AROC - Archrock: We Have Liftoff

Summary

- After waiting four years, Archrock finally restated dividend growth in early 2023.

- Whilst their financial performance during 2022 was soft versus 2021, it should improve materially during 2023 given their guidance.

- Since they are undertaking large growth investments, they are not expected to generate any free cash flow during 2023.

- In the short term, this hinders dividend growth, but in the medium to long term, it should help as these bear fruit.

- This should unlock plenty more free cash flow to support deleveraging and further dividend growth, and thus, I believe that maintaining my buy rating is appropriate.

Introduction

It might have taken four years but Archrock ( AROC ) started 2023 on a positive note by lifting their dividends higher for the first time since 2019, thereby seeing that a new era of dividend growth is afoot, as my previous article predicted would be forthcoming given the bullish outlook for natural gas production in the United States. Now that we have lift-off, there should be even more dividend growth forthcoming in future years, as their growth investments bear fruit.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

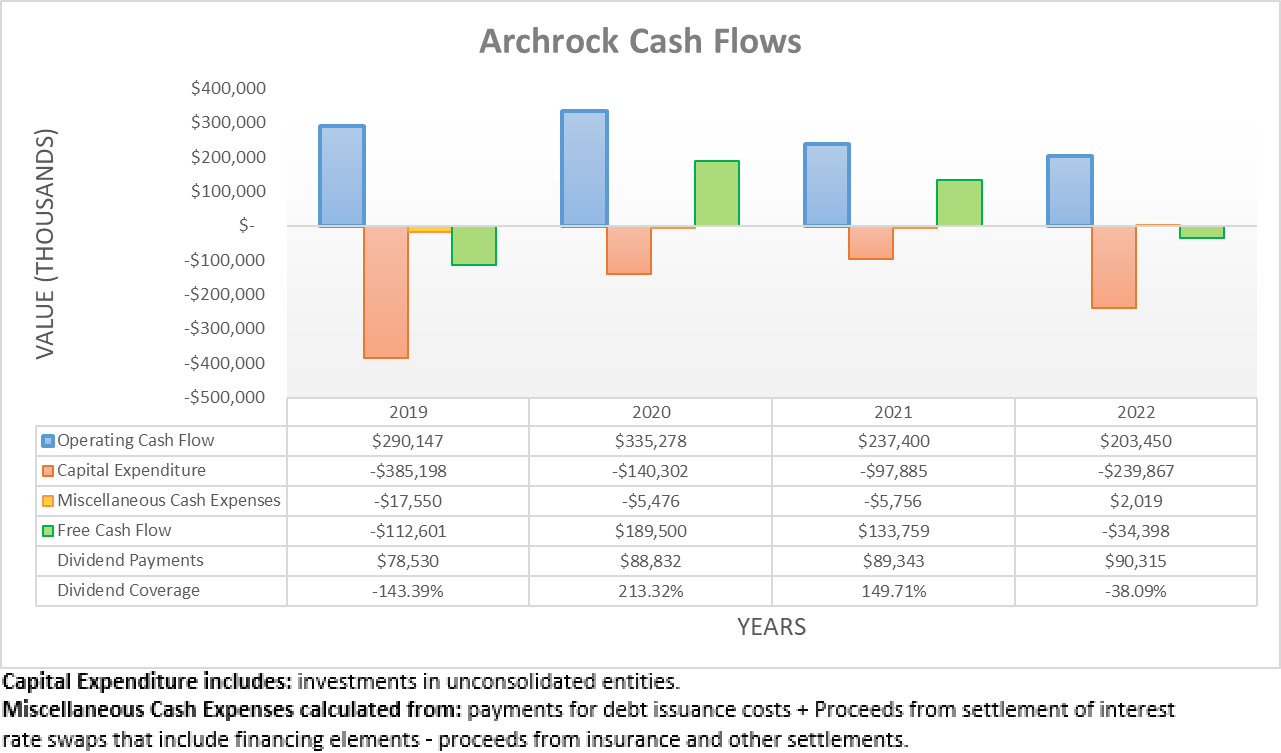

Following a soft start to 2022 with their cash flow performance down year-on-year across the first nine months, this subsequently continued throughout the fourth quarter. As a result, their operating cash flow for the full year landed at $203.5m and thus down circa 14% year-on-year versus their previous result of $237.4m during 2021. That said, at least it was down less than the circa 20% year-on-year decrease observed during the first nine months of 2022, when conducting the previous analysis.

