APMSF - Aperam: Guiding For A Long-Term EPS Of 6.5-7 EUR Per Share

Summary

- Aperam, listed in Amsterdam, is one of the most important producers of stainless steel in the world.

- The company is pretty cyclical but is actively taking steps to reduce its exposure to the sometimes violent cycles.

- The 2025 guidance calls for an EBITDA of 800-850M EUR, which should result in an EPS of 6.5-7 EUR, while the sustaining FCF should be even higher.

Introduction

Aperam (APEMY) (APMSF) is one of the world’s largest producers of stainless steel and specialty steel in the world. Originally spun off from steel giant ArcelorMittal ( MT ), Aperam went its own way and has done so quite successfully. Despite its dependence on nickel and natural gas in the production process, Aperam has successfully been able to protect its margins – although we obviously have to be mindful of the downturn this cyclical sector is in.

{kind=link}

Yahoo Finance

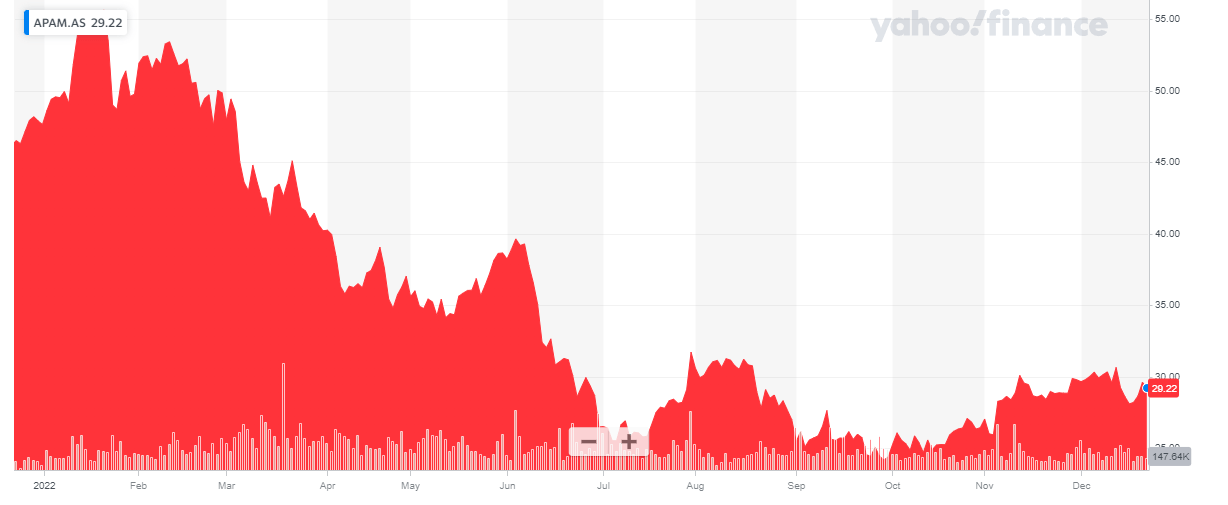

Aperam's main listing is on Euronext Amsterdam where the stock is trading with APAM as its ticker symbol. The average daily volume exceeds 200,000 shares, making it the most liquid listing. There are approximately 75.5M shares outstanding, resulting in a market cap of just around 2.25B EUR.

