HINKF - Anheuser-Busch InBev's Upside Isn't Over Quite Yet

2024-01-07 22:14:31 ET

Summary

- Investing in controversial companies can lead to attractive upside opportunities as others move away.

- Anheuser-Busch InBev has faced controversy but has shown strong financial results and growth in international markets.

- Despite some weaknesses, BUD's revenue, profits, and cash flows continue to rise, making it a slightly cheap buy.

Some of the most attractive investment opportunities can be had by investing when others won't dare. This can occur when the company in question happens to be highly controversial. Investors who cannot handle the heat of controversy or who are alienated by the company in question tend to move away from it. That causes shares to drop and opens the door for attractive upside. And I think everybody would agree with me that few companies were as controversial last year as the producer of Bud Light, Anheuser-Busch InBev SA/NV ( BUD ).

By this point, I probably do not need to go over the details of the controversy. They were widely reported and I even touched on them to some extent in an article that I published about the company earlier this year. In my most recent article about the company, published in early August, I covered financial results covering the second quarter of the 2023 fiscal year. I show that, while there were still some signs of weakness in the domestic market caused by the aforementioned controversy, the company as a whole was doing remarkably well. Domestic market share had stabilized and international growth was impressive. This led me to keep the company rated a 'buy' and encouraged me to claim that the firm had drink the 'go woke, go broke' mob under the table.

Now that so much time has passed, I figured it would be a good idea to revisit the situation. In addition to reporting additional financial results covering the third quarter of 2023, the company has also seen its share price spike 14.4% at a time when the S&P 500 was up a more modest 6.5%. Based on the most recent data available, I would argue that, in the long run, Anheuser-Busch is still certainly appealing. However, upside from this point is becoming more limited. I still think that the company is attractive enough to rate a 'buy', but only marginally so.

