VNAM - APAC Economic Outlook For 2024 Remains Bright

2024-01-06 12:15:00 ET

Summary

- After rapid expansion in 2023, the Asia-Pacific (APAC) region is expected to be the fastest growing region of the world economy in 2024.

- Some improvement in East Asian exports will also support economic expansion.

- The APAC tourism industry is expected to continue to recover during 2024, as international tourism flows normalize to pre-pandemic levels in many countries.

APAC GDP growth expected to remain strong

Economic growth in the APAC region strengthened in 2023, reaching an estimated pace of 4.5% year-over-year (y/y), significantly higher compared with GDP growth of 3.3% in 2022. An important factor supporting the upturn in growth momentum during 2023 was improving growth in mainland China following the winding down of COVID-19 restrictions since late 2022. An upturn in growth in Japan and continued rapid economic expansion in India also helped to underpin the APAC region's robust economic growth in 2023.

{kind=link}

The APAC economic outlook for 2024 is for continued rapid economic expansion, helped by resilient domestic demand in a number of large Asian emerging markets, including mainland China, India, Indonesia, Malaysia and Philippines. Strong foreign direct investment inflows are expected to continue into India and some ASEAN nations, as multinationals continue to diversify their manufacturing supply chains.

Some upturn in merchandise exports is expected during 2024, after a significant downturn in exports of goods in many Asian industrial nations during 2023, notably due to declining exports of electronics products.

Economic recovery continuing in mainland China

Economic recovery is expected to continue in mainland China for a second year, albeit the pace of economic expansion is expected to be moderate somewhat. Private consumption is expected to be a key driver of economic growth in 2024. The pace of growth of retail sales of consumer goods showed significant improvement during the second half of 2023, with retail sales in November rising by 10.1% y/y, compared with a growth rate of only 2.5% y/y in July. For the first 11 months of 2023, retail sales of consumer goods rose by 7.2% y/y.

The headline seasonally adjusted Caixin General Manufacturing Purchasing Managers' Index ('PMI') increased from 50.7 in November to 50.8 in December, to signal a marginal positive expansion in manufacturing conditions. Supporting the positive survey reading for November was a quicker rise in overall new orders received by Chinese goods producers in December, reflecting strong demand for consumer goods. However, new export orders continued to fall slightly, marking the sixth consecutive month of contraction in export orders, although the rate of decline moderated.

{kind=link}

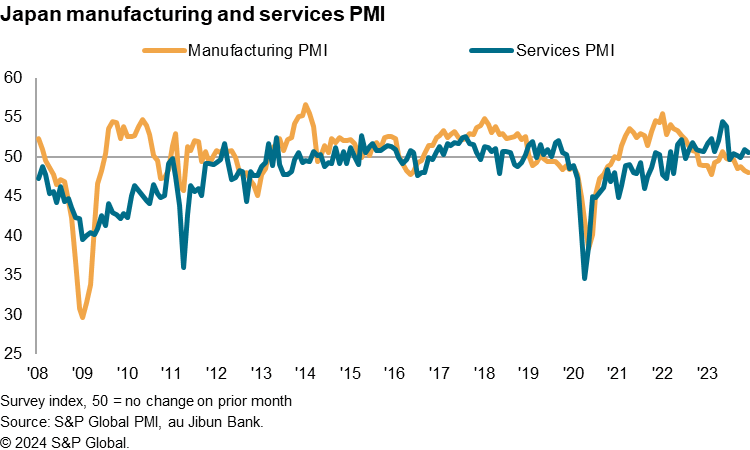

Japan's economy boosted by service sector

Japan's GDP growth strengthened in 2023, helped by improving private consumption after COVID-19 pandemic restrictions were gradually removed.

The au Jibun Bank Flash Japan Services Business Activity Index picked up from 50.8 in November to 52.0 in December, to signal continuing expansionary conditions at a pace that was the quickest since September. In contrast, business conditions in the manufacturing sector continued to show moderate contraction according to the headline au Jibun Bank Japan PMI, which edged lower to 47.9 in December from 48.3 in November. Manufacturing companies reported a sharp decline in new orders, which in turn led to a slightly quicker reduction in factory output.

{kind=link}

South Korean exports rebound

South Korea's Ministry of Trade, Industry and Energy (MOTIE) announced that South Korea's exports for the month of December grew by 5.1% y/y in value terms, following a rise of 7.8% y/y in November. This marks a sharp turnaround after significant contractions recorded for exports earlier during 2023.

