ACA - Arcosa Q4 2022 Earnings Preview: Opinion Unchanged

Summary

- Arcosa is due to report financial data soon for the final quarter of its 2022 fiscal year.

- Results for the bulk of 2022 were encouraging, but management has been cautious about guidance.

- Shares aren't great, but they aren't bad either, but the picture hasn't improved enough to warrant an upgrade.

I don't know about you, but when I think of diverse firms, the thought of massive businesses comes to mind. I rarely imagine a company with diverse operations being a fairly small enterprise, largely because most market opportunities are big enough to allow firms to become worth billions of dollars before they run out of growth opportunities in their core space. But the fact of the matter is that there are some companies out there that are both fairly small and operationally diverse. One example of this can be seen by looking at Arcosa ( ACA ). Historically speaking, the company's operations included a Construction Products segment that provides aggregates, specialty materials, and construction site support to its clients. Its Engineered Structures segment has historically involved the production and sale of utility structures, wind towers, and storage tanks. And its Transportation Products segment has focused on the production and sale of barges and related components. Fundamentally speaking, the business seems to be doing quite well as of late. This is true both from a fundamental perspective and a share price perspective. Having said that, it does not mean that it's an ideal opportunity for investors to hop on. All those shares of the company are not outrageously priced by any means, they are a bit mixed in nature. Because of this, I still do believe that the enterprise makes for a better 'hold' candidate than a 'buy' candidate at this time, but only marginally so.

Changes, both financial and operational

In late September of 2021, I wrote an article discussing how well Arcosa had performed in the years leading up to the COVID-19 pandemic. During 2021, financial performance was a bit soft, largely as a result of broader economic issues. In some ways, I also felt that shares of the enterprise looked cheap. But in other ways, the stock looked a bit lofty. This mixed pricing, combined with the performance of the firm most recently up to that point, led me to rate it a 'hold', a rating that signified my belief that shares should generate upside or downside that would more or less match the broader market moving forward. How wrong I was. Since then, the S&P 500 has seen downside of 4.9%. By comparison, Arcosa experienced upside of 18.2%.

