RCA - Annaly Capital's BV Sector Valuation And Dividend Sustainability Vs. 19 mREIT Peers - Part 2 (Includes Q1 2023 + Q2 2023 Dividend Projection)

Summary

- This article compares NLY’s recent dividend per share rates, yield percentages, and several dividend sustainability metrics to 19 mREIT peers.

- This includes an analysis of NLY’s quarterly estimated REIT taxable income, estimated core earnings, and normalized core earnings which directly impact the company's dividend sustainability.

- This article also discusses NLY’s dividend decrease for the second quarter of 2020 and projects NLY’s dividend sustainability for Q1 2023 and Q2 2023.

- Contrary to some recent opinions, it is not “a given” NLY will need to reduce the company’s dividend during early 2023, even as borrowing costs have quickly risen.

- However, when compared to sector peers, NLY is currently deemed to be slightly overvalued. Most peers trade at a discount to CURRENT BV while NLY trades at a modest premium.

Focus of Article:

The focus of this two-part article is to provide a very detailed analysis comparing Annaly Capital Management Inc. ( NLY ) to 19 other mortgage real estate investment trust (mREIT) peers I currently fully cover. I am writing this two-part article due to the continued requests that such an analysis be specifically performed on NLY and some of the company’s mREIT peers at periodic intervals. F or readers who just want the summarized conclusions/results, I would suggest to scroll down to the “Conclusions Drawn” section at the bottom of each part of the article.

PART 1 of this article analyzed NLY’s recent results and compared several of the company’s metrics to 19 mREIT peers. PART 1 also showed how NLY’s book value (“BV”) as of 9/30/2022 compared to the 19 other mREIT peers. PART 1 helps lead to a better understanding of the topics and analysis that will be discussed in PART 2. The link to PART 1’s analysis is provided below:

REIT Forum Version (Expanded Analytics):

Scott Kennedy’s mREIT Sector Comparison Article: Annaly Capital’s BV , Sector Valuation, And Dividend Versus 19 mREIT Peers – Part 1 (Post Q3 2022 Earnings)

Public Version:

A nnaly Capital's BV , Sector Valuation, And Dividend Vs. 19 MREIT Peers - Part 1 (Post Q3 2022 Earnings)

The focus of PART 2 of this article is to compare NLY’s recent dividend per share rates, yield percentages, and several dividend sustainability metrics to 19 mREIT peers. This analysis will show recent past data with supporting documentation within Table 9 below. This article will also discuss NLY’s dividend sustainability which is partially based on the metrics outlined in Table 9. A more in-depth analysis of NLY’s dividend sustainability will be provided in Table 10 below. This includes a discussion of NLY’s dividend decrease of ($0.03) per common share which occurred during the second quarter of 2020.

By analyzing these metrics, one will better understand which mREIT generally has a safer dividend rate going forward versus other peers who generally have a higher risk for a dividend decrease or a higher probability of a dividend increase and/or a special periodic dividend being declared. When both back testing and projecting the metrics within this analysis, the results have continued to be proven extremely reliable. This is not the only data that should be examined to initiate a position within a particular stock/sector. However, I believe this analysis would be a good “starting-point” to begin a discussion on the topic. At the end of this article, there will be a conclusion regarding the following comparisons between NLY and the 19 mREIT peers: 1) trailing 12-month (“TTM”) yields based on a stock price as of 12/30/2022 (including 1- and 3-year dividend change) ; 2) annual forward yield based on a stock price as of 12/30/2022 ;and 3) annual forward yield based on my estimated CURRENT BV (BV as of 12/31/2022) . I will also provide my current BUY, SELL, or HOLD recommendation, dividend per share rate projection for the first quarter of 2023 and second quarter of 2023, and price target on NLY.

Side Note: I believe there are several different classifications when it comes to mREIT companies. For purposes of this article, I am focusing on 4. For readers who are new to my articles or for existing readers who need a “refresher” on several different mREIT classifications, please see PART 1 of this article (link provided above).

Dividend Per Share Rates and Yield Percentages Analysis - Overview:

Let us start this analysis by getting accustomed to the information provided in Table 9 below. This will be beneficial when comparing NLY to the 19 mREIT peers within this analysis.

