APEMY - Aperam: Dividend Yield Of 7.1% And Strong Results For A Cyclical Trough Year

2023-10-11 17:25:54 ET

Summary

- The European steel sector is having a tough year, but I expect Aperam to book EBITDA of over €400 million ($424 million).

- This is a cyclical business, and the company’s EBITDA has been getting stronger in each market downturn over the past decade.

- Aperam’s balance sheet looks strong, sustaining capital is low, and the quarterly dividend of €0.50 ($0.53) per share seems safe.

Introduction

French cabling specialist Nexans ( NXPRF ) is the largest position in my stock portfolio at the moment and I’ve been looking for other investment opportunities in France. One company that caught my attention is steel producer Aperam ( APEMY ) due to its 7.1% dividend yield and solid balance sheet. While 2023 is shaping up as a tough year for the steel industry in Europe, I think the company's EBITDA for the full year could surpass €400 million ($424 million) and that the quarterly dividend of €0.50 ($0.53) per share is likely to be kept unchanged. My rating on the stock is a speculative buy. Let’s review.

Overview of the business and financials

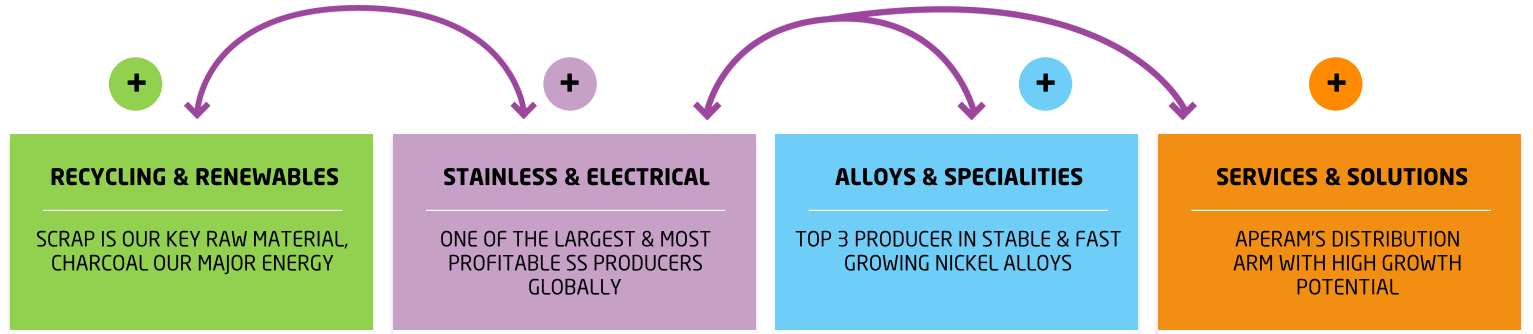

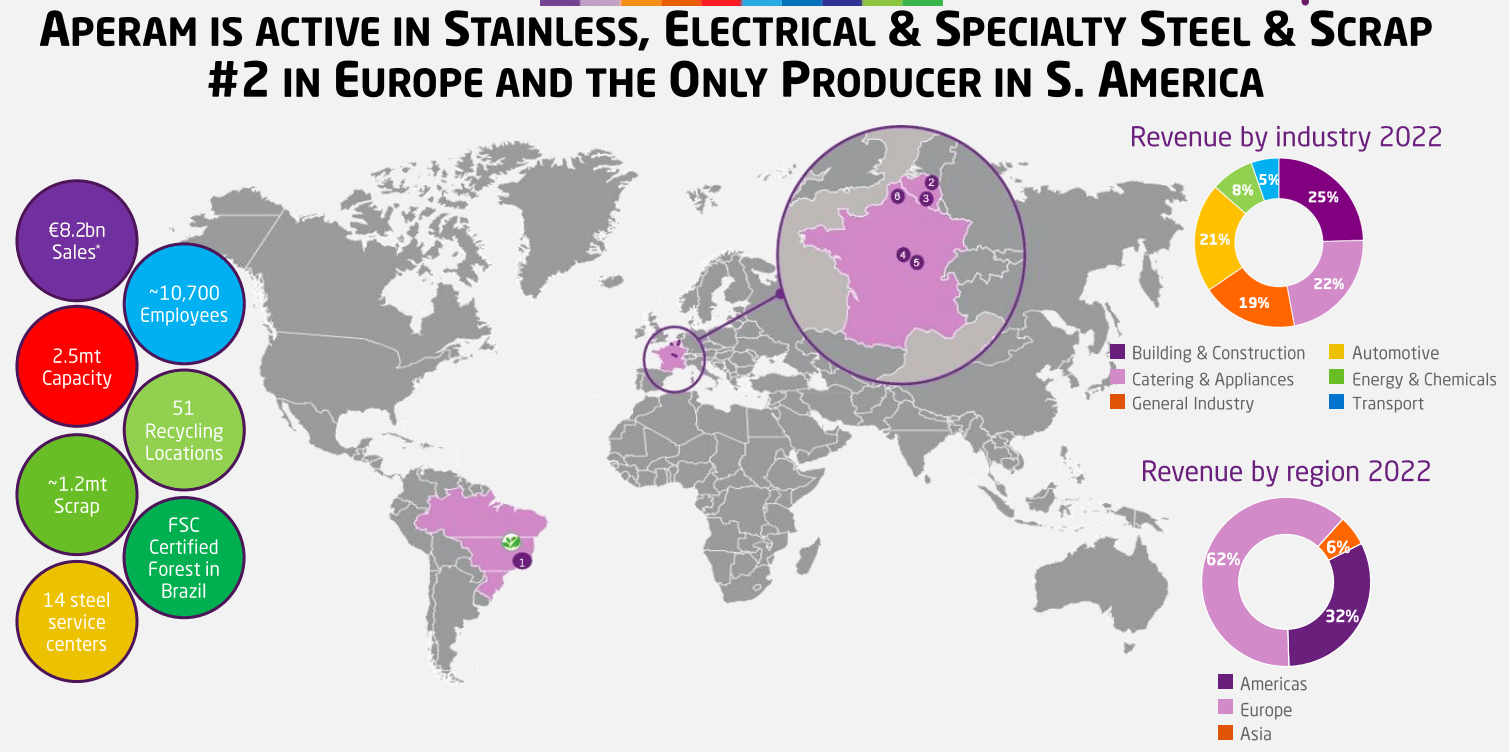

Aperam is a Belgian-French stainless, electrical, and specialty steel producer with a network of six production facilities in Brazil, Belgium, and France and customers in over 40 countries worldwide. The company has a flat stainless and electrical steel capacity of 2.5 million tonnes per year and is the second largest flat stainless steel producer in Europe. In 2022, it had steel shipments of 1.6 million tonnes and generated sales of €8.16 billion ($7.74 billion) and an adjusted EBITDA of €1.08 billion ($1.02 billion). Aperam is also a major producer of high performance alloys as well as recycler of stainless steel scrap. The company’s business is split into four reportable segments, namely stainless and electrical steel, services and solutions, alloys and specialties, and recycling and renewables. Its shares are listed on Euronext Amsterdam, Euronext Paris, Euronext Brussels, and the Luxembourg Stock Exchange.

