GAINZ - Ares Capital's NAV Valuation And Dividend Vs. 14 BDC Peers - Part 2 (Includes Q1 + Q2 2024 Dividend Projection)

2023-12-19 23:31:11 ET

Summary

- Part 2 of this article compares ARCC’s recent dividend per share rates, yield percentages, and several other highly detailed (and useful) dividend sustainability metrics to 14 other BDC peers.

- This includes a comparative analysis of ARCC’s cumulative undistributed taxable income ratio, percentage of floating-rate debt investments, recent weighted average annualized yield, and weighted average interest rate on outstanding borrowings.

- Ares Capital's dividend sustainability remains one of the highest in the sector. When comparing/analyzing all metrics (including additional metrics not mentioned), ARCC is currently deemed to be slightly undervalued (Buy).

- Simply put, contrary to recent speculation, ARCC’s dividend remains very safe. In addition, the possibility of a special periodic dividend continues to exist.

- Most BDCs will continue to have sustainable-slightly growing (and some special periodic) dividends over the foreseeable future. However, credit risk will rise heading into 2024 (something I will continually monitor/model).

Focus of Article:

The focus of this two-part article is a very detailed analysis comparing Ares Capital ( ARCC ) to some of the company's business development company ("BDC") peers (all sector peers I currently fully cover). I am writing this two-part article due to the continued requests that such an analysis be specifically performed on ARCC and some of the company's BDC peers at periodic intervals. For readers who just want the summarized conclusions/results, I would suggest scrolling down to the "Conclusions Drawn" section at the bottom of each part of the article.

PART 1 of this article analyzed ARCC's recent quarterly results and compared several of the company's metrics to 14 other BDC peers. PART 1 helps lead to a better understanding of the topics and analysis that will be discussed in PART 2. The link to PART 1's analysis is provided below:

REIT Forum Version (Expanded Analytics/Sorted Tables):

Public Version:

PART 2 of this article compares ARCC's recent dividend per share rates, yield percentages, and several other highly unique dividend sustainability metrics to 14 other BDC peers. This analysis will show recent past data with supporting documentation within Table 3 below. This article will also provide ARCC's dividend sustainability projection for the calendar first and second quarters of 2024 which is partially based on the metrics shown in Table 3 and several additional metrics shown in Table 4 below.

By analyzing these metrics, one will better understand which BDC generally has a safer dividend rate going forward versus other peers who have a higher risk for a dividend decrease or a higher probability of a dividend increase and/or a special periodic dividend being declared. This is not the only data that should be examined to initiate a position within a particular stock/sector or project future dividend per share rates. However, I believe this analysis would be a good "starting point" to begin a discussion on the topic. At the end of this article, there will be a conclusion regarding various comparisons between ARCC and the 14 other BDC peers. In addition, I will provide my current BUY, SELL, or HOLD recommendation and price target on ARCC. Dividend projections for the calendar first quarter of 2024 (or next set of dividend declarations) and excess taxable income balances for the other 14 BDC peers are exclusive to our subscribers.

Side Note: As of 12/15/2023, MidCap Financial Investment Corp. ( MFIC ), ARCC, Oaktree Specialty Lending Corp. ( OCSL ), FS KKR Capital Corp. ( FSK ), Gladstone Investment Corp. ( GAIN ), Golub Capital BDC Inc. ( GBDC ), SLR Investment Corp. ( SLRC ), BlackRock TCP Capital Corp. ( TCPC ), Sixth Street Specialty Lending Inc. ( TSLX ), Capital Southwest ( CSWC ), PennantPark Floating Rate Capital ( PFLT ), and TriplePoint Venture Growth ( TPVG ) had a stock price that "reset" lower regarding each company's regular monthly/quarterly dividend accrual. In other words, this company's "ex-dividend date" has occurred. In addition, OCSL, FSK, GAIN, GBDC, TCPC, TSLX, CSWC, and Blue Owl Capital Corp. ( OBDC ) (formerly ORCC) had a stock price that reset lower regarding each company's special periodic dividend accrual. Main Street Capital ( MAIN ), Prospect Capital Corp. ( PSEC ), and OBDC had a stock price that had not reset lower regarding each company's regular December 2023 monthly/quarterly dividend accrual. MAIN had a stock price that has not reset lower regarding the company's special periodic dividend accrual. Readers should take this into consideration as the analysis is presented below.

Dividend Per Share Rates and Yield Percentages Analysis - Overview:

Let us start this analysis by first getting accustomed to the information provided in Table 3 below. This will be beneficial when comparing ARCC to the 14 other BDC peers regarding quarterly dividend per share rates and yield percentages.