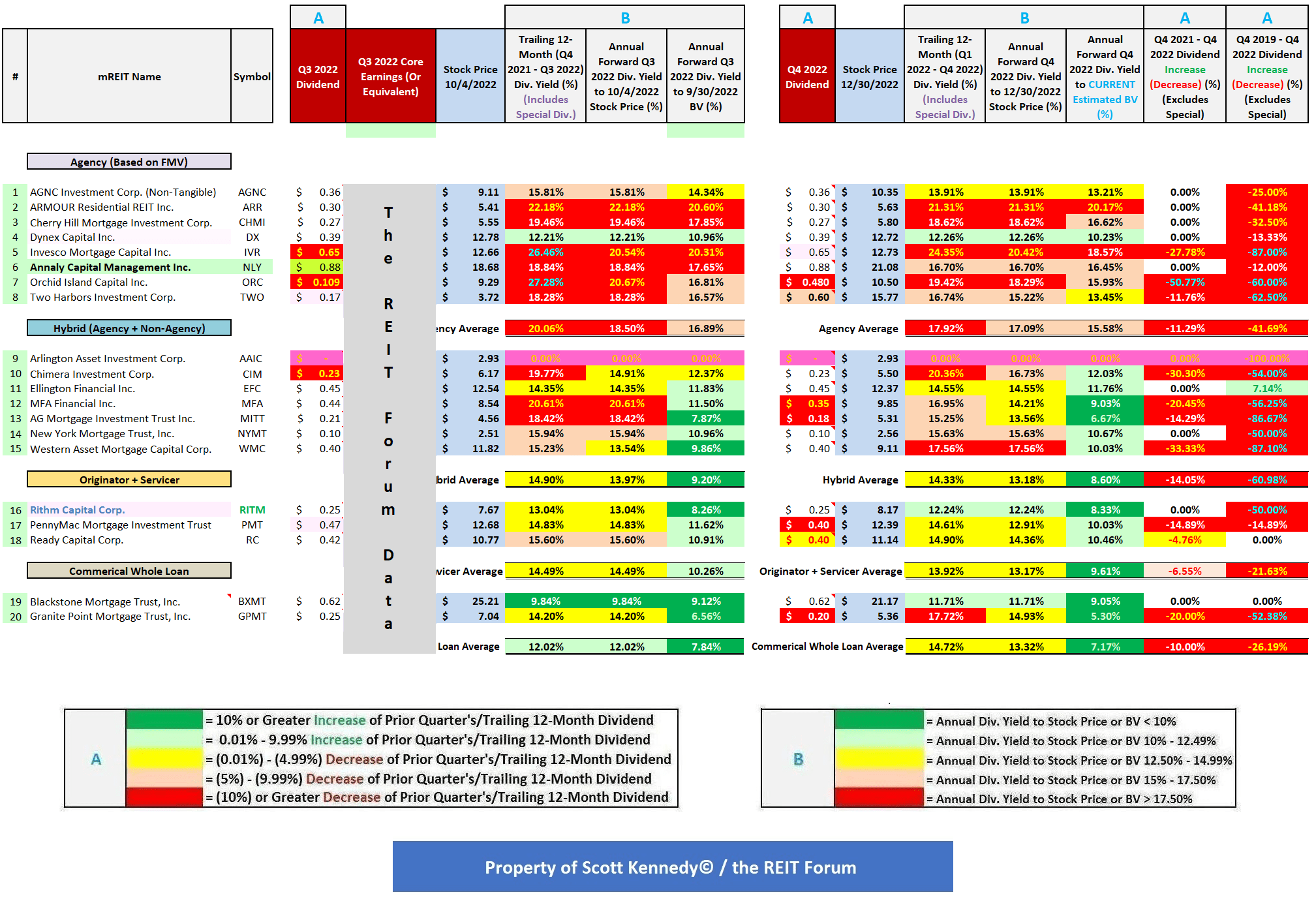

Table 9 – Dividend Per Share Rates and Yield Percentages

{kind=link}

(Source: Table created by me, obtaining historical stock prices from NASDAQ and each company’s dividend per share rates from the SEC’s EDGAR Database )

Note: Table 9 does NOT retroactively apply ORC’s and TWO’s 1:5 and 1:4 reverse stock split, respectively, to each company’s dividend per share rate for the third quarter of 2022.

Using Table 9 above as a reference, the following information is provided (see each corresponding column): 1) dividend per share rate for the third quarter of 2022 (for monthly dividend payers, the total monthly dividends during the quarter) ; 2) core earnings (or core earnings equivalent) for the third quarter of 2022 ; 3) stock price as of 10/4/2022 ; 4) TTM dividend yield (dividend per share rate from the fourth quarter of 2021-third quarter of 2022) ; 5) annual forward dividend yield based on the dividend per share rate for the third quarter of 2022 using the stock price as of 10/4/2022 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 6) annual forward dividend yield based on the dividend per share rate for the third quarter of 2022 using a BV as of 9/30/2022 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 7) dividend per share rate for the fourth quarter of 2022 (for monthly dividend payers, the total monthly dividends during the quarter) ; 8) stock price as of 12/30/2022 ; 9) TTM dividend yield (dividend per share rate from the first quarter of 2022-fourth quarter of 2022) ; 10) annual forward dividend yield based on the dividend per share rate for the fourth quarter of 2022 using the stock price as of 12/30/2022 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 11) annual forward dividend yield based on the dividend per share rate for the fourth quarter of 2022 using estimated CURRENT BV (BV as of 12/31/2022) (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 12) dividend per share rate for the fourth quarter of 2022 versus the fourth quarter of 2021 (percentage fluctuation) ; and 13) dividend per share rate for the fourth quarter of 2022 versus the fourth quarter of 2019 (percentage fluctuation; shows COVID-19 impact to each company’s dividend ).

As of 12/30/2022, NLY, AGNC Investment Corp. ( AGNC ), ARMOUR Residential REIT Inc. ( ARR ), Cherry Hill Mortgage Investment Corp. ( CHMI ), Dynex Capital Inc. ( DX ), Orchid Island Capital Inc. ( ORC ), Chimera Investment Corp. ( CIM ), Ellington Financial Inc. ( EFC ), MFA Financial Inc. ( MFA ), AG Mortgage Investment Trust Inc. ( MITT ), New York Mortgage Trust, Inc. ( NYMT ), Western Asset Mortgage Capital Corp. ( WMC ), Rithm Capital Corp. ( RITM ) (formerly New Residential Investment Corp.), PennyMac Mortgage Investment Trust ( PMT ), Ready Capital Corp. ( RC ), Blackstone Mortgage Trust, Inc. ( BXMT ), and Granite Point Mortgage Trust, Inc. ( GPMT ) had a stock price that “reset” lower regarding each company’s monthly/quarterly dividend accrual. In other words, each company’s “ex-dividend date” for December 2022/the fourth quarter of 2022 had already occurred.

As of 12/30/2022, Invesco Mortgage Capital Inc. ( IVR ) and Two Harbors Investment Corp. ( TWO ) had a stock price that had not reset lower in reference to the company’s December 2022/the fourth quarter of 2022 dividend accrual. Arlington Asset Investment Corp. ( AAIC ) did not declare a common stock dividend for the fourth quarter of 2022. Readers should take these points into consideration as the analysis is presented below. Let us now begin the comparative analysis between NLY and the 19 mREIT peers.

Analysis of NLY:

Using Table 9 above as a reference, NLY declared a dividend of $0.88 per common share for the third quarter of 2022 (post-reverse 1:4 stock split). This was an unchanged per common share dividend when compared to the prior quarter on a split-adjusted basis. It should also be noted previously, after 22 consecutive quarters of a stable quarterly per share rate, NLY decreased the company’s common stock dividend by ($0.20) per share (on a reverse split-adjusted basis) during the second quarter of 2019. Due to the fact NLY aggressively reduced the company’s dividend from $2.60 per share during the fourth quarter of 2011 to $1.20 per share by the fourth quarter of 2013 (on a reverse split-adjusted basis), the company was also able to maintain its quarterly dividend per share rate over a longer time period when compared to most sector peers (especially its fixed-rate agency mREIT sub-sector peers). Mainly due to a flattening yield curve that began back in 2018, along with the continued less “specialness” when it came to dollar-roll (off-balance sheet) financing, there was mounting pressure for NLY to reduce the company’s dividend per share rate as 2019 progressed as short-term interest rates rose to 2.50%-2.75%.

