: Annual Net Management Fees & Operating Income

Data Source: Amundi Annual Reports

{kind=link}

By product line, Amundi is mostly in active solutions (~63% AUM ex. JVs). This exposes it to fee margin pressure due to the rise of passive investing, but with the acquisition of Lyxor a couple of years ago it is in the process of beefing up its passive offering and is the number two European ETF provider behind Blackrock (BLK). Amundi offers a broad range of asset classes, including bonds, real assets, equities and alternative assets. Operating a diversified product line also contributes to relatively stable fee generation across the cycle, as does the relatively low share of volatile performance fees (only ~6-7% of the overall mix) versus simple management fees.

Solid AUM Growth

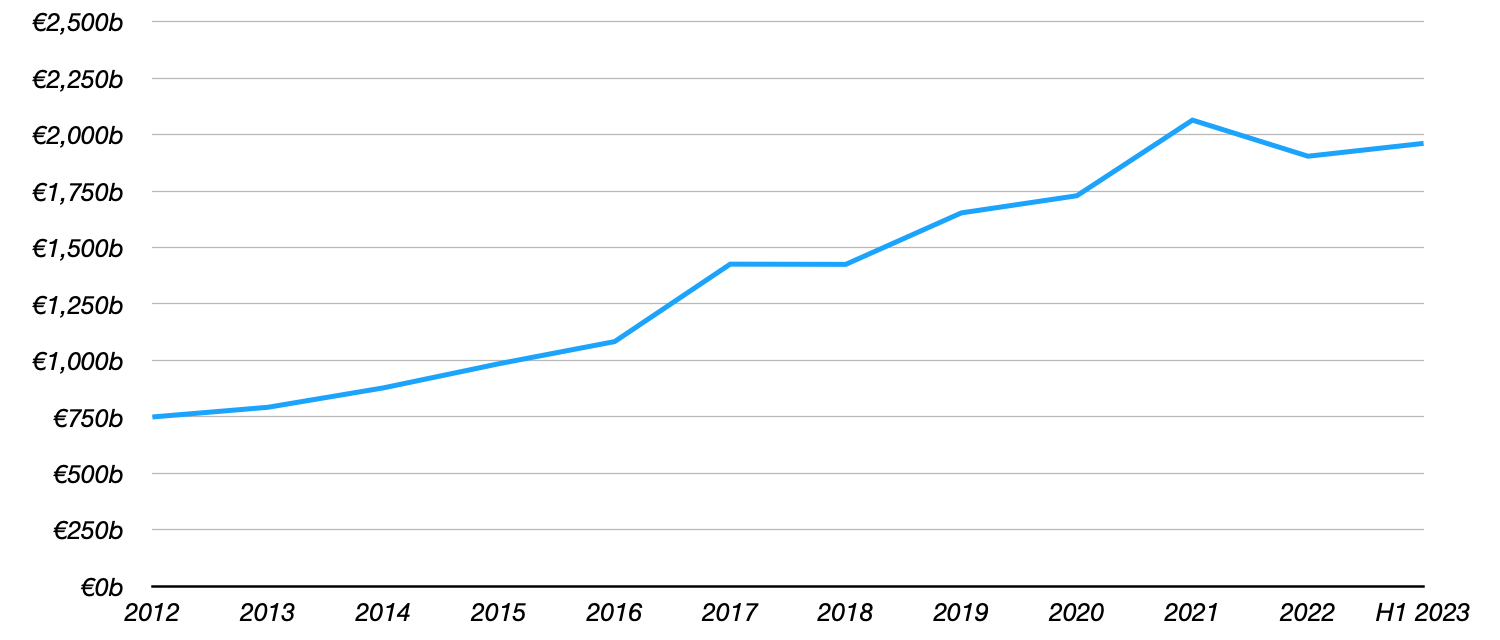

AUM growth has been robust, averaging around 10% per annum over the past decade.

Amundi: Assets Under Management

Data Source: Amundi annual reports and investor presentations

{kind=link}

While market effect (i.e. higher asset values) and M&A explains a portion of AUM growth, organic growth has been solid, with positive net inflows in each year since IPO, including in the challenging 2022 fiscal year. Organic AUM growth is important as dependence on market effect for growth will naturally lead to more volatile performance across a cycle.

