AROC - Archrock: Recent Guidance Increase And Deleveraging Expectations

2023-08-23 14:52:27 ET

Summary

- Archrock, Inc. is a leading energy infrastructure company specializing in midstream natural gas compression.

- I believe that investors would most likely be interested in the new capital expenditures planned to cope with demand from clients.

- Further increases in the average operating horsepower and horsepower utilization driven by efficiency and scalability thanks to a capacity increase will most likely lead to FCF margin improvements.

Archrock, Inc. ( AROC ) recently noted intentions to lower the debt levels, and announced further capital expenditures to cope with the growing demand from customers. Management also noted increases in average operating horsepower and horsepower utilization, which may lead to larger FCF margin in the near future. I believe that there are several risks with respect to the total amount of debt and inflation, however, I also think that the company could be worth close to $20 per share.

Archrock: Increase In Guidance And Gross Margin In Aftermarket Service

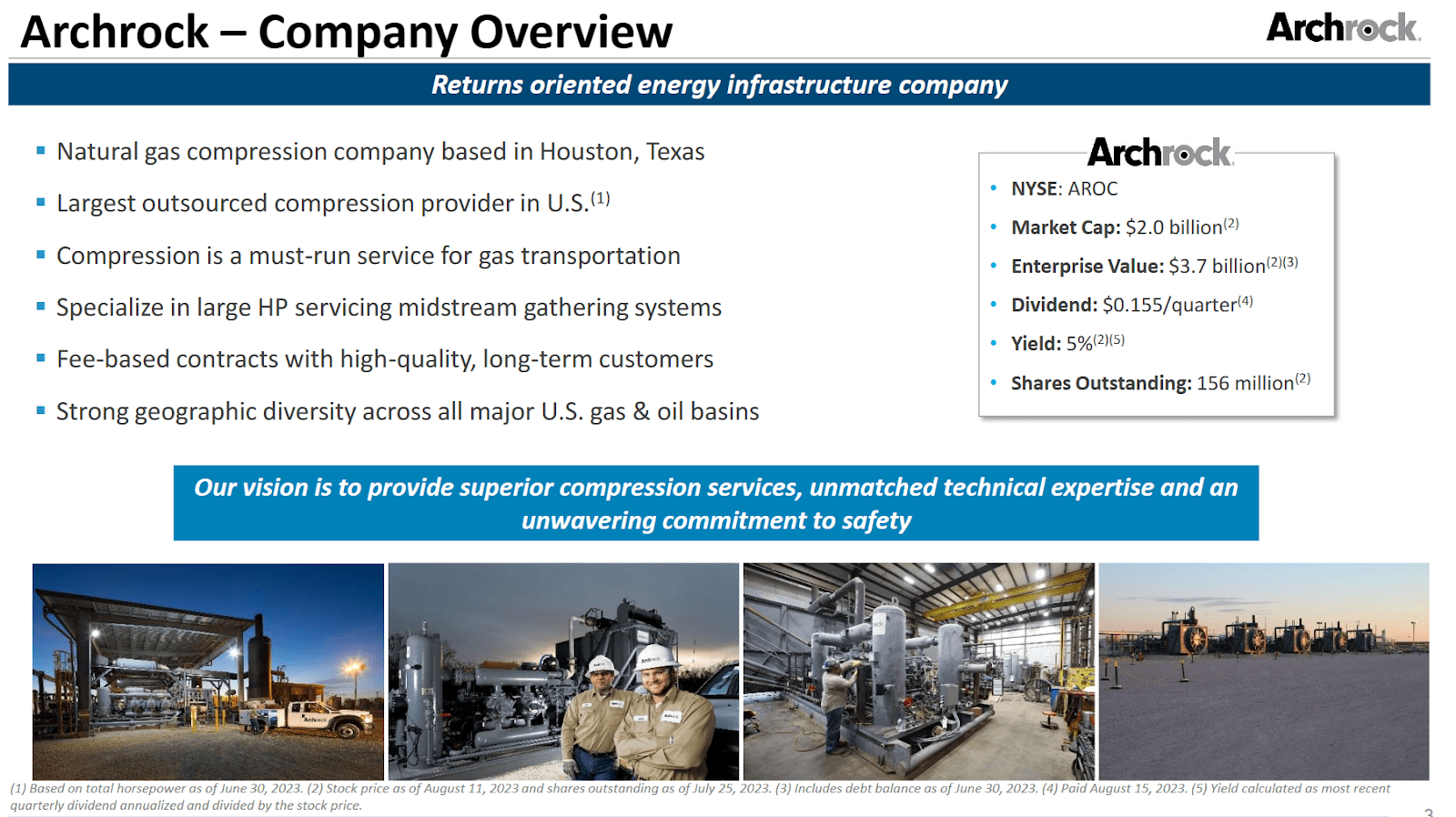

Archrock, Inc. is a leading energy infrastructure company specializing in midstream natural gas compression. It arose as a result of the merger of Universal Compression Holdings, Inc. and Hanover Compressor Company in 2007. Since then, it has established itself as the leader in natural gas compression in the United States, operating in two key segments: contract operations and aftermarket services.

{kind=link}

Archrock, Inc. operates a strong aftermarket service, encompassing the sale of parts and components as well as providing operation, maintenance, overhaul, and reconfiguration services to its compression equipment customers. With highly experienced staff and access to full compression facilities, it is well positioned to provide these services. I believe that investors may want to study carefully the recent increase in gross margins in the aftermarket services. It reports lower net sales than the contract operations segment, but the increase in margins appears promising.