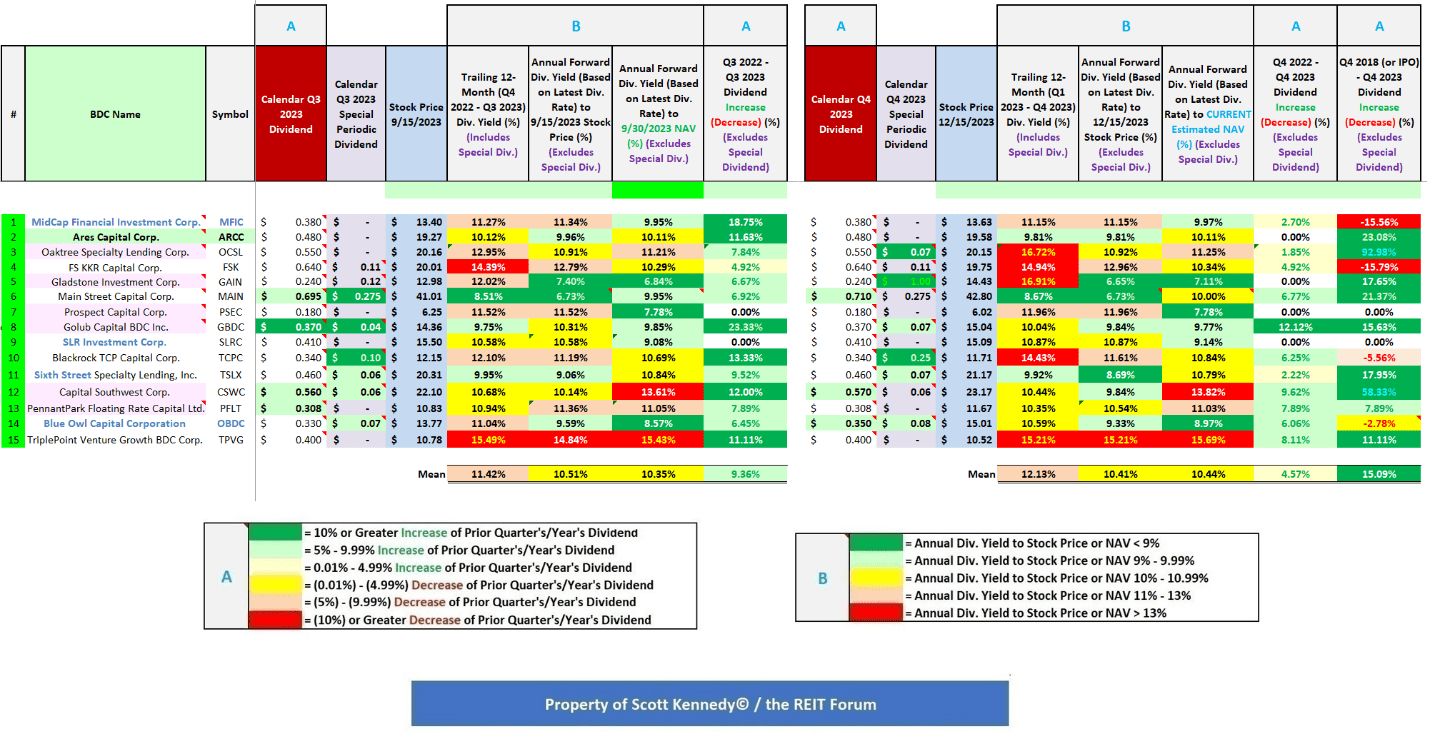

Table 3 - Dividend Per Share Rates and Yield Percentages

{kind=link}

(Source: Table created entirely by myself, obtaining historical stock prices from NASDAQ and each company's dividend per share rates from the SEC's EDGAR Database )

Using Table 3 above as a reference, the following information is presented in regards to ARCC and 14 other BDC peers (see each corresponding column): 1) dividend per share rate for the calendar third quarter of 2023 (including any special periodic dividend) ; 2) stock price as of 9/15/2023 ; 3) trailing 12-month ("TTM") dividend yield (dividend per share rate from the calendar fourth quarter of 2022 - third quarter of 2023 [includes all special periodic dividends]) ; 4) annual forward dividend yield based on the dividend per share rate for the calendar third quarter of 2023 using the stock price as of 9/15/2023 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 5) annual forward dividend yield based on the dividend per share rate for the calendar third quarter of 2023 using the NAV as of 9/30/2023 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 6 ) TTM dividend increase (decrease) percentage (for monthly dividend payers, dividend per share rate fluctuation from September 2022 - September 2023) ; 7) dividend per share rate for the calendar fourth quarter of 2023 (including any special periodic dividend) ; 8) stock price as of 12/15/2023 ; 9) TTM dividend yield (dividend per share rate from the calendar first quarter of 2023 - fourth quarter of 2023 [includes all special periodic dividends]) ; 10) annual forward dividend yield based on the dividend per share rate for the calendar fourth quarter of 2023 using the stock price as of 12/15/2023 (for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 11) annual forward dividend yield based on the dividend per share rate for the calendar fourth quarter of 2023 using my projected CURRENT NAV (NAV as of 12/15/2023; for monthly dividend payers, the latest monthly dividend per share rate during the quarter) ; 12) TTM dividend increase (decrease) percentage (for monthly dividend payers, dividend per share rate fluctuation from December 2022 - December 2023) ; and 13) 5-year dividend increase (decrease) percentage (for monthly dividend payers, dividend per share rate fluctuation from December 2018 - December 2023). Let us now begin the comparative analysis between ARCC and the 14 other BDC peers.

