ACA - Arcosa: Government Spending Is A Tailwind But Valuation Is High

2023-11-03 05:56:23 ET

Summary

- Arcosa benefits from the $1 trillion Infrastructure Bill and the $370 billion Inflation Reduction Act, which management believes will create multi-year tailwinds for many of the company's businesses.

- Arcosa grew revenue and adjusted EBITDA further in the third quarter, although perhaps less than the market expected, given the stock reaction on November 2.

- In Q3, Arcosa's engineered structures segment's profitability was below management expectations.

- Although it has good growth prospects, Arcosa trades for a high valuation for the growth. It might be a 'hold' right now.

Arcosa, Inc. (ACA) is a leading provider of infrastructure related products and solutions that has benefited from increased government infrastructure spending and smart M&A in recent years. As a result, the company's stock price has increased since its IPO in 2018.

Arcosa has three business segments , construction products, engineered structures, and transportation products.

The company's construction products business makes natural and recycled aggregates, specialty materials, trench shields and shoring products. The construction products business services the infrastructure market including road bridge and other products.

Arcosa's engineered structures business produces utility structures, wind towers, telecommunication structures and more. The business serves the electricity transmission and distribution, wind power generation markets, and other markets.

The company's transportation business produces inland barges and manufactured steel products for the transportation industry.

In 2022, Arcosa's construction products had $924 million in revenues, the engineered structures business had $1.002 billion in revenues, and the transportation products business had $317 million in sales.

Government Spending

In terms of potential growth, Arcosa benefits from increased government spending such as the $1 trillion Infrastructure Bill and the $370 billion Inflation Reduction Act which management believes will create multi-year tailwinds for many of the company's businesses.

In the $1 trillion Infrastructure Bill , which became law in 2021 and allocates money over 10 years, there is $110 billion for roads, bridges, and major projects, and $42 billion for airports, ports, and waterways.

In the $370 billion Inflation Reduction Act, which also allocates money over 10 years, there is $250.6 billion in new funding to help with clean electricity and transmission.

In terms of benefits, Arcosa said in its 2022 annual report that it believes approximately half of its current portfolio of construction materials are used in infrastructure projects. For its engineered structures business, Arcosa also benefits from utilities upgrading the grid. The company also benefits from more onshore wind demand from the Inflation Reduction Act.

