TTE - APA Corporation: Playing The Block-58 Waiting Game

2023-09-20 08:00:00 ET

Summary

- APA Corporation stock has experienced oscillations due to delays in achieving FID in Suriname, Block-58 and low gas prices.

- Recent bearish trading was caused by a drop in crude prices and an increase in inventories.

- APA Corp has a well-distributed global footprint and strong production in the U.S., UK, and Egypt.

- We think the FID for Block-58 is a near certainty and discuss why it is taking extra time.

- We rate APA Corporation a buy at current levels, subject to individual investor's risk tolerance.

Introduction

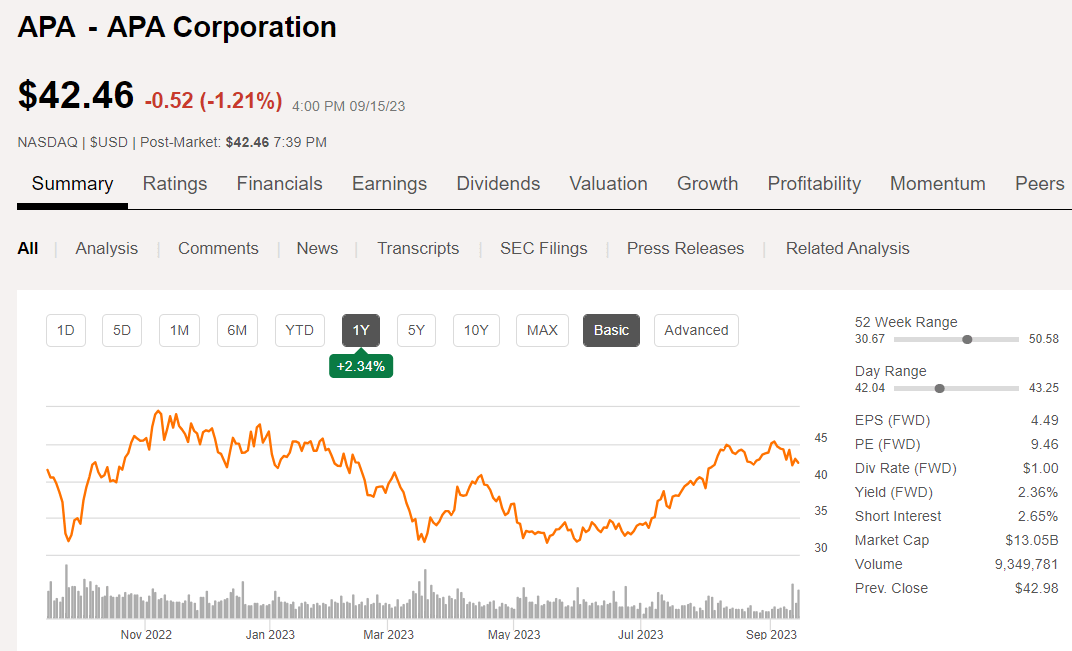

Shares of APA Corporation ( APA ) have rallied since our last article in January of 2022, where I called a buy at $30.00. This was on the strength of the 4th successful well test in Block-58, offshore Suriname, and the expectation of an FID in late 2022. This call has aged fairly well although the stock has oscillated several times in a range for a number of reasons.

{kind=link}

A problem with geological interpretation has led to a multi-year delay in achieving FID, and helped to put a drag on the stock. Low gas prices have also contributed to the stock being range bound in the mid-$30's to low $40's, as the company's other signature asset, Alpine High is a dry gas producer primarily.

Recently trading in the stock has been bearish, with a massive 12 mm share down day on Wednesday the 13th. This was thanks to a ~$2.00 drop in the crude price on news of the ~4 mm bbl build in inventories as reported by the EIA .

Let's take a quick look at the near term fundamentals for APA and see if we are at a decent entry point for future growth. We will also discuss the impact of the newly released agreement to do a Pre-FID study on the project's feasibility.

APA Corp snapshot and thesis for owning

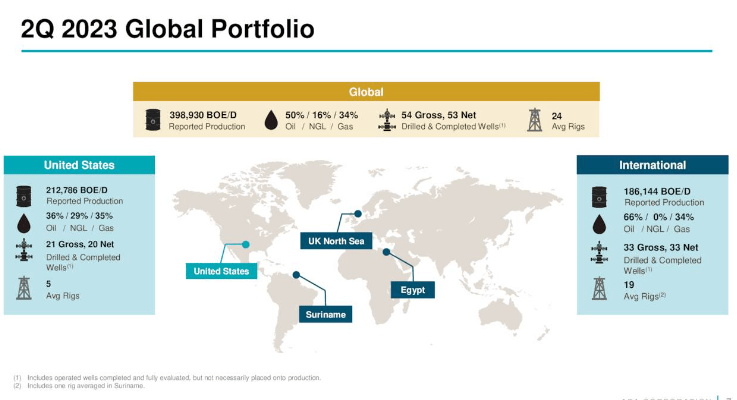

APA has a well distributed footprint globally with operations in the U.S., UK, Eygpt, and Suriname. At present the U.S. provides the bulk of its revenue through the Alpine High gas asset in the Permian basin and an oil-weighted buy last year in the Delaware to temper low gas prices, followed closely by Egypt. Lastly comes the UK, where it has suspended investment in new drilling, presumably due to the UK Windfall Profits Tax regime.