Source: 10-Q

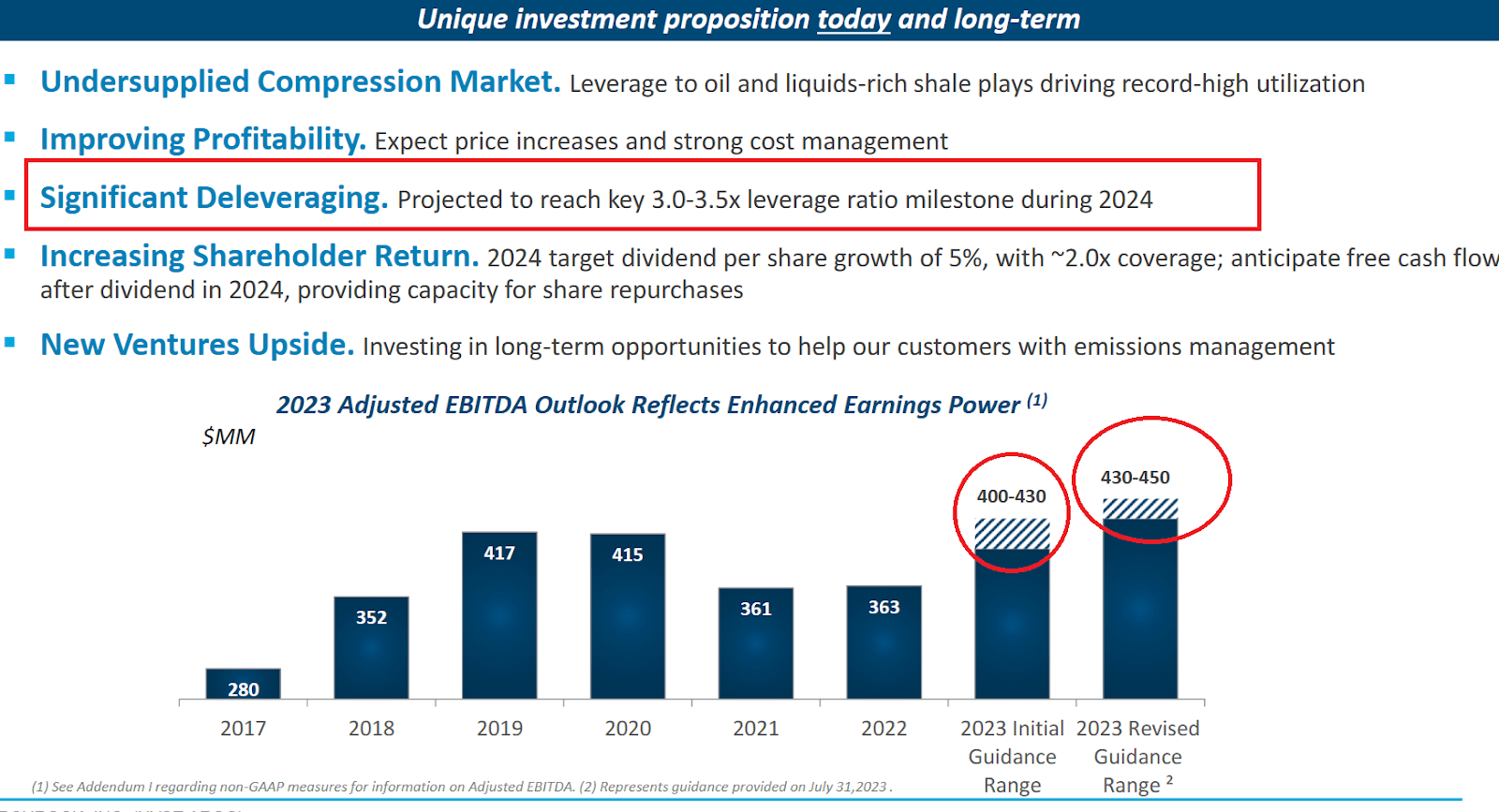

Besides, I believe that the most relevant thing about Archrock, Inc. is the recent Adjusted EBITDA guidance, which was recently increased. The company believes that it could see growth in its EBITDA from close to $363 million in 2022 to about $430-$450 million.

{kind=link}

Balance Sheet

As of June 30, 2023, Archrock, Inc. reported cash and cash equivalents of about $1 million, accounts receivable close to $120 million, inventory worth $93 million, and total current assets close to $223 million. The ratio of current assets/current liabilities is larger than 1x, so I believe that there is no liquidity issue out there.

The property, plant, and equipment is worth $2300 million, which is the most relevant asset that the company reports. It represents close to 80%-85% of the total amount of assets. Besides, the company reports deferred tax assets of $20 million and total assets of about $2.68 billion.