A key factor supporting the rebound has been an upturn in semiconductors exports, which ended 15 successive months of contraction in November, posting growth of 12.9% y/y, helped by a recovery in prices for memory chips. Semiconductors exports posted even stronger growth in December, growing by 21.8% y/y. Exports of displays rose by 10.9% y/y in December, reflecting strong demand for smartphone panels. South Korean exports were also boosted by strong growth of 17.9% y/y in the export value of autos, helped by buoyant growth in exports of electric vehicles.

Reflecting the upturn in South Korean manufacturing exports, the seasonally adjusted S&P Global South Korea Manufacturing PMI was at 49.9 in December, similar to the figure of 50.0 in November, continuing to signal close to neutral operating conditions in South Korea's manufacturing sector. The November reading ended a 16-month sequence of decline.

Taiwan's exports continue to recover

Taiwan's exports grew by 3.8% y/y in November, after having shown sharp declines throughout the first half of 2023 before gradually improving during the second half.

An important driver for the improvement was a 74% y/y rise in exports of information, communication and audio-video products. Key growth markets were the US, with exports to the US rising by 33% y/y in November, while exports to ASEAN rose by 13.8% y/y. However, exports to mainland China and Hong Kong SAR fell by 6.3% y/y. For the first eleven months of 2023, exports to mainland China and Hong Kong SAR fell by 19.1% y/y.

Despite the upturn in exports, the S&P Global Taiwan Manufacturing PMI declined in December to a reading of 47.1 from 48.3 in November. The index still signalled moderate contractionary business conditions for the nineteenth successive month, although the pace of reduction has moderated since March 2023.

ASEAN outlook

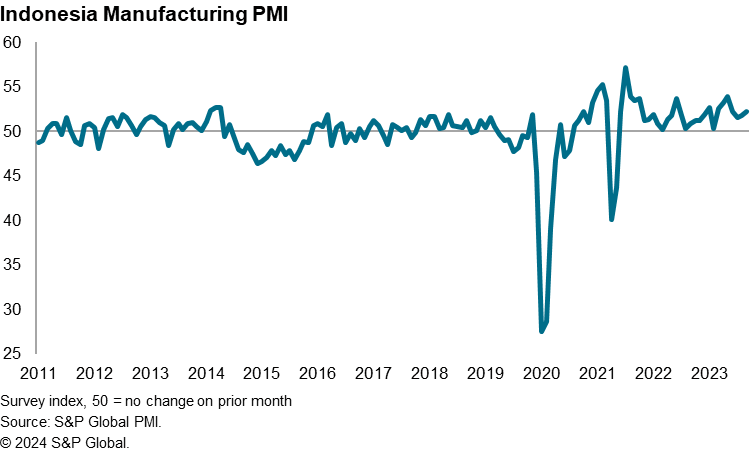

Indonesia's GDP growth rate in 2023 is estimated at around 5%, with a similar pace of economic growth forecast for 2024. Private consumption is a key driver of economic growth, accounting for around 53% of total GDP and growing at a pace of 5.1% y/y in the third quarter of 2023. The outlook for 2024 is for continued robust growth in private consumption and fixed investment. During 2023, foreign direct investment inflows remained strong, buoyed by large investment inflows into the base metals sector, notably new nickel smelter projects, as well as into downstream projects for manufacturing of electric vehicle batteries for which nickel is an important input.

The headline seasonally adjusted S&P Global Indonesia Manufacturing PMI rose to 52.2 in December, up from 51.7 in November, to signal that manufacturing sector conditions continued to improve and at the fastest rate since September. This extended the current period of manufacturing sector expansion to 28 months.