Amundi: Annual Net Inflows

Data Source: Amundi Annual Reports

{kind=link}

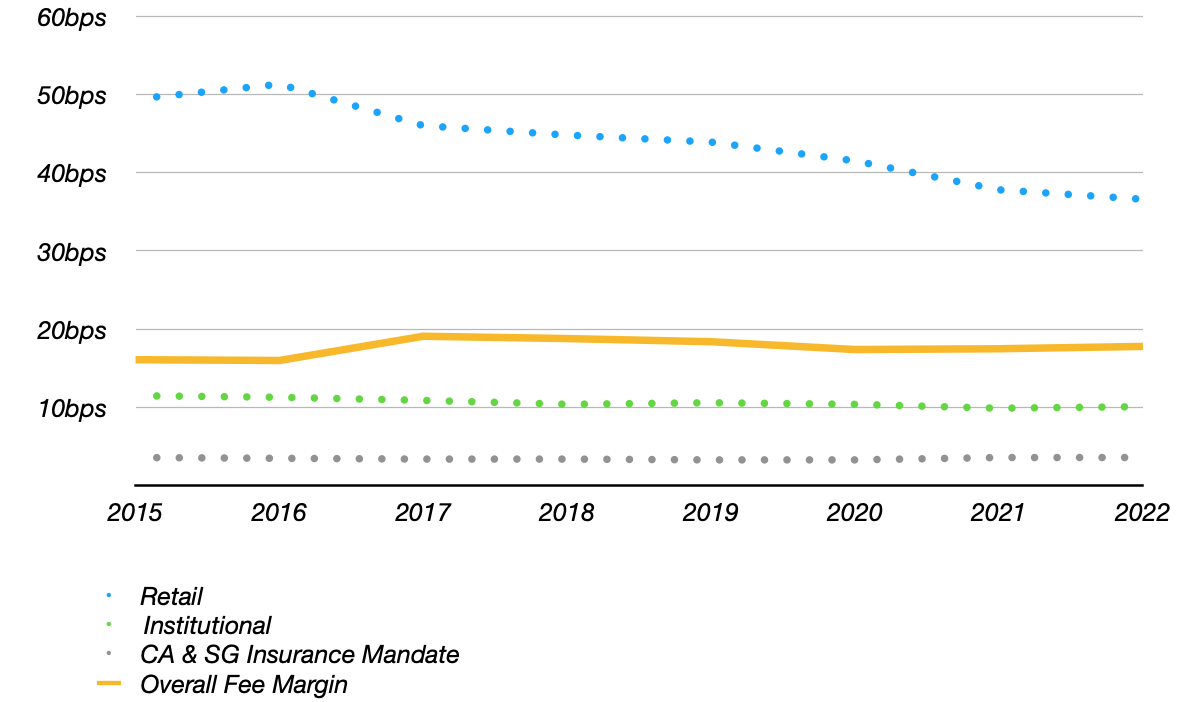

Amundi's past AUM growth has diversified management fees away from the Crédit Agricole & Société Générale insurance mandates. As mentioned above, these provide very dependable revenue to the company but are also very low margin.

In the year of its IPO (2015), assets attributable to the CA & SG insurance companies contributed approximately 45% of Amundi's total AUM and 10% of fee income. Those ratios had fallen to 21% and 5% respectively as of H1 2023. This has actually resulted in modest fee margin expansion in that time even though margins in each discrete client segment have been falling.

Amundi: Fee Margin By Client Segment

Data Source: Amundi Annual Reports

{kind=link}

In the long run, I expect margin contraction to present a persistent headwind to fee income growth. Group wide fee margins have generally been falling having added 3bps in 2016 (due principally to M&A activity that year).