NLY’s ($0.12) per common share dividend decrease for the second quarter of 2020 (on a reverse split-adjusted basis) was mainly the result of the lower size of NLY’s investment portfolio coming out of the initial COVID-19 “pandemic panic” during March 2020. During this timeframe, prior to the Federal (“Fed”) Reserve’s quick, decisive action to calm markets through both interest rate and monetary policy, repurchase (“repo”) agreement and hedging counterparties quickly (and incorrectly in my opinion) initiated margins calls on most sector peers which created a “snowball” effect on this specific market. This included both agency and non-agency mortgage-related investments. In other words, there was a quick, sharp leverage/liquidity crisis across certain pockets of credit markets where certain assets/investments are used as collateral to underlying outstanding borrowings/debt. Most sector peers either voluntarily, or were forced, to deleverage and raise cash during this time period. Results varied greatly from peer-to-peer regarding the severity of each company’s investment portfolio reduction. NLY was one of the sector peers who actually came out of the COVID-19 pandemic panic not too much “worse for wear” . Some agency, most hybrid, some originator + servicer, and some commercial whole loan mREIT peers could not make the same claim.

NLY’s stock price traded at $18.68 per share on 10/4/2022. When calculated, this was a TTM dividend yield of 18.84%, an annual forward yield to NLY’s stock price as of 10/4/2022 of 18.84%, and an annual forward yield to the company’s BV as of 9/30/2022 of 17.65%. When comparing each yield percentage to NLY’s agency mREIT peers within this analysis, the company’s TTM dividend yield percentage was modestly (at or greater than 1.00% but less than 2.00%) below average, the company’s annual forward yield percentage based on its stock price was near (within 0.50%) average, and its annual forward yield percentage based on its BV as of 9/30/2022 was slightly (greater than 0.50% but less than 1.00%) above average.

As was discussed in PART 1 of this article, as of 9/30/2022 NLY had the 4th lowest at-risk leverage ratio (on- and off-balance sheet) when compared to the 7 other agency mREIT sub-sector peers within this analysis. NLY typically runs lower leverage versus most of its fixed-rate agency mREIT peers. From charting past trends, typically lower leverage ratios within the fixed-rate agency mREIT sector generally equate to below average-average dividend yield percentages. Of course, there are various other factors at play regarding dividend sustainability (especially in light of the events surrounding the COVID-19 pandemic panic back in March 2020). However, a company’s leverage ratio is one “general” metric which I believe should be analyzed.

I continue to believe three important metrics to analyze when assessing NLY’s near-term dividend sustainability are the company’s quarterly estimated REIT taxable income (“ERTI”), estimated core earnings (“ECE”), and its normalized core earnings (“NCE”). NLY’s earnings available for distribution (“EAD”) is now the equivalent to the company’s previously disclosed NCE. As such, the terms are interchangeable within this article. Currently, NLY’s NCE (or EAD) is the closest metric to the company’s “true earnings power” regarding its investment portfolio’s performance. To analyze/explain these three metrics, Table 10 is provided below.

Table 10 – NLY Quarterly ERTI, ECE, and NCE/EAD Analysis (Q1 2020 – Q3 2022)

{kind=link}

The REIT Forum

(Source: Table created by me, partially using data obtained from NLY’s quarte rly shareholder presentation for the first quarter of 2019–third quarter of 2022 )

Note: Table 10 does NOT retroactively apply NLY’s 9/23/2022 1:4 reverse stock split to periods prior to the third quarter of 2022.Most important, applying or not applying NLY’s 9/23/2022 1:4 reverse stock split does NOT impact the results of the company’s quarterly dividend distributions payout ratio [same payout ratio regardless]).

Using Table 10 above as a reference, NLY reported quarterly ERTI available to common shareholders of NLY reported quarterly ERTI available to common shareholders of ($40.9) million for the first quarter of 2020 (see red reference “E” ). When calculated, NLY had ERTI available to common shareholders of ($0.03) per share (see red reference “E / F” ). This figure was notably below the company’s dividend of $0.25 per common share for the first quarter of 2020.

However, this figure excluded the impact of NLY’s net long “to-be-announced” (“TBA”) mortgage-backed securities (“MBS”) position. When including “net dollar roll” (“NDR”) income of $44.9 million (see red reference “G” ), NLY reported quarterly ECE available to common shareholders of $4.0 million for the first quarter of 2020 (see red reference “I” ). When calculated, NLY had quarterly ECE available to common shareholders of less than $0.01 per share (see red reference “I / F” ).

However, NCE considers an additional Generally Accepted Accounting Principles (“GAAP”) to IRC adjustment when compared to quarterly ERTI and ECE (specifically when it comes to NLY) . When it comes to most other mREIT peers, this specific adjustment is performed within each mREIT’s quarterly ERTI figure. Very important to understand. Dependent upon management’s projected lifetime conditional prepayment rate (“CPR”) in regards to NLY’s MBS portfolio, the “catch-up” premium amortization expense adjustment can materially alter the company’s quarterly ERTI and ECE figures. NCE excludes/reverses this GAAP adjustment since an entity’s cost basis per the IRC is not par.

As such, when also including NLY’s catch-up premium amortization expense adjustment of $290.7 million (see red reference “L” ), the company reported NCE/EAD available to common shareholders of $294.7 million for the first quarter of 2020 (see red reference “N” ). When calculated, NLY had NCE/EAD available to common shareholders of $0.21 per share (see red reference “N / F” ). NLY’s NCE/EAD calculates to a quarterly dividend distributions payout ratio of 121% for the first quarter of 2020 (see red reference “J / N” ). This percentage surpassed the third quarter of 2019 as being NLY’s highest quarterly dividend distributions payout ratio since the first quarter of 2014.