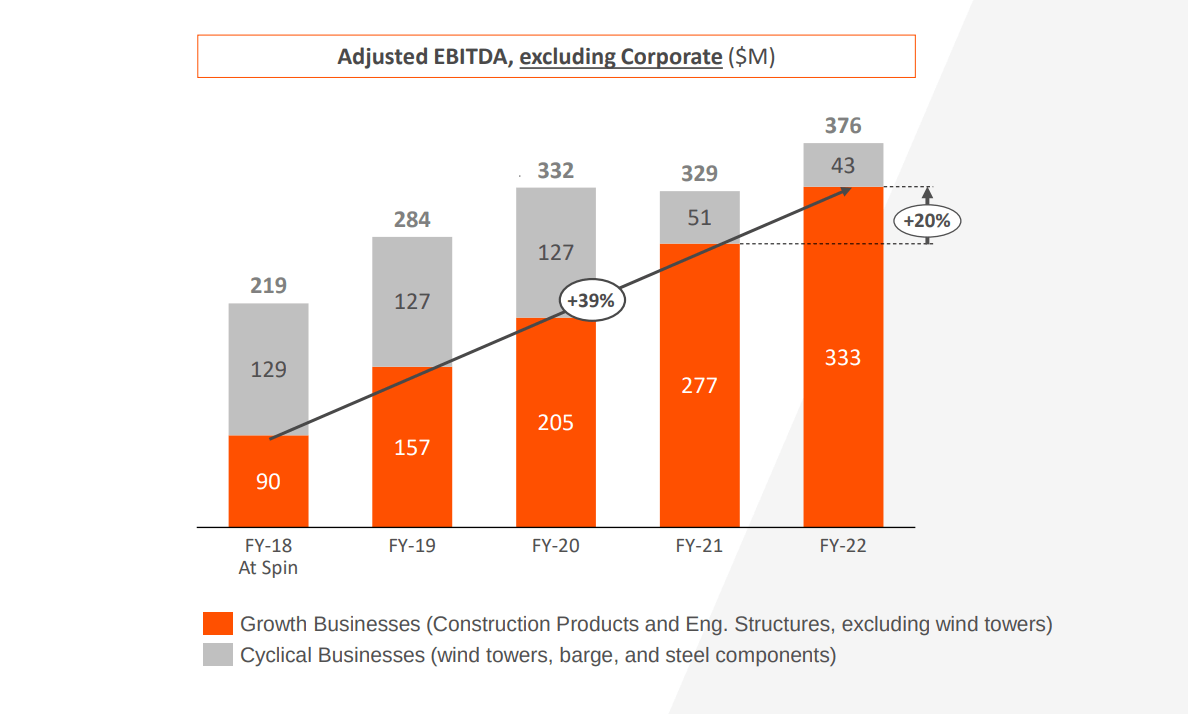

With the tailwinds and other factors, the company has grown adjusted EBITDA when excluding corporate in recent years.

{kind=link}

In terms of diluted net income per common share, however, Arcosa earned $1.54 for 2018, $2.32 in 2019, $2.18 in 2020, $1.42 in 2021, and what I calculate as $2.04 in 2022 when factoring out the pretax gain of the sale of the storage tank business ( $99 million in net income excluding the pretax gain of the sale of the storage tank business/48.5 million in diluted weighted average number of shares outstanding). As reported, the company earned $5.05 per share in 2022 but that includes the one-time gain.

So while there is pretty consistent growth in terms of adjusted EBITDA excluding corporate, Arcosa's earnings growth has been less consistent but still higher from 2018.

M&A

In terms of its segments, Arcosa's overall business composition has changed in the last several years for a company with a market capitalization of around $3.15 billion as of November 2.

With M&A, Arcosa has invested around $1.4 billion on 5 large acquisitions and multiple complementary bolt-ons to expand its construction products platform. The company also divested its storage tanks business for $275 million in October 2022.

Given its history of doing M&A, Arcosa might continue to do M&A for further growth.

In terms of recent purchases, Arcosa completed three construction products acquisitions in September and October for $41 million.

As of Q3 2023, Arcosa has a relatively solid balance sheet with net debt to adjusted EBITDA of 1 .

Q3 2023

In terms of Q3 2023 , Arcosa's revenue excluding the sale of the storage tanks business rose 10% year over year to $591.7 million, and adjusted EBITDA excluding the storage business rose 24% year over year to $89.4 million.

Adjusted EBITDA rose due to strong price momentum and reduced inflationary cost pressures.

Adjusted EBITDA margin was 15.1% versus the prior year same quarter 15%.

Adjusted diluted EPS was $0.73 for the quarter, up 4% year over year.

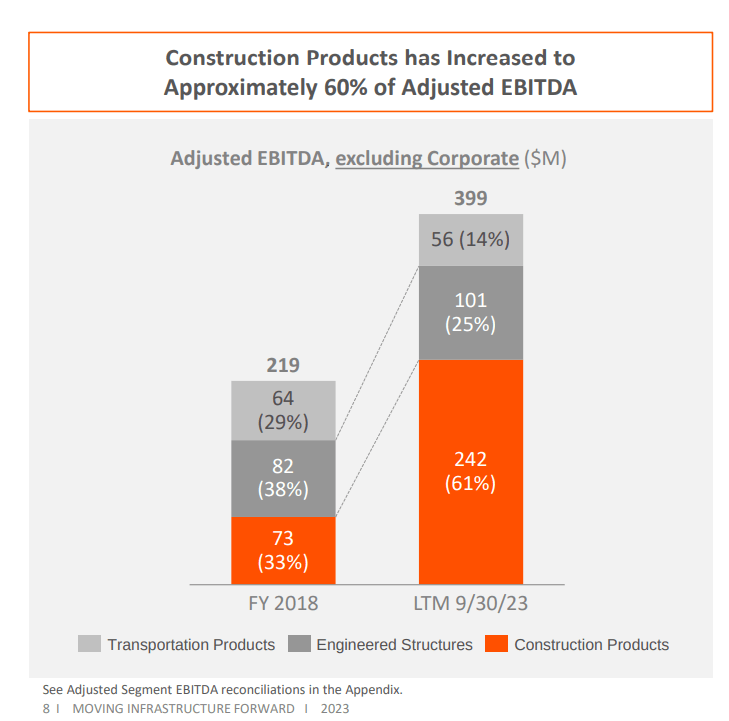

In terms of segments, Arcosa's construction products business grew 9% in terms of adjusted EBITDA growth given strong pricing and a recovery in natural aggregate volumes.

