ARNGF - Argonaut: A Kitchen-Sink Quarter

Summary

- Argonaut Gold has gone from one of the best performing miners in Q4 2022 to one of the worst performers in Q1 2023 after a disappointing year-end report.

- The report saw another increase to upfront capex (3%), a significant miss on FY2022 cost guidance, an underwhelming 2023 outlook, and a large impairment.

- Although its current operating assets take a backseat to Magino, the weaker outlook will weigh on FY2023 cash flow, and I've had to revise fair value down given the outlook.

- At a current share price of US$0.33, Argonaut remains very reasonably valued, but I don't see the reward/risk ratio as favorable enough just yet, so I exited my position for a ~36% gain following the news.

It has been a rough Q4 earnings season for the Gold Juniors Index ( GDXJ ) and while it looked like Minera Alamos ( OTCQX:MAIFF ) might take the cake for the most disappointing production results, Argonaut's ( OTCPK:ARNGF ) results were not much prettier, with ~42,500 gold-equivalent ounces (GEOs) produced at all-in-sustaining costs of $2,266/oz. This capped off what was already an ugly year, with costs coming in well above already upward revised cost guidance (cash costs/AISC) of $1,325/oz and $1,690/oz, respectively. Finally, Argonaut announced a significant impairment at its operating assets and a further increase in upfront capex at its Magino Mine that's now just months from pouring its first gold.

Although I had expected a tough finish to the year given that inflationary pressures were stickier than expected and the CFE Power Line connection only came in October at San Agustin, this was a kitchen sink quarter and one could argue the kitchen sink came along as well in the Q4 results with a ~3% capex increase, and cost to completion now sitting at ~$170 million. Unfortunately, this has led to a downgrade in the stock's fair value given that while I was already being conservative with the value of assets ex-Magino, I didn't expect an impairment of this magnitude nor further cost creep at Magino. Hence, I exited my position for a ~36% gain yesterday after my trailing stop was hit.

{kind=link}

Magino Project (Company Website)