{kind=link}

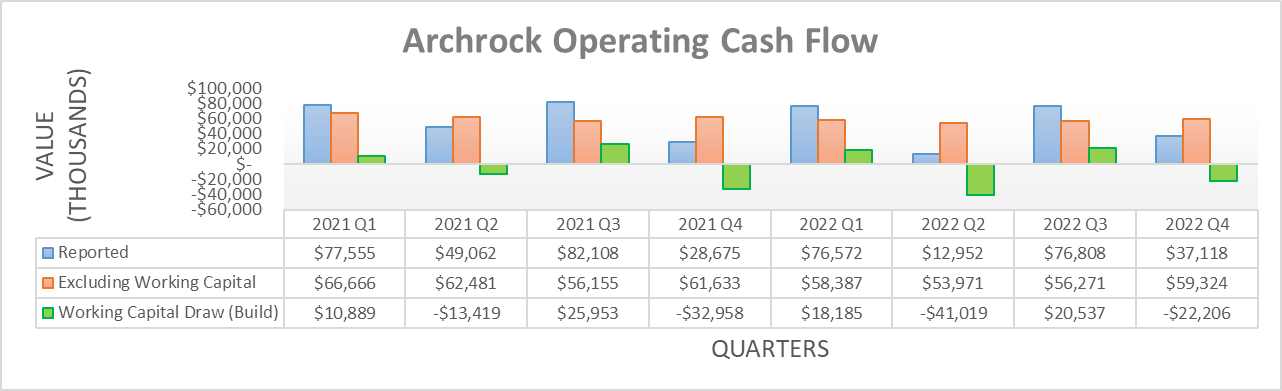

When viewed quarterly, their operating cash flow during 2022 shows a few different moving parts, the first of which being their working capital movements with a sizeable build of $22.2m during the fourth quarter alone. If aggregated with the former build and draws during the first three quarters, it sees a total build of $24.5m for the full year, which boosts their underlying operating cash flow to $228m during 2022. Applying this same process to their previous results during 2021 sees its equivalent underlying result at $246.9m and thus, regardless of their working capital movements, 2022 saw similar decreases year-on-year versus 2021. That said, it was nevertheless somewhat positive to see their underlying quarterly results increasing sequentially quarter-to-quarter during the third and fourth quarters of 2022, which hopefully foretells positive momentum heading into 2023.

Archrock Fourth Quarter Of 2022 Results Announcement

Despite their soft financial performance during 2022, at least it appears 2023 is looking strong, as my previous analysis expected would be forthcoming. When looking at their guidance for 2023, the main item is their adjusted EBITDA forecast of $415m at the midpoint, which represents an increase of circa 14% year-on-year versus their result of $363.3m during 2022, as per their fourth quarter of 2022 results announcement . In theory, this should see their underlying operating cash flow excluding working capital movements scale proportionally higher in tandem given their positive correlations and therefore, lifting it from $228m during 2022 to circa $260m during 2023.

Elsewhere, their guidance for 2023 sees growth capital expenditure of $190m, maintenance capital expenditure of $77.5m and other capital expenditure of $15m at the midpoints, as per their previously linked fourth quarter of 2022 results announcement. Once aggregated, it makes for a total of $282.5m and thus even with better-than-expected operating cash flow, it should leave little to no free cash flow during 2023. If anything, it should actually leave negative free cash flow of circa $22.5m, give or take a little and thus by default, it means very weak dividend coverage.

Even though this very weak coverage is not necessarily ideal in the short-term, the majority of their capital expenditure pertains to growth investments. As a result, in the medium to long-term these should bear fruit and thus, it stands to unlock plenty more free cash flow for dividend growth in future years, especially if they also ease back on their capital expenditure.