{kind=link}

U.S. Production is at 212,796 BOEPD, with 36% oil, 29% NGL's, and 30% gas. Activity was strong in the Midland basin with 10 new oil wells TIL'd, and in the Delaware with 11 new wells TIL'd in Q-2. Alpine High activity is suspended due to low gas and gas liquids prices.

Egypt produced 144K BOEPD of 61% oil, no NGL's and 39% gas. Production is forecast to grow to 148K BOEPD in Q-3.

In the U.K APA produced 42,118K BOEPD of 83% oil, 2% NGL's, and 15% gas. Q-3 is expected to increase output to 47K BOEPD thanks to a restoration of curtailment, and new well contribution from Storr North. APA has a number of exploration prospects advantaged by the massive amount of infrastructure in the North Sea, but do not compete for capital under the present oppressive tax regime.

That brings us to Suriname, and rates its own section.

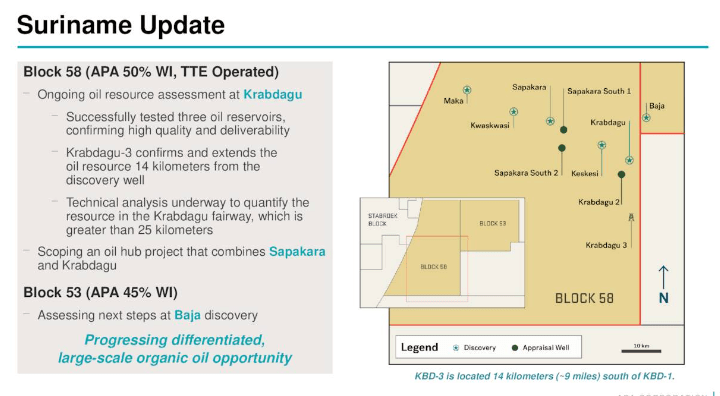

Suriname, Block-58

Apache and partner, TotalEnergies ( TTE ) have had a string of successes since forming the JV in late 2019. With the success of the test on Krabdagu#3, a petroleum system has been established that runs from Maka#1 to K-3, as the second bullet notes. With the recent discovery in Block-53, additional reserves may be lumped in, further complicating the decision not to go forward - I think we are there, but rather...how to go forward. That's the key, and I will next discuss why (I think) this is taking so long. Matt Andre, Platts Analytics manager for energy analysis–production, was quoted in a SP Global article as saying-

"A discovery in Block 53 just adds to the optimism" for the country's offshore acreage, Andre said. "And since the company's Dikkop exploration well in Block 58 has been plugged and abandoned, now [APA has] more options with the discovery in Block 53."

{kind=link}

The company's language is instructive if you know what to read in between the lines. "Technical Analysis," mentioned in the first bullet suggests to me that before taking the final FID, the JV wants to understand the reservoir better, as the key for development is a low production cost. Patrick Pouyane, CEO of TTE commented in a Reuters article , in regard to Block 58-

TotalEnergies expects the project could be developed at a production cost of less than $20 barrel, Pouyane said.

Efficiently draining the reservoir is key to hitting Mr. Pouyane's target. The way I see it, the Production Technologists are determining-

- Building an accurate 3-D view of the reservoirs. This, among other things reveals the tilt of the plane of the reservoir with respect to the surface, and is referred to in technical jargon as the "dip." You want to be careful not siphon off the gas cap prematurely . Even though they will be reinjecting gas for pressure maintenance, you want to leave the natural gas cap in place to ensure maximum ultimate recovery.

- areas of maximum permeability and connectivity. This will help determine the location of the subsea wells, casing exits into the reservoir, and the mudline piping to production hubs for the FPSO.

- Rock properties. This is critical for completion style. The big question will be will they have to gravel pack, or will a standalone screen suffice?

- The topography of the seabed. Are they crossing any canyons? Or obstacles that may impede or delay completion.

- Reservoir pressures, oil analysis, connate water analysis, gas analysis, and many other things too numerous to list here will play a role in the final determination that these reservoirs can be produced profitably.

