ARGX - argenx: CIDP Data Better Than Expected Maintaining Hold Rating

2023-07-21 13:01:14 ET

Summary

- argenx has released preliminary results from the ADHERE trial, which tested VYVGART Hytrulo on adults with chronic inflammatory demyelinating polyneuropathy (CIDP), where the trial results were positive.

- The trial, involving 322 adult patients, found that VYVGART Hytrulo led to clinical improvements, potentially positioning it as a competitor in the immunoglobulin market (SCIG equivalent).

- We maintain a non-consensus hold rating due to the market's unrealistic optimism around CIDP market opportunity and a decrease in likelihood for a potential M&A at the current valuation of $27bn.

Reason for update: CIDP Adhere trial readout

argenx (ARGX) recently disclosed preliminary results from the ADHERE trial that examined VYVGART Hytrulo (efgartigimod alfa and hyaluronidase-qvfc) in adults suffering from chronic inflammatory demyelinating polyneuropathy (CIDP). In-depth findings from ADHERE are set to be shared at a future medical conference, which we look forward to analyzing in detail in a future article.

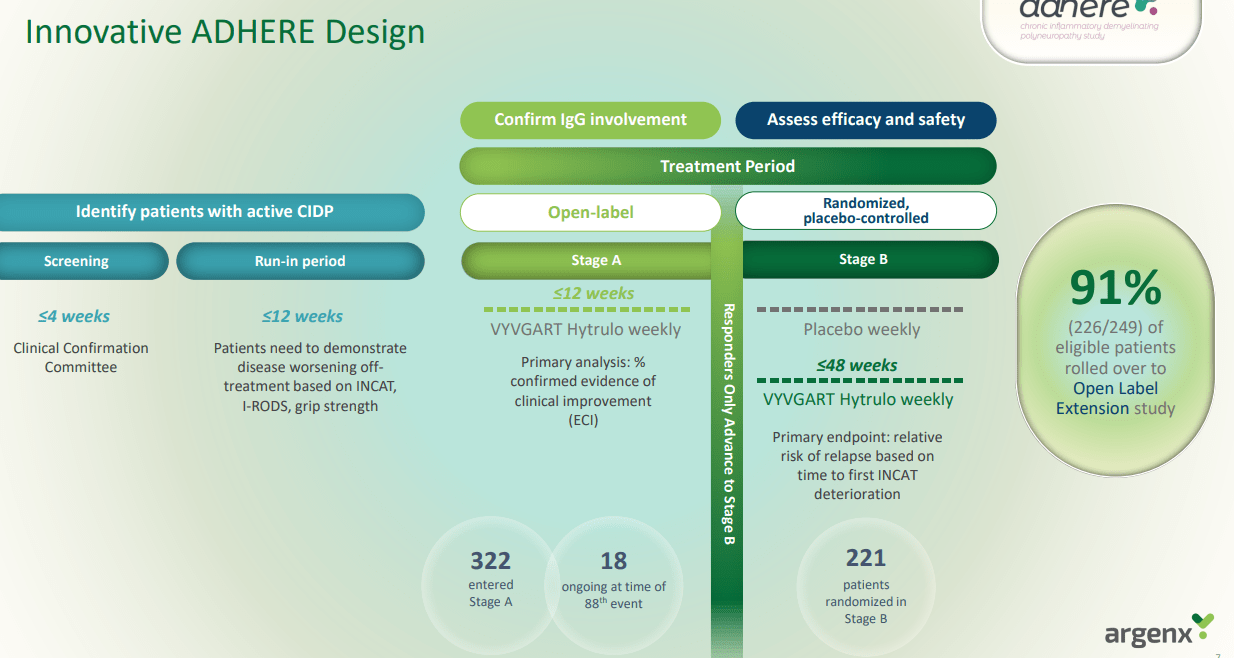

CIDP Trial Design (Company Source)

{kind=link}

To give more context around the CIDP trial design :

the ADHERE trial was a multi-site, double-blind, placebo-controlled experiment that explored the effectiveness of VYVGART Hytrulo in treating CIDP. This study enrolled 322 adult patients, either newly diagnosed, not currently receiving treatment, or being managed with immunoglobulin therapy or corticosteroids. The trial comprised an open-label Phase A, followed by a randomized, placebo-controlled Phase B.

In order to progress to Phase B, patients had to display clinical improvements after treatment with VYVGART Hytrulo, demonstrated through improvements in INCAT score, I-RODS, or mean grip strength. The primary endpoint was the relative risk of relapse determined by time to the first adjusted INCAT deterioration of ?1 point.