{kind=link}

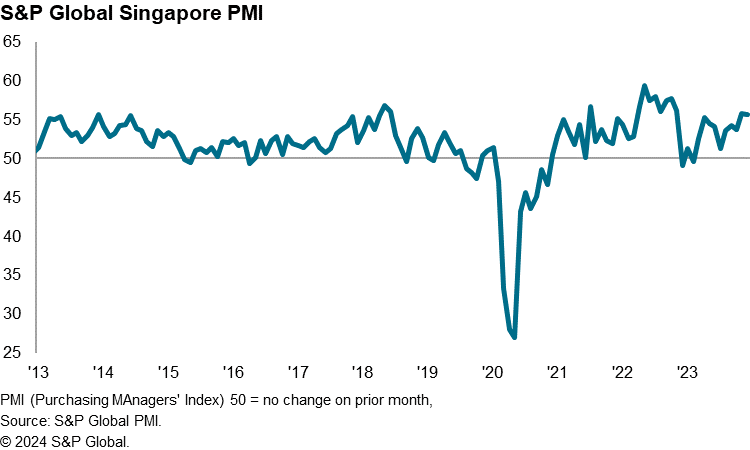

Singapore's GDP growth rate improved to a pace of 2.8% y/y in the fourth quarter of 2023 according to the advance estimate of GDP from the Ministry of Trade and Industry (MTI). This compared with GDP growth of 1.0% y/y in the third quarter of 2023. For calendar 2023, GDP growth was 1.2%, significantly slower than the growth rate of 3.6% recorded in 2022, when the economy rebounded strongly after the COVID-19 pandemic.

{kind=link}

The headline seasonally adjusted S&P Global Singapore PMI posted 55.7 in December, edging lower from 55.8 in November. The latest reading signalled a tenth consecutive monthly expansion of Singapore's private sector economy and signalled continued strong business conditions. Incoming new business continued to rise at the end of 2023, growing at the fastest pace in seven months on the back of better underlying demand conditions.

{kind=link}

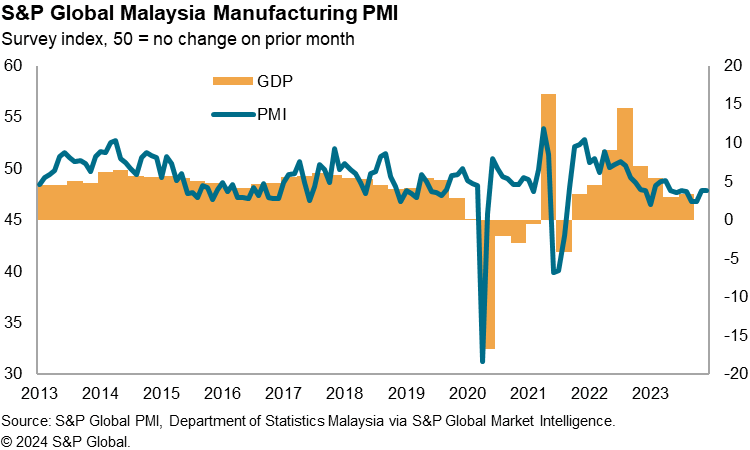

Malaysia's economy showed resilient economic expansion in 2023 at an estimated rate of around 4%, albeit the pace of growth moderated after the buoyant 8.7% GDP growth rate recorded in 2022.

Malaysian GDP growth improved to a pace of 3.3% y/y in the third quarter of 2023, compared with growth of 2.9% y/y in the second quarter of 2023. When measured on a quarter-on-quarter (q/q) basis, the pace of growth strengthened to 2.6% q/q, compared with 1.5% q/q in the second quarter of 2023 and just 0.9% q/q in the first quarter of 2023.

The seasonally adjusted S&P Global Malaysia Manufacturing PMI was unchanged at 47.9 in December, indicating that business conditions remained challenging for manufacturing firms. Demand conditions in international markets remained contractionary, with new export orders falling for the eighth month in a row, but at the softest rate since May.

{kind=link}

Philippines economic growth remained strong in 2023, with GDP growth improving to a pace of 5.9% y/y in the third quarter of 2023, compared with GDP growth of 4.3% y/y in the second quarter of 2023. The outlook for 2024 is for continued rapid economic growth, helped by expected gradual easing of monetary policy during the course of 2024.

The headline S&P Global Philippines Manufacturing PMI was at 51.5 in December 2023, continuing to indicate expansionary conditions in the manufacturing sector, albeit moderating from November's nine-month high of 52.7.