The stainless steel market held up better than I had expected

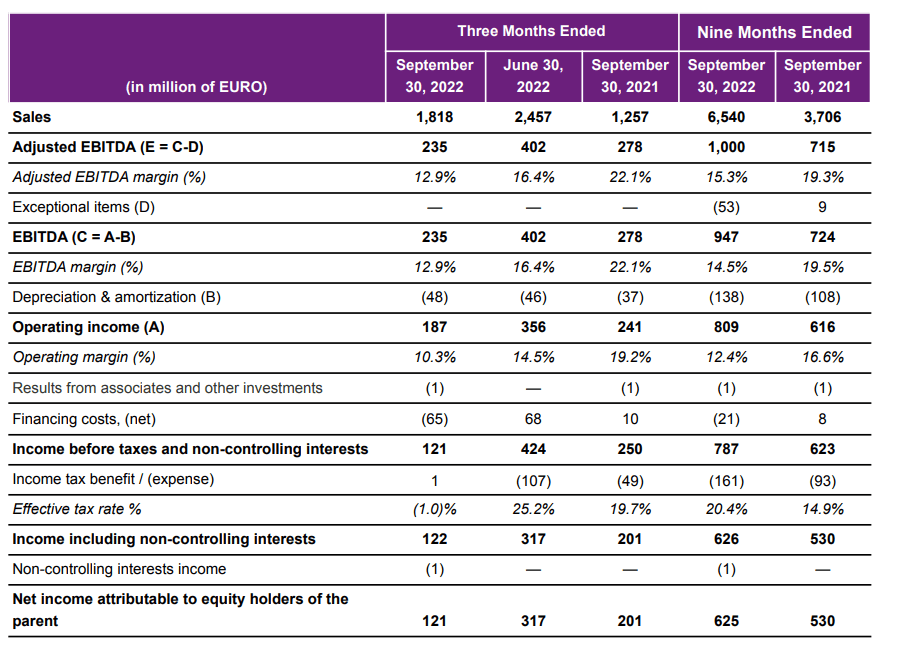

During the third quarter, Aperam shipped just over 500,000 tonnes of steel. Not only is this a 20% decrease compared to the second quarter, it also is a 25% decrease compared to the first quarter of this year. It still is a step-up from the fourth quarter of last year thanks to the acquisition of ELG , but the stainless steel was sold at a lower margin.

{kind=link}

Aperam Investor Relations

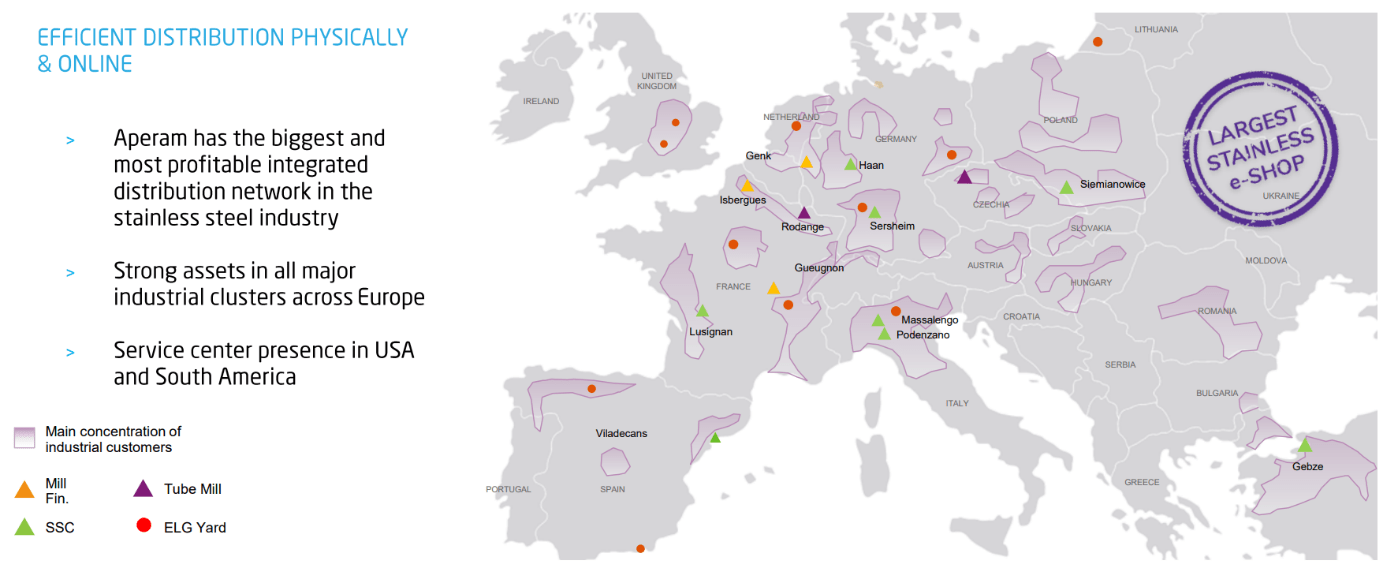

Thanks to the acquisition of ELG, Aperam has now further worked towards vertically integrating its production process.

{kind=link}

Aperam Investor Relations

The total revenue in the third quarter was 1.82B EUR , a decrease of approximately a third compared to the second quarter. The total adjusted EBITDA was approximately 235M EUR and although this still sounds great in absolute numbers, it is a 40% decrease compared to the second quarter and even a 15% decrease compared to the third quarter of last year (which excludes the impact of the ELG acquisition).