{kind=link}

{kind=link}

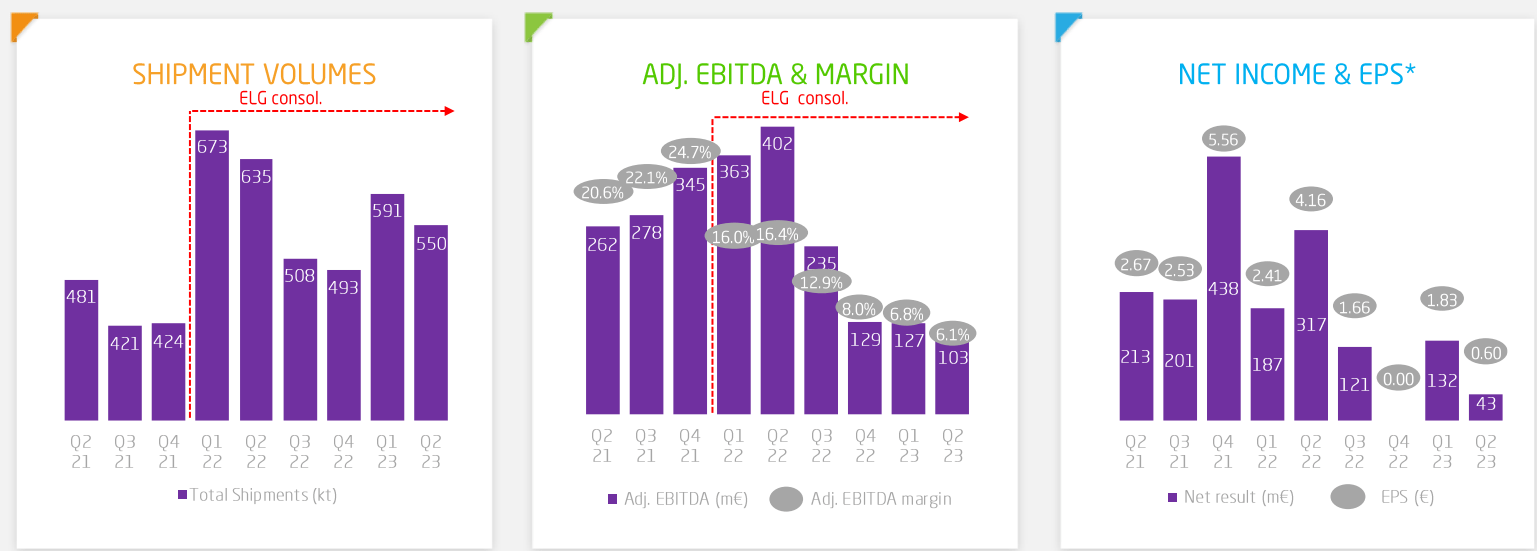

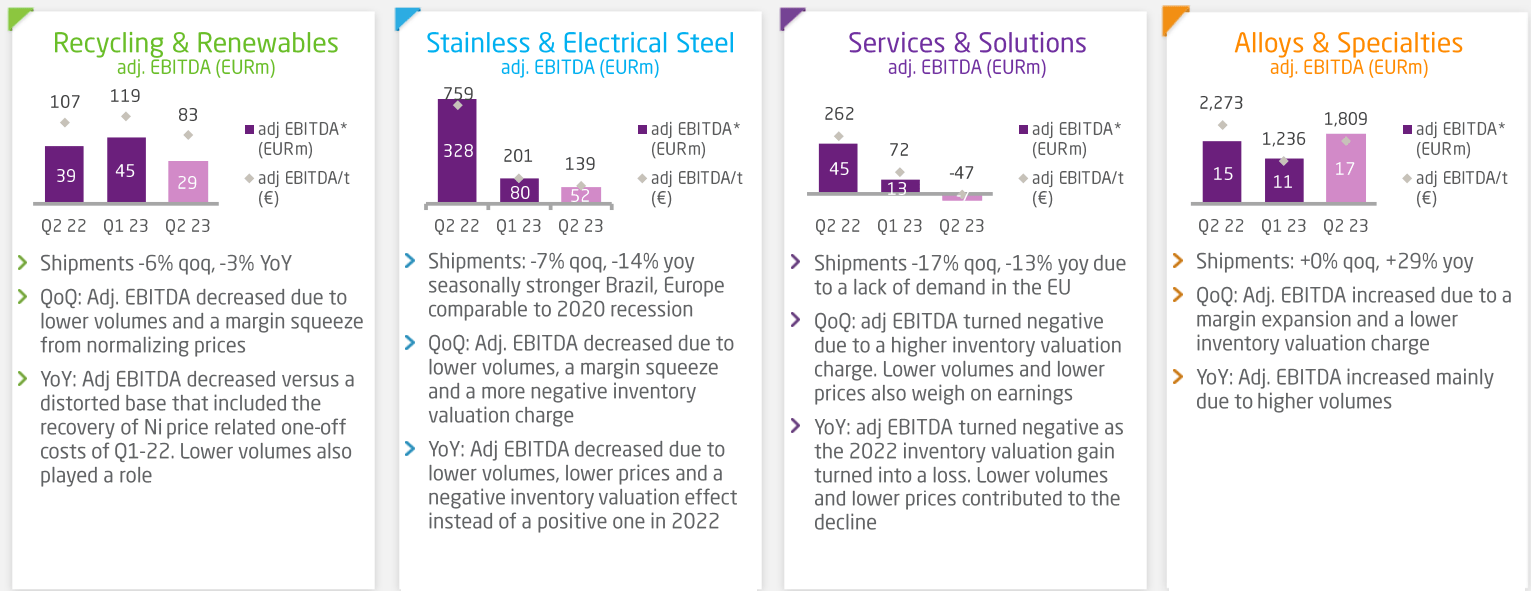

Looking at the financial performance of the business, Aperam had a strong 2022 as the prices of several commodities including steel soared during the year following the end of COVID-19 restrictions. Both sales and adjusted EBITDA registered record highs. Yet, the performance of the business started deteriorating in the second half of 2022 as steel shipments fell due to destocking by customers in Europe while EBITDA margins were under pressure due to negative inventory valuation, and a price/cost squeeze. Steel shipments increased in the first half of 2023 due to seasonal factors but continued to be negatively affected by destocking in Europe as well as weak steel demand on the continent. The adjusted EBITDA margin, in turn, was down to just 6.1% in Q2 2023 due to lower realized prices as the growth of Europe’s economy is slowing down amid rising interest rates and geopolitical