Analysis of ARCC:

Using Table 3 above as a reference, ARCC declared a dividend of $0.48 per share for the third quarter of 2023. This was an unchanged dividend when compared to the prior quarter. ARCC's stock price traded at $19.27 per share on 9/15/2023. When calculated, this was a TTM dividend yield (including special periodic dividends when applicable) of 10.12%, an annual forward yield to ARCC's stock price as of 9/15/2023 of 9.96%, and an annual forward yield to the company's NAV as of 9/30/2023 of 10.11%. When comparing each yield percentage to ARCC's BDC peers within this analysis, the company's TTM yield based on its stock price as of 9/15/2023 was modestly (at or greater than 1.00% but less than 2.00%) below average, the company's annual forward yield based on its stock price as of 9/15/2023 was slightly (at or greater than 0.50% but less than 1.00%) below average, and its annual forward yield to my projected CURRENT NAV was near (less than 0.50%) average.

When combining this type of data with various other analytical metrics, I correctly projected ARCC had a very high (90%) probability of a stable-modestly increasing dividend per share rate for the fourth quarter of 2023 (which ultimately came to fruition).

To provide readers with several additional, important metrics to consider regarding each BDC's dividend sustainability, Table 4 is provided below. Again, it should be noted there are additional dividend sustainability metrics that I perform for each company. However, those metrics are more elaborate in detail and require additional analysis/discussion which I believe is beyond the scope of this particular article. That type of analysis would be better suited when analyzing each company on a "standalone" basis versus a sector comparison article. I have discussed some of these more elaborate metrics in prior ARCC, GAIN, MAIN, NewtekOne (NEWT), OCSL, PSEC, SLRC, and TSLX articles (see my profile page for links to prior articles regarding those companies).