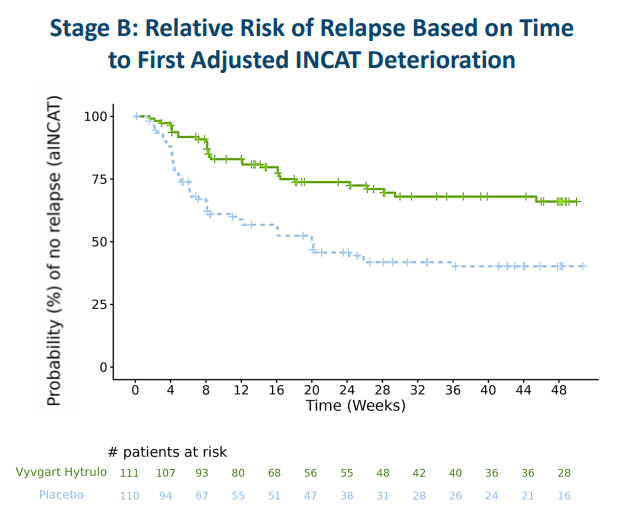

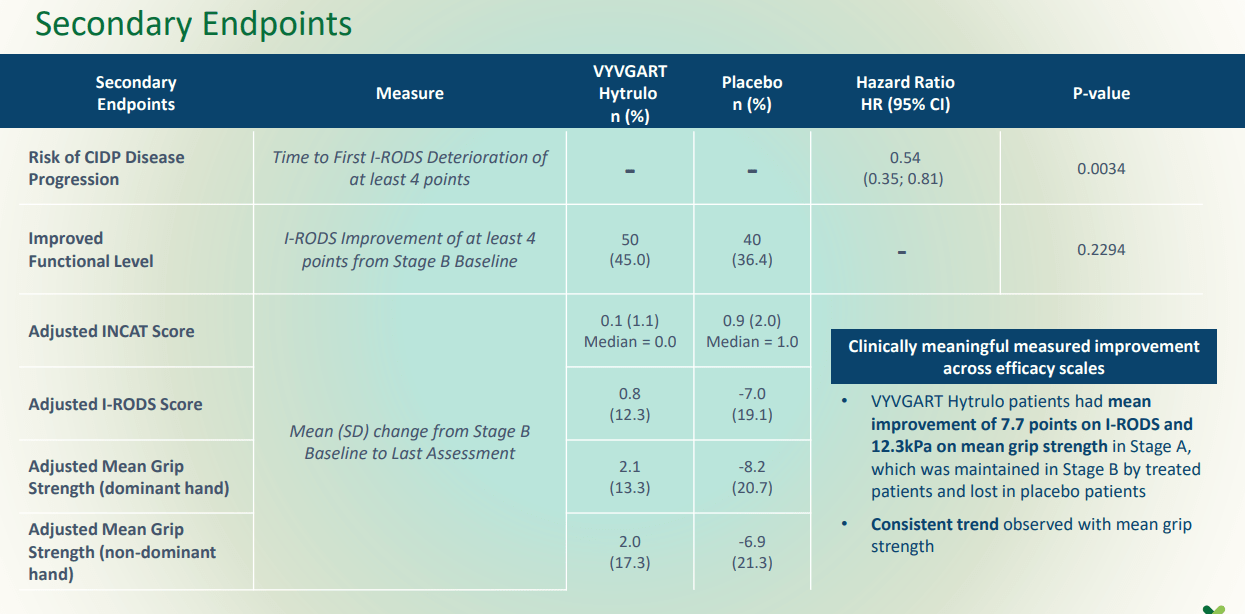

CIDP data (Company Source) CIDP secondary endpoints (Company Source)

{kind=link}

{kind=link}

Trial data summary :

Efficacy

Of the 322 patients who were treated with VYVGART Hytrulo in Stage A, 67% showed evidence of clinical improvement. For those who moved to Stage B, VYVGART Hytrulo significantly lowered the risk of CIDP relapse compared to placebo. In fact, the primary endpoint was met with a 61% reduction (HR: 0.39 95% CI: 0.25; 0.61) in the risk of relapse compared to placebo based on time to the first adjusted INCAT deterioration of ?1 point.