Indian economy shows buoyant expansion

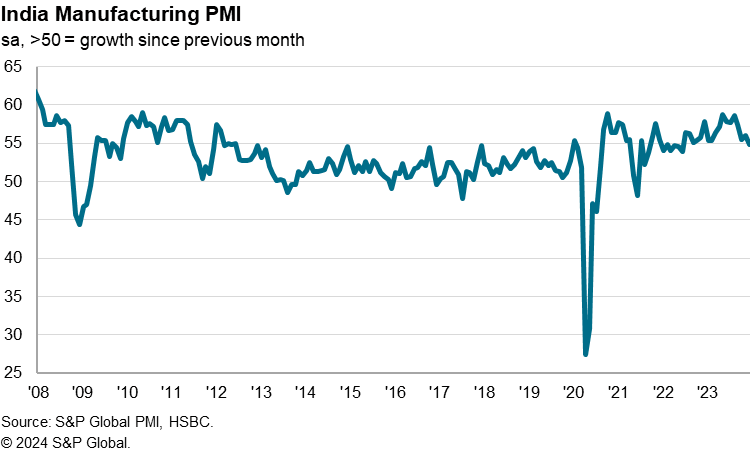

In India, GDP growth remained buoyant in the July-September quarter of 2023, at 7.6% y/y, after growth of 7.8% y/y in the April-June quarter. Industrial output has shown strong growth during 2023, with the latest industrial production data showing an 11.7% y/y rise in October. Manufacturing output rose by 10.4% y/y in October, boosted by a 22.6% y/y rise in output of capital goods. Production of infrastructure/construction goods also showed rapid growth in October, rising by 11.3% y/y, while output of consumer durables rose by 15.9% y/y.

{kind=link}

Despite falling from 56.0 in November to 54.9 in December, the seasonally adjusted HSBC India Manufacturing PMI, compiled by S&P Global, continued to indicate strong expansion in the Indian manufacturing sector, remaining well above the neutral mark of 50. New orders placed with Indian manufacturers continued to show positive demand conditions in December, albeit moderating from the previous month.

APAC medium-term economic outlook

The medium-term outlook is for continued resilient expansion in the APAC region, with robust domestic demand in many Asian emerging economies, including mainland China, India, Indonesia, Philippines and Vietnam supporting economic growth momentum.

The positive medium-term outlook for the APAC economy is supported by a number of factors.

Continued strong expansion in domestic consumer markets in large APAC economies, notably mainland China, India and Indonesia, will be an important factor supporting further growth in intra-APAC trade in raw materials, intermediate goods and final manufactured products. Sustained firm economic growth is driving rapid growth in per capita GDP in many of Asia's largest emerging markets, helping to boost demand for a wide range of goods and services in Asian consumer markets.

An important medium-term strength for many APAC industrial economies is their global competitiveness in the electronics manufacturing supply chain. Electronics production is an important part of the manufacturing export sector for many Asian economies, including South Korea, mainland China, Japan, Malaysia, Singapore, Philippines, Taiwan, Thailand and Vietnam. India also rapidly building up its electronics manufacturing sector. Furthermore, the electronics supply chain is highly integrated across different economies in East Asia.

The medium-term outlook for Asian electronics manufacturing is supported by many key growth drivers. This includes continued 5G rollout over the next five years, which will continue to support demand for 5G mobile phones, as well as demand growth for electronics products that integrate artificial intelligence capabilities. Demand for industrial electronics is also expected to grow rapidly over the medium term, helped by Industry 4.0, as industrial automation and the Internet of Things boosts rapidly growth in demand for industrial electronics.

APAC auto manufacturing hubs are also benefiting from the global transition to electric vehicles (EV), which is driving demand for EV exports produced in mainland China, Japan and South Korea. In early 2023, Hyundai started assembly of Ioniq 5 EVs at its new Hyundai Motor Group Innovation Center in Singapore. Indonesia has also benefited from strong foreign direct investment flows from multinationals to build new nickel smelters and electric vehicle battery plants.

With international tourism travel recovering strongly following the COVID-19 pandemic, the tourism industry is expected to be another important growth driver for APAC exports over the medium-term. Over the medium-term outlook, international tourism flows to the APAC region are expected to show strong growth, helped by rapidly rising household incomes in large Asian economies, notably mainland China, India and Indonesia.

The rapid growth of APAC exports is also expected to be strengthened by the APAC regional trade liberalization architecture. This includes the large Regional Comprehensive Economic Partnership (RCEP) and Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) multilateral trade agreements as well as the growing network of major bilateral FTAs involving APAC economies.

Overall, the medium-term economic outlook for the APAC region remains positive. APAC is already the largest region of the global economy measured in terms of size of nominal GDP, with emerging Asia expected to continue to grow rapidly over the decade ahead.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

APAC Economic Outlook For 2024 Remains Bright