ARGX - argenx Q3: Navigating The Highs And Hurdles Of A Market Odyssey (Rating Upgrade)

2023-11-27 11:04:09 ET

Summary

- argenx's Q3 earnings exceeded expectations, with Vyvgart sales beating by 11%, indicating strong market demand.

- The anticipated approval for Vyvgart in CIDP by H2 2024 suggests continued positive sales growth.

- argenx's robust cash position, increasing revenue from Efgartigimod sales, and decreasing operating loss point towards cash flow positivity in 2024-2025.

- We upgrade argenx to a buy rating, but we caveat readers that the valuation seems to be priced to perfection.

Q3 Earnings and Efgartigimod's Sales Ramp

We have previously (July 21, 2023) maintained our hold rating on argenx (ARGX) due to several unclear catalysts, such as CIDP readout and sales slowing down. We finally decided to upgrade to a buy rating post Q3 2023 earnings and we will explain our rationale further in this article.

argenx reported robust results in Q3, significantly exceeding consensus expectations with Vyvgart product sales beating by 11%. The positive momentum in Vyvgart sales, especially after adjusting for one-time factors, indicates a strong market demand. The subcutaneous formulation, Vyvgart Hytrulo, is also seeing favorable uptake, primarily from new patients.

CIDP launch is expected to be a meaningful add to the sales ramp

Given the ongoing success and the anticipated approval for Vyvgart in CIDP (Chronic Inflammatory Demyelinating Polyneuropathy) by H2 2024, a continued positive sales ramp is expected. The Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) market presents an attractive opportunity for Efgartigimod, w ith analysts estimating its sales potential to be around $2 billion (evaluate Pharma) . We see this valuation as highly achievable, considering the robust market ramp that we have seen so far and the high unmet need in the MG space without any alternative effective option other than IVIgs or C5 inhibitors.

This significant market size, coupled with Vyvgart's unique features, such as its more convenient and tolerable administration compared to traditional IVIG and SCIG therapies, positions it well for potential commercial success. However, there are notable concerns. Intense competition from established market leaders like CSL and Grifols in the IVIG space could challenge argenx's market share, especially if these competitors innovate more rapidly or provide more effective solutions. Additionally, the therapeutic landscape in CIDP is complicated by mechanical uncertainties, even though the phase 3 data from argenx was highly compelling . The effectiveness of Efgartigimod across various CIDP phenotypes, particularly those not driven by IgG, remains unclear, potentially limiting its overall market reach (which we will only figure out in real life as the various phenotypes of the disease would be hard to replicate in clinical trials). Net-net, we are cautiously optimistic about the CIDP launch with the recent robust data on hand and the novel mechanism of action that efgartigimod offers in a market dominated by IVIgs.

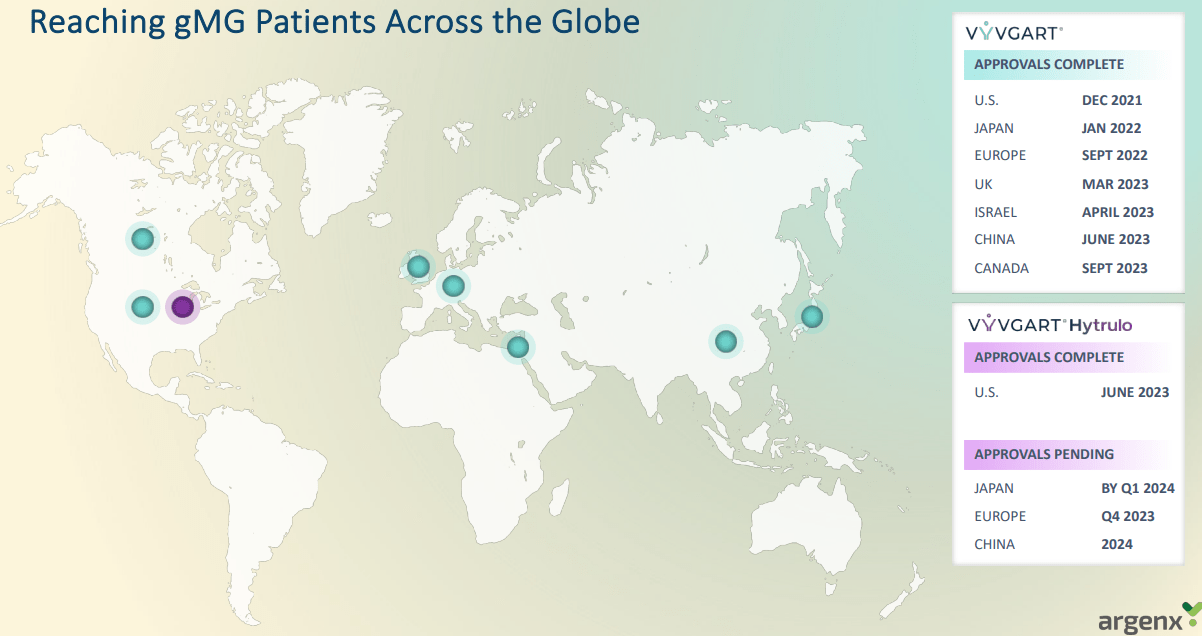

{kind=link}

Global Launch of Efgartigimod (Company IR deck)

Pipeline Assets and R&D Catalysts

argenx's pipeline is rich with potential catalysts. Key among these are the anticipated readouts for Vyvgart in pemphigus and bullous pemphigoid, with pivotal trial starts in thyroid eye disease and a decision on myositis expected in H2 2024. The company is on track to file Vyvgart in CIDP by the end of the year, leveraging a supplemental BLA route with a priority review voucher. Positive data from the Vyvgart intravenous trial in Immune Thrombocytopenia [ITP] and promising developments in pemphigus vulgaris and immune thrombocytopenic purpura suggest high expectations for these upcoming readouts. Additionally, the anticipated developments in other indications like COVID POTS, Sjogren’s Syndrome, and Myositis, along with Phase 2 results for empasiprubart (ARGX-117) in MMN, are set to bolster the pipeline further.