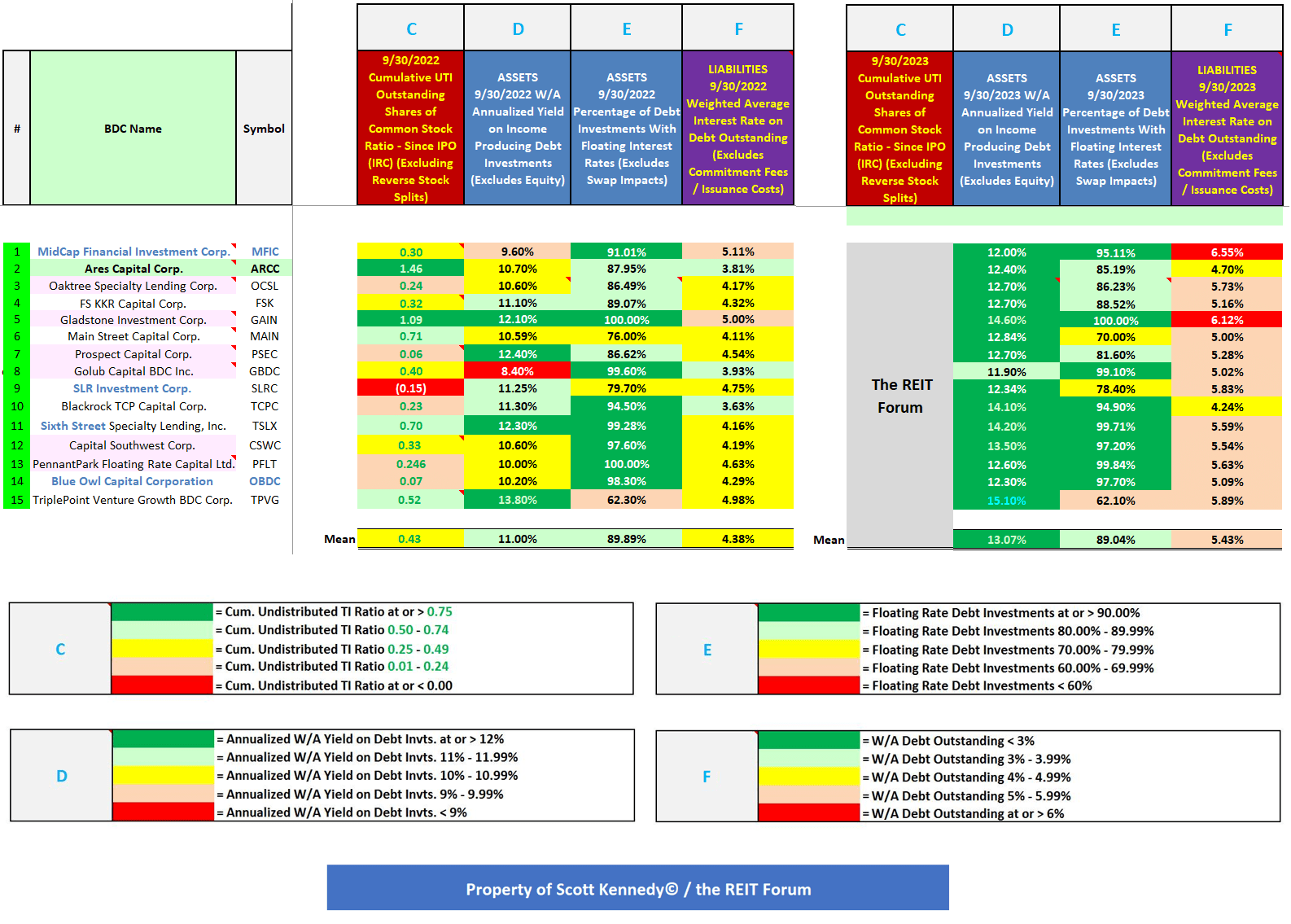

Table 4 - Several Additional Dividend Sustainability Metrics (9/30/2023 Versus 9/30/2022)

{kind=link}

(Source: Table created entirely by myself, partially using data obtained from the SEC's EDGAR Database [link provided below Table 3])

Using Table 4 above as a reference, a very important metric to consider regarding a BDC's long-term dividend sustainability is each company's cumulative undistributable taxable income ("UTI") outstanding shares of common stock ratio (highly valuable "forward-looking" data). Cumulative UTI is "built up" /retained net investment company taxable income ("ICTI") in excess of previously paid dividend distributions since an entity's initial public offering ("IPO") or after the most recent tax year when an entity overdistributed its ICTI with no such surplus to offset the difference. This figure/metric has been covered, at length, in previous BDC dividend sustainability articles. To calculate this ratio, I take a company's cumulative UTI and divide this amount by its outstanding shares of common stock . The higher this ratio is, the more positive the results regarding a company's future dividend sustainability. Since most BDC peers have continued to gradually net increase their outstanding shares of common stock, this ratio shows if a company has been able to increase its cumulative UTI balance by a similar proportion.

ARCC had a cumulative UTI coverage of outstanding shares of common stock ratio of 1.35 as of 9/30/2023 (see blue reference "C" ). When calculated, this was a (0.11) decrease during the TTM (nothing alarming). Simply put, ARCC continued to have a notable net ICTI surplus to distribute over the foreseeable future. ARCC's ratio, both as of 9/30/2022 and 9/30/2023, was notably more attractive versus the mean of 0.43 and 0.46 of the 15 BDC peers within this analysis, respectively.

ARCC has had the highest ratio throughout the trailing 12 months by a fairly large margin. This remains a very positive catalyst/trend to consider and, in my opinion, one of the main reasons why ARCC typically trades at a modest premium to CURRENT NAV.

In addition, I would point out ARCC has not decreased the company's dividend per share rate since the second quarter of 2009. Yes, that is correct. ARCC has not reduced the company's quarterly dividend per share rate for 14+ years (while periodically declaring minor special periodic dividends). During this time, ARCC has increased the company's dividend from $0.3447 per share to $0.48 per share. I believe the company should be "rewarded" per se, from a valuation standpoint, for not having to decrease its dividend for such a long time (and continued to increase its dividend).

For example, since the fourth quarter of 2018, MFIC, FSK, TCPC, and OBDC have declared a net decrease to each company's dividend (excluding any current special periodic dividends) of (16%), (16%), (6%), and (3%), respectively (includes accounting for MFIC's and FSK's reverse stock split of 1:3 and 1:4, respectively; excludes special periodic dividend classifications). I believe that is a very important point to consider. In addition, ARCC's management team continues to imply the company's current quarterly regular dividend per share rate, at worst, will remain unchanged over the foreseeable future (currently at $0.48 per share). There remains the fair high - high probability for minor - modest gradual increases to ARCC's quarterly dividend and/or minor special periodic dividends being declared over the foreseeable future (beyond 2023) to release some of the company's notable cumulative UTI balance (to remain in compliance with the Internal Revenue Code ("IRC").