Source: 10-Q

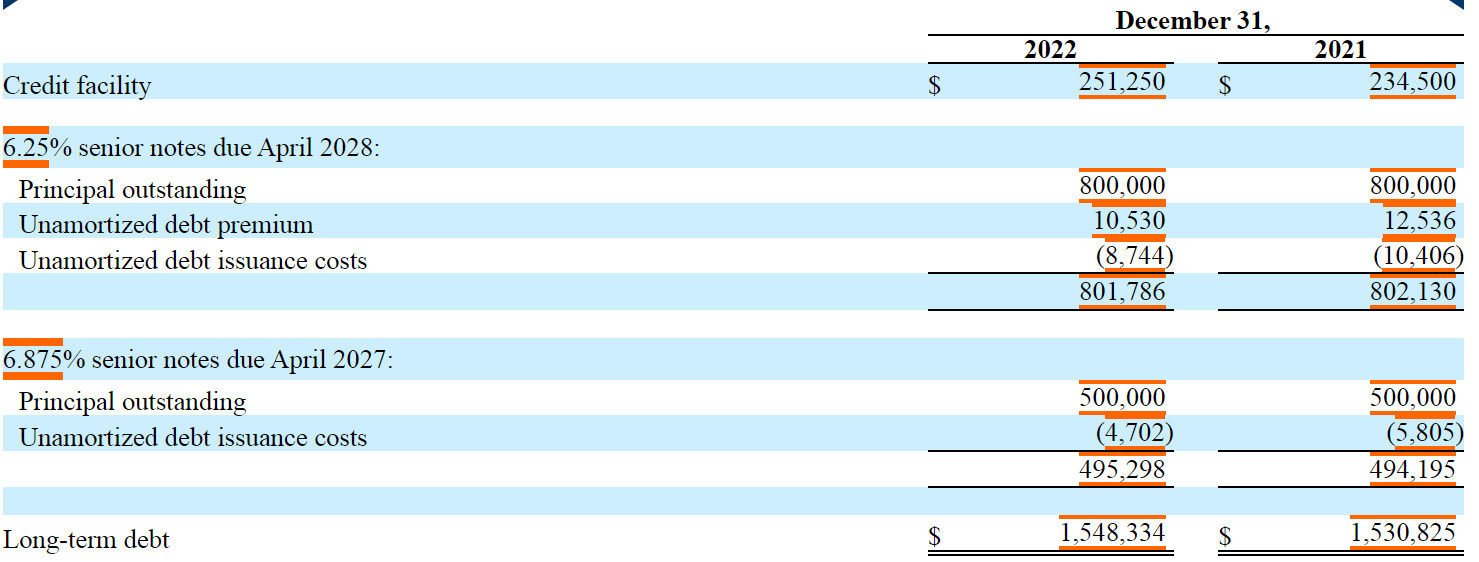

The list of liabilities includes accounts payable worth $64 million, accrued liabilities close to $76 million, and total current liabilities worth $148 million, Besides, with long-term debt of $1548 million, total liabilities are equal to $1.738 billion.

Source: 10-Q

Considering the total amount of debt, I think that having a look at the contractual obligations makes a lot of sense. As of December 31, 2022, Archrock, Inc. has a facility with a total loan commitment of $750.0 million, maturing in November 2024, with the option to increase commitments up to an additional $250.0 million. The loans are backed by assets and subsidiaries, with variable interest rates based on Archrock's choice of base rate or LIBOR, plus a spread.

{kind=link}

Archrock, Inc. currently has a financial debt/EBITDA of close to 4x-5x, so I believe that conservative individuals may not appreciate the business model. With that, let's note that Archrock, Inc. did report a financial debt/EBITDA of close to 11x. In my view, further decrease in the leverage ratio may lead to further interest from market participants.

Source: Ycharts

Financial Valuation

Archrock, Inc. intends to leverage its competitive advantages as well as to pursue a number of key strategies. Focused on the US natural gas compression industry, Archrock, Inc. would most likely capitalize on growing demand and increased natural gas production and exports.

I also believe in further improving profitability by optimizing processes and technologies, including advanced analytics and telematics to reduce costs. Besides, further improvement in capacity will most likely bring economies of scale. In this regard, it is worth noting that the average operating horsepower and horsepower utilization continued to increase in 2023. With this in mind, I remain optimistic about the future.

Source: 10-Q

More in particular, I believe that we may see further increase in the gross margin percentage driven by net sales growth and lower increase in cost of sales like we saw in the last quarter.

Revenue in our contract operations business increased primarily due to higher rates and an increase in average operating horsepower for contract compression in response to market conditions, partially offset by the impact of strategic dispositions of horsepower in 2022. Source: 10-Q

Archrock, Inc. recently made significant investments in new compression equipment as the company appears to be experiencing higher customer demand. I believe that investors will most likely enjoy growing free cash flow as capex lowers over time. In this regard, I believe that investors may want to have a look at the following lines.

The increase in 2023 capital expenditures, and further into 2024 particularly for growth capital expenditures, as compared to 2022 is due to increased investment in new compression equipment as a result of higher customer demand. Source: 10-Q

Under my financial model, I assumed that lowering the net debt/EBITDA levels would most likely offer financial flexibility. As a result, I believe that Archrock, Inc. could undertake acquisitions, which may accelerate capacity increases too. In the annual report, the company noted that it needs acquisitions to grow effectively.