As such, the pressure to consider reducing NLY’s quarterly common stock dividend of $0.25 per share, which began back in the second half of 2019, only mounted with the company’s performance of this specific metric during the first quarter of 2020 (which I correctly stated at the time). I believe two of the main reasons why NLY reduced the company’s quarterly common stock dividend during the second quarter of 2020 were the following: 1) reduction in investment portfolio size as a direct result of the “spike” in leverage, liquidity ; and 2) spread/basis risk in March 2020 as a direct result of the COVID-19 pandemic panic (including the impact this event had on broader credit/equity markets).

With that said, NLY’s quarterly dividend was reduced twice within five quarters. Simply from an annual taxation standpoint, this boded well for dividend sustainability in the future (less taxable income is being paid out during the year; leading to less “short-falls” at year-end). As important, NLY’s “prospects” for taxable income over the foreseeable future “brightened” as a direct result of the early 2020 rapid decline of the Fed Funds Rate; which in turn caused a quick drop in agency repo loan rates. In addition, the specialness/attractiveness of the forward TBA MBS market once again increased (especially within lower coupons).

At the time, since the probability of short-term rates remaining “lower for longer” appeared to greatly outweigh the 2018-2019 trend of rising short-term interest rates, mREIT peers who continued (or “rotated” ) capital into agency MBS experienced attractive net interest margins (even as lower coupons become a greater share of the secondary MBS market). This began to play out during the second quarter of 2020 which continued during the third and fourth quarters of 2020 (which was previously correctly projected). The magnitude of borrowing cost decreases “outweighed” continued elevated prepayments and the gradual shift into lower coupons. As such, net portfolio yields are an important metric to continually monitor (which is something I always project/track).

NLY reported quarterly ERTI available to common shareholders of $239.8, $298.8, and $285.4 million for the second, third, and fourth quarters of 2020, respectively. When calculated, NLY had ERTI available to common shareholders of $0.17, $0.21, and $0.20 per share, respectively. These figures were slightly-modestly below the company’s dividend of $0.22 per common share for the second-fourth quarters of 2020. As discussed earlier, this figure excluded the impact of NLY’s net long TBA MBS position and lifetime CPR adjustment. When including NDR income of $97.5, $114.1, and $99.0 million, NLY reported quarterly ECE available to common shareholders of $337.3, $412.9, and $384.4 million for the second, third, and fourth quarters of 2020, respectively. When calculated, NLY had quarterly ECE available to common shareholders of $0.24, $0.29, and $0.27 per share, respectively.

When also including NLY’s catch-up premium amortization expense adjustment of $51.7, $33.9, and $39.1 million, the company reported NCE/EAD available to common shareholders of $389.1, $446.8, and $423.5 million for the second, third, and fourth quarters of 2020, respectively. When calculated, NLY had NCE/EAD available to common shareholders of $0.27, $0.32, and $0.30 per share, respectively. This calculates to a quarterly dividend distributions payout ratio of 80%, 69%, and 73%, respectively. With the nice “bounce back” in NLY’s NCE/EAD, along with the reduced dividend, these were the lowest quarterly dividend distributions payout ratios since the I began covering this mREIT back in the first quarter of 2013 (a very positive catalyst/trend).

Moving to 2021, NLY reported quarterly ERTI available to common shareholders of $528.3, $159.3, $234.3, and $236.1 million for the first, second, third, and fourth quarters of 2021, respectively. When calculated, NLY had ERTI available to common shareholders of $0.38, $0.11, $0.16, and $0.16 per share, respectively. This figure was notably above, notably below, modestly below, and modestly below the company’s dividend of $0.22 per common share for the first, second, third, and fourth quarters of 2021, respectively. As discussed earlier, this figure excluded the impact of NLY’s net long TBA MBS position and lifetime CPR adjustment. When including NDR income of $98.9, $111.6, $115.6, and $119.7 million, NLY reported quarterly ECE available to common shareholders of $627.2, $270.9, $349.9, and $355.8 million for the first, second, third, and fourth quarters of 2021, respectively. When calculated, NLY had quarterly ECE available to common shareholders of $0.45, $0.19, $0.24, and $0.24 per share, respectively. When also including NLY’s catch-up premium amortization expense adjustment of ($214.6), $153.6, $60.7, and $57.4 million, the company reported NCE available to common shareholders of $412.6, $424.5, $410.6, and $413.2 million for the first, second, third, and fourth quarters of 2021, respectively. When calculated, NLY had NCE available to common shareholders of $0.29, $0.30, $0.28, and $0.28 per share, respectively. This calculates to a quarterly dividend distributions payout ratio of 75%, 75%, 78%, and 78% for the first, second, third, and fourth quarters of 2021, respectively. Simply put, an attractive quarterly dividend distributions payout ratio throughout 2021.

Moving to 2022, NLY reported quarterly ERTI available to common shareholders of $453.8, $429.8, and $393.7 million for the first, second, and third quarters of 2022, respectively. When calculated, NLY had ERTI available to common shareholders of $0.31, $0.28, and $0.92 per share, respectively (third quarter of 2022 includes the impact of NLY’s 9/23/2022 1:4 reverse stock split). As discussed earlier, this figure excluded the impact of NLY’s net long TBA MBS position and lifetime CPR adjustment. When including NDR income of $129.5, $161.7, and $105.5 million, NLY reported quarterly ECE available to common shareholders of $583.3, $591.4, and $499.2 million for the first, second, and third quarters of 2022, respectively. When calculated, NLY had quarterly ECE available to common shareholders of $0.40, $0.39, and $1.16 per share, respectively (third quarter of 2022 includes the impact of NLY’s 9/23/2022 1:4 reverse stock split). When also including NLY’s catch-up premium amortization expense adjustment of ($179.5), ($127.5), and ($45.4) million, the company reported NCE available to common shareholders of $403.7, $463.9, and $453.8 million for the first, second, and third quarters of 2022, respectively. When calculated, NLY had NCE available to common shareholders of $0.28, $0.30, and $1.056 per share, respectively (third quarter of 2022 includes the impact of NLY’s 9/23/2022 1:4 reverse stock split). This calculates to a quarterly dividend distributions payout ratio of 80%, 77%, and 91% for the first, second, and third quarters of 2022, respectively. Simply put, a fairly attractive quarterly dividend distributions payout ratio this past quarter but the margin has shrunk some.