{kind=link}

Aperam Investor Relations

The pre-tax income was approximately 121M EUR resulting in a net income of 122M EUR thanks to a 1M EUR tax benefit. The attributable net income was 1.66 EUR per share as the net income attributable to the non-controlling interests was 1M EUR.

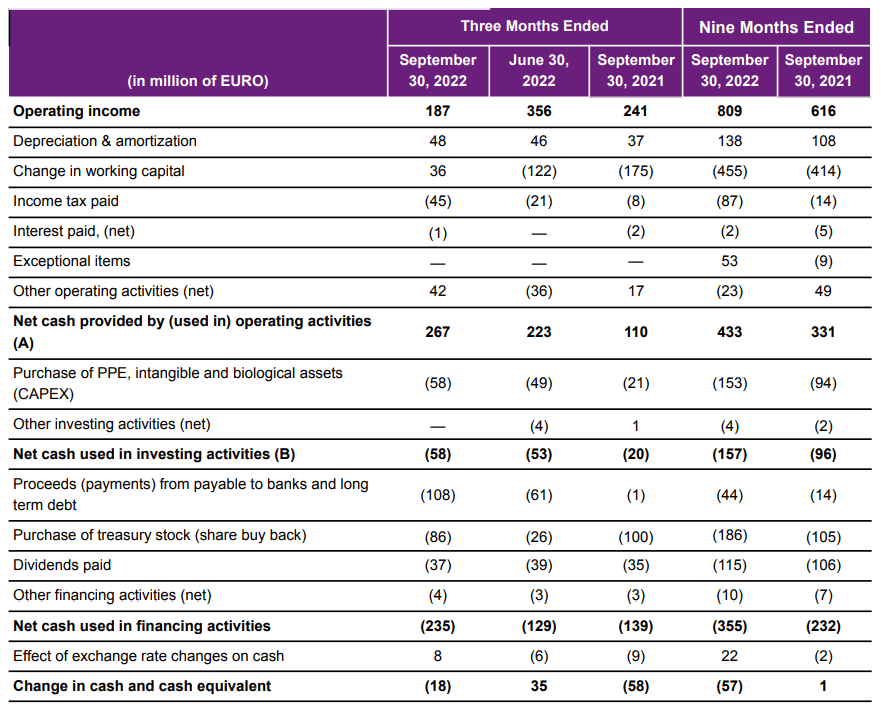

One of the main reasons why I always liked Aperam is its ability to generate a positive operating and free cash flow. Despite the weaker results in the third quarter, Aperam was still cash flow positive. Its reported operating cash flow was 265M EUR. This does include a 36M EUR contribution from working capital changes, and the adjusted operating cash flow was 229M EUR.

{kind=link}

Aperam Investor Relations

The total capex was 58M EUR, which means Aperam generated about 171M EUR in free cash flow. Divided over 75.5M shares outstanding, this means the underlying free cash flow 2.26 EUR per share. That’s higher than the reported net income mainly due to the high non-cash finance expenses during the quarter. This was entirely related to FX changes as Aperam’s net interest expense was close to zero as the interest payments were offset by the income on the cash in the treasury.

As of the end of September, Aperam had about 467M EUR in cash, 269M EUR in short-term debt and 680M EUR in long-term debt for a net debt of 482M EUR. Aperam continues to reduce its net debt with the incoming free cash flow and considering the YTD EBITDA came in at 1B EUR and even the Q3 adjusted EBITDA was 235M EUR, the debt ratio will likely be less than 0.5 by the end of this year.

The 2022 capital markets day was enlightening

Earlier this year, Aperam organized a capital markets day. One of the main focus points was Aperam’s role in the circular economy and that’s another reason why the ELG acquisition was important for Aperam. The management’s long-term incentive plans are now also aligned with these targets.

{kind=link}

Aperam Investor Relations

The company is also aiming to increase its normalized EBITDA by 300M EUR . Seeing how the adjusted EBITDA in 2016- 2017-2018 was respectively 503M EUR, 559M EUR and 504M EUR for an average EBITDA of 522M EUR, the 2025 guidance implies a normalized adjusted EBITDA of 800-850M EUR.

