FWRG - Are QSR Companies Becoming Recession Resistant? We Think So And Starbucks Is Our Favorite

2023-05-30 09:42:07 ET

Summary

- The consumer sector is experiencing an interesting trend, with QSR companies performing exceptionally well while other consumer stocks face demand slowdown.

- In this article, I take a deep dive into this trend and examine the reason for QSR's outperformance during this downturn and how it is evolving into a recession-resistant industry.

- I also discuss my top pick in the industry.

Overview

There has been a lot of concern regarding consumer health recently due to high inflation and rising interest rates, and we have seen its impact in several sectors such as home improvement, building products, retail, etc. However, the Quick Service Restaurant, or QSR, industry has escaped unscathed so far. Indeed, a number of QSRs, including McDonald's ( MCD ), Starbucks ( SBUX ), Restaurant Brands ( QSR ), and Wingstop ( WING ), recently reported better-than-expected results. As we can see in the table below, in the last quarter, only YUM! Brands ( YUM ) missed the consensus EPS estimates in the QSR category, while all the other listed QSR chains reported better-than-expected EPS.

Table 1: QSR Earnings Summary (Company Data, GS Analytics Research)

| Company (Ticker) |

| Last Quarter (Reporting Date YYYY-MM-DD) |

| Earnings Summary |

| QSRs |

| McDonald's Corporation |

| Q1 2023 (2023-04-25) |

| EPS of $2.63 beats by $0.29 |

| Domino's Pizza Inc ( DPZ ) |

| Q1 2023 (2023-04-27) |

| EPS of $2.93 beats by $0.21 |

| Wendy's Co ( WEN ) |

| Q1 2023 (2023-05-10) |

| EPS of $0.21 beats by $0.01 |

| Restaurant Brands Inc |

| Q1 2023 (2023-05-02) |

| EPS of $0.75 beats by $0.11 |

| First Watch Restaurant Group Inc ( FWRG ) |

| Q1 2023 (2023-05-02) |

| EPS of $0.17 beats by $0.07 |

| Papa John's International Inc ( PZZA ) |

| Q1 2023 (2023-05-04) |

| EPS of $0.68 beats by $0.01 |

| YUM! Brands Inc |

| Q1 2023 (2023-05-03) |

| EPS of $1.06 misses by $0.07 |

| Wingstop Inc |

| Q1 2023 (2023-05-03) |

| EPS of $0.59 beats by $0.07 |

| Dutch Bros Inc ( BROS ) |

| Q1 2023 (2023-05-09) |

| EPS of $0.00 beats by $0.03 |

| Starbucks Corporation |

| Q2 2023 (2023-05-02) |

| EPS of $0.74 beats by $0.09 |

| Carrols Restaurant Group Inc ( TAST ) |

| Q1 2023 (2023-05-11) |

| EPS of $0.00 beats by $0.26 |

In this article, I have explored the factors that are contributing to the resilience of Quick Service Restaurants (QSRs) in this downturn. I have also discussed my favorite pick to capitalize on this emerging trend.

Consumer Stocks: A Tale Of Two Stories

During the recent earning season for the first fiscal quarter of 2023, consumer companies portrayed contrasting sentiments regarding the operating environment and consumer demand. On one side, QSR chains, such as McDonald's, Starbucks, Restaurant Brands, First Watch Restaurant groups, Wingstop, and Wendy's, expressed optimism about consumer behavior. These companies reported an increase in both traffic count and the number of transactions, coupled with growth in average check size, leading to strong revenue growth. This reflects a healthy consumer demand in the restaurant industry, greatly benefiting QSR chains.

On the other hand, consumer companies like Home Depot ( HD ), Lowe's ( LOW ), Amazon ( AMZN ), Target ( TGT ), P&G ( PG ), Walmart ( WMT ), and Costco ( COST ) reported a decline in consumer sentiment. In their management commentary, these companies expressed concerns about consumers scaling back on discretionary spending due to the inflationary environment. Additionally, they exhibited caution regarding consumer demand in the upcoming quarters, projecting a slowdown as consumers continue to tighten their spending.

Below, you'll find the management commentary providing insight into these diverging narratives from the latest earnings calls of these companies.

| Restaurant Companies |

| Other Consumer Companies |

| McDonald's “Let's start with the numbers. At the top line, you only need to know one number, 12.6%. US comparable sales, 12.6%, IOM comparable sales, 12.6%, IDL comparable sales, 12.6%, and global comparable sales, you guessed it, 12.6%. These results reflects strong consumer demand for McDonald's that we are seeing around the world despite a challenging operating environment and historically low consumer sentiment in many markets.” |

| Home Depot “We also saw a continuation of the trend we observed in the fourth quarter with consumers pulling back on big ticket and some discretionary type purchases.” “...we expected 2023 to be a year of moderation in the home improvement market, driven by monetary policy actions to dampen overall consumer demand. In our view, we are in a transitional period in the consumer economy.” |

| Starbucks "The company exceeded expectations in Q2 fiscal year 2023 by nearly all measures, delivering strong results across the broader Starbucks portfolio. Our performance, including continued success in the U.S. and international markets as well as the recovery we've been seeing in China can be attributed to the strength of the global brand, relevant innovation in our product and stores and powerful execution by our partners. Let me first start globally and then with both America and the U.S. Our Q2 revenue was $8.7 billion, up 14% for the prior year and up 17%, excluding more than 2% impact of foreign currency translation. North America delivered revenue growth of 17% in Q2, growing to $6.4 billion. We captured a remarkable 11% comp growth globally with 12% comp growth in both North America and the U.S. for the second quarter, driven by mid-single-digit growth balanced between transactions and ticket. Our North America growth comes on top of 12% comp growth in the prior year.” |