Next up is their dividends, which should cost $94m per annum, given their quarterly rate of $0.15 per share along with their accompanying latest outstanding share count of 156,644,485. When everything is combined, it means they should see a cash burn of circa $115m during 2023, absent of any working capital movements. Whilst this might sound concerning, it actually does not impose too significant of a cost upon their financial position.

{kind=link}

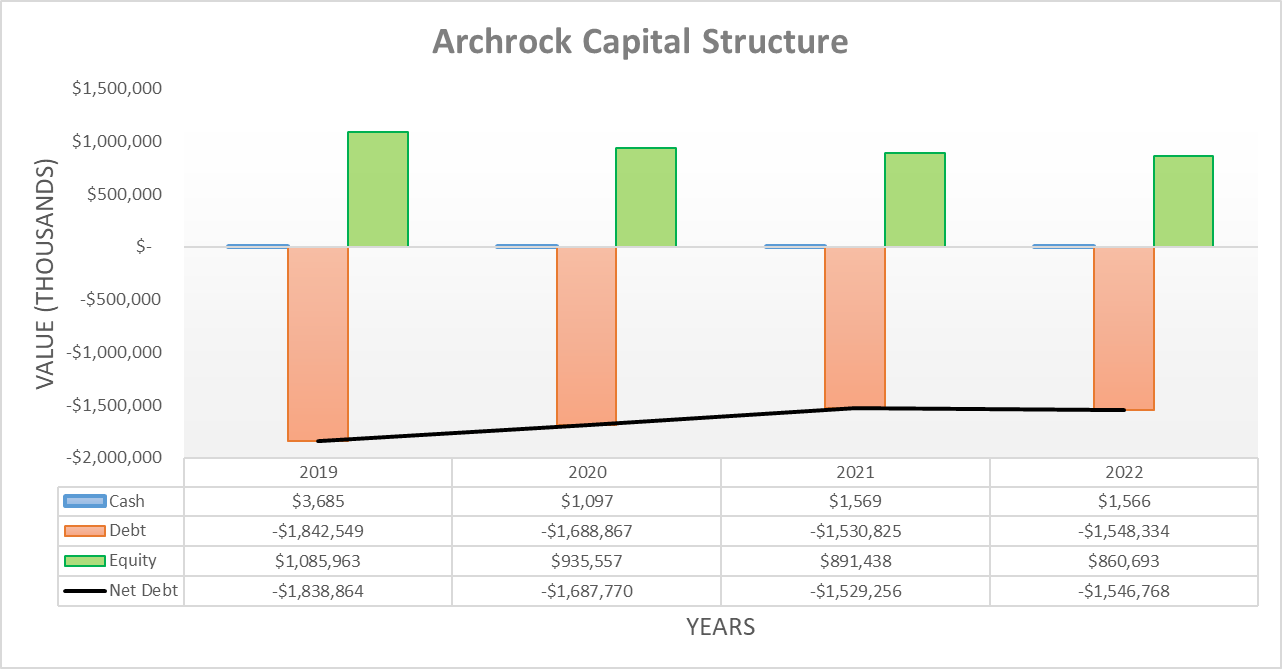

Since conducting the previous analysis following the third quarter of 2022, the subsequent fourth quarter saw their net debt climb slightly to $1.547b versus its previous level of $1.497b. Going forwards into 2023, their guidance indicates their net debt should increase by circa $115m before considering any presently unknown acquisitions, divestitures and working capital movements. If this comes to pass, it represents an increase of circa 7.50% year-on-year and thus, merely half the aforementioned forecast for their adjusted EBITDA. In theory, this means their leverage should actually improve during 2023, which lowers risks and helps facilitate further dividend growth in future years. When combined with the only small change since conducting the previous analysis, it would be redundant to reassess their leverage, debt serviceability and liquidity in detail, especially as their outlook for 2023 was the primary focus of this follow-up analysis.