As a result of M&A and growth, the company's construction products business accounted for around 61% of adjusted EBITDA excluding corporate on a LTM basis as of 9/30/2023.

{kind=link}

For the quarter, Arcosa's engineered structures segment's profitability was below management expectations , however, given headwinds in the utility structures business such as some high margin orders delayed until 2024, unfavorable shift in production mix, unfavorable foreign exchange, and operational challenges such as equipment downtime that required outsourcing at higher costs.

Given Arcosa's pretty high valuation with a forward PE ratio of 23.11 before the earnings report, the market might have expected a better performance from the engineered structures segment and that might be one reason for the stock decline on November 2.

Hotter weather in the quarter also affected construction in places such as Texas that might have been a headwind.

In better news, management is confident in the growth outlook for its wind tower business which only serves the onshore market.

For full year 2023, Arcosa has guidance of $2.25-$2.3 billion in revenue, or an increase of 11% year over year when excluding the storage tanks business. The company also has a guidance of $355-$370 million in adjusted EBITDA versus the $278 million in adjusted EBITDA in FY2022 when excluding the storage tanks business.

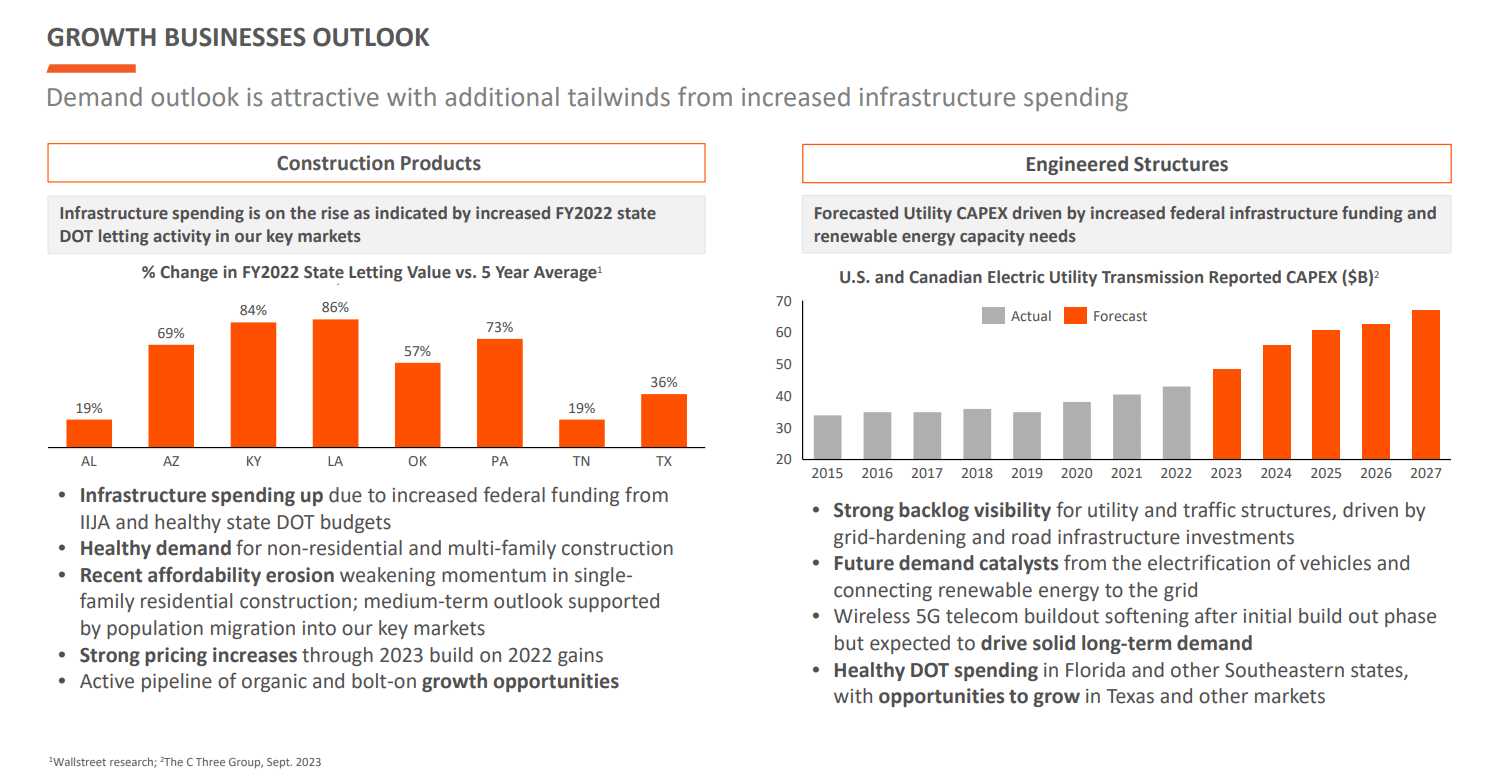

Longer term, Arcosa anticipates continuing to benefit from infrastructure spending, bolt-on growth opportunities in construction products, and growth in U.S. and Canadian electric utility transmission capex.

{kind=link}

Risks

Arcosa faces headwinds in that U.S. Treasury yields have increased over the past year and a half. The rising yields have made debt financing for M&A more expensive. So there could be less opportunity to create value and more risk.

If future M&A does not work out, it would be a headwind for margins and profits.

Higher interest rates would be a headwind for housing demand, which would in turn be a headwind for the company's construction products business.

If the U.S. Treasury yields rise too much, there could be less support for more infrastructure spending in the near term as politicians try to better control the budget deficit. Although it might be difficult, new governments might try to repeal the $1 trillion Infrastructure Bill and the $370 billion Inflation Reduction Act or at least not spend as much. If there is less spending on infrastructure, Arcosa's construction products business might face headwinds.