| Lowe’s “...we are expecting a pullback in discretionary consumer spending over the near term.” “...comparable sales were down 4.3%, partly driven by a later start to spring and a more cautious consumer. This also includes approximately 350 basis points of lumber deflation. Please note that comparable sales are calculated based on weeks 2 through 14 in fiscal 2022. Comparable average ticket was down 0.3%, largely driven by lumber deflation as ticket increased in the majority of our other merchandise divisions. Comp transactions declined 4% due to the delayed start of spring and lower-than-expected DIY discretionary sales.“ “...when we look at this topic of normalization, home improvement share of wallet, definitely seeing normalization back to services in terms of where discretionary purchases are going from consumers, travel, restaurants and a shift back to some necessity-based spend, groceries, gas, taking up a larger share of wallet given the inflation that we're seeing. But just as we look at the business at a broad level, units transactions well documented back in below, in some cases, to 2019 levels” |

| Wingstop “The momentum we saw in our business in the back half of 2022 has continued into 2023, and given us a strong start to the year. At the foundation of our strategies is people, and I couldn't be prouder of our team and brand partners who are fueling our path to becoming a top 10 global restaurant brand. In the first quarter, we delivered 20.1% same-store sales growth. Substantially, all of our comp was driven by transaction growth a true demonstration of the underlying strength of the Wingstop brand.” |

| Amazon “Across the geographies we serve, customers appreciate our focus on staying sharp on pricing, having strong selection and easier convenience, including delivery speeds, which continued to improve throughout the first quarter. That said, the uncertain economic environment and ongoing inflationary pressures continue to be a factor, and we believe it’s continuing to drive cautious spending across consumers. This means our customers are looking to stretch their budgets further and are focused on value.” “We saw moderated spending on discretionary categories as well as shifts to lower-priced items and healthy demand in everyday essentials, such as consumables and beauty.” |

| Restaurant Brands “We had a good start to the year with first quarter consolidated comparable sales growing 10.3% year-over-year, and net restaurant growth of 4.2%. This translated into global system wide sales growth of 14.7%, organic adjusted EBITDA growth of 15.6% and organic adjusted EPS growth of 22.1%. We delivered strong comparable sales in our home markets, including 15.5% growth at Tim Hortons Canada, and 8.7% at Burger King U.S. In addition to 12.3% and our Burger King International business. Popeyes U.S. grew 3.4% and Firehouse U.S. was up 6.7% for the quarter. Importantly, our top line results coupled with moderation and overall cost inflation helped drive improvements in restaurant level profitability this quarter.” |

| Target “As it did throughout last year, pressure from inflation and rising interest rates affected the mix of retail spending in Q1, with a further softening in discretionary categories in the March and April time frame. This coincided with the deterioration in consumer confidence, reflecting recent events such as the banking crisis that emerged in March.” |

| Wendy’s ( WEN ) “We delivered against our strong global same-restaurant sales expectations in the first quarter, achieving 8% growth on a 1-year basis and 10.4% growth on a 2-year basis. Our International business achieved another outstanding quarter with same-restaurant sales growth of 13.9% and an eighth consecutive quarter of double-digit same-restaurant sales growth on a 2-year basis. Our U.S. business delivered same-restaurant sales growth of 7.2%, holding our strong dollar and traffic share within the QSR burger category and widening our share gap to several competitors. These results were underpinned by the continued benefit of our strategic pricing actions alongside year-over-year customer count growth each month of the quarter.” |

| Procter & Gamble “To conclude, we continue to face highly volatile consumer and macro dynamics. We also continue to see high year-over-year input costs, inflation in the upstream supply chain and in our own operations. Headwinds from foreign exchange, geopolitical issues, and historically high inflation impacting consumer budgets.” |

| Costco “Well, I think as we talked about even the last 12 weeks ago, in the quarterly numbers, we've seen some weakness in what I'll call big-ticket discretionary items. I'm not an economist, but I think it's a combination of the economy and concerns out there as well as particularly strong numbers that we enjoyed not only a year ago but a year prior to that with COVID that we, of course, benefited in big ways with those big-ticket items.” |

| First Watch Restaurant Groups “We delivered an exceptional quarter despite the difficult March comparison we alluded to on our previous call. When we look at March and that tougher comps, I think it's important to note that we did not see a deceleration and our average weekly traffic count actually held steady throughout the quarter. Compared to pandemic highs, we did experience a softening of off-prem, similar to others in the industry. However, this was offset by growing dining room traffic as more and more people see us as a place to gather and connect with others.” |

| Walmart “At the headline level, consumer spending has proven resilient. But below the surface, we continue to see signs that customers remain choiceful, particularly in discretionary categories. In Q1, we saw a nearly 360 basis point shift in U.S. sales mix from general merchandise to grocery and health and wellness. To benchmark, the magnitude of this shift exceeds the 330 basis points of category mix shift we experienced in all of last year.” “The persistently high rates of inflation in these categories lasting for such a long period of time are weighing on some of the families we serve. This stubborn inflation in dry grocery and consumables is one of the key factors creating uncertainty for us in the back half of the year because of the cumulative impact on discretionary spending in other categories, specifically general merchandise.” |

It is evident from the management commentary of restaurant stocks and other consumer stocks that sentiment is completely contrasting. This stark difference in trends concerning discretionary spending within the same consumer base is intriguing and warrants further examination.