In my opinion, another important metric to consider regarding a BDC's dividend sustainability is a company's weighted average annualized yield on its debt investments (asset side of the balance sheet). ARCC had a weighted average annualized yield on the company's debt investments of 12.40% as of 9/30/2023 (see blue reference "D" ). This percentage remained slightly below the mean of 13.07% of the 15 BDC peers within this analysis. ARCC's weighted average annualized yield on the company's debt investments increased 1.70% during the TTM without any material change in portfolio characteristics. Outside a couple of BDC outliers, this was fairly consistent with the overall trend within the BDC sector due to the recent very quick increase in the U.S. London Interbank Offered Rate ("LIBOR")/Standard Overnight Financing Rate ("SOFR")/PRIME (various debt investments "reset" higher) partially offset by a notable tightening of spreads over the past several years (new originations during 2019 - early 2022 at lower effective interest rates when compared to prepaid/repaid/sold debt investments). This metric should begin to plateau during the fourth quarter of 2023 - early 2024 before slightly declining during 2024. In addition, it should be noted the higher LIBOR/SOFR/PRIME rises, the more underlying credit risk (non-accruals) needs to be respected (and monitored). This will have heightened importance as we head into 2024.

Taking a look back to prior historical trends for this specific metric, prior to the early 2020 coronavirus (COVID-19) sell-off/panic, there was some 2019 "spread/yield compression" due to the recent suppression of long-term rates/yields. As I correctly previously pointed out, LIBOR across all tenors/maturities had continued to decrease which lowered this metric, to varying degrees, across basically all BDC peers during 2019-2021. The lone outlier was OCSL where some previous non-accrual portfolio companies were put back on accrual status and the relatively new investment management team, at the time, was able to source some new loan originations through the Oaktree platform.

With that said, due to the COVID-19 pandemic, spreads across speculative-grade credit/high yield debt initially experienced a quick, notable "spike" in yields (at its peak by approximately 800 basis points [bps]). The severity of broader credit spread increases/widening was the most notable in speculative-grade credit/high yield debt (typically bearing the most risk). With that said, with notable stimulus by the Federal ("Fed") Reserve/Federal Open Market Committee ("FOMC") within certain pockets of broader credit markets, markets notably "calmed down" as the calendar second quarter of 2020 passed. This overall sentiment "rippled" through broader markets; including speculative-grade credit/high yield debt. During the calendar second quarter of 2020, average speculative-grade spreads/yields narrowed/decreased by approximately (500) bps. These are notable changes for just one quarter. During the calendar third quarter of 2020, average speculative-grade spreads/yields narrowed/decreased by approximately (50) bps. This general trend continued during the calendar fourth quarter of 2020, first quarter of 2021, and second quarter of 2021 as average speculative-grade spreads/yields narrowed/decreased by approximately (160), (75), and (50) bps, respectively. So, speculative-grade/high yield debt spreads notably tightened in a little over 1 year.

While some BDC peers experienced a slight increase in weighted average annualized yields during the second half of 2020, I correctly projected this general "blip" would not continue during most of 2021. In fact, during 2021 - early 2022 speculative-grade/high yield debt spreads were even tighter than prior to the onset of COVID-19. This is one of the main reasons why BDC stock prices notably climbed from 2020 lows (asset prices increase when spreads/yields decrease; inverse relationship).

During 2022, speculative-grade spreads/yields began to widen out/increase. This trend continued during the calendar first quarter of 2023 (especially during March 2023). Not nearly as severe as the COVID-19 pandemic panic but something that should be noted. However, LIBOR/SOFR/PRIME continued to rise which was a net positive catalyst/factor. This short-lived trend reversed course during the calendar second quarter of 2023as previous fears of a mild-modest recession that were considered "all but a certainly" in early 2023 became more open to uncertainty. This general trend has continued during the calendar third and fourth quarters of 2023.

That said, I personally do not see spreads within this specific sector getting much tighter. In fact, a gradual widening is inevitable in my professional opinion. To use an analogy, I believe there is a lot of "tension" on this particular rubber band. It cannot be "stretched" too much further (BDC spreads would not tighten too much further). There will eventually be a widening of spreads (release the rubber band's tension) as government support continues to wane; whether there are no more rounds of consumer stimulus and/or no additional rounds of small business Paycheck Protection Program ("PPP") loans. The Fed Reserve/FOMC had also fairly recently completed its asset tapering program and there has fairly recently been a very rapid increase in the Fed Funds Rate.

Most recently, the announcement of the eventual expiration of the student loan forgiveness program will very likely have negative consequences for pockets of the U.S. economy. This event will not be a total "calamity" but it is only prudent to take this new development into consideration regarding economic impacts and ultimately spreads in speculative-grade credit. When spreads widen, asset pricing/valuations decrease so readers need to consider this impact on NAV. This also considers the eventual rise in credit risk (especially if rates/yields rise too quickly; "shock" to financial markets). It takes time for these impacts to be felt across broader markets. These notions have already been taken into consideration when it comes to projecting dividend per share rates and recommendation ranges provided towards the end of this article (already "embedded" into all modeling through the beginning of calendar year 2025).