Continued growth amidst weakness

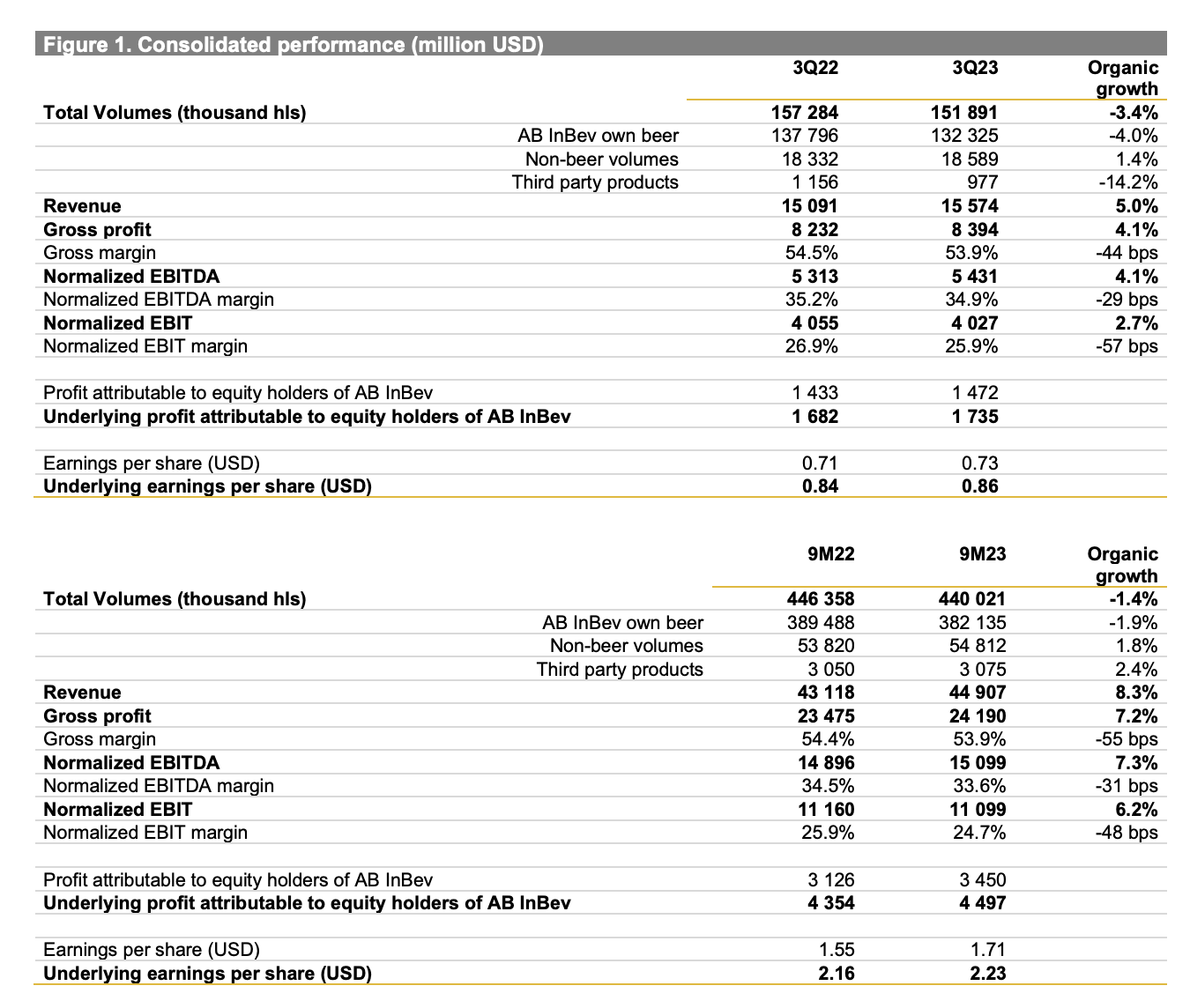

As a foreign business that's listed for trading in the US, Anheuser-Busch does not have to reveal comprehensive financial results each and every quarter. But it does come out with enough that gives us a good picture of the overall health of the enterprise. To start with, we should touch on the positive side of things. This would involve revenue and profits for the third quarter of the 2023 fiscal year. During that quarter, sales totaled $15.57 billion. That's 5% lower than the $15.09 billion generated one year earlier.

{kind=link}

As a massive, multinational company, there's a lot to unpack here. What goes into the revenue figure is a number of different things. For instance, on the negative side, the company reported a 3.4% decline in organic volume. Although some might point to this as a sign that the company is unhealthy, I detailed in one of the other articles that I wrote about the company, already linked to earlier in this piece, that volumes have been declining for years now. Beer volume has been particularly impacted, with sales down 4% on an organic basis. By comparison, non-beer volumes are actually up 1.4%. Also included in the mix is pricing. Year over year, revenue per hl (hectoliter) managed to rise by 9%.