Three Industry Trends Driving This Tale Of Two Stories

While taking a deep-dive into what is causing the resiliency in the demand for the QSR category, I came across three major industry trends that are supporting consumer spending when it comes to eating out at QSRs. These trends include a shift in personal expenditures from products to services, market share gains during the pandemic, and consumer trade-down due to inflation.

Transition From Products to Services

During the COVID-19 pandemic, individuals found themselves confined to their homes, leading to a heightened focus on general merchandise such as televisions, electronics, kitchen appliances, and home renovations. Conversely, the demand for services experienced a decline as people were unable to partake in activities outside their homes due to travel and mobility restrictions.

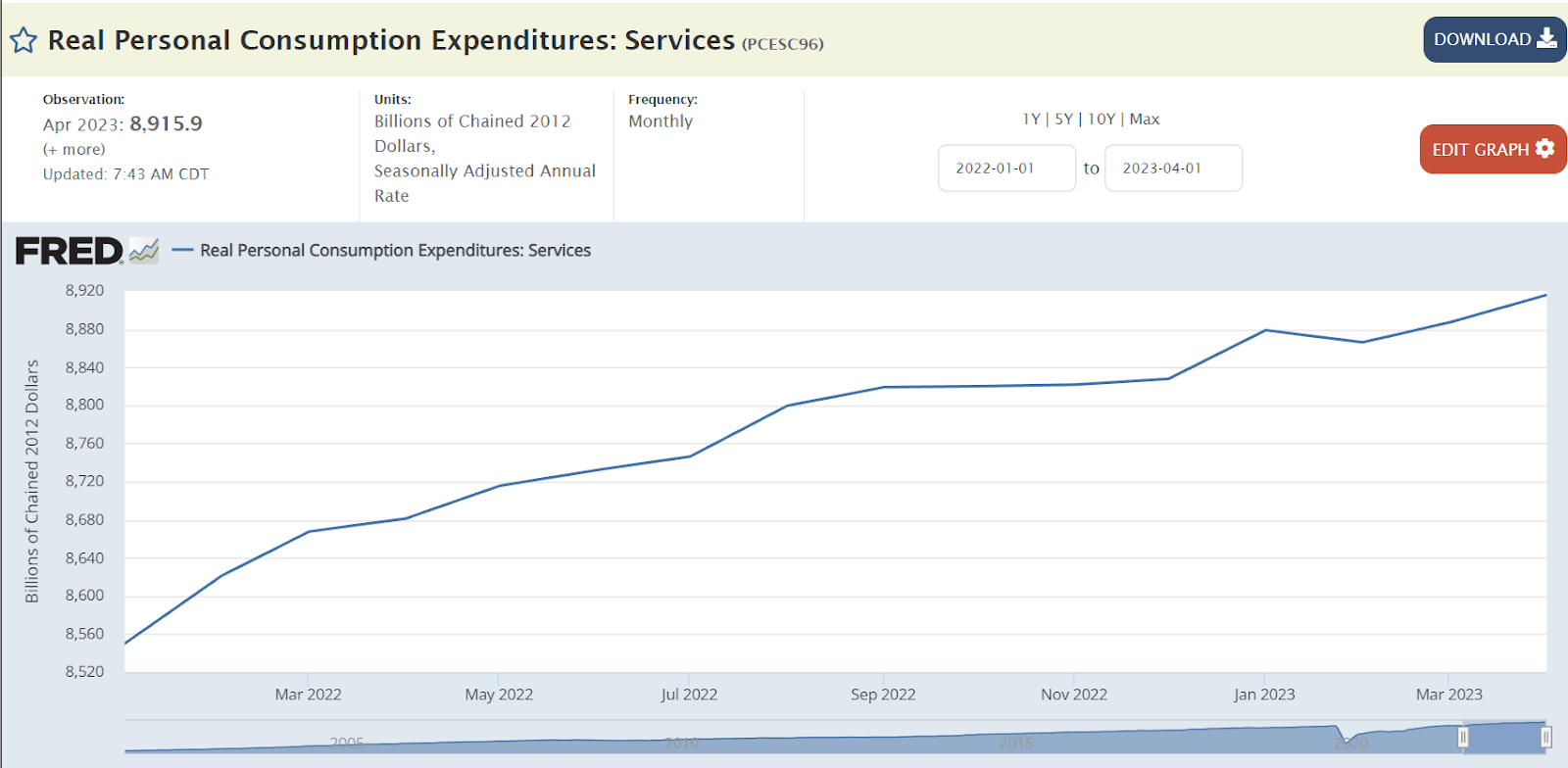

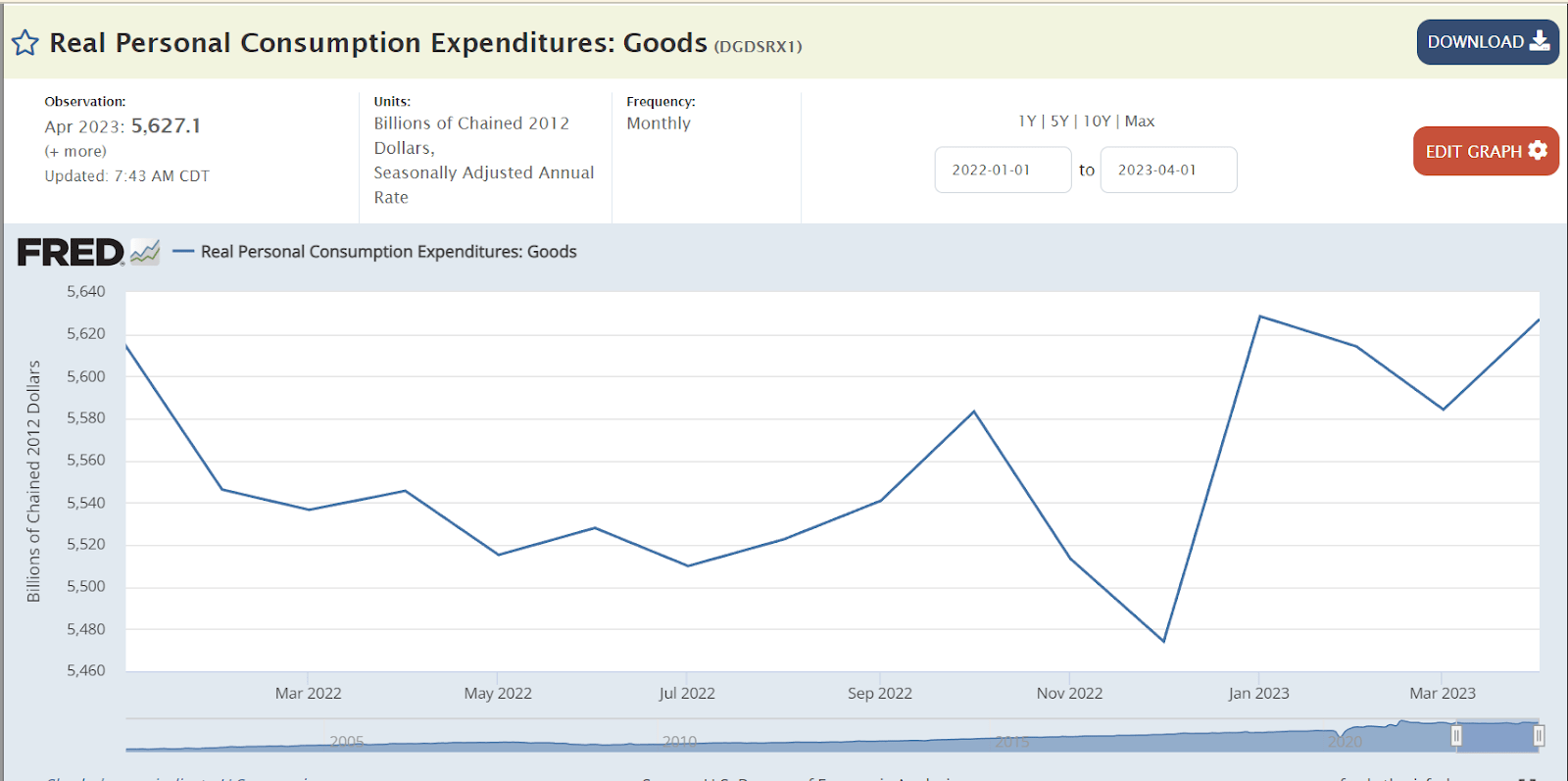

However, these mobility restrictions and lockdown measures created significant pent-up demand for services like dining in restaurants, hotel stays, and medical procedures. Consequently, as travel restrictions eased and the economy reopened, people swiftly shifted their purchasing patterns from goods to services. According to FRED, real-time personal expenditure for services has consistently increased since the beginning of 2022, while the demand for goods has remained range bound.

{kind=link}

Real Personal Consumption Expenditures: Services (FRED)

{kind=link}

Real Personal Consumption Expenditures: Goods (FRED)