When compared to my NLY NCE/EAD projection of $1.080 per common share for the second quarter of 2022 (provided to subscribers of the REIT Forum), NLY’s NCE/EAD of $1.056 per common share was nearly an exact match-very minor underperformance (well within my range was $1.005-$1.155 per share). On a reverse split adjusted basis, NLY’s NCE/EAD was $1.218 per common share for the second quarter of 2022. As such, I projected a NCE/EAD decrease of ($0.138) per common share. In actuality, NLY reported a NCE/EAD decrease of ($0.162) per common share. The institutional analysts’ consensus average was NCE/EAD of $0.994 per common share for the third quarter of 2022. As such, my projection was slightly-modestly more accurate when compared to the institutional analysts’ consensus average (a consistent theme within most covered mREIT peers this past earnings season).

Including this past quarter, I personally have beaten the institutional analysts’ consensus average on earnings in 39 out of a total of 42 quarters regarding the stocks I personally cover in 2 different sectors. This calculates to a 92.9% outperformance rating. Simply put, to be among the best (regarding projecting valuations/earnings), you have to get your hands dirty (have to put in the extensive research/work necessary to set [and keep] the bar high). This is especially true when it comes to any type of paid, subscriber-based platform in my professional opinion. This is something long-term readers/subscribers of our service have come to know, understand, and rely upon quarter-after-quarter, year-after-year. This is why this particular Marketplace Service has continued to have an extremely high subscriber retention rate when compared to other services/teams. I/we put the work in so subscribers have accurate, reliable data which ultimately enables them to make more informed decisions on their investment decisions/strategies.

Once again using Table 9 as a reference, NLY declared a dividend of $0.88 per share for the dividend quarter of 2022. This was an unchanged dividend when compared to the prior quarter when factoring in the 9/23/2022 1:4 reverse stock split. NLY’s stock price traded at $21.08 per share on 12/30/2022. When calculated, this was a TTM dividend yield of 16.70%, an annual forward yield to NLY’s stock price as of 12/30/2022 of 16.70%, and an annual forward yield to the company’s estimated CURRENT BV of 16.45%. When comparing each yield percentage to NLY’s agency mREIT peers within this analysis, the company’s TTM dividend yield percentage remained modestly below average, the company’s annual forward yield percentage based on its stock price remained near average, and its annual forward yield percentage based on its estimated CURRENT BV remained slightly above average. Going forward, I continue to believe NLY should have an annual forward yield slightly-modestly above the agency mREIT average.

A Couple Comparisons Between NLY and the Company’s 19 mREIT Peers in Ranking Order:

The REIT Forum Feature

I believe this metric only solidifies more caution/risk regarding ORC, CHMI, IVR, and ARR.

That said, it should be noted 1 agency, all 7 hybrid, all 3 originator + servicer, and both commercial whole loan sub-sector peers still have very low-relatively low forward yields (below 12.50%). However, as is always the case, this is something I/we will continuously monitor as 2023 unfolds.

I would point out ORC accounts for the company’s premium amortization expense equivalent differently when compared to its agency mREIT sub-sector peers. First, this leads to timing differences which can “prop up” weighted average yields during certain interest rate cycles. As such, ORC’s yield percentages continue to be above the agency mREIT sub-sector average. Second, this can “appear to buoy” ORC net spread metrics when, in reality, a reclassification of the company’s equivalent to premium amortization expense would show a much more modest net spread income metric. This is also typically why a larger than average agency mREIT percentage of ORC’s dividend declarations over the past several years have been classified as a “return on capital” (“ROC”) distribution. Simply put, ORC continues to distribute dividends in excess of the company’s annual REIT taxable income (“AREITTI”). However, the recent (51%) dividend reduction has notably lowered this overdistribution. Further discussion of this ORC topic is beyond a NLY sector comparison article (also has been extensively covered in prior ORC mREIT articles over the years).

Conclusions Drawn (PART 2):

PART 2 of this article compared NLY to 19 mREIT peers in regards to recent dividend per share rates, yield percentages, and several other dividend sustainability metrics. This article also discussed NLY’s past dividend decrease during the second quarter of 2020. Using Table 9 as a reference, the following were the recent dividend per share rate and yield percentages for NLY:

NLY: $0.88 per common share dividend for the fourth quarter of 2022; 16.70% TTM dividend yield; 16.70% annual forward yield to the company’s stock price as of 12/30/2022; and 16.45% annual forward yield to my projected CURRENT BV.

When combining this data along with metrics within Table 10 (most notably NCE/EAD) and other modeling sources, the following probability regarding NLY’s near-term dividend sustainability is provided:

NLY: High (80%) probability of a stable dividend for Q1 2023

NLY: Relatively High (70%) probability of stable dividend for Q2 2023

Q4 2022 Projected NCE/EAD: $0.900-$1.000 per common share

Preliminary Q1 2023 Projected NCE/EAD: $0.855-$0.955 per common share

Preliminary Q2 2023 Projected NCE/EAD: $0.825-$0.925 per common share

I believe the movement of MBS prices will directly impact NLY’s use of the TBA forward market (which directly impacts NDR income). As explained in PART 1 of this article, NLY’s portfolio composition, leverage, borrowing costs, hedging coverage ratio (risk management strategy), and prepayment speeds also need to be considered when discussing this topic.

While I believe NLY’s NCE/EAD will net decrease over the foreseeable future as short-term funding costs quickly rise during the first half of 2023, I also believe the company continues to have a modest “cushion” to support the current dividend per share rate. I would also point out NLY will continue to rotate into higher coupons fixed-rate agency MBS (and other mortgage-related investments) which will result in a gradual increase in weighted average coupon (“WAC”), will continue to experience an increase in net yields due to both a decrease in purchased fixed-rate agency MBS pricing (including more favorable pricing of other mortgaged-related investments) and lower than average constant/conditional prepayment rates (“CPRs”), and will continue to realize more favorable current period hedging income (expense) regarding its existing interest rate payer swaps and exercised swaptions (though this specific benefit will eventually fade some during 2023).