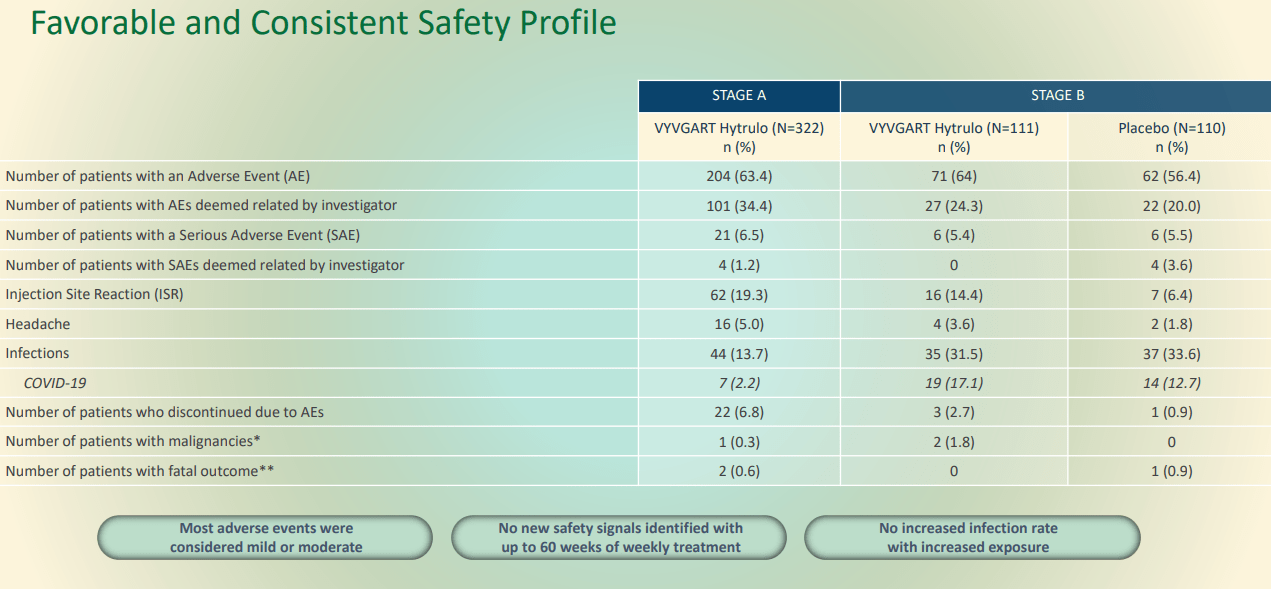

Safety

Adverse events were minimal, with the most common being injection site reactions, all of which were mild to moderate and resolved over time.

Efgartigimod AE summary (Efgartigimod AE summary)

{kind=link}

We believe the ADHERE trial is the most comprehensive trial conducted in CIDP patients to date, which enrolled adults who were a) either treatment-naïve or b) currently on immunoglobulin ((IG)) therapy or corticosteroids. We believe Vyvgart's unique features, such as its convenient and tolerable administration compared to the onerous infusions that can take a couple of hours for IVIG and also SCIG (SC version but still can take a long time), are likely to prove critical in argenx's commercial ramp competing with the established immunoglobulin products currently dominating the space. Of note, CSL and Grifols are the market leaders in the IVIG space. Although we consider convenience a key factor that prescribers would consider in making treatment decisions, we do not believe efgartigimod will be a replacement for IVIG due to the mechanical uncertainty around what drives CIDP (as there could be multiple non-IgG driven phenotypes where efgartigimod may not be effective in (i.e., T-cell driven)) and the current market's optimism around CIDP's sales opportunity (some analysts projecting it to be $2bn ) may be unrealistic.

The additional capital infusion from a +1Bn raise

On the heel of the positive data, Argenx has raised ~1.1Bn; considering the robust growth momentum in MG, we forecast Argenx to reach operating profitability by 2025 (cash reserve of $2.0 billion as of the end of Q2 and cash burn of ~$500m guided). Furthermore, Argenx also disclosed in the company's supplemental prospectus Q2 Vyvgart sales of $269 million, which we believe is a stellar commercial performance and shows the growth momentum has not stopped since its launch in Q1 2022.

Efgartigimod sales (Company Source)

Risks

-

Over-optimistic Market Expectations: The current market expectations regarding CIDP's sales opportunity may be unrealistic, as analysts are projecting it to be $2 billion. If these projections are not met, it could lead to a sell-off in the stock, negatively impacting the share price.

-

Competition from Market Leaders: CSL and Grifols, the current market leaders in the IVIG space, present formidable competition. If these companies can innovate faster or provide more effective treatments, Argenx's VYVGART Hytrulo could lose market share, hampering revenue growth.

-

Mechanical Uncertainty in CIDP Treatment: There is still a significant amount of uncertainty around the mechanical aspects of what drives CIDP. If it is found that there are multiple non-IgG-driven phenotypes, efgartigimod might not be a universal solution for CIDP, limiting its market opportunity.

-

High Valuation Impedes Acquisition Chances: After the positive trial results, Argenx's valuation shot up to $27 billion, making potential M&A deals with big pharma unlikely. This could limit the company's options for raising capital or strategic partnerships, and if the valuation were to decrease significantly, this could negatively impact the stock price.

Conclusion

The CIDP readout was undoubtedly significantly more positive than what we expected, and the Q2 earnings results were positive. However, we do not believe efgartigimod will be a replacement for IVIG due to the mechanical uncertainty around what drives CIDP (as there could be multiple non-IgG driven phenotypes that efgartigimod may not be able to treat) and the current market's optimism around CIDP's sales opportunity (some analysts projecting it to be $2bn ) may be unrealistic. Furthermore, the current valuation of $27bn after the readout further makes the potential big pharma M&A unlikely (until big pharma sees the actual roll-out of the non-MG indications at this valuation). As a benchmark, Alexion's Soliris net sales were ~ $4bn when AstraZeneca acquired the company, significantly above the current efgartigimod's sales.

For further details see:

argenx: CIDP Data Better Than Expected, Maintaining Hold Rating