This ongoing trend of shifting from goods to services is proving advantageous for the QSR industry, as an increasing number of individuals opt for dine-in food services following the reopening of the economy. Consequently, the demand for QSR companies has managed to remain resilient despite the economic downturn. One thing to note here is not all QSRs are benefiting equally. QSRs focused on Pizza are not doing that well as they already had a good presence in the delivery end-market prior to Covid and people were ordering pizza frequently during the COVID-19 lockdown. This helped their sales during that period and now they are seeing some normalization. So, as compared to Starbucks or McDonald’s where dine-in or takeaway are the bigger portion of sales, Domino’s and Papa John’s are seeing much weaker trends.

Market Share Gains

During the pandemic, safety concerns and mobility restrictions caused people to eat out less and opt for at-home dining. As a result, there was a notable decline in restaurant traffic worldwide. This particularly affected small-scale establishments compared to larger players. Larger players with better resources were able to quickly pivot to online delivery and were able to secure concessions on rental agreements which tilted the advantage in their favor.

Additionally, the implementation of hygiene and safety regulations due to COVID-19 created additional costs for restaurants. Small-scale restaurants, already experiencing declining transactions and profits, struggled to meet these new requirements. In contrast, larger restaurant chains were better equipped to handle these incremental costs due to their balance sheet strength, access to financing, and ability to maintain food hygiene and employee safety standards. Furthermore, national restaurants chains capitalized on their reputation for providing quality food and emphasized hygiene and quality in global advertising campaigns, attracting cautious consumers.