20 mREIT Dividend Projections for Q1 2023:

The REIT Forum Feature

My BUY, SELL, or HOLD Recommendation:

From the analysis provided above, including additional catalysts/factors not discussed within this article, I currently rate NLY as a SELL when I believe the company’s stock price is trading at or greater than a 2% premium to my projected CURRENT BV (BV as of 12/31/2022; $20.70 per share), a HOLD when trading at less than a 2% premium through less than a (8%) discount to my projected CURRENT BV, and a BUY when trading at or greater than a (8%) discount to my projected CURRENT BV.

Therefore, with a closing stock price of $21.69 per common share as of 1/4/2023, I currently rate NLY as SLIGHTLY OVERVALUED from a stock price perspective.

As such, I currently believe NLY is a SELL recommendation. My current price target for NLY is approximately $21.10 per common share. This is currently the price where my recommendation would change to APPROPRIATELY VALUED/a HOLD recommendation. The current price where my classification/recommendation would change to UNDERVALUED/a BUY recommendation is approximately $19.05 per common share. Put another way, the following are my CURRENT BUY, SELL, or HOLD per share recommendation ranges (the REIT Forum subscribers get this type of data on all 20 mREIT stocks I currently cover on a weekly basis):

$21.10 per share or above = SELL

$19.06 - $21.09 per share = HOLD

$16.96 - $19.05 per share = BUY

$16.95 per share or below = STRONG BUY

Along with the data presented within this article, this recommendation considers the following mREIT catalysts/factors: 1) projected future MBS/investment price movements ; 2) projected future derivative valuations ; and 3) projected near-term (up to 1-year) dividend per share rates. As discussed earlier, this includes all recent, current, and projected macroeconomic indicators and FOMC monetary policy.

Current Sector/Recent NLY/AGNC Stock Disclosures:

On 3/18/2020, I initiated a position in NLY at a weighted average purchase price of $5.05 per share (large purchase). This weighted average per share price excluded all dividends received/reinvested. On 6/9/2021, I sold my entire NLY position at a weighted average sales price of $9.574 per share as my price target, at the time, of $9.55 per share was surpassed. This calculates to a weighted average realized gain and total return of 89.6% and 112.0%, respectively. I held this position for approximately 15 months.

On 3/18/2020, I once again initiated a position in AGNC at a weighted average purchase price of $7.115 per share (large purchase). This weighted average per share price excluded all dividends received/reinvested. On 6/2/2021, I sold my entire AGNC position at a weighted average sales price of $18.692 per share as my price target, at the time, of $18.65 per share was surpassed. This calculates to a weighted average realized gain and total return of 162.7% and 188.6%, respectively. I held this position for approximately 14.5 months.

On 10/11/2022, I once again initiated a position in AGNC at a weighted average purchase price of $7.445 per share. On 10/24/2022, I increased my position in AGNC at a weighted average purchase price of $7.500 per share. When combined, my AGNC position had a weighted average purchase price of $7.473 per share. This weighted average per share price excluded all dividends received/reinvested. On 11/9/2022, I sold my entire AGNC position at a weighted average sales price of $8.750 per share as my price target, at the time, of $8.75 per share was surpassed. This calculates to a weighted average realized gain and total return of 17.1% and 18.7%, respectively. I held this position for approximately 3 weeks.

On 1/31/2017, I initiated a position in RITM (at the time was NRZ) at a weighted average purchase price of $15.10 per share. On 6/29/2017, 7/7/2017, and 12/21/2018, I increased my position in RITM at a weighted average purchase price of $15.775, $15.18, and $14.475 per share, respectively. When combined, my RITM position had a weighted average purchase price of $14.912 per share. This weighted average per share price excluded all dividends received/reinvested. On 2/6/2020, I sold my entire RITM position at a weighted average sales price of $17.555 per share as my price target, at the time, of $17.50 per share was surpassed. This calculates to a weighted average realized gain and total return of 17.7% and 41.2%, respectively. I held this position, on a weighted average basis, for approximately 20 months.

On 9/22/2020, I once again initiated a position in RITM at a weighted average purchase price of $7.645 per share. On 1/28/2021, 7/16/2021, 8/20/2021, 4/7/2022, 6/13/2022, 6/14/2022, 6/17/2022, 9/23/2022, and 9/26/2022, I increased my position in RITM at a weighted average purchase price of $9.415, $9.525, $9.485, $10.11, $9.345, $9.055, $8.421, $8.010, and $7.558 per share, respectively. When combined, my RITM position has a weighted average purchase price of $8.383 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, RITM is 66.8% of my mREIT sector common stock allocation.

On 1/2/2020, I initiated a position in AAIC at a weighted average purchase price of $5.57 per share. On 1/9/2020, 3/16/2020, 9/24/2020, 5/6/2021, 9/2/2021, 9/10/2021, 11/10/2021, 11/24/2021, 3/3/2022, 8/8/2022, and 11/8/2022, I increased my position in AI at a weighted average purchase price of $5.59, $3.25, $2.53, $3.875, $3.748, $3.75, $3.752, $3.70, $3.39, $3.16, and $3.005 per share, respectively. When combined, my AAIC position has a weighted average purchase price of $3.339 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, AAIC is 7.5% of my mREIT sector common stock allocation.

On 10/19/2020, I initiated a position in PMT at a weighted average purchase price of $16.275 per share. On 10/29/2020, 8/12/2021, 8/20/2021, 11/18/2021, 2/4/2022, 4/19/2022, and 9/9/2022, I increased my position in PMT at a weighted average purchase price of $14.90, $18.693, $18.407, $18.180, $16.024, $14.721, and $14.04 per common share, respectively. When combined, my PMT position has a weighted average purchase price of $15.492 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, PMT is 12.8% of my mREIT sector common stock allocation.

On 12/1/2020, I initiated a position in DX at a weighted average purchase price of $16.59 per share. On 12/20/2021, I increased my position in DX at a weighted average purchase price of $15.35 per share. When combined, my DX position has a weighted average purchase price of $15.66 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, DX is 2.5% of my mREIT sector common stock allocation.

