APMSF - Aperam: Trading At A 12% FCF Yield Despite A 47% Lower EBITDA Assumption

2023-03-13 11:30:00 ET

Summary

- Aperam is one of the largest stainless steel producers in the world.

- As expected, Q4 2022 was tough, and while Q1 2023 should be better, let's remain realistic.

- I anticipate a 40+% EBITDA decrease compared to 2022, but even a 600M EUR EBITDA result should result in a very strong free cash flow result.

- The longer term targets remain intact: Aperam intends to grow its EBITDA to 800-850M EUR by 2025. That's realistic.

Introduction

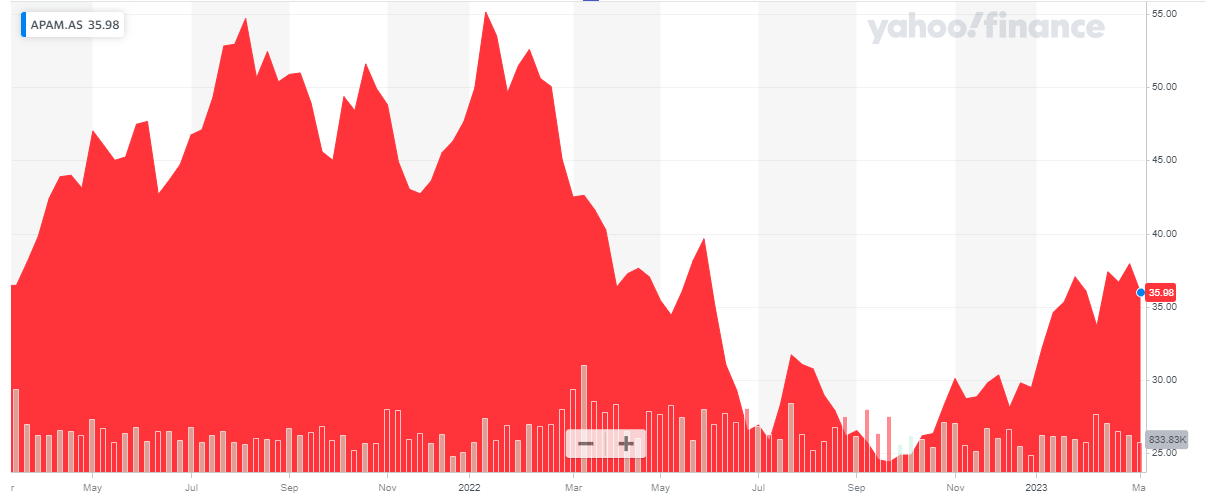

I’m keeping close tabs on two stainless steel producers in Europe. In an article published last week I discussed Acerinox ( OTCPK:ANIOY ) but I obviously also wanted to follow up on how Aperam ( OTC:APEMY ) ( OTCPK:APMSF ) is doing after turning bullish on the company in an article published in December last year. The market seems to agree with my bullish interpretation of Aperam’s previous set of results as the stock is currently trading almost 20% higher, which is quite remarkable given the S&P 500 remained flat.

Seeking Alpha

Aperam's main listing is on Euronext Amsterdam where the stock is trading with APAM as its ticker symbol. The average daily volume is approximately 210,000 shares , making it the most liquid listing. There are approximately 72M shares outstanding, resulting in a market cap of just around 2.6B EUR, up from the 2.25B EUR the company was trading at when I last discussed Aperam.

{kind=link}

This article is meant as a follow-up to specifically discuss the recently published Q4 results. For a better understanding of the company and why I have a long-term bullish view, please have a look at my December article .

The fourth quarter was indeed rather weak, but Aperam remains in a good shape

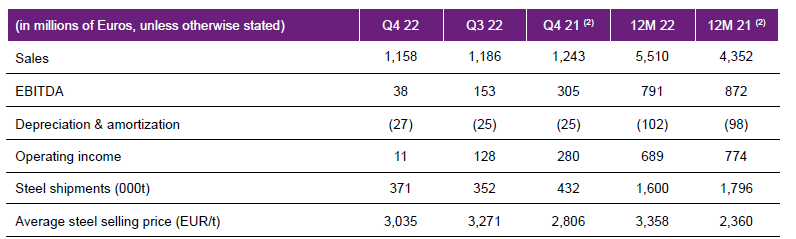

During the final quarter of 2022, Aperam saw the total amount of steel shipments increase versus the third quarter (up by over 5%) but unfortunately the average selling price decreased by about 7% which resulted in a revenue of just 1.16B EUR in the stainless steel segment. And not only did the revenue decrease, the operating expenses increased which really put pressure on the EBITDA as the EBITDA fell from 153M EUR to 38M EUR on the back of a price/cost squeeze.