{kind=link}

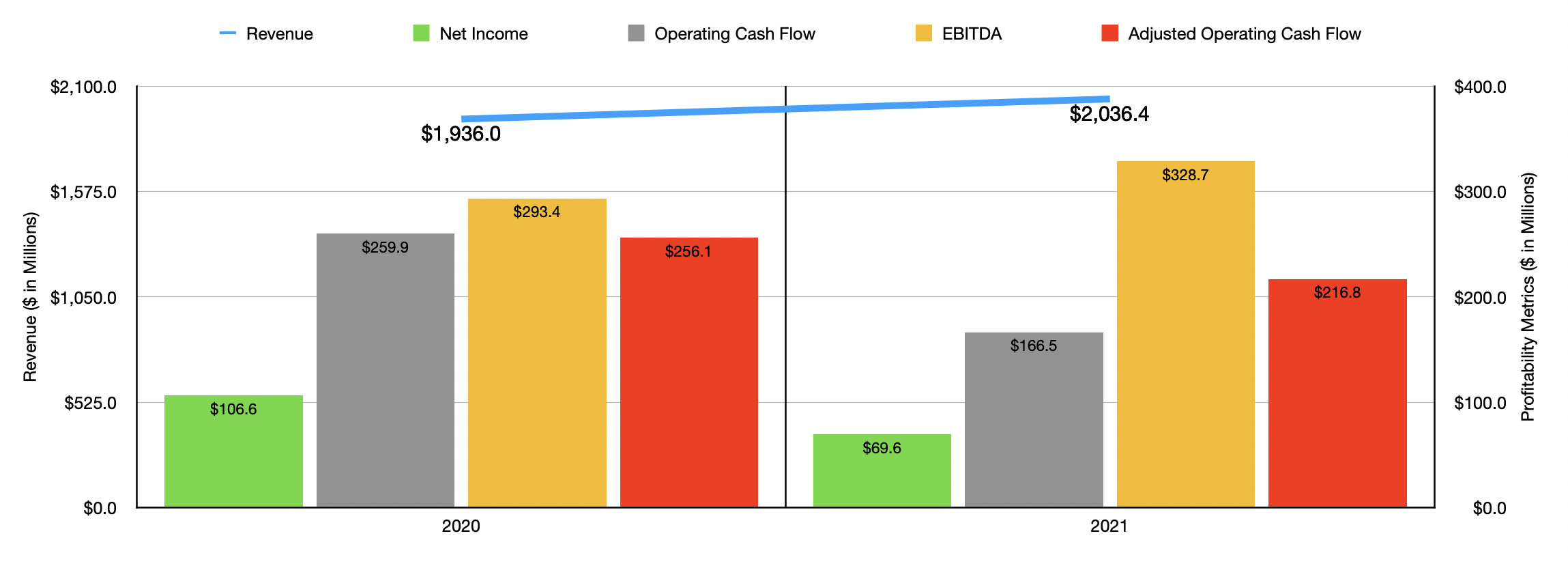

To understand exactly why Arcosa has managed to outperform the broader market, we should first look at how it finished its 2021 fiscal year . During that time, sales came in at $2.04 billion. That represents an increase of 5.2% over the $1.94 billion reported for the 2020 fiscal year. The biggest increase the company experienced during this time fell under its Construction Products segment, with sales spiking 34.2% from $593.6 million to $796.8 million. This increase, management said, was mostly due to higher natural and recycled aggregates volumes from businesses that had acquired. It also benefited from higher volumes associated with its own legacy aggregates business. Also on the rise was the Engineered Structures segment, with revenue popping 6.4% thanks to increased pricing across the board that was, in turn, driven by higher steel prices. Higher volumes in utility structures and US storage tanks also played a role here. The only weakness the company experienced was under the Transportation Products segment, with revenue plunging 34.5% because of lower volumes associated with its inland barge business.

The rise in revenue did not bring with it higher profits. Net income actually fell during this time, dropping from $106.6 million to $69.6 million. Higher operating costs in the amount of 8.1% was instrumental in driving net income down. The pain was especially bad under the Transportation Products segment, with operating profits dropping from $54.6 million to only $6.4 million. Other profitability metrics were mixed. Operating cash flow, as an example, dropped from $259.9 million down to only $166.5 million. If we adjust for changes in working capital though, the drop would have been more modest from $256.1 million to $216.8 million. On the other hand, EBITDA for the company expanded from $293.4 million to $328.7 million.