The next metric shown in Table 4 is each BDC's proportion of debt investments with floating interest rates (asset side of the balance sheet; additional forward-looking data). ARCC's proportion of debt investments with floating interest rates was 85.19% as of 9/30/2023 (see blue reference "E" ). ARCC's near-average floating-rate percentage was more attractive during the rising interest rate environment of 2017 - 2018. However, as noted above, LIBOR gradually decreased during 2019 which "accelerated" in 2020 as a direct result of the COVID-19 pandemic. As such, when floating-rate loans experienced a net decrease in stated rates when compared to late 2018-2019, ARCC was impacted very similarly to most BDC peers. That said, with the fairly recent quick increase in LIBOR/SOFR/PRIME, most BDC peers have already moved above their weighted average cash LIBOR floor. While several BDC peers publicly disclose this figure, the majority of companies do not. Since I/my team personally calculate/confirm each BDC's weighted average cash LIBOR floor each quarter (which is typically very time-consuming), I believe this is a strategic advantage to my/our service. As such, I have decided not to disclose these percentages (other services could simply "poach" this valuable information with no effort). This data, when combined with the other factors/metrics presented in this article (including several other factors not publicly disclosed), is used to determine dividend sustainability probabilities later in the article and project future NII per share amounts. This is 1 of the main reasons why I/we have beaten the institutional analysts' consensus average in 43 out of the past 46 quarters within the combined mREIT and BDC sectors regarding earnings projections (when combining all fully covered sector peers).

The last metric shown in Table 4 above is each BDC's weighted average interest rate on all debt outstanding (liability side of the balance sheet). ARCC had a weighted average interest rate of 4.70% on the company's outstanding borrowings as of 9/30/2023 (excludes commitment fees and loan issuance costs; see blue reference "F" ). This is compared to a weighted average interest rate of 4.56% as of 6/30/2023. When compared to the 15 BDC peers within this analysis, ARCC continued to have a slightly - modestly below average weighted average interest rate on all debt outstanding. As of 9/30/2023, 27.73% of ARCC's debt outstanding bore floating rates (credit facilities) while 72.27% of the company's debt outstanding bore fixed rates (convertible and unsecured notes). I believe taking a "snapshot" of each BDC's weighted average interest rate on all debt outstanding allows readers to better understand which companies will experience generalized characteristics in the future (thus impacting future net investment income [NII]/TI).

Once again using Table 3 as a reference, ARCC declared a dividend of $0.48 per share for the fourth quarter of 2023. This was an unchanged dividend when compared to the prior quarter. Unlike in 2022, ARCC did not declare a special period dividend per share during the first - fourth quarters of 2023. This gets back to the notion ARCC's management team is typically very cautious regarding dividend increases (even when the company has a very large cumulative UTI balance). To be frank, ARCC EASILY could have declared another special periodic dividend (similar to what has recently occurred with a handful of sector peers).

ARCC's stock price traded at $19.58 per share on 12/15/2023. When calculated, this was a TTM dividend yield (including special periodic dividends when applicable) of 9.81%, an annual forward yield to ARCC's stock price as of 12/15/2023 of 9.81%, and an annual forward yield to my projected CURRENT NAV of 10.11%. When comparing each yield percentage to ARCC's BDC peers within this analysis, the company's TTM yield based on its stock price as of 12/15/2023 was now notably (at or greater than 2.00%) below average, the company's annual forward yield based on its stock price as of 12/15/2023 remained slightly below average, and its annual forward yield to my projected CURRENT NAV remained near average. These percentages are not surprising when it comes to ARCC's dividend sustainability due to the company's weighted average annualized yield on debt investments and weighted average interest rate on debt outstanding (amongst the other factors discussed earlier).

Various Comparisons Between ARCC and the Company's 14 BDC Peers in Ranking Order:

Investing Group Feature

Most BDC peers have seen a minor - modest rebound in their cumulative UTI ratio over the past 2 years. Only CSWC and MFIC have experienced a minor decrease (nothing alarming).

Conclusions Drawn (PART 2):

This article has compared ARCC and 14 other BDC peers in regard to recent dividend per share rates, yield percentages, and several other highly detailed (and useful) dividend sustainability metrics. This article also discussed ARCC's dividend sustainability through the second quarter of 2024. Using Table 3 above as a reference, the following were the recent dividend per share rates and yield percentages for ARCC:

ARCC: Regular dividend of $0.48 per share for the calendar fourth quarter of 2023 (no special periodic dividend) ; 9.81% TTM dividend yield (when including special periodic dividends [when applicable]) ; 9.81% annual forward yield to the company's stock price as of 12/15/2023 ; and 10.11% annual forward yield to my projected CURRENT NAV.

Since ARCC had a similar positive TTM weighted average annualized yield increase on the company's debt investments (assets) when compared to the sector peers within this analysis (a positive catalyst/trend), a very low weighted average cash LIBOR/SOFR/PRIME floor (a positive catalyst/trend; becomes a negative factor/trend when LIBOR/SOFR/PRIME NOTABLY decreases [not anticipated over the foreseeable future]), the most attractive/largest cumulative UTI balance (a very positive catalyst/trend), a slightly - modestly below average interest rate on all debt outstanding (liabilities; a positive factor/trend), and a near average percentage of floating interest rate debt investments (generally a positive catalyst/trend when LIBOR/SOFR/PRIME rises; becomes a negative factor/trend when LIBOR/SOFR/PRIME NOTABLY decreases [not anticipated over the foreseeable future]), I continue to believe the company should have an annual forward yield to its NAV slightly - modestly above the average of the 15 BDC peers within this analysis.