Q4 Production and Sales

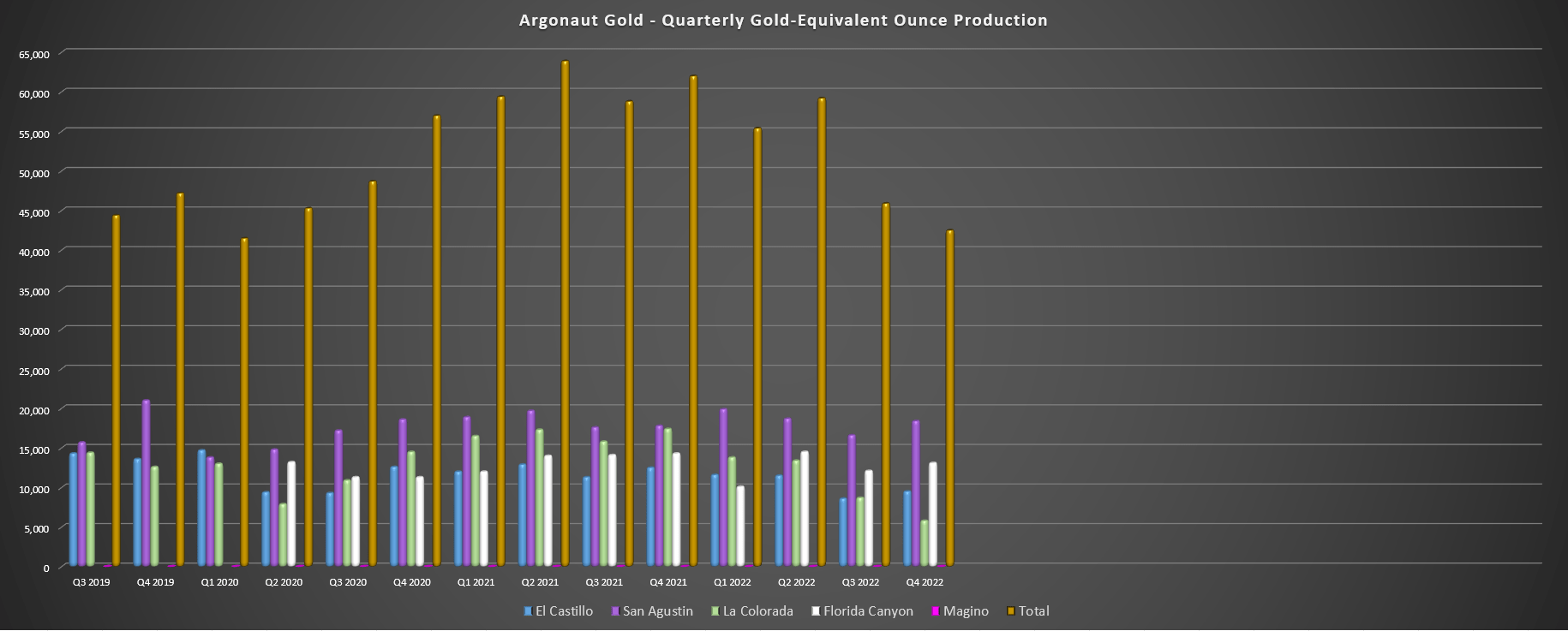

Argonaut Gold released its Q4 and FY2022 results this week, reporting quarterly production of ~42,500 GEOs, a 32% decline from the year-ago period. The sharp decline in production was related to the cessation of mining at El Castillo, a much softer quarter at La Colorada due to reduced contribution from the higher-grade El Creston Pit, and a weaker quarter at Florida Canyon. This mediocre finish to the year resulted in annual production coming in ~6% below its FY2022 guidance mid-point of 215,000 GEOs at just ~203,200 GEOs, and costs came in well above already upward revised cost guidance, with cash costs and all-in-sustaining costs [AISC] of $1,443/oz and $1,765/oz, respectively.

{kind=link}

Argonaut Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

Looking ahead to FY2023, the outlook wasn't much better, with Argonaut guiding for 215,000 GEOs at costs of $1,675/oz even with Magino set to come online in May. This guidance outlook is actually worse than the initial 2022 outlook (215,000 GEOs at $1,470/oz), highlighting how significant inflationary pressures can be on low-grade operations that lack economies of scale, and why it can be tough to place reliance on short mine life assets like El Castillo (production was halted in Q4 and mining headed into lower recovery areas making it uneconomic to mine). As for Magino's 2023 outlook, the silver lining is that we're just a few months away from first gold pour in May, commercial production is expected in Q3 2023, and the mine should contribute upwards of 70,000 ounces in a partial year of production.

Finally, digging in further on its existing operations, Argonaut took a ~$135 million impairment in 2022, with this related to land acquisition and permitting challenges at La Colorada and San Agustin, and inflationary pressures and lower metallurgical recoveries at Florida Canyon. The company also noted that San Agustin and La Colorada are expected to complete their final phases of mining this year and leaching processes will be complete in 2024. Following this, the assets will be placed into care and maintenance while Argonaut aims to secure land access and permits to allow the company to exploit additional resources and reserves on the properties. So, while Magino will hit its stride in 2024 (120,000-plus ounces), we will see a material production shortfall from lack of production from its Mexican operations.

{kind=link}

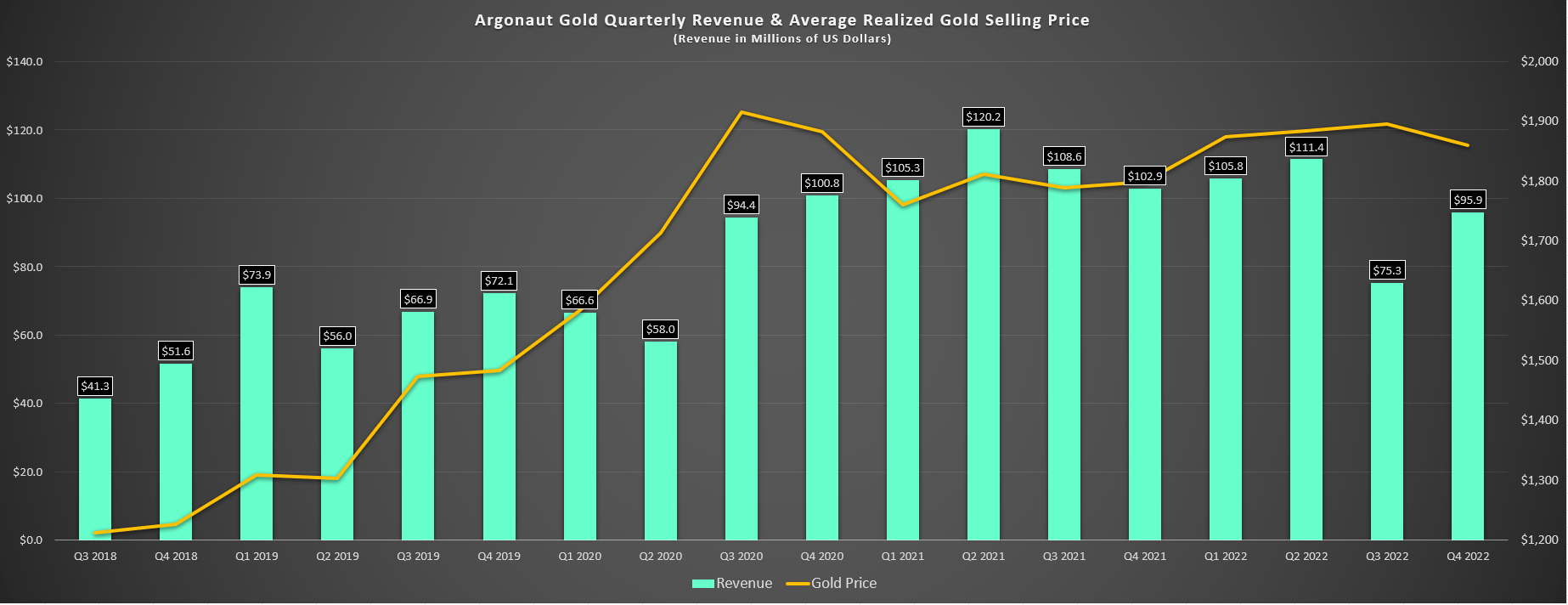

Argonaut - Quarterly Sales & Average Gold Price (Company Filings, Author's Chart)