On 10/12/2018, I initiated a position in GPMT at a weighted average purchase price of $18.155 per share. On 5/12/2020, 5/27/2020, 5/28/2020, 8/26/2020, 9/10/2020, and 9/11/2020, I increased my position in GPMT at a weighted average purchase price of $4.745, $5.144, $5.086, $6.70, $6.19, and $6.045 per share, respectively. My last two purchases made up approximately 50% of my total position (to put things in better perspective). When combined, my GPMT position had a weighted average purchase price of $6.234 per share. This weighted average per share price excluded all dividends received/reinvested. On 6/8/2021, I sold my entire GPMT position at a weighted average sales price of $15.783 per share as my price target, at the time, of $15.75 per share was surpassed. This calculates to a weighted average realized gain and total return of 153.2% and 168.7%, respectively. I held this position, on a weighted average basis, for approximately 11 months.

On 12/10/2021, I once again initiated a position in GPMT at a weighted average purchase price of $11.817 per share. On 12/15/2021, 4/19/2022, 4/29/2022, 9/23/2022, and 12/21/2022, I increased my position in GPMT at a weighted average purchase price of $11.318, $9.998, $9.69, $8.08, and $5.724 per share, respectively. When combined, my GPMT position has a weighted average purchase price of $7.251 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, GPMT is 7.1% of my mREIT sector common stock allocation.

On 1/24/2022, I initiated a position in RC at a weighted average purchase price of $13.39 per share. On 6/29/2022, I increased my position in RC at a weighted average purchase price of $11.69 per share. When combined, my RC position has a weighted average purchase price of $12.257 per share. This weighted average per share price excludes all dividends received/reinvested. Currently, RC is 3.3% of my mREIT sector common stock allocation.

Final Note: All trades/investments I have performed over the past several years have been disclosed to readers in “real time” (that day at the latest) via either the StockTalks feature of Seeking Alpha or, more recently, the “live chat” feature of the Marketplace Service the REIT Forum (which cannot be changed/altered). Through these resources, readers can look up all my prior disclosures (buys/sells) regarding all companies I cover here at Seeking Alpha (see my profile page for a list of all stocks covered). Through StockTalk disclosures and/or the live chat feature of the REIT Forum, at the end of November 2022 I had an unrealized/realized gain “success rate” of 84.4% and a total return (includes dividends received) success rate of 89.1% out of 64 total past and present mREIT and business development company ( “BDC”) positions (updated monthly; multiple purchases/sales in one stock count as one overall position until fully closed out). I encourage other Seeking Alpha contributors to provide real time buy and sell updates for their readers/subscribers which would ultimately lead to greater transparency/credibility. Starting in January 2020, I have transitioned all my real-time purchase and sale disclosures solely to members of the REIT Forum. All applicable public articles will still have my purchase and sale disclosures (just not real-time alerts).

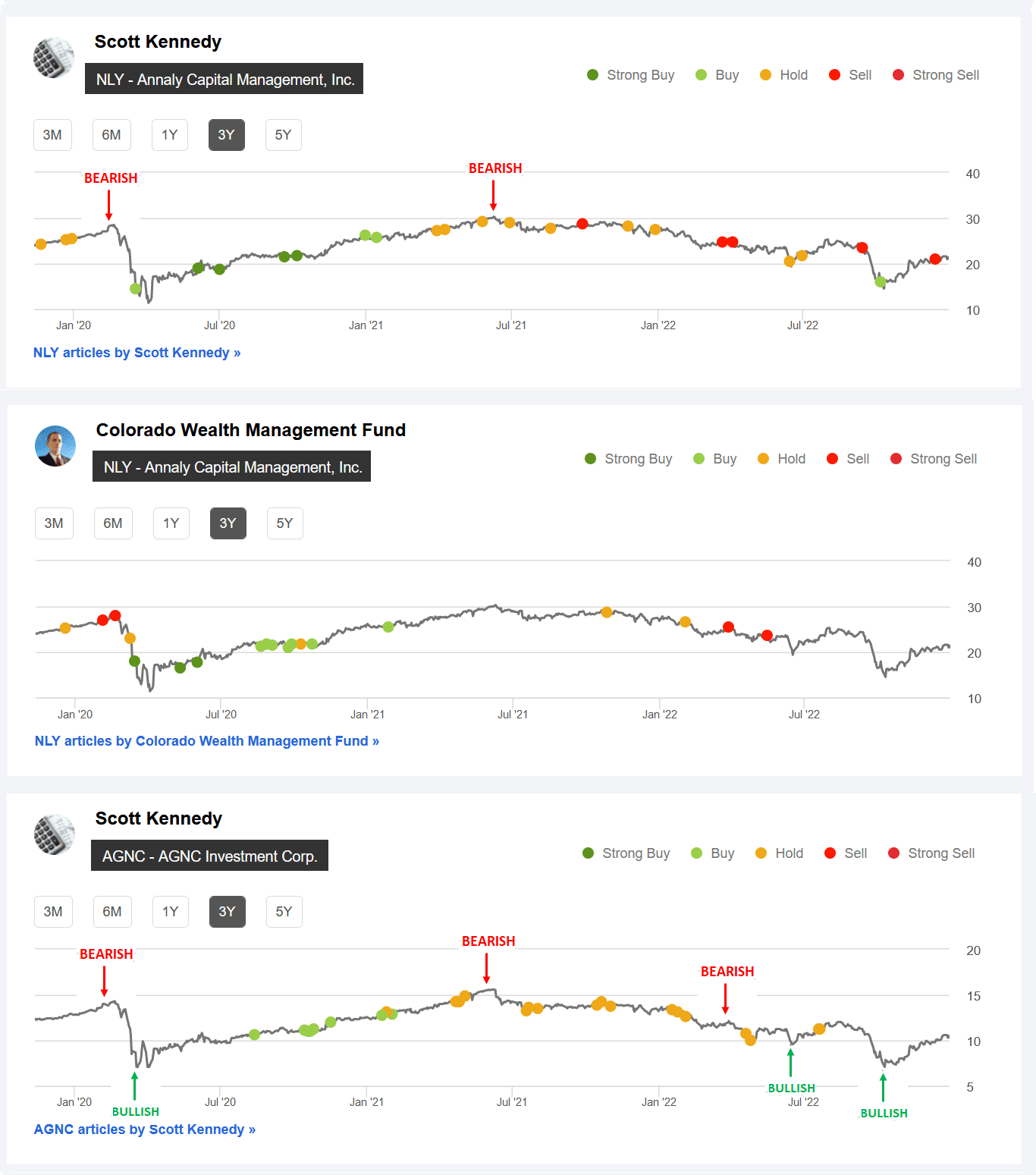

Table 14 – The REIT Forum NLY + AGNC Seeking Alpha Recommendations ( December 2019 – December 2022 Timeframe)