Furthermore, most of the listed QSR companies were able to provide financial support and maintain full salaries for their employees even during business slowdowns. In contrast, small-scale restaurants, with low earnings, often had to cut staff and were unable to meet employee expenses. This resulted in employees leaving their jobs, further impacting the operations of small-scale restaurants. Consequently, many small-scale and individual-owner food service businesses closed temporarily or permanently due to the effects of COVID-19.

According to an article published on ScienceDirect , the National Restaurant Association's April 2020 survey of over 6,500 restaurant operators indicated an average sales decline of 78%, resulting in a sales loss of over $30 billion in March and $50 billion in April. Full-service restaurants experienced the greatest impact, losing 83% of their customers, while limited-service restaurants faced a 61% loss. Many smaller players were not able to bear this brunt resulting in them shutting down permanently. A CNBC article reported that over 110,000 restaurants and bars closed, either temporarily or permanently, in 2020. These closures contributed to QSRs gaining market share during the pandemic and are now driving increased demand for their food services.

Consumer Trade Down In An Inflationary Environment

The increase in demand for QSR categories is not solely attributed to the pandemic, but is also being influenced by rising interest rates and high inflation. Despite the impact of inflation, consumers are still willing to spend on dine-in services and there is a pent-up demand for eating out. However, in an inflationary environment, consumers are more cautious about their budgets and seek out less expensive options for dining out. QSR chains, being more affordable compared to full-service fine dining and fast-casual restaurants, are experiencing higher traffic counts as people opt for their quick and affordable services. Thus, QSR has emerged as an affordable luxury during inflationary times and a potential choice during economic downturns. If we look at numbers, many fast-casual and full-service restaurants reported earnings miss last quarter, whereas, as discussed earlier, all QSR companies, except YUM! Brands, reported better than expected EPS.

Table 2: Fast-Casual Restaurants Earning Summary ( Based on earnings releases and Seeking Alpha Consensus Estimates)

| Company (Ticker) |

| Last Quarter (Reporting Date YYYY-MM-DD) |

| Earnings Summary |

| Fast Casual Restaurants |

| BurgerFi International Inc ( BFI ) |

| Q1 2023 (2023-05-16) |

| EPS of -$0.32 misses by $0.08 |

| Shake Shack Inc ( SHAK ) |

| Q1 2023 (2023-05-04) |

| EPS of -$0.01 beats by $0.07 |

| Sweetgreen Inc ( SG ) |

| Q1 2023 (2023-05-04) |

| EPS of -$0.17 beats by $0.08 |

| Chipotle Mexican Grill Inc ( CMG ) |

| Q1 2023 (2023-04-25) |

| EPS of $10.50 beats by $1.55 |

| FAT Brands Inc ( FAT ) |

| Q1 2023 (2023-05-08) |

| EPS of -$1.95 misses by $0.91 |

| Fiesta Restaurant Group Inc (FRGI) |

| Q1 2023 (2023-05-10) |

| EPS of -$0.08 misses by $0.10 |

| Jack in the Box Inc ( JACK ) |

| Q2 2023 (2023-05-17) |

| EPS of $1.47 beats by $0.25 |

| Potbelly Corp ( PBPB ) |

| Q1 2023 (2023-05-04) |

| EPS of $0.02 misses by $0.01 |

Table 3: Full-Service Restaurants Earning Summary (Based on earnings releases and Seeking Alpha Consensus Estimates)

| Company (Ticker) |

| Last Quarter (Reporting Date YYYY-MM-DD) |

| Earnings Summary |

| Casual Dining Restaurants |

| Cracker Barrel Old Country Store Inc ( CBRL ) |

| Q3 2023 (2023-06-06) |

| Result will be declared on June 6th |

| Darden Restaurants Inc ( DRI ) |

| Q3 2023 (2023-03-23) |

| EPS of $2.36 beats by $0.12 |

| Brinker International Inc ( EAT ) |

| Q3 2023 (2023-05-03) |

| EPS of $1.23 beats by $0.03 |

| Dine Brands Global Inc ( DIN ) |

| Q1 2023 (2023-05-03) |

| EPS of $1.97 beats by $0.27 |

| BJ's Restaurants Inc ( BJRI ) |

| Q1 2023 (2023-04-27) |

| EPS of $0.15 beats by $0.11 |

| Texas Roadhouse Inc ( TXRH ) |

| Q1 2023 (2023-05-04) |

| EPS of $1.28 misses by $0.08 |

| Denny's Corporation ( DENN ) |

| Q1 2023 (2023-05-02) |

| EPS of $0.13 misses by $0.01 |

| Red Robin Gourmet Burgers Inc ( RRGB ) |

| Q4 2022 (2023-02-28) |

| EPS of -$1.35 misses by $0.73 |

| Bloomin' Brands Inc ( BLMN ) |

| Q1 2023 (2023-04-28) |

| EPS of $0.98 beats by $0.09 |

| Cheesecake Factory Inc ( CAKE ) |

| Q1 2023 (2023-05-10) |

| EPS of $0.61 beats by $0.02 |

| Kura Sushi USA Inc ( KRUS ) |

| Q2 2023 (2023-04-04) |

| EPS of -$0.10 beats by $0.12 |

| Fine Dining Restaurants |

| Ruth's Hospitality Group Inc ( RUTH ) |

| Q1 2023 (2023-05-08) |

| EPS of $0.35 misses by $0.02 |

| Polished Casual |

| ONE Group Hospitality Inc ( STKS ) |

| Q1 2023 (2023-05-04) |

| EPS of $0.08 misses by $0.01 |

These consumer trends, driven by convenience, affordability, and trade-down behavior, are paving the way for the QSR category to exhibit resilience during economic downturns compared to other restaurant category. Based on these trends, there is reason to be optimistic about the future growth of the QSR category, as it is expected to outperform other consumer stocks.