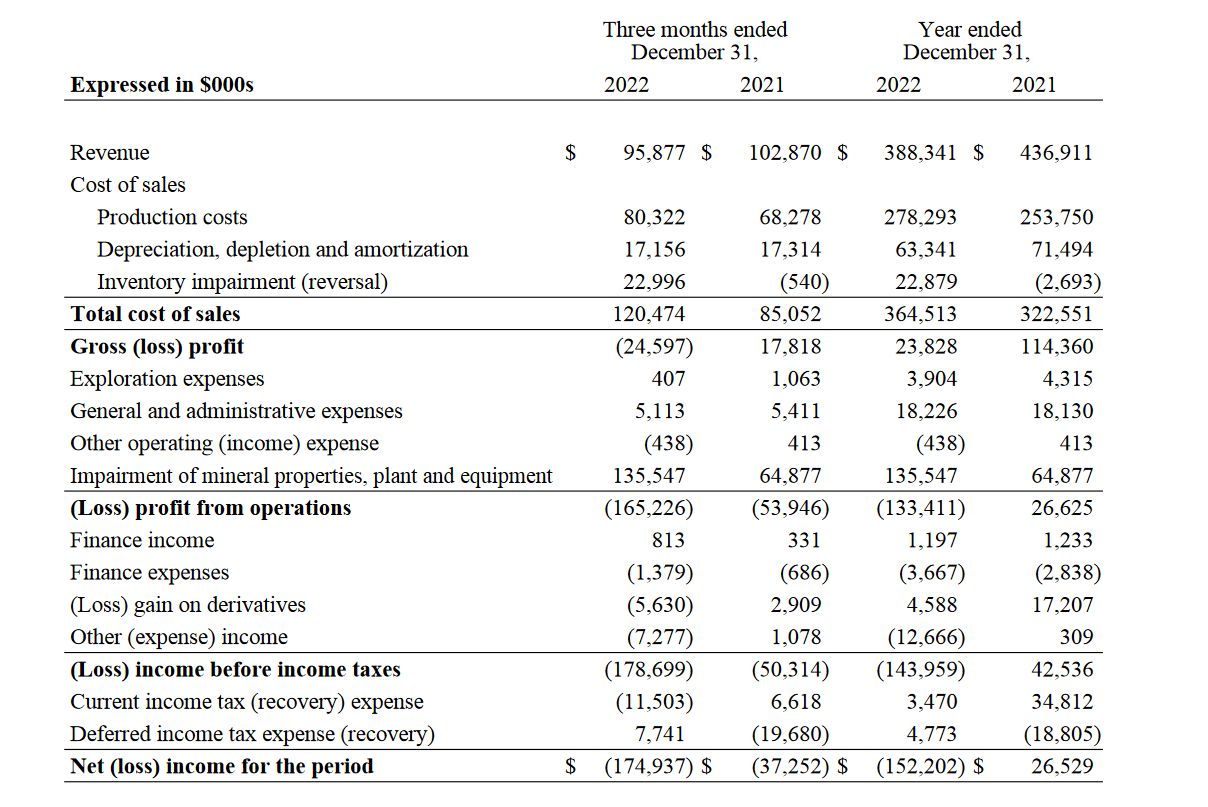

Looking at Argonaut's financial performance, it obviously wasn't very pretty given the lower than expected output. The company reported quarterly revenue of $95.9 million (down 6% year-over-year) and FY2022 revenue of $388.3 million (down 11% year-over-year), with this related to lower sales volumes with a weaker year from San Agustin, El Castillo, and especially La Colorada (~43,800 GEOs sold vs. ~64,500 in 2021). In fact, the company's sales were actually better than they would have been if not for favorable hedging, with Argonaut reporting an average realized gold price of $1,877/oz, more than 5% above the industry average. From a cash flow standpoint, operating cash flow sunk to $70.6 million, down from $124.9 million in the year-ago period. Let's take a look at costs and margins a little closer:

Costs and Margins

Just over nine months ago, I warned on Argonaut Gold above US$2.00 per share, and noted:

"The inflationary environment has deteriorated the investment thesis for smaller producers. There are exceptions, but the smaller producers typically lack the balance sheets to invest aggressively in exploration, purchasing items ahead or in bulk, and technology/innovation. They also lack economies of scale. For example, Paracatu is a very profitable operation at sub 0.50 gram per tonne gold grades even in an inflationary environment.

The story is not the same for operations producing less than 60,000 ounces per annum (Florida Canyon and El Castillo). To summarize, while some junior/mid-tier producers are investable, I do not see the Argonaut of today as investable, with the company being in one of the worst positions among its peers. This is because the company operates four high-volume, low-grade operations in mostly Tier-2 jurisdiction (Mexico) and has a relatively short mine life at El Castillo."

- ARNGF Seeking Alpha Article, April 3rd, 2022