{kind=link}

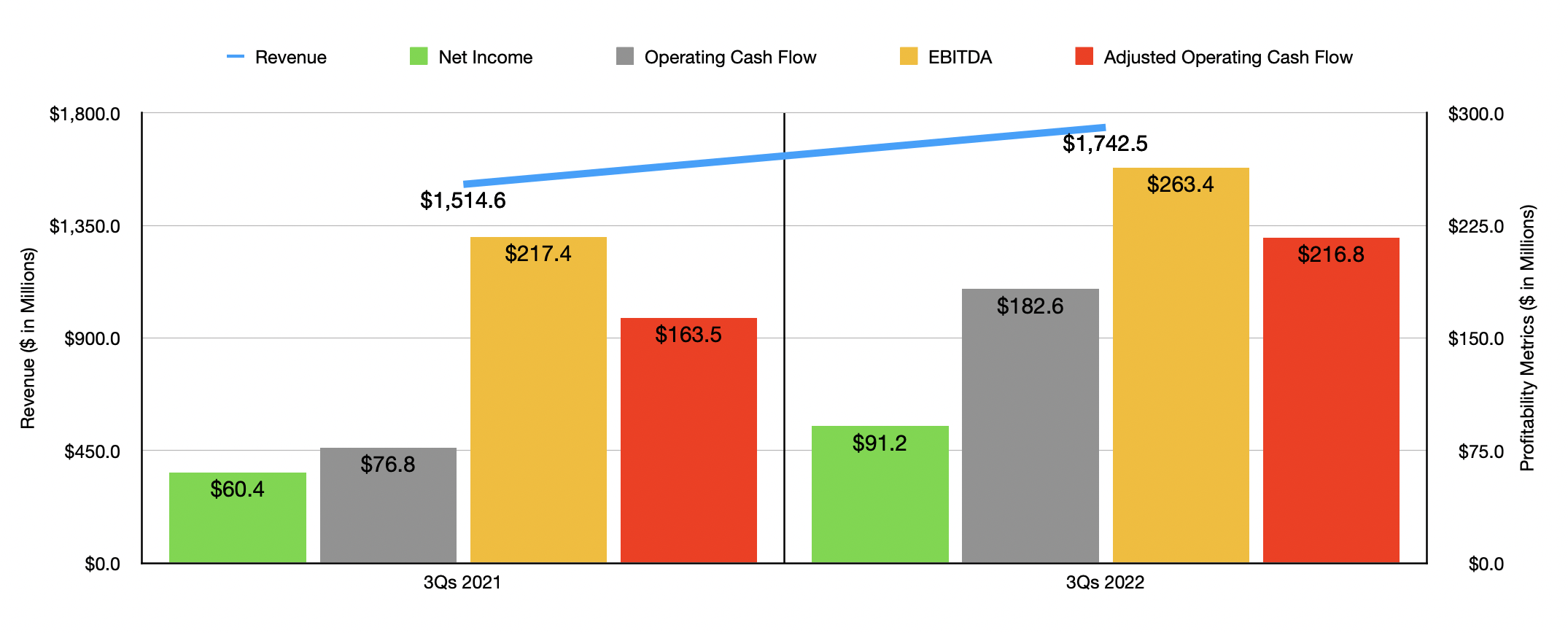

When it comes to the 2022 fiscal year, the overall picture for the company has been very positive. Revenue of $1.74 billion for the first three quarters of the year came in higher than the $1.51 billion reported one year earlier. This allowed net income to spike from $60.4 million to $91.2 million. Operating cash flow shot up from $76.8 million to $182.6 million, while the adjusted figure for this rose from $163.5 million to $216.8 million. And finally, EBITDA for the business expanded from $217.4 million to $263.4 million.

For 2022 as a whole, the picture looks a bit different than what you might think. Even though the first nine months of the year came in strong, management is forecasting some weakness in the final quarter. Total revenue for 2022 should be between $2.20 billion and $2.25 billion. This is actually down from the prior expectation of between $2.20 billion and $2.30 billion. This would imply sales in the final quarter of between $480 million and $485 million. This would be down from the $521.8 million generated in the final quarter of the firm's 2021 fiscal year. However, it would still be above the $476.1 million in revenue that analysts have forecasted for when the company reports financial results after the market closes on February 23rd. On the bottom line, management has forecasted EBITDA of between $320 million and $330 million. Previously, they were expecting this to be between $325 million and $345 million. The company did not provide any guidance when it came to earnings per share. But for context, analysts are expecting a profit of $1.19, with an adjusted profit of $0.21 per share. This adjusted profit should stack up against the $0.19 per share that the company generated one year earlier.

Some of the complexity in looking at the company and valuing it comes from the fact that management recently sold off their storage tank business. For 2022 in its entirety, Sales from this business are expected to be between $245 million and $255 million. From a profitability perspective, the expectation is for EBITDA of between $52 million and $55 million. Since we are given these numbers, I was able to go in and figure out what kind of valuation the company is trading at after factoring in this deal. I assumed that operating cash flow would change by the same amount that EBITDA is expected to change, with the one exception being that Operating cash flow should still be subjected to a 21% corporate tax rate. I also factored in the $275 million in cash that the company received in exchange for the storage tank business.