So, How To Invest In This Trend?

Since I am bullish on QSR companies and the factors I discussed above are expected to boost the sales of most of these companies, I tried to find ETFs that provide good exposure to QSR companies and the restaurant industry in general. However, I encountered a problem with most of the low-cost, larger ETFs that have exposure to the restaurant sector. Most of them also have exposure to categories that are not expected to do as well. For example, the Consumer Discretionary Select Sector SPDR Fund ( XLY ) also includes exposure to other discretionary categories like home improvement products, which are expected to see a slowdown.

There is one pure-play restaurant ETF - the Advisor Shares Restaurant ETF ( EAT Z ) - which offers decent exposure to the QSR industry. However, it is not low-cost, has a limited track record and was launched in April 2021, and has a very low assets under management ((AUM)). Its top holding is Arcos Darados Holding Inc Class A ( ARCO ), which operates McDonald’s franchises in Latin America. Interestingly, its top 10 holdings do not include the two biggest QSR giants, McDonald’s and Starbucks. Based on my experience, investing in brands usually offers better long-term risk-return prospects than investing in their franchises. Considering the limited track record, high expense rates, and current holdings, I don't believe EATZ is a good proxy to capitalize on the dynamics of the QSR industry. Therefore, a better way to participate in this trend is by investing in individual QSR companies.

Starbucks: My Favorite Pick Despite All the Noise Around Unionization

After conducting a deep-dive of various QSR companies' prospects, I found one stock that stands out as a potential winner and could provide good returns in the future - Starbucks. Many investors are concerned about recent discussions around unionization, resulting in the stock trading at a significant discount compared to its historical levels. This presents an opportunity to buy the stock at a lower price.

While there have been increased instances of union strikes and disruptions in industries such as Hollywood and airlines like Southwest Airlines ( LUV ), I don't believe there is a significant threat from unionization at Starbucks. Please note that I am not someone who outright dismisses these risks, as I understand how unionization can harm a business. In a previous article , I advised caution with UPS ( UPS ) until their negotiations with the Teamsters Union concluded, as I identified a significant risk there.

However, it is crucial to evaluate each case individually, and in the case of Starbucks, it is much more challenging for a union to have sufficient bargaining power compared to the powerful Teamsters Union, which consists of full-time truck drivers dedicated to their profession long-term. SBUX baristas, for the most part, work for a few years to fund their college or other expenses and do not typically plan to work in this job until retirement, unlike LUV pilots, Hollywood writers, or Teamsters drivers, although there may be exceptions based on individual circumstances. The work of baristas is not as stressful as that of truck drivers, and these baristas are easily replaceable, especially after the post-COVID reopening. Additionally, the company provides decent pay, with an average wage of around $17.50 per hour and a total compensation of $27 per hour when considering benefits.

Despite some stores unionizing, they have not been successful in negotiating a bargaining agreement with the management thus far due to the reasons mentioned above. Given that the company already offers competitive compensation, it does not face significant reputational risks by not entertaining union demands. Furthermore, a recent survey indicated that its sales are unlikely to be impacted, regardless of whether the company reaches an understanding with its employees attempting to unionize or not.

SBUX: Revenue Outlook

The company's business is thriving, and it has promising prospects for revenue growth and margin expansion. Over the past year, SBUX has experienced revenue growth driven by the heightened demand for services and dining out following the impact of COVID-19. Additionally, Starbucks has capitalized on its reputation as a socializing and connecting hub, further contributing to its revenue growth.