{kind=link}

Multiple catalyst in 2024 (Company IR deck)

Financials

As of September 30, 2023, argenx reported a total of $3.2 billion in cash, cash equivalents, and current financial assets. This marked a significant increase from the $2.2 billion recorded at the end of 2022, primarily fueled by a global offering of shares, which brought in $1.2 billion in net proceeds in July 2023. This strong cash position is critical in supporting the company's operational activities and R&D investments.

In terms of revenue, argenx has shown impressive growth. The company's product net sales for the third quarter of 2023 were $329.1 million, a substantial increase from $131.3 million in the same quarter of 2022. For the nine months ended September 30, 2023, the product net sales were $816.4 million, compared to $227.3 million in the same period of 2022. This growth is indicative of the successful ramp-up of Efgartigimod, contributing significantly to the company's revenue stream.

However, argenx is still experiencing an operating loss, albeit a decreasing one. The operating loss for the third quarter of 2023 was $80.6 million, compared to $208.6 million in the same quarter of the previous year. The cumulative operating loss for the nine months ended September 30, 2023, was $286.4 million, a reduction from $605.9 million in the corresponding period of 2022. This reduction in operating loss, coupled with the increased revenue from Efgartigimod sales, suggests a trajectory towards cash flow positivity ??.

The operating expenses, including research and development, and selling, general, and administrative expenses, were substantial but showed a strategic allocation of resources. Research and development expenses amounted to $191.8 million for the third quarter and $553.1 million for the nine months ended September 30, 2023. Selling, general and administrative expenses were $191.9 million for the quarter and $503.1 million for the nine months. These expenses reflect the company's continued investment in its product development and market expansion efforts?.

In conclusion, argenx's robust cash balance, significant ramp in Efgartigimod sales, and a decreasing trend in operating loss ($80.6M in Q3 2023), all contribute to cash flow positivity in 2024-2025.

Valuation

Considering that the efgartigimod's SC and IV version accounts for ~$6.4Bn peak sales in 2028, using peak sales multiple of 3 (conservative industry standard estimate for the biotech sector), we get an enterprise value of 19.2Bn. We believe the valuation is priced to perfection, but the market is pricing in additional platform value for efgartigimod to enter into, as described above. Although the current enterprise value is higher than our implied valuation, we upgraded argenx to a buy rating (from a hold rating) due to positive momentum in Vyvgart's MG sales ramp and upcoming potential launches. Furthermore, we also highlight that the street is projecting that the company will turn profitable by 2025 with the current rate of sales ramp of efgartigimod and reduced R&D spending during the next 1-2 years due to completion of phase 3 studies in IPD and CIDP.

{kind=link}

Efgartigimod IV consensus forecast (EV Pharma)

{kind=link}

Efgartigimod SC version consensus forecast (EV Pharma)

Risk Factors

Despite the positive outlook, several risk factors warrant consideration. The competition in the myasthenia gravis market, although seen as an opportunity for market expansion, presents a challenge. In Europe, particularly in Germany, Vyvgart faces annual renegotiations if annual revenue exceeds certain thresholds, leading to potential pricing declines. Furthermore, achieving significant market penetration in indications like pemphigus vulgaris and bullous pemphigoid will require navigating established biologic standards of care and complex payer approval policies. Also, the effectiveness of existing standards of care in CIDP could lead to a slower ramp in sales compared to myasthenia gravis. Finally, we highlight that any slowdown in ramp for a few quarters significantly under consensus from here can meaningfully impact the stock price, and we recommend investors carefully monitor the next few earnings moving forward.

Investment Thesis

argenx's solid Q3 performance, driven by strong Vyvgart sales and a robust pipeline, underpins the upgrade to a buy rating. In our experience following biotech stocks, the first 1 year of performance is highly indicative of future success as, usually, the first few quarters are the toughest time for the company due to market access and prescriber inertia; we believe argenx has successfully passed our test and expect this momentum to continue. Furthermore, we don't see any other anti-FcRN entering the market anytime soon. Net-net, the company's strategic positioning, with multiple near-term catalysts and the potential for significant label expansions, positions it well for sustained growth. The anticipation of favorable data readouts in several key indications and the ongoing success of Vyvgart, both in existing and new markets, support a bullish outlook. While acknowledging the competitive landscape and pricing challenges, the overall potential of argenx's pipeline, combined with its strategic initiatives, makes it a compelling investment opportunity.

For further details see:

argenx Q3: Navigating The Highs And Hurdles Of A Market Odyssey (Rating Upgrade)