tensions. In its presentation for the Q2 2023 financial results, Aperam said that volumes and prices in Europe are consistent with a recession (see slide 4 here ).

{kind=link}

{kind=link}

On a positive note, Aperam said that demand in Brazil was high, and I think the recycling and renewables, and alloys businesses had a decent quarter in terms of EBITDA. Unfortunately for investors, the bulk of the company’s EBITDA usually comes from the stainless and electrical steel segment which is currently struggling.

{kind=link}

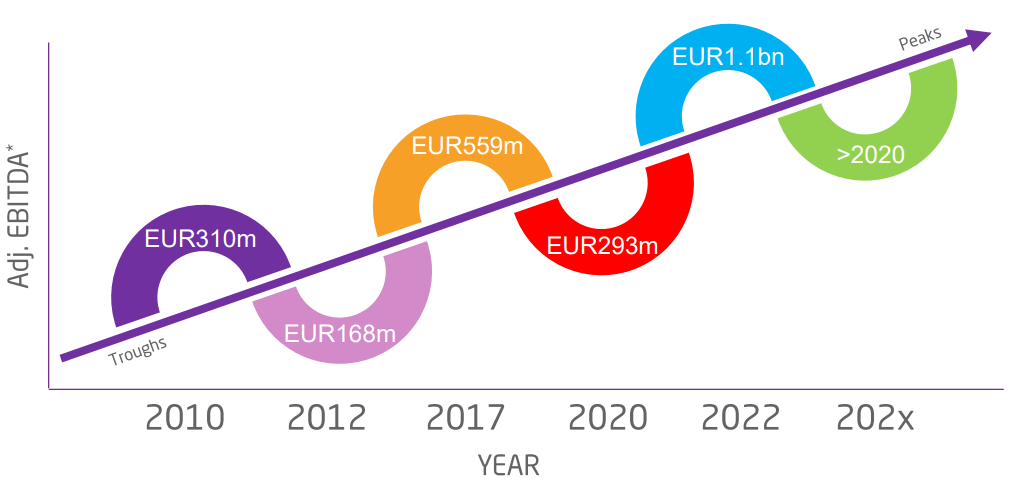

Overall, Aperam is operating in a tough macroeconomic environment at the moment, but I think that its financial performance for 2023 so far has been good. This is a cyclical business, and the company’s EBITDA has been getting stronger in each market downturn over the past decade. In my view, this is being reflected in the share price as Aperam’s stock is down just 7.08% YTD on Euronext Amsterdam (its primary listing).