{kind=link}

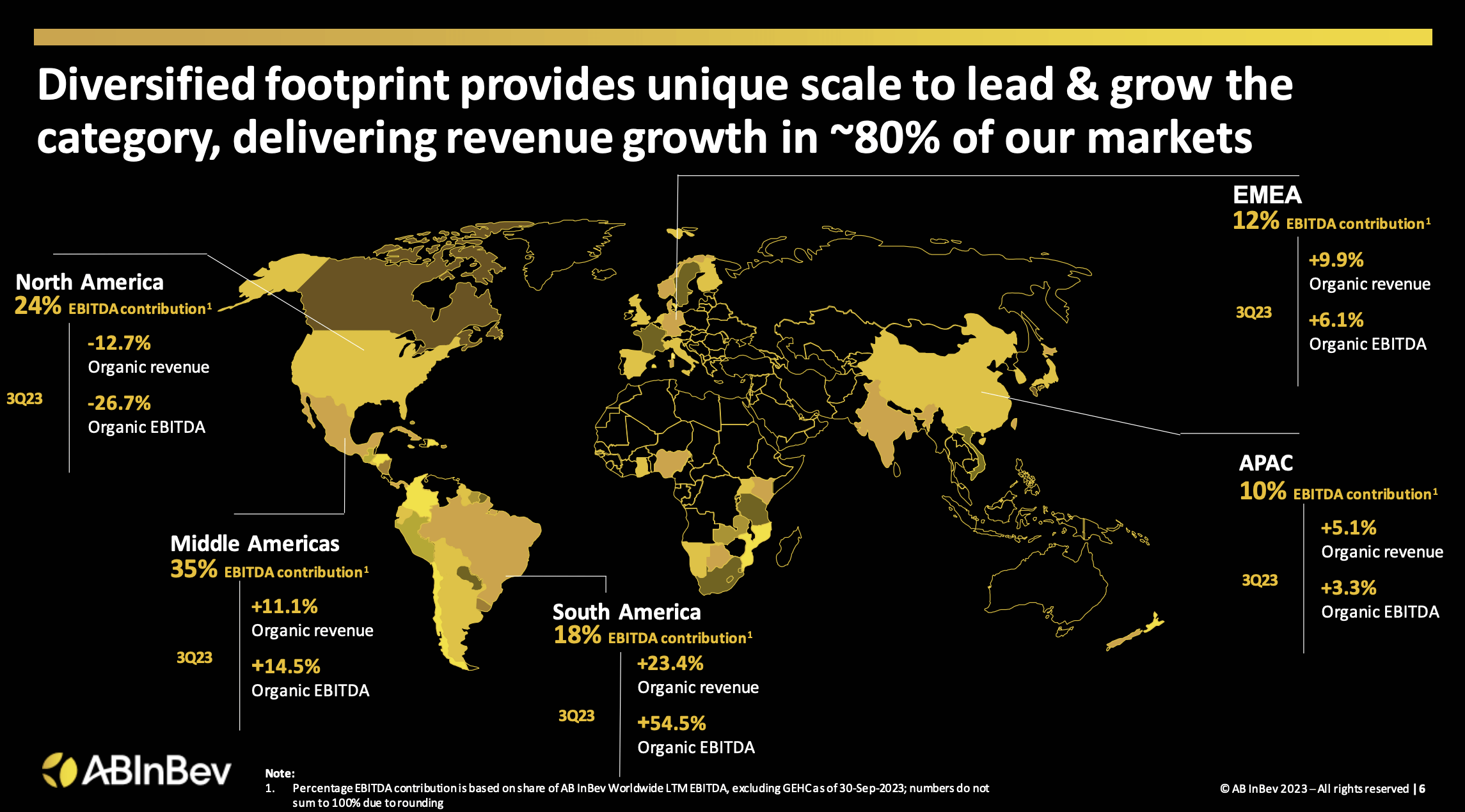

We can look at the data in an even more segmented manner. If we look at the North American market, which management considers to be just the US and Canada, organic revenue during the latest quarter was down 12.7%. Continued backlash against the Bud Light brand is likely to blame. But when you move outside of that market, the firm has experienced rapid growth. In the Middle Americas, organic revenue jumped 11.1% year over year. In South America, growth was an even more impressive 23.4% on an organic basis. Across the EMEA (Europe, Middle East, and Africa) regions, organic revenue jumped 9.9%. And even in the Asia Pacific region, organic revenue managed to climb a modest 5.1%.