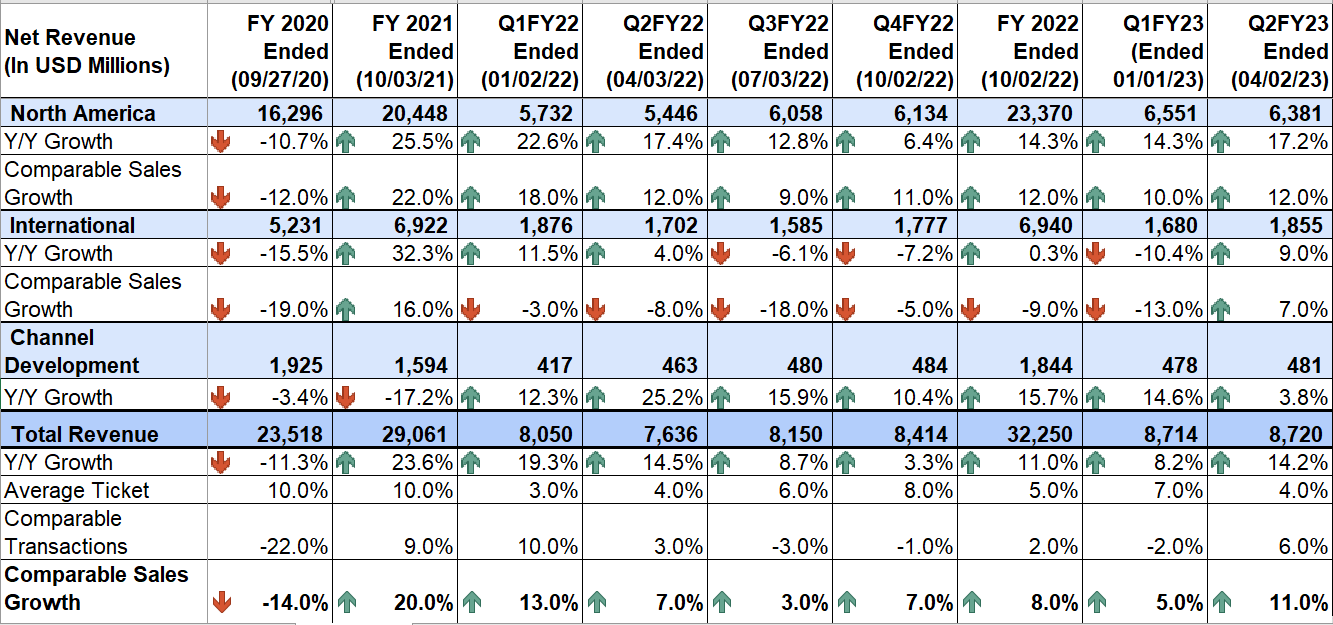

In the second quarter of fiscal 2023, SBUX sustained its growth momentum. The company witnessed an increase in guest traffic, indicating strong demand. Furthermore, it achieved favorable average check growth due to a rise in food attach rate (the proportion of food items included with beverage orders) and implemented price increases. SBUX also benefited from a better-than-expected recovery in China, where its stores experienced a boost in traffic count. Consequently, the company delivered a notable 14.2% year-over-year increase in revenue, reaching $8.7 billion. On a comparable store basis, SBUX's revenue grew by 11% year over year, with a 4% contribution from average check growth and a 6% contribution from an increase in transactions.

{kind=link}

SBUX’s Historical Revenue (Company Data, GS Analytics Research)

Looking ahead, I anticipate that Starbucks will continue to deliver revenue growth driven by several factors like the increase in consumer demand, the recovery of China, expanding store count globally, and the popularity of Starbucks as a socializing and connecting hub. Starbucks restaurants are well-known for providing a welcoming atmosphere, making them a preferred destination for people to meet and socialize, particularly for business meetings. With the economy reopening and business meetings resuming, Starbucks' traffic is expected to experience significant growth.

The company should also see similar trends in China, the second-largest market for Starbucks, as it reopens. With the country recovering from the long-lasting disruptions caused by the pandemic, I expect similar industry trends to play out there, including the transition from products to services and market share gains resulting from COVID-related closures of small-scale restaurants. Additionally, as China emerges from the pandemic and people become more immune to COVID infections, there will be a growing need for socialization, further supporting revenue growth in the region.

The company should also benefit from its new offerings. The demand for SBUX's cold and customized beverages is expected to benefit the company and is resonating well with young consumers, particularly Gen Z, who have a preference for customized and cold beverages over traditional coffee. To meet this demand, Starbucks introduced handheld cold foam blenders, which enhance customization options. This focus on customization and innovation gives Starbucks a competitive edge and can help gain market share. In addition to customized offerings, the company's new beverage innovations, such as the Oleato line, have gained significant traction and increased demand. This expansion of product offerings, coupled with successful global launches, contributes to sustaining demand and driving revenue growth.

Another key driver of revenue growth is Starbucks' reward membership program, which enhances customer engagement and loyalty. The program allows customers to earn "Stars" for their Starbucks e-card recharge, which can be redeemed for free drinks in the future. This incentivizes customers to spend on their Starbucks e-card, driving transaction growth and customer loyalty. The expansion of the reward membership program in licensed franchise stores further enhances customer engagement and transaction growth.

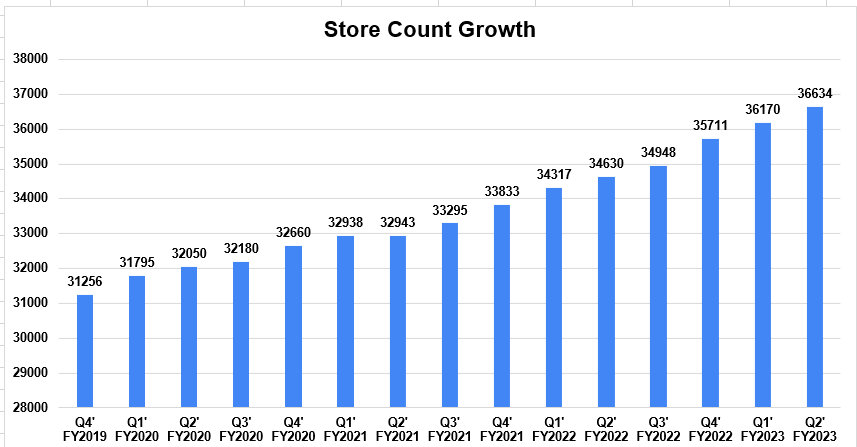

Lastly, the company's continuous expansion of its restaurant footprint is a good catalyst for revenue growth. Starbucks is consistently adding new stores, providing greater convenience and accessibility to the customers availing its food and beverage services. In the second quarter of fiscal 2023, Starbucks opened 464 net new stores, representing a 6% year-over-year growth to reach a total of 36,634 stores. The international store count increased by 8% YoY to 19,152, with a target of reaching 20,000 international stores by the end of fiscal 2023.