So you can see there is a lot to do to cross all the t's and dot the i's to total up the costs. Now Total has some experience at doing these projects, and I would expect them to know within a couple of hundred million what the final cost will be. But, it is estimated at $9 bn, and if it's actually going to be $15 bn, this would be a great time to find out.

As practical matter, unless something really unusual - war, fear, famine, pestilence,.... the Four Horsemen of the Apocalypse - show up.... this is a "done" deal. You don't have company presidents flying around the world to meet with heads of state and the petroleum ministry of a country to just eat rubber chicken. Unless you are pretty darned sure you've set the slips, these meetings don't take place.

Q2 2023 and Guidance

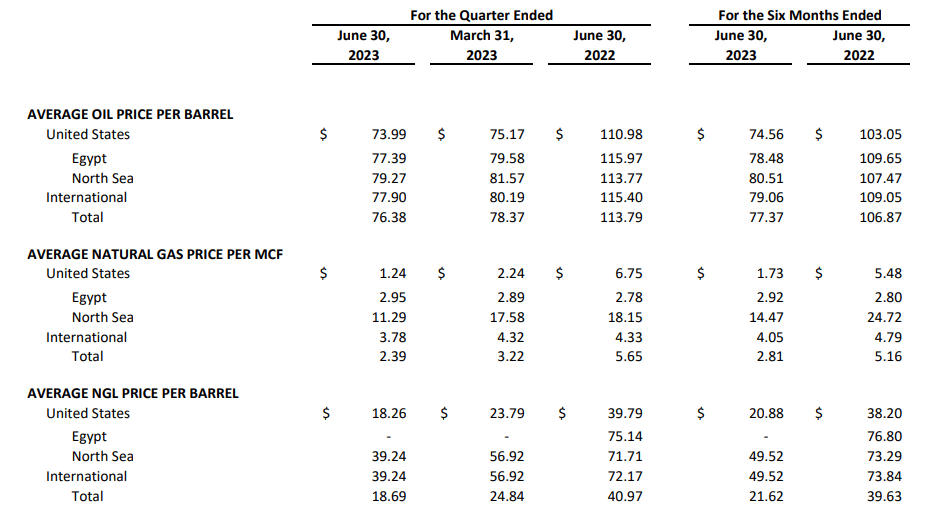

On revenue of $1.79 bn for the quarter, APA generated 1.24 bn in EBITDA, $1.0 bn in OCF- up ~3X sequentially and down 30% YoY, and $381 mm in Net Income. A sequential drop of 10%, and a YoY of 30% respectively for revenue and EBITDA. Net Income rose sequentially due to some asset sales to $381 mm from $242 mm, but declined YoY from $926 mm, most thanks to lower realizations on produced products.

{kind=link}

Capex on a run rate basis in running $2.3 bn for the year, but management has reduced capex through the end of the year, with expectations for it coming in at $1.9 bn. Curtailments in Alpine High and no further drilling this year in Suriname account for this reduction.

Capital returns to shareholders have totaled $2.9 bn since 2021, and debt now standing at $5.3 bn has been cut by $3.2 bn over the same period.

Moody's returned APA debt to investment grade in June.

Guidance

Production guidance is for daily output between 404-408 BOEPD as we exit 2023. On an unadjusted basis this represent about a 10% growth YoY. On an adjusted basis expectations are for ~325k BOEPD, an 8% bump higher from the 304 reported in 2022.

Risks

Several risks are apparent for APA Corp. The first are oil prices, as noted in the cash flow commentary, current pricing around $90-95 for WTI and Brent will take cash flow back toward $3.5-4.0 bn on a run rate basis. If we sag back there are risks to shareholder returns and the stock price ultimately.

It's worth noting the company had to dip into cash reserves to pay out dividends and stock buybacks for the quarter, as cash flow fell short by $29 mm. I think the company made a good decision to fund the share buyback at $38, as I think the company is under priced at those levels.

Any change in OPEC+'s posture with production restraint or by our own government with respect toward additional SPR releases would have an adverse effect on share prices.

Finally if they don't take FID on Suriname for whatever reason, the shares will struggle to improve from current levels.

Your takeaway

APA Corp is trading at 3.2X EV/EBITDA at present prices, and $55K per flowing barrel. Neither one of those metrics are excessive in my book, and I would rate the company as a buy for short term gains and modest income.

Longer term, as I have taken pains to point out, I think shares of APA are a steal at current prices. You will have to look long and hard to find a company with the revenue and cash flow potential that a successful FID on Block-58 gives to APA.

Similarly priced competitor, Murphy Oil ( MUR ) trades at 3.4X EV/EBITDA and $46K per flowing barrel, so slightly better, but doesn't have that potential cash cow of Block-58, Suriname hanging in the window a few years hence. I think APA wins the tip off on that basis.

For further details see:

APA Corporation: Playing The Block-58 Waiting Game