When combining this data with various other analytical metrics not discussed within this specific article (including projected non-accrual rates during 2024 [anticipating a modest increase]; some factors were covered in PART 1),

I believe the likelihood of ARCC having a stable - modestly increasing quarterly dividend through the end of the second quarter of 2024 is very high (90% probability; range $0.48 - $0.53 per share). I also believe there is the possibility of ARCC declaring a special periodic dividend of up to $0.15 per share for the first quarter of 2024.

Looking back to prior dividend projections, I correctly projected a higher probability that FSK, OCSI, and TCPC would need to reduce each company's quarterly dividend at some point in 2020. This analysis also correctly identified a high probability of a special periodic dividend for ARCC, GAIN, MAIN, and TSLX during 2019 (and in GAIN's case an increased special periodic dividend). This analysis also previously correctly projected there was a higher probability MAIN, at the least, would need to reduce the company's special periodic dividend (and in a more bearish case cease declaring this type of dividend). As we now know, MAIN suspended the company's semi-annual special periodic dividend starting in the first half of 2020. More recently, this analysis correctly identified that TSLX would continue to declare special periodic dividends in both 2020 and 2021 (after a very brief "interruption" during the third quarter of 2020). More recently, 6 quarters ago, this analysis correctly identified the growing probability that ARCC would declare an increase to the company's quarterly dividend per share rate, along with a special periodic dividend during 2022. The same holds true regarding MAIN's fairly recent monthly dividend per share rate increases and reintroduction of a minor - modest, special periodic dividend. This also included the rising probability a majority of sector peers would report an increase in monthly/quarterly dividends and various special periodic dividends.

My BUY, SELL, or HOLD Recommendation:

From the analysis provided above, including additional factors not discussed within this article, I currently rate ARCC as a SELL when I believe the company's stock price is trading at or greater than a 15% premium to my projected CURRENT NAV (NAV as of 12/15/2023; $19.00 per share), a HOLD when trading at greater than a 5% premium but less than a 15% premium to my projected CURRENT NAV, and a BUY when trading at or less than a 5% premium to my projected CURRENT NAV.

Therefore, with a closing price of $19.75 per common share as of 12/18/2023, I currently rate ARCC as slightly undervalued from a stock price perspective. However, ARCC is currently very close to being appropriately valued.

As such, I currently believe ARCC is a BUY recommendation (but very close to a HOLD recommendation).

My current price target for ARCC is approximately $21.85 per share. This is currently the price where my recommendation would change to a SELL. The current price where my BUY recommendation would change to a HOLD is approximately $19.95 per share. Put another way, the following are my CURRENT BUY, SELL, or HOLD per share recommendation ranges for ARCC (our Investing Group subscribers get this type of data on all 15 BDC stocks I currently cover on a weekly basis):

$21.85 per share or above = SELL (Overvalued)

$19.96 - $21.84 per share = HOLD (Appropriately Valued)

$18.06 - $19.95 per share = BUY (Undervalued)

$18.05 per share or below = STRONG BUY (Notably Undervalued)

Basically, all of the 15 BDC peers I currently cover should have a stable - slightly increasing dividend for the calendar first quarter of 2024 (or each applicable company's next set of dividend declarations). For some select BDC peers with a higher/growing cumulative UTI balance, this includes a high probability of a special periodic dividend.