Our ability to grow depends, in part, on our ability to make accretive acquisitions. Source: 10-k

I also think that the repurchase of stock planned under the 2023 Share Repurchase Program may lower the cost of capital, which may have a beneficial effect on the future stock valuation. In this regard, I believe that we may see more stock buybacks from 2024. Let's keep in mind that the company has a long history of stock buybacks.

On April 27, 2023, our Board of Directors authorized a share repurchase program that allows us to repurchase up to $50.0 million of outstanding common stock. Under the 2023 Share Repurchase Program, shares of our common stock may be repurchased periodically, including in the open market, privately negotiated transactions, or otherwise in accordance with applicable federal securities laws, at any time until April 27, 2024.Source: 10-Q

Source: Ycharts

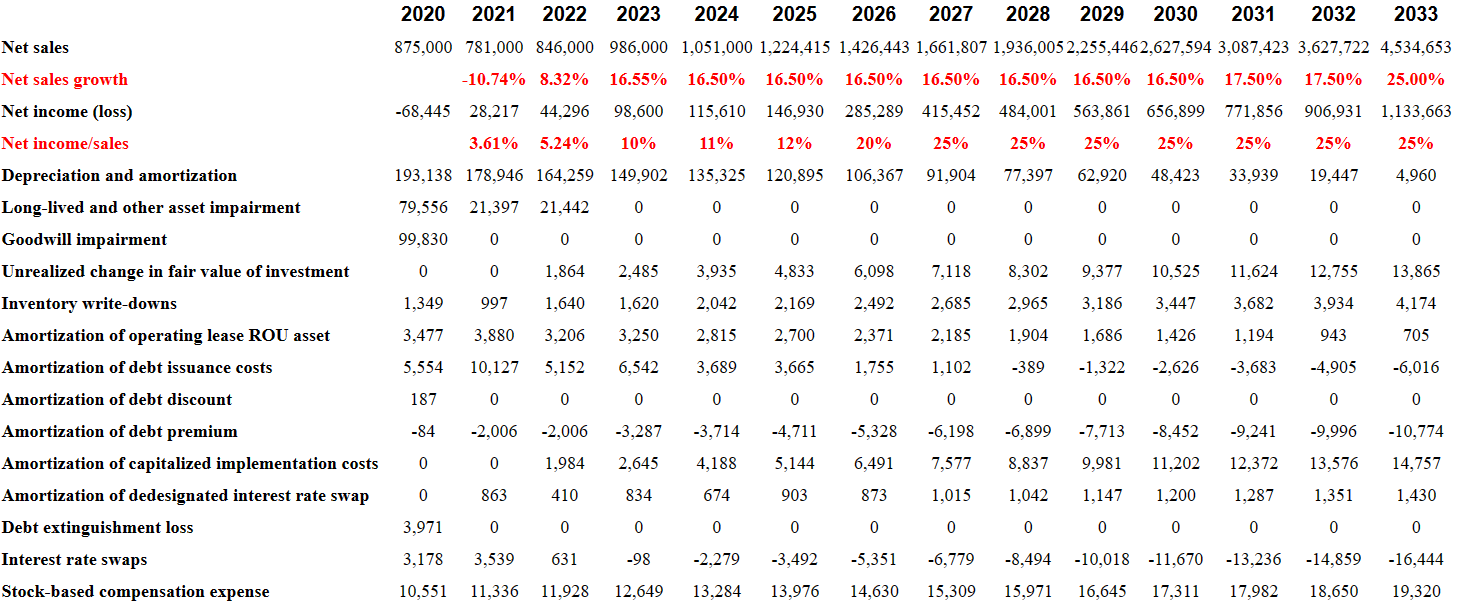

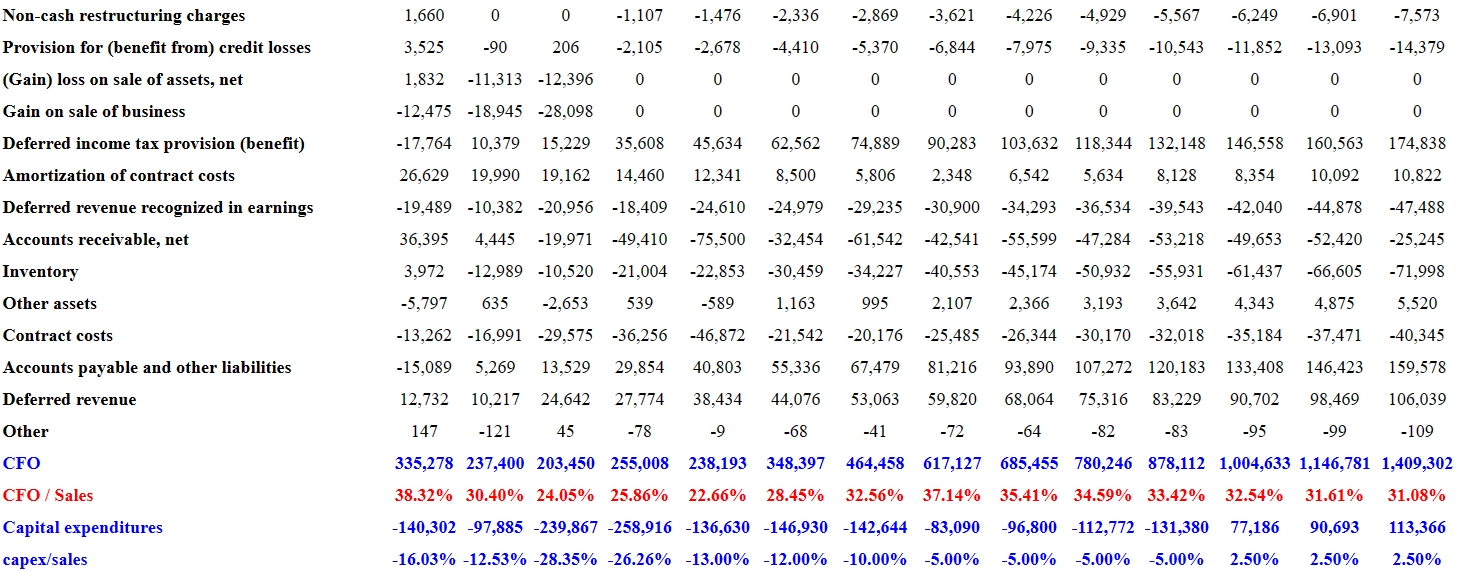

My financial model includes double digit sales growth from 2023 to 2033, growing net income/sales, decreasing D&A, no goodwill impairments, and gains in sale of businesses or assets. CFO and FCF would also increase with CFO/sales at double digit and a decrease in capex/sales. For the calculation of most variables in the cash flow statement, I used figures that are not far from the figures reported by management.

Source: Ycharts

My results include 2033 net sales close to $4.534 billion, 2033 depreciation and amortization of $4 million, unrealized change in fair value of investment close to $13 million, amortization of debt premium close to -$11 million, and 2033 stock-based compensation expense of close to $19.05 million.

{kind=link}

Other items in my cash flow model include 2033 changes in deferred revenue recognized in earnings of close to -$48.55 million, changes in accounts receivable worth -$26.5 million, changes in inventory worth -$72.55 million, and changes in contract costs close to -$41.05 million. Finally, with accounts payable and other liabilities of about $159.05 million and changes in deferred revenue of $106.05 million, 2033 CFO would be $1409.5 million.