Shares Reasonable Value

Amundi shares trade for €54.45 at time of writing in Paris, equivalent to around 10x prior-year EPS (FY22 EPS: €5.28 per share) and circa 1x book value per share ("BVPS"). In contrast, peer BlackRock, the largest pure-play listed asset manager in the US, trades at twice the P/E and 2.7x BVPS. A discount is probably warranted for a number of reasons, including:

- Amundi's relatively high share of active products compared to Blackrock's largely passive offering, which could result in downward pressure on fee margins and net flows at the former.

- Blackrock's consistently higher ROE, which has typically landed a few points ahead of Amundi's:

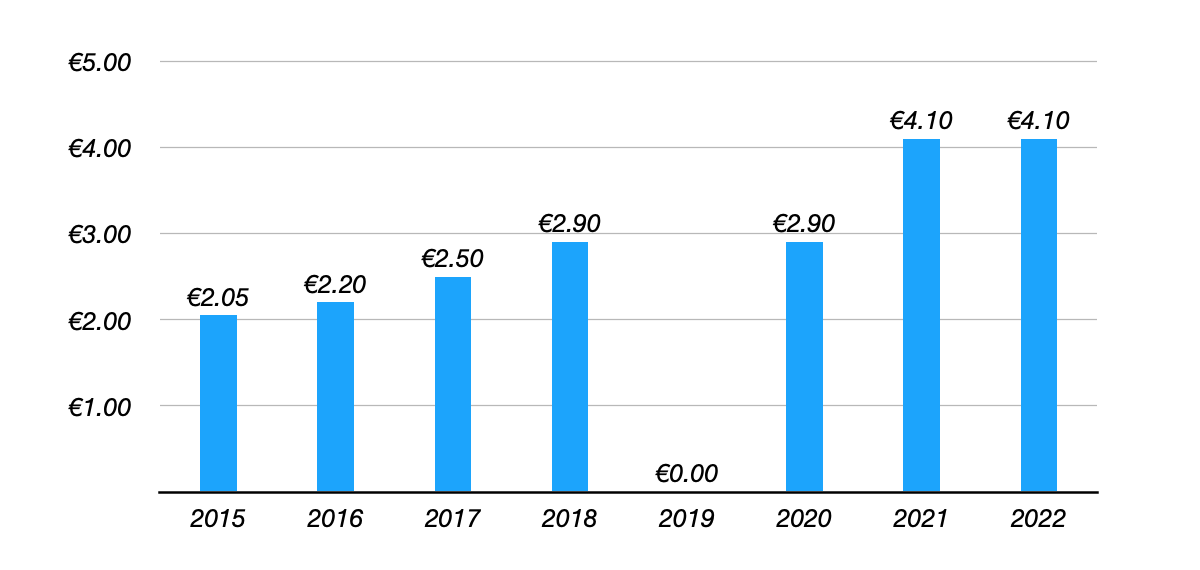

Nonetheless, Amundi's current valuation only needs very conservative long-term growth to deliver acceptable returns of shareholders. Management guides for a payout ratio of at least 65% of net income, so on a 10x P/E investors would receive high single-digits from cash distributions alone. Note the DPS has compounded at an 10.5% CAGR since IPO:

Amundi: Annual Dividend Per Share (2015 - 2022)

Data Source: Amundi Annual Reports

{kind=link}

I do expect that growth rate to slow down on a combination of fee margin pressure and lower positive AUM contributions from market effect, but in the long-run Amundi can contribute modest supplemental annual EPS/DPS growth based on a combination of:

- Natural organic growth potential in its nascent Asian businesses. AUM attributable to Asia has risen from €118B in 2015 to €376B (as of 1H 2023), equal to a circa 17% CAGR. Rising regional wealth is a long-term tailwind for AUM growth.

- Natural long-term positive market effect contribution, albeit this can be volatile over shorter timeframes (e.g. equity market corrections, interest rate changes and so on).

- A higher propensity for savers in its core markets to be in cash.

- Retained earnings that can fund inorganic growth via M&A, or in the absence of that additional capital returns to shareholders. An ROI of 10% on its surplus capital would alone be good for low single-digit per annum growth.

With Amundi's current share price reflecting fairly conservative long-term growth profile, these shares look like a credible option for value investors. Buy.

For further details see:

Amundi: The Market's Expectations Are Acceptably Conservative