The company doesn't have high barriers to entry in its markets and more competition would be a headwind.

Valuation

I think Arcosa has a lot of growth potential in the future given the increased government infrastructure spending over the next decade or so. Although it is always a risk, I don't think the government in the future will cut infrastructure spending much if at all and I actually think there could be new infrastructure spending bills passed in the future.

With that said, it is hard to buy right now given the valuation. Even with the decline in November 2, the stock trades for a forward PE ratio of 21.5 given the fiscal period ending December 2023 EPS estimate of $3.01 .

With the fiscal period ending December 2024 EPS of $3.29, the forward PE multiple for the year would still be 19.7.

Given 2023 is almost over, the 2024 forward PE is probably more relevant, but it is still pretty high. Arcosa's adjusted EPS isn't growing particularly all that fast at 4% in Q3 2023 and analysts aren't expecting that fast of growth for 2024.

In the case of Arcosa, analyst estimates have usually been pretty conservative and the market has likely priced in higher earnings per share than analyst estimates given the company's history of beating analyst estimates in the majority of quarters in recent years. With one reason being higher market estimates, Arcosa beat EPS estimates by $0.05 for Q3 2023, and yet its stock still fell on November 2.

Given analysts have usually been pretty conservative, I think Arcosa will likely earn more than $3.29 per share for 2024, and as a result, the stock is trading for a lower PE valuation than 19.7 for that year.

I don't think Arcosa will earn that much more next year than analyst estimates, however, to justify the valuation as growth has been pretty slow.

The company's forward EV/EBITDA ratio of around 9.53 (according to my calculations) is also not particularly a great value versus the sector median of 10.39 as it doesn't offer that much more margin of safety.

I rate Arcosa a 'Hold' but I think there could be opportunity if the stock falls 15% or so and management does well in M&A.

For further details see:

Arcosa: Government Spending Is A Tailwind But Valuation Is High