{kind=link}

Seeking Alpha

(Source: Table directly from Seeking Alpha; 1 st AGNC “Bearish” indicator included by me directly from the public AGNC article dated 2/5/2020 recommendation [which can’t be changed once public], AGNC “Bullish” indicator included by me directly from the public AGNC article dated 4/17/2020 recommendation [which can’t be changed once public], 2 nd AGNC and 1 st NLY “Bearish” indicator included by me directly from the REIT Forum’s weekly subscriber recommendation article series [ week of 6/4/2021 for AGNC and week of 6/11/2021 for NLY], 3 rd AGNC “Bearish” indicator included by me directly from the REIT Forum’s weekly subscriber recommendation article series [ week of 4/8/2022 ], 2 nd AGNC “Bullish” indicator included by me directly from the REIT Forum’s weekly subscriber recommendation article series [ week of 6/17/2022 ], and 3 rd AGNC “Bullish” indicator included by me directly from the REIT Forum’s weekly subscriber recommendation article series [ week of 9/30/2022 ].)

I just want to quickly highlight my/our AGNC and NLY Seeking Alpha recommendation ranges over the past several years. In my personal opinion, a stock with a BUY recommendation should increase in price over time, a SELL recommendation should decrease in price over time, and a HOLD recommendation should remain relatively unchanged in price over time (pretty logical). Simply put, my/our “valuation methodology” has correctly timed when both AGNC and NLY have been undervalued (a BUY recommendation; bullish), overvalued (a SELL recommendation; bearish), and appropriately valued (a HOLD recommendation; neutral).

Using Table 14 above as a reference, I believe we have done a pretty good job in my/our AGNC and NLY recommendation ratings. For NLY, both pricing charts should really be viewed as 1 combined chart since CO and I are part of the same Marketplace service team. Not only do I/we want to provide guidance/a recommendation that enhances total returns for subscribers, I/we also want to protect these generated returns by subsequently minimizing total losses. I personally believe this methodology/strategy is very important. In other words, correctly spotting both positive catalysts/trends and negative factors/trends as economic and interest rate cycles fluctuate.

This methodology/strategy was extremely useful/accurate when going back to very late 2019 and early 2020 (both pre-COVID-19) where I/we had a SELL recommendation on both AGNC and NLY. For some reason, this S.A. pricing chart does not show my AGNC SELL recommendation pre-COVID-19 but one can simply look back to past public articles in early 2020 (just an omission on S.A.’s end in this particular case). As an alternative, simply look at the NLY SELL recommendation highlighted in CO’s pricing chart (AGNC and NLY typically have very similar recommendation ranges when considering similar time periods). Furthermore, after the initial “pandemic panic” , I/we had a STRONG BUY recommendation on both AGNC and NLY later in the spring of 2020.

Simply put, a contributor’s/team’s recommendation track record should “count for something” and should always be considered when it comes to credibility/successful investing. You will not see most (if not all) other contributor teams use this type of factual, recommendation-driven price chart because the results are not nearly as “attractive” when compared to our own.

Understanding My/Our Valuation Methodology Regarding mREIT Common and BDC Stocks:

The basic "premise" around my/our recommendations in the mREIT common and BDC sectors is value. Regarding operational performance over the long-term, there are above average, average, and below average mREIT and BDC stocks. That said, better-performing mREIT and BDC peers can be expensive to own, as well as being cheap. Just because a well-performing stock outperforms the company’s sector peers over the long-term, this does not mean this stock should be owned at any price. As with any stock, there is a price range where the valuation is cheap, a price where the valuation is expensive, and a price where the valuation is appropriate. The same holds true with all mREIT common and BDC peers. As such, regarding my/our investing methodology, each mREIT common and BDC peer has their own unique BUY, SELL, or HOLD recommendation range (relative to estimated CURRENT BV/NAV). The better-performing mREITs and BDCs typically have a recommendation range at a premium to BV/NAV (varying percentages based on overall outperformance) and vice versa with the average/underperforming mREITs and BDCs (typically at a discount to estimated CURRENT BV/NAV).

Each company’s recommendation range is "pegged" to estimated CURRENT BV/NAV because this way subscribers/readers can track when each mREIT and BDC peer moves within the assigned recommendation ranges (daily if desired). That said, the underlying reasoning why I/we place each mREIT and BDC recommendation range at a different premium or (discount) to estimated CURRENT BV/NAV is based on roughly 15-20 catalysts which include both macroeconomic catalysts/factors and company-specific catalysts/factors (both positive and negative). This investing strategy is not for all market participants. For instance, not likely a “good fit” for extremely passive investors. For example, investors holding a position in a particular stock, no matter the price, for say a period of 5+ years. However, as shown throughout my articles written here at Seeking Alpha since 2013, in the vast majority of instances I have been able to enhance my personal total returns and/or minimize my personal total losses from specifically implementing this particular investing valuation methodology. I hope this provides some added clarity/understanding for new subscribers/readers regarding my valuation methodology utilized in the mREIT common and BDC sectors.

Each investor's BUY, SELL, or HOLD decision is based on one's risk tolerance, time horizon, and dividend income goals. My personal recommendation will not fit each reader’s current investing strategy. The factual information provided within this article is intended to help assist readers when it comes to investing strategies/decisions. Please disregard any minor “cosmetic” typos if/when applicable.

For further details see:

Annaly Capital's BV, Sector Valuation, And Dividend Sustainability Vs. 19 mREIT Peers - Part 2 (Includes Q1 2023 + Q2 2023 Dividend Projection)