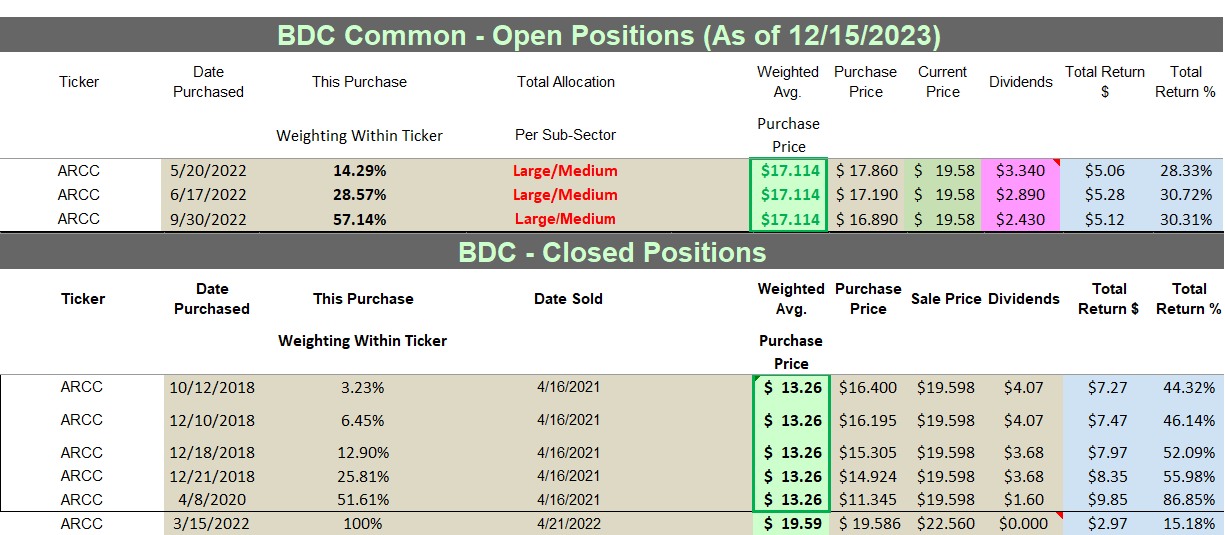

My Personal ARCC Past + Current Stock Disclosures:

The following are my ARCC past and current stock disclosures and total returns since I have been writing on Seeking Alpha:

Table 10 - ARCC Past + Current Stock Disclosures/Returns

{kind=link}

Source: Taken Directly from the REIT Forum's © Spreadsheets/Data

Final Note: All trades/investments I have performed over the past 6+ years have been disclosed to readers in "real-time" (that day at the latest) via either the StockTalks feature of Seeking Alpha or, more recently, the "live chat" feature of our Investing Group (which cannot be changed/altered). Through these resources, readers can look up all my prior disclosures (buys/sells) regarding all companies I cover here at Seeking Alpha (see my profile page for a list of all stocks covered). Through StockTalk disclosures and/or the live chat feature of the REIT Forum, at the end of November 2023 I had an unrealized/realized gain "success rate" of 89.9% and a total return (including dividends received) success rate of 97.1% out of 69 total past and present mREIT and BDC positions (updated monthly; multiple purchases/sales in one stock count as one overall position until fully closed out). I encourage other Seeking Alpha contributors to provide real-time buy and sell updates for their readers/subscribers which would ultimately lead to greater transparency/credibility. Beginning in January 2020, I transitioned all my real-time purchase and sale disclosures solely to members of the REIT Forum. All applicable public articles will still have my "main ticker" purchase and sale disclosures (just not real-time alerts).

Understanding My/Our Valuation Methodology Regarding mREIT Common and BDC Stocks:

The basic "premise" around my/our recommendations in the mREIT common and BDC sectors is value. Regarding operational performance over the long term, there are above-average, average, and below-average mREIT and BDC stocks. That said, better-performing mREIT and BDC peers can be expensive to own, as well as being cheap. Just because a well-performing stock outperforms the company's sector peers over the long-term, this does not mean this stock should be owned at any price. As with any stock, there is a price range where the valuation is cheap, a price where the valuation is expensive, and a price where the valuation is appropriate. The same holds true with all mREIT common and BDC peers. As such, regarding my/our investing methodology, each mREIT common and BDC peer has their own unique BUY, SELL, or HOLD recommendation range (relative to estimated CURRENT BV/NAV). The better-performing mREITs and BDCs typically have a recommendation range at a premium to BV/NAV (varying percentages based on overall outperformance) and vice versa with the average/underperforming mREITs and BDCs (typically at a discount to estimated CURRENT BV/NAV).

Each company's recommendation range is "pegged" to estimated CURRENT BV/NAV because this way subscribers/readers can track when each mREIT and BDC peer moves within the assigned recommendation ranges (daily if desired). That said, the underlying reasoning why I/we place each mREIT and BDC recommendation range at a different premium or (discount) to estimated CURRENT BV/NAV is based on roughly 15-20 catalysts which include both macroeconomic catalysts/factors and company-specific catalysts/factors (both positive and negative). This investing strategy is not for all market participants. For instance, not likely a "good fit" for extremely passive investors. For example, investors holding a position in a particular stock, no matter the price, for say a period of 5+ years. However, as shown throughout my articles written here at Seeking Alpha since 2013, in the vast majority of instances I have been able to enhance my personal total returns and/or minimize my personal total losses from specifically implementing this particular investing valuation methodology. I hope this provides some added clarity/understanding for new subscribers/readers regarding my valuation methodology utilized in the mREIT common and BDC sectors.

Each investor's BUY, SELL, or HOLD decision is based on one's risk tolerance, time horizon, and dividend income goals. My personal recommendation will not fit each reader's current investing strategy. The factual information provided within this article is intended to help assist readers when it comes to investing strategies/decisions. Please disregard any minor "cosmetic" typos if/when applicable.

For further details see:

Ares Capital's NAV, Valuation, And Dividend Vs. 14 BDC Peers - Part 2 (Includes Q1 + Q2 2024 Dividend Projection)