{kind=link}

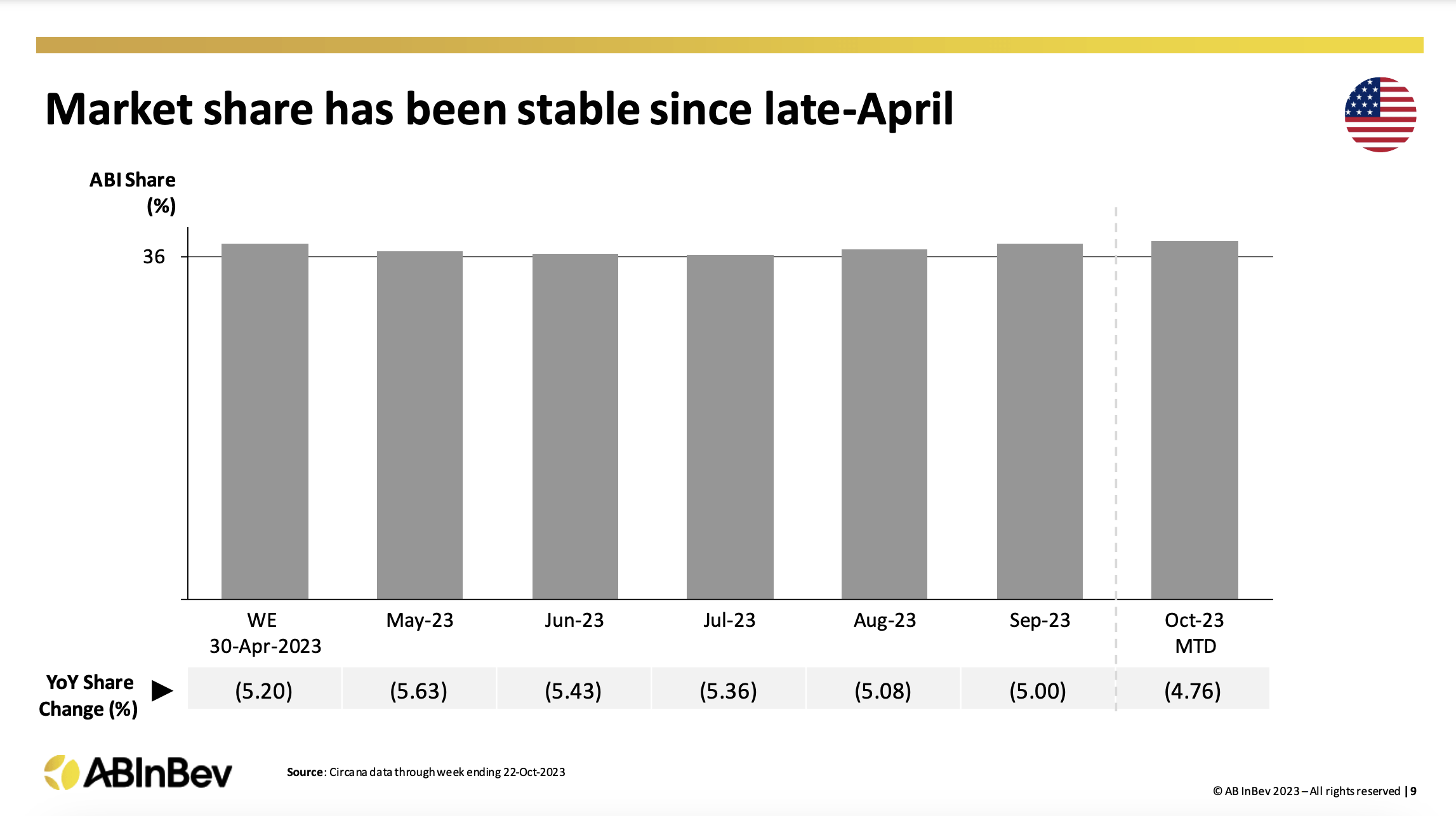

Even though the US market has been a source of pain for the company, management asserts that market share here at home has stabilized since late April. During this time, it has been hovering around 36% of the overall market. Globally, the company has some major leading brands that are continuing to achieve rapid growth. Outside of Mexico, for instance, the Corona brand has seen an 18.8% year over year increase in revenue in the third quarter. Outside of the US, organic revenue associated with Budweiser has jumped 11.8%. And outside of the US, Michelob Ultra has jumped by 11.5%. The most impressive, however, has been the Stella Artois brand, which reported a 20.3% increase in revenue outside of Belgium.