{kind=link}

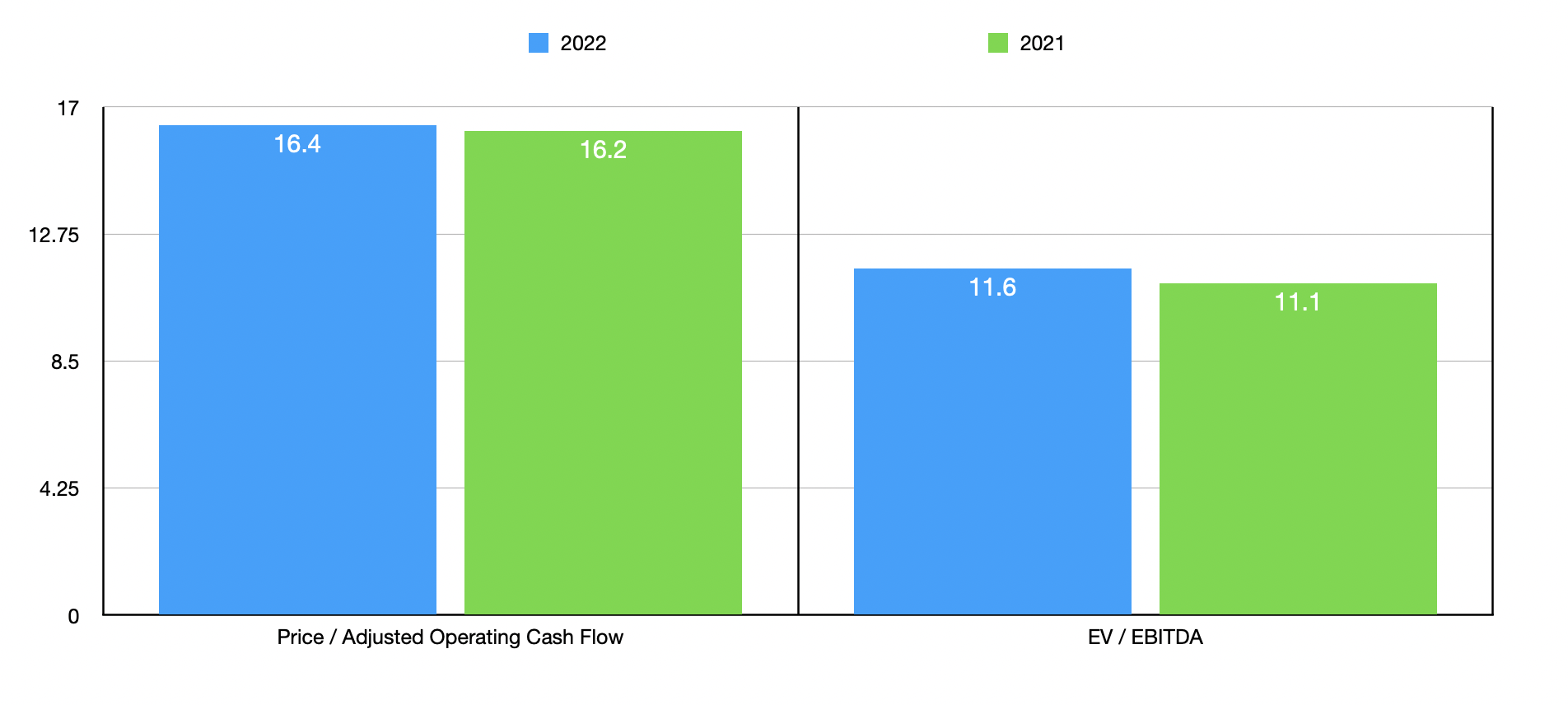

Based on these numbers, Arcosa seems to be trading at a price to adjusted operating cash flow multiple of 16.4. This is only slightly higher than the 16.2 reading that we get using data from its 2021 fiscal year. Meanwhile, the EV to EBITDA multiple should be 11.6. By comparison, using data from 2021 and making the aforementioned adjustments, the multiple would be a bit lower at 11.1. As part of my analysis, I decided to compare Arcosa to five similar firms. On a price to operating cash flow basis, the four companies with positive readings were trading at multiples ranging from a low of 16.6 to a high of 69.3. In this case, Arcosa was the cheapest of the group. Meanwhile, using the EV to EBITDA approach, the range for the five firms was between 9.9 and 18.4. In this case, two of the five firms were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Arcosa |

| 16.4 |

| 11.6 |

| Ameresco ( AMRC ) |

| N/A |

| 18.3 |

| Dycom Industries ( DY ) |

| 37.9 |

| 9.9 |

| Granite Construction ( GVA ) |

| 69.3 |

| 14.7 |

| MYR Group ( MYRG ) |

| 16.6 |

| 10.2 |

| Construction Partners ( ROAD ) |

| 34.1 |

| 18.4 |

Takeaway

Right now, Arcosa is going through a bit of a change because of the aforementioned asset sale. Economic conditions are also worrisome and I can understand why investors may decide to stay away as a result of these factors. With that in mind though, the firm is not doing all that bad. In fact, from a profitability perspective recently, I would say that it is doing quite well. In terms of valuation, the company is not the cheapest prospect I have seen. But it is definitely near the cheap end of the spectrum when stacked up against similar businesses. Because of the volatility experienced by the firm, as well as how shares are priced on an absolute basis, I cannot quite bring myself to rate the business a 'buy'. But if bottom line results do improve further and/or if the stock were to take a step back, I could see myself upgrading it to a soft 'buy'.

For further details see:

Arcosa Q4 2022 Earnings Preview: Opinion Unchanged