{kind=link}

Fortunately, the company has other divisions making up for the weak set of results in the steel production division and the EBITDA contribution from the alloys and specialties segment more than doubled to 12M EUR while the EBITDA in the recycling and renewables division also increased by 80% to 55M EUR compared to the third quarter of last year. It’s even more remarkable the company was able to do so despite a 7% revenue increase.

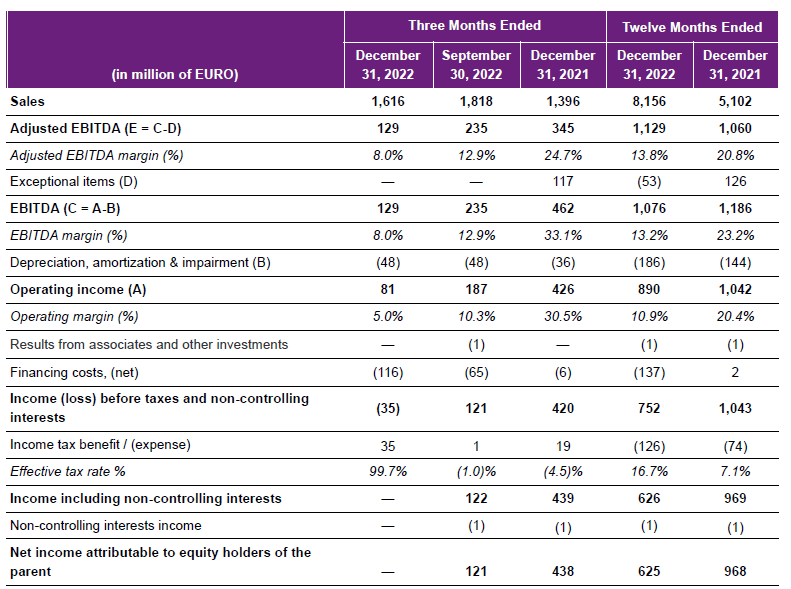

On a consolidated basis, the total revenue in the third quarter was approximately 1.62B EUR, a decrease of approximately 10% compared to the third quarter, but the more important element was the margin pressure as the EBITDA margin fell from 12.9% to just 8.0% on a QoQ basis.

{kind=link}

This obviously had a very negative impact on the bottom line and although the operating income remained positive, the company ended the year without any profit in the final quarter of 2022. There was a pre-tax loss of 35M EUR due to higher financing costs but this was compensated by a 35M EUR tax benefit.

Of course the first semester of 2022 was very strong and Aperam’s full-year EBITDA came in at 1.13B EUR of which about 70% was generated in the first half of the year. The bottom line also shows a very strong net income result of 625M EUR or 8.33 EUR per share.