{kind=link}

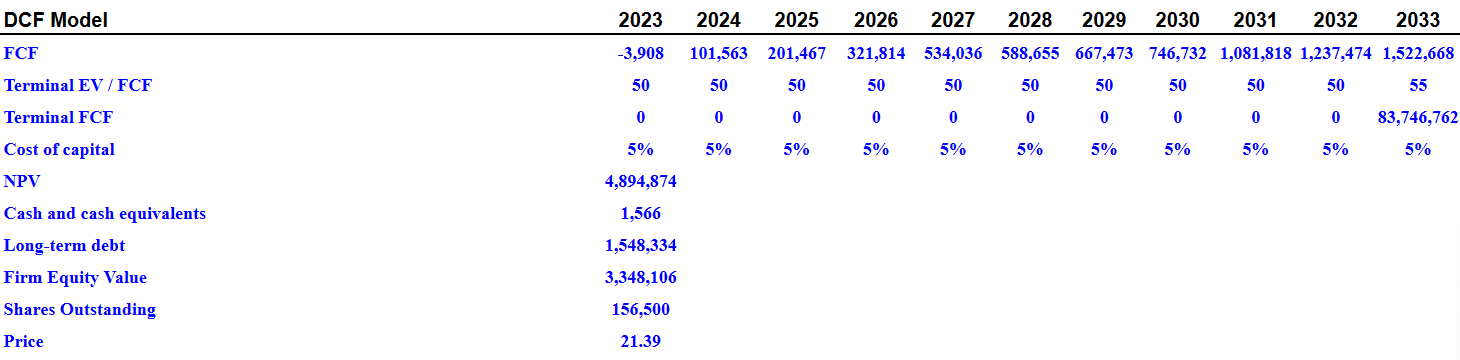

If we also include 2033 capital expenditures of about $113.55 million, 2033 FCF would stand at $1.522055 billion. If we assume EV / Terminal FCF of 55x, the net present value would be close to $4.8955 billion. If we also add cash and cash equivalents of $1.5 million with long-term debt of $1.548 billion, the firm equity value would be about $3.34855 billion. Finally, the implied price would be about $21.385 per share.

{kind=link}

Risks And Competitors

Archrock presents inherent risks, such as equipment failure, natural disasters, and gas leaks, which can result in damage, injury, contamination, and other harms. Although the company has insurance for various risks, the coverages may be insufficient to cover losses. It is self-insured for workers' compensation, employee health, and offshore property damage. In the event of significant liability not covered by insurance, the business and financial situation could be affected. Adequate attention to risks and insurance is vital to its stability.

I would also be quite concerned about further increase in operating expenses and higher pricing throughout the supply chain. As a result, we may see a decline in free cash flow, which would most likely lead to stock valuation declines. In this regard, the company made a warning in the most recent quarterly report.

Maintenance, lube oil and other operating expenses increased, driven by higher pricing throughout our supply chain, as well as increased volumes associated with unit redeployment as customer activity accelerated. Source: 10-Q

I would also expect a lot of problems if inflation continues to be a problem in 2023 and 2024. Higher wages, higher financing costs, and higher supplier prices may reduce the FCF margins, which would lead to lower stock valuation.

If inflationary pressures continue into 2023, this will increase our labor costs and the costs of parts, lube oil and other materials used in our operations. Continued inflation or an increase in inflation rates could negatively affect our profitability and cash flows, due to higher wages, higher operating costs, higher financing costs, and/or higher supplier prices. We may be unable to pass along such higher costs to our customers. Source: 10-k

In a highly competitive market with low entry barriers, the company faces constant competition from companies that are agile in technological adaptation and economic changes. The advantage of Archrock, Inc. lies in price competitiveness, equipment availability, customer service, flexibility to meet needs, technical expertise, quality, and reliability of compression packages and services.

My Takeaway

I am optimistic about deleveraging expectations. Also, I believe that more investors would most likely be interested in the new capital expenditures planned to cope with demand from clients. In addition, further increase in the average operating horsepower and horsepower utilization driven by efficiency and scalability thanks to capacity increase will most likely lead to FCF margin improvements. I do see risks from inflation, wages increase, and the debt levels, however I believe that Archrock could trade at around $20 per share soon.

For further details see:

Archrock: Recent Guidance Increase And Deleveraging Expectations