{kind=link}

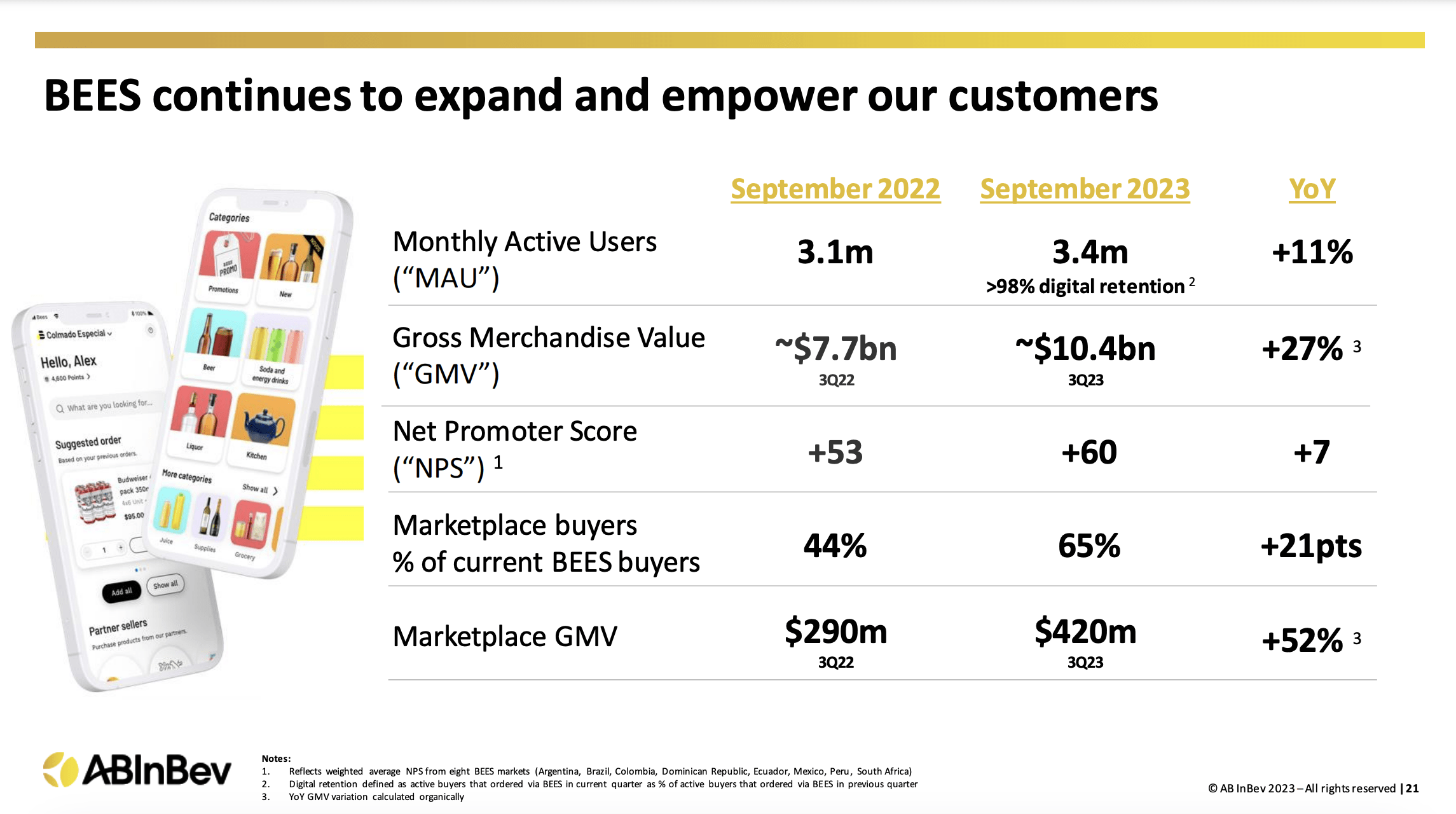

Management is also continuing to achieve progress when it comes to some of the interesting initiatives the company has invested in over the years. BEES, a digital ordering platform that connects consumers directly to the company, reported 3.4 million MAUs (monthly active users) in September of 2023. That's up from the 3.1 million reported one year earlier and it compares favorably to the 3.3 million reported for June of last year. Gross merchandise value transacted on the platform has skyrocketed, jumping around 27% year over year from $7.7 billion in the third quarter of 2022 to $10.4 billion at the same time this year. Meanwhile, the gross merchandise value for the company's marketplace on the service managed to jump 52% from $290 million to $420 million. Over the same window of time, revenue associated with the company's digital direct to consumer mega brands has jumped around 9% from $110 million in the third quarter to $125 million, with the number of online orderings remaining unchanged at 17 million but the number of active consumers jumping from 8.9 million last year to 10 million this year.