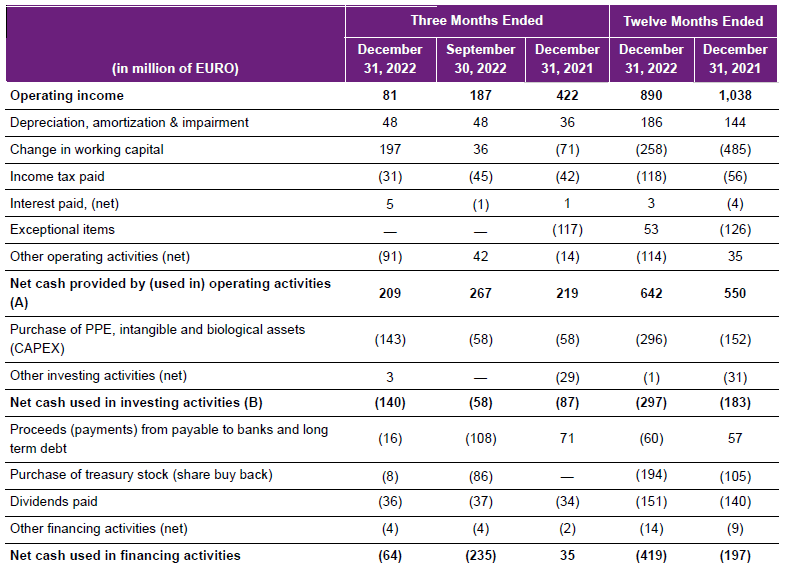

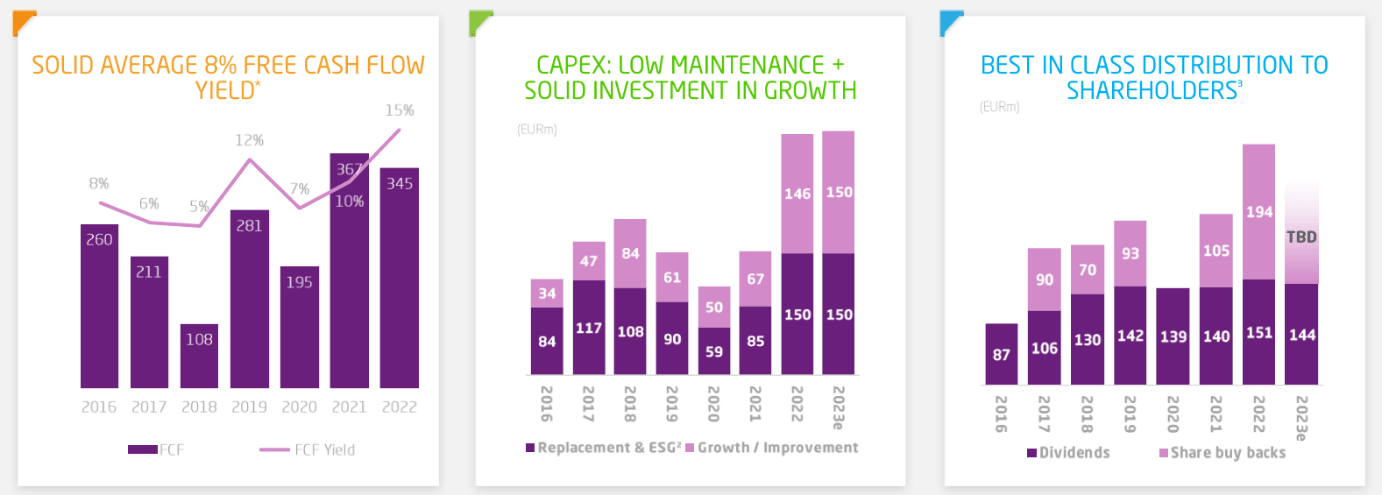

And despite not being able to generate a profit in the final quarter, Aperam’s cash flow was strong although the reported positive free cash flow was mainly related to the 197M EUR release of working capital elements which pushed the reported operating cash flow to 209M EUR despite a negative hit of 91M EUR from other operating activities.

{kind=link}

The capex was also pretty heavy in the final quarter of the year as the company spent 143M EUR on capital expenditures versus just 153M EUR in the first nine months of the year. The 143M capex bill is also approximately three times the depreciation expenses and it’s probably not a surprise to see Aperam investing in growth. As you can see below, the sustaining capex was just 150M EUR last year (and will be roughly the same for this year) which is approximately 75% of the depreciation and amortization expenses.

{kind=link}

2023 still is a question mark as it is tough to have a good idea of what the rest of the year will look like. Aperam did provide a Q1 outlook and the company expects a slightly higher amount of shipments and an increase of the adjusted EBITDA compared to the fourth quarter of 2022 so that is already encouraging.

The company is also sticking with its dividend policy: the company pays 2.00 EUR per share per year in four equal quarterly installments of 0.50 EUR per share.

Investment thesis

The second half of 2022 was pretty weak, and I’m also not expecting much from the first half of 2023 although it is looking like we have seen the bottom in the stainless steel market as both Acerinox and Aperam are guiding for a higher EBITDA in Q1 versus Q4. That’s not entirely surprising considering the final quarter is usually pretty soft due to a seasonal impact.

I currently have no position in Aperam. Subsequent to the publication of my December article I wrote a combination of in the money and out of the money put options but they all expired out of the money. I will likely continue to write put options as I like Aperam’s plans for the future. Expect a rather weak EBITDA this year (600-700M EUR would likely be a good ballpark number, and even at 600M EUR in EBITDA, the company should still be posting a sustaining free cash flow result of 4.25-4.50 EUR per share)) and I think there will be more opportunities to pick up stock throughout this year.

For further details see:

Aperam: Trading At A 12% FCF Yield Despite A 47% Lower EBITDA Assumption