We know the annual depreciation expenses are about 200M, the net interest expenses should be zero which means the long-term guidance should result in a pre-tax income of 600-625M EUR. The effective tax rate should continue to be roughly 20-22% resulting in a reported net income of 468-500M EUR for an EPS of 6.5-7 EUR per share.

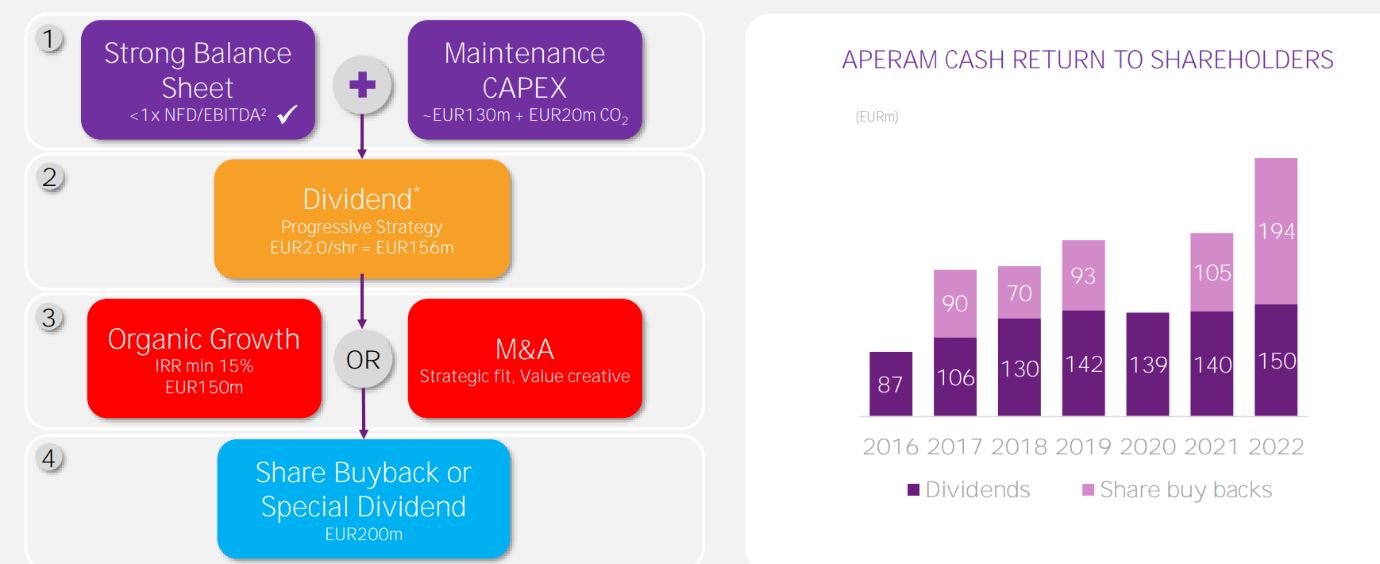

We also know the maintenance capex + CO2 payments are just about 150M EUR per year, which means the free cash flow result should be slightly higher than the reported net income.

{kind=link}

Aperam Investor Relations

Aperam also plans to pay a dividend of 2 EUR per share which will cost the company just over 150M EUR per year. The remainder will be spent on organic growth (with a minimum required Internal Rate of Return of about 15%). The remaining cash could the subsequently be used to buy back stock and/or a special dividend.

Investment thesis

I have no position in Aperam, as I already have a long position in Acerinox (ANIOY), a Spain-based stainless steel producer. But seeing how well Aperam’s financial results are holding up (not unlike Acerinox’ results), perhaps I should start buying Aperam as well.

In any case, I think Aperam is a well-led producer of stainless steel and the acquisition of ELG will likely prove to be a good addition in the long run. I also like how Aperam is planning on improving its sales mix to get more exposure to the smaller customers where the EBIDA margins are higher. I also like the company’s plan to diversify away from being a pure stainless steel producer as its alloys and specialties EBITDA will double ‘till 2025’ which I interpret as ‘it will double every year’.

I fully realize the steel and stainless steel sector are currently in a down-cycle. But I would like to initiate a long position within the next few months. I noticed the option premiums for Aperam are pretty solid with for instance the premium for a P25 expiring in March coming in at 0.90 EUR these days thanks to the elevated volatility levels.

For further details see:

Aperam: Guiding For A Long-Term EPS Of 6.5-7 EUR Per Share