{kind=link}

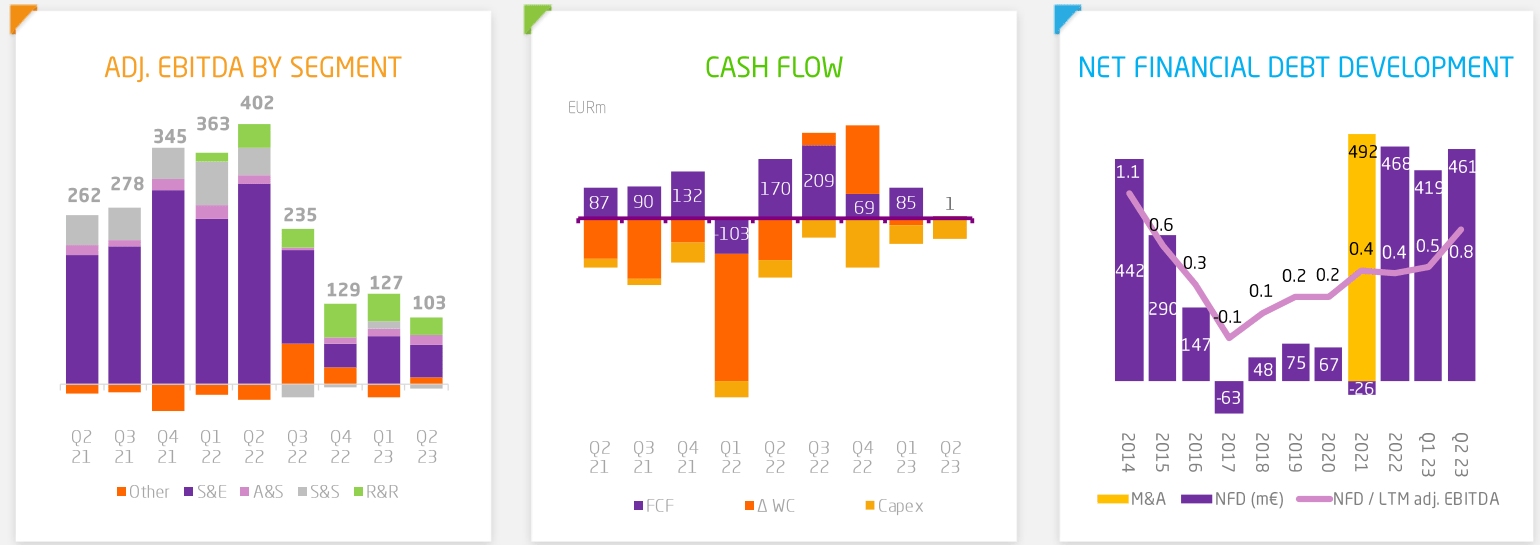

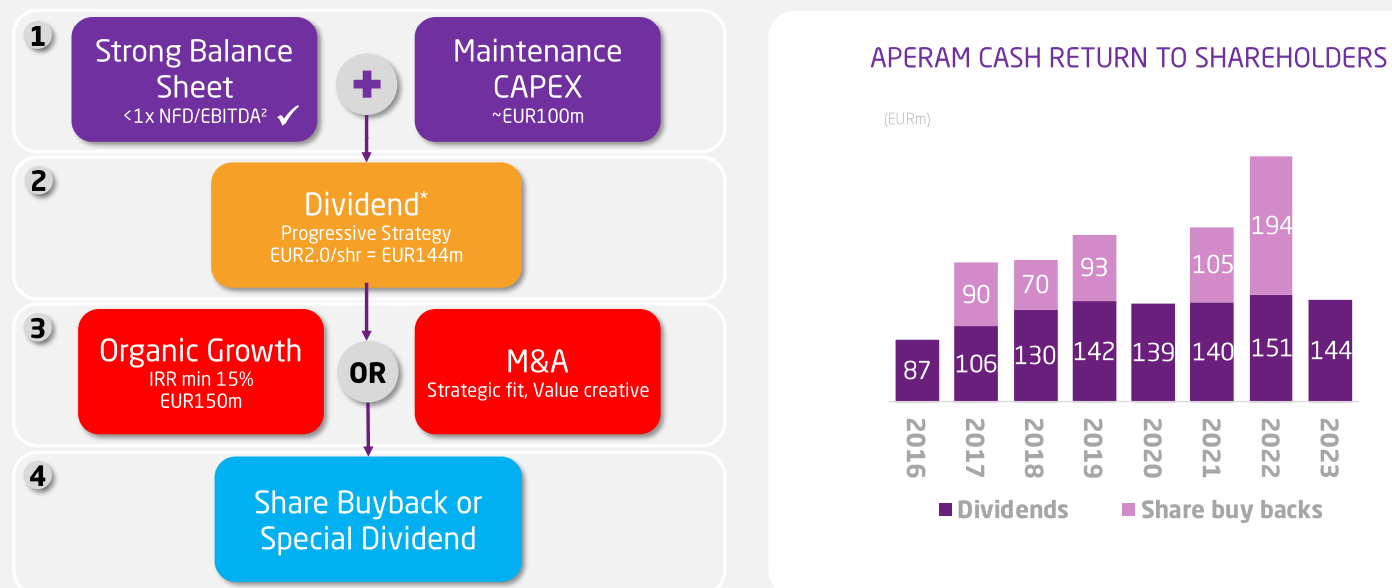

Turning our attention to the balance sheet, I think that Aperam is in a good position to weather the storm as net financial debt was just €461 million ($488 million) as of June 2023 (see page 7 here ), which translates into a gearing ratio of 0.78x on a TTM basis. Annual maintenance CAPEX is about €100 million ($106 million) and free cash flow for H1 2023 alone stands at €86 million ($91 million).

Looking at what to expect for the future, I think that steel shipments and EBITDA will continue to fall in Q3 and Q4 as economic growth in Europe is still slowing down. That being said, I expect EBITDA for the full year to remain above €400 million ($424 million) and considering the quarterly dividend of €0.50 ($0.53) per share costs the company only about €36 million ($38 million) each quarter, I think it’s likely for the size of dividend payments to remain unchanged. That being said, it seems likely that share buybacks will dry up over the coming quarters. Aperam will release its Q3 2023 financial results around November 10.

{kind=link}

Turning our attention to the valuation, Aperam has an enterprise value of €2.66 billion ($2.82 billion) as of the time of writing and the company is trading at an EV/EBITDA ratio of 4.5x on a TTM basis. Considering the balance sheet is strong, the dividend seems safe, and I expect 2023 EBITDA to remain above €400 million ($424 million), I think Aperam should be worth at least 6x EV/EBITDA on a TTM basis.

Looking at the downside risks, I think that the major one is a prolonged recession in Europe as this could keep steel demand low for 2024 and potentially 2025. The situation is starting to look particularly concerning in Germany where the Government has just announced that it expects the economy to shrink by 0.4% in 2023 and grow by just 1.3% in 2024. In addition, the share price of Aperam could be under pressure over the coming months due to the lack of share buybacks.

Investor takeaway

Aperam has been performing well financially in 2023 considering this is shaping up as a cyclical trough year for the European steel industry and I think the quarterly dividend looks safe. The balance sheet looks strong, sustaining capital is low, and I expect EBITDA for the full year to remain above €400 million ($424 million). That being said, Europe could face a long recession which is why my rating on the stock is a speculative buy. Note that if you want to open a position, it could be best to avoid the US OTC market as the daily trading volume there rarely surpasses 1,000 shares.

For further details see:

Aperam: Dividend Yield Of 7.1% And Strong Results For A Cyclical Trough Year