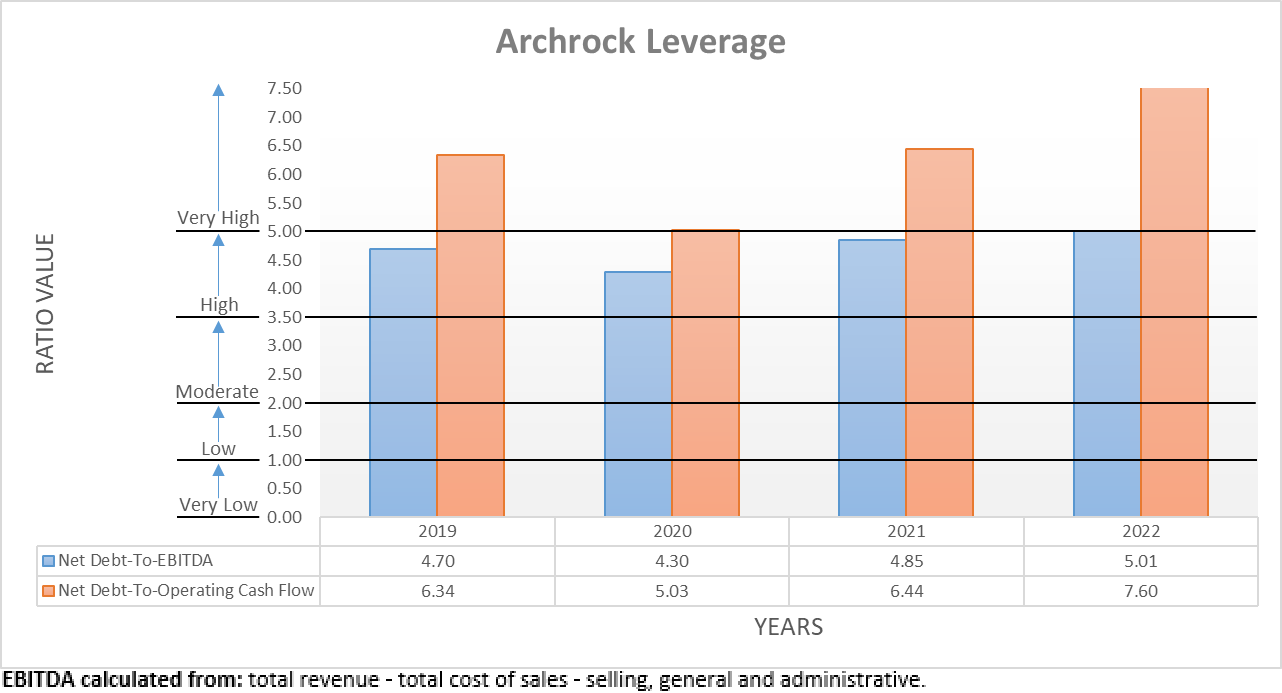

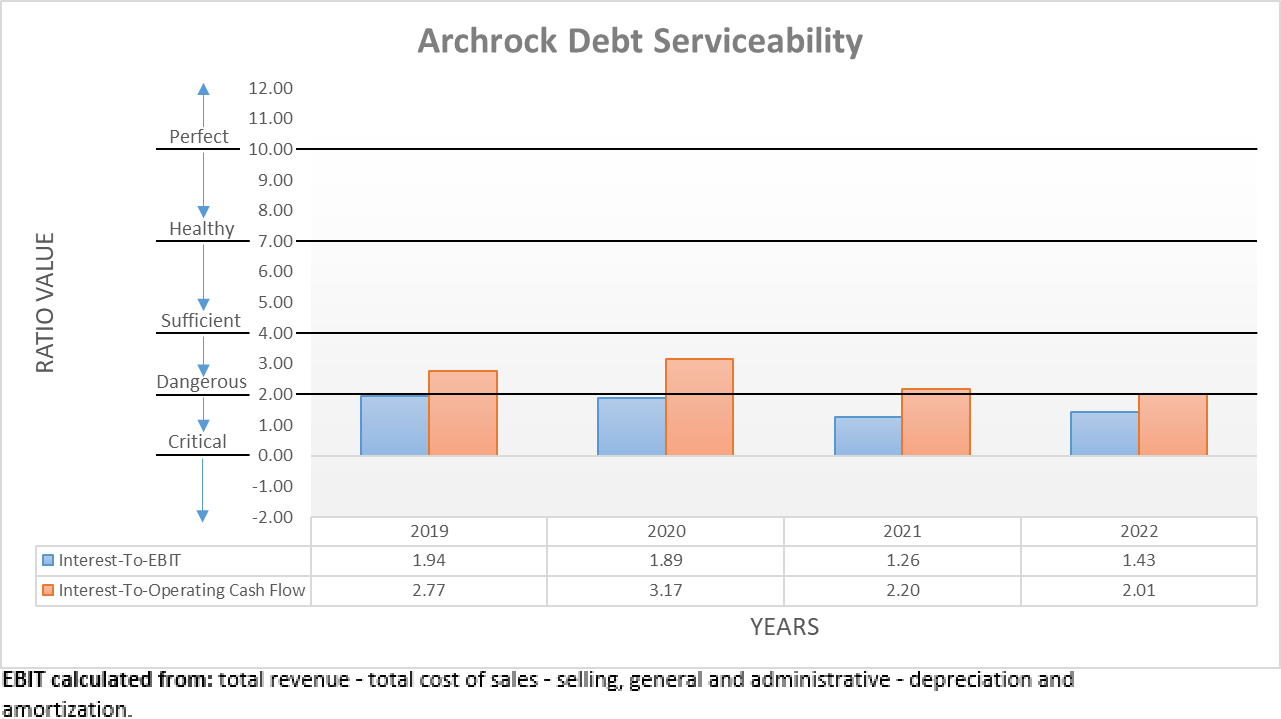

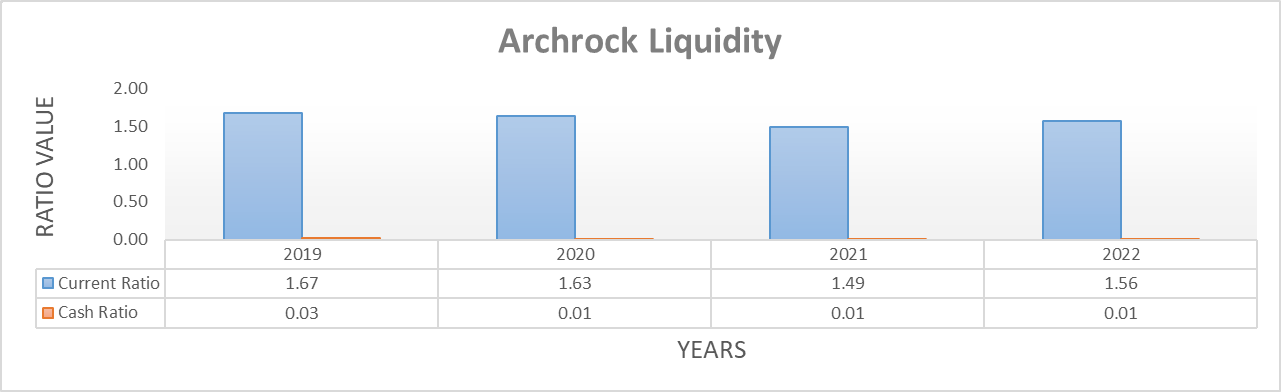

The three relevant graphs are still included below to provide context for any new readers, which shows once again their leverage in the very high territory with their net debt-to-EBITDA at 5.01 and net debt-to-operating cash flow equalling or exceeding the applicable threshold of 5.01. Concurrently, their debt serviceability also continues seeing interest coverage of 1.43 and 2.01, which remains within the range I consider dangerous. At least, they still retain adequate liquidity with a current ratio of 1.56 that helps ease risks, despite their accompanying cash ratio of only 0.01. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

Conclusion

Whilst their financial position poses hurdles for dividend growth given its very high leverage in the short-term, the improving outlook for their financial performance eases risks during 2023 as their leverage should actually improve, despite a cash burn pushing their net debt higher. Once their growth investments bear fruit in future years, it stands to unlock plenty more free cash flow to support deleveraging and further dividend growth and thus, I believe that maintaining my buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Archrock's SEC Filings , all calculated figures were performed by the author.

For further details see:

Archrock: We Have Liftoff