{kind=link}

SBUX’s Historical Store Count Growth (Company Data, GS Analytics Research)

Considering these factors, I believe that Starbucks is well-positioned for revenue growth in the coming quarters, supported by industry trends, the recovery of China, customized cold beverage offerings, new product launches, increasing customer engagement through the reward membership program, and expanding store count globally.

SBUX: Margin Outlook

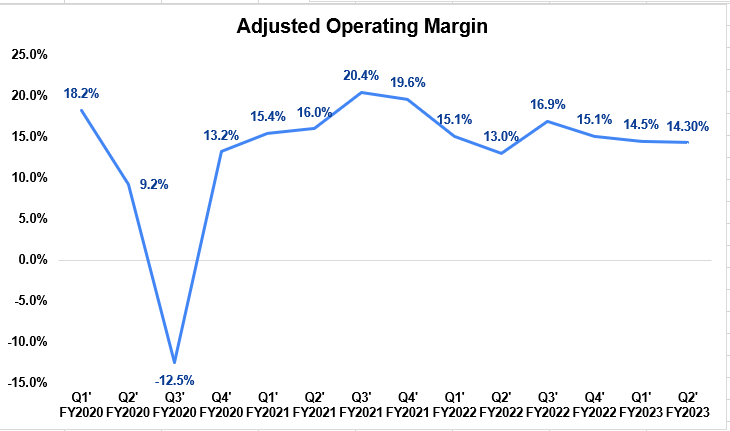

The company’s margin prospects also look good. In the second quarter of fiscal 2023, SBUX experienced margin growth driven by various factors. The company benefited from sales leverage, thanks to better-than-expected sales growth in China, cost savings, pricing initiatives, and productivity gains. Additionally, SBUX no longer incurred incremental costs associated with Omicron compared to the previous year's quarter. Furthermore, a margin benefit of approximately 60 basis points was captured in the quarter due to the re-evaluation of Starbucks Rewards liability.

These factors collectively led to a year-over-year increase of 130 basis points in adjusted operating margin, reaching 14.3%. In the North American segment, the operating margin saw a significant increase of 200 basis points year over year, reaching 19.2%. Meanwhile, the international segment experienced an even greater increase of 390 basis points year over year, resulting in an operating margin of 17%.

{kind=link}

SBUX’s Historical Adjusted Operating Margin (Company Data, GS Analytics Research)

Moving forward, SBUX operating margin should continue to improve. As we progress into the second half of fiscal 2023 and beyond, the further recovery of the Chinese market and overall revenue growth will contribute to increased sales leverage, supporting margin expansion. SBUX remains focused on driving productivity and cost-saving measures to further enhance margins.

In the second quarter of fiscal 2023, SBUX saw a reduction in barista turnover, leading to fewer new hires per store and lower hiring and training costs. The company has also made progress in optimizing partner (barista) scheduling hours, resulting in a 4% year-over-year increase in average hours per barista per week. This metric is important as it aligns with the company's goal of providing appropriate compensation to its partners and can have positive implications in the current unionization matters. Improved pay for baristas, coupled with productivity gains in operations, benefits the company overall.

SBUX is also focusing on technology and automation to improve partner scheduling and reduce workloads. The rollout of Clover Vertica brewers, which brew coffee more efficiently, began in the second quarter of fiscal 2023 and is expected to be available in nearly 40% of company-operated stores across the U.S. by the end of the fiscal year. This implementation will improve operational efficiency, saving partners time and allowing them to focus more on customer engagement.

Considering these productivity gains and cost-saving initiatives, I hold an optimistic outlook for margin growth in the coming quarters. SBUX's focus on enhancing operational efficiency, reducing costs, and sustainability efforts should continue to drive margin expansion moving forward.

SBUX: Valuations

As of now, SBUX's forward P/E ratios stand at 28.65x for FY23 and 23.97x for FY24, based on consensus EPS estimates of $3.44 and $4.11, respectively. In my view, the recent correction in stock price due to unionization concerns and conservative guidance has made SBUX even more attractive when compared to its historical 5-year average P/E ratio of 35.51x. Given the company's strong revenue growth prospects in the coming years, driven by factors such as its ability to attract people for socializing in a post-COVID era, industry trends supporting demand, new store growth, customer loyalty through Starbucks reward membership, and prospects for margin improvement, I believe the stock deserves a higher valuation and has the potential to outperform in the future. This makes it an attractive investment opportunity, especially considering its current lower-than-historical valuation.

Do Share Your Perspective

Other than SBUX, there are additional opportunities in the QSR segment, as well as the broader restaurant industry, with numerous companies showcasing strong financial performance, while their stocks trade at a discount compared to historical levels. We will be conducting a comprehensive analysis of these companies individually over the upcoming weeks, and we welcome your thoughts in the comments section regarding your preferred stocks among QSR companies. If there is a restaurant company you would like us to cover, please feel free to share the name.

For further details see:

Are QSR Companies Becoming Recession Resistant? We Think So And Starbucks Is Our Favorite