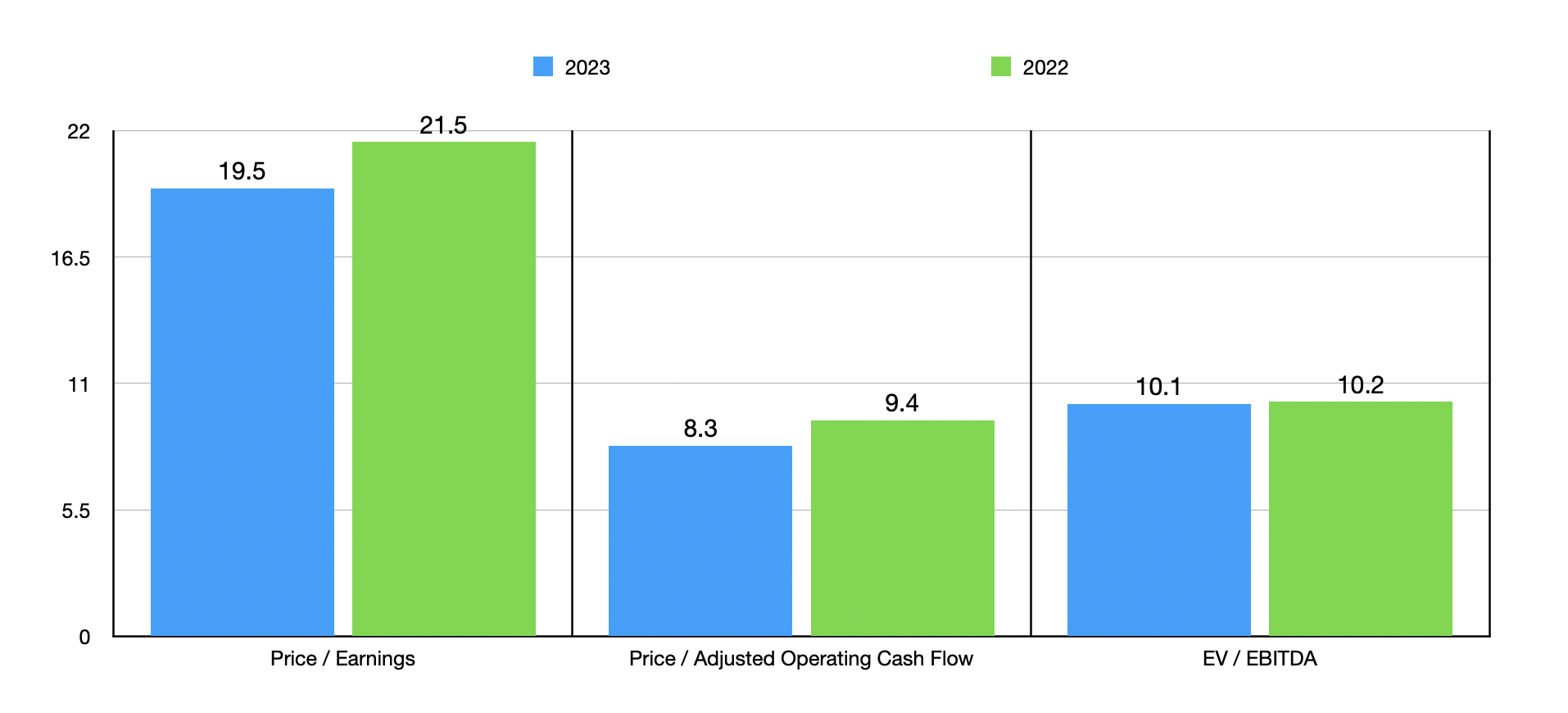

This growth in revenue brought with it higher profits and cash flows as well. Net income, for instance, went from $1.43 billion in the third quarter of 2022 to $1.47 billion in the third quarter of this year. Meanwhile, EBITDA has grown from $5.31 billion to $5.43 billion. Earlier in this article, I mentioned how certain data is not reported. The most recent data that we have for operating cash flow, for instance, is from the first half of 2022. And in that window of time, it was down 26.8%. But if we adjust for changes in working capital, it is up 12.5%. Also, for context, you can see the aforementioned financial results for the first nine months of the 2023 fiscal year compared to the first nine months of the 2022 fiscal year, as shown in the chart below. With this increased profitability and likely recognizing that the stock is undervalued, management initiated a $1 billion share buyback program. That was approved on October 30th, which was one day prior to the company approving a cash tender offer of up to $3 billion for the acquisition of outstanding bonds. From the time the share buyback program was announced through December 22nd, the company repurchased over 5.66 million shares for around $352.2 million.

{kind=link}

Based on the current data available, I believe that net profits for 2023 will have ended up being around $6.59 billion. Adjusted operating cash flow should be somewhere around $15.35 billion, while EBITDA should be somewhere around $20.11 billion. Based on these estimates, I was able to value the company as shown in the chart above. On a forward basis, shares do look a bit cheaper than if we were to use the data from 2022. I then, in the table below, compared the firm to five similar companies. On a price to earnings basis, two of the five firms were cheaper than it. Using the price to operating cash flow approach, Anheuser-Busch ended up being the cheapest of the group. And lastly, using the EV to EBITDA approach, I found that two of the five companies ended up being cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Anheuser-Busch InBev SA/NV |

| 19.5 |

| 8.3 |

| 10.1 |

| Heineken N.V. ( OTCQX:HEINY ) |

| 21.6 |

| 16.6 |

| 12.5 |

| Ambev S.A. ( ABEV ) |

| 14.7 |

| 9.8 |

| 9.5 |

| Molson Coors Beverage Company ( TAP ) |

| 53.2 |

| 6.7 |

| 13.3 |

| Carlsberg A/S ( OTCPK:CABGY ) |

| 16.0 |

| N/A |

| 9.3 |

| The Boston Beer Company ( SAM ) |

| 51.1 |

| 20.5 |

| 17.9 |

Takeaway

From all that I can see at the moment, there are still some signs of weakness regarding Anheuser-Busch. However, for the most part, the fundamental picture is healthy. Revenue, profits, and cash flows continue to rise. Shares are not exactly cheap. But they are slightly cheap relative to similar firms. So even in spite of the continued weaknesses and the nice increase in price that shares have seen so far since I last wrote about the company, I would argue that a soft 'buy' rating still makes sense at this time.

For further details see:

Anheuser-Busch InBev's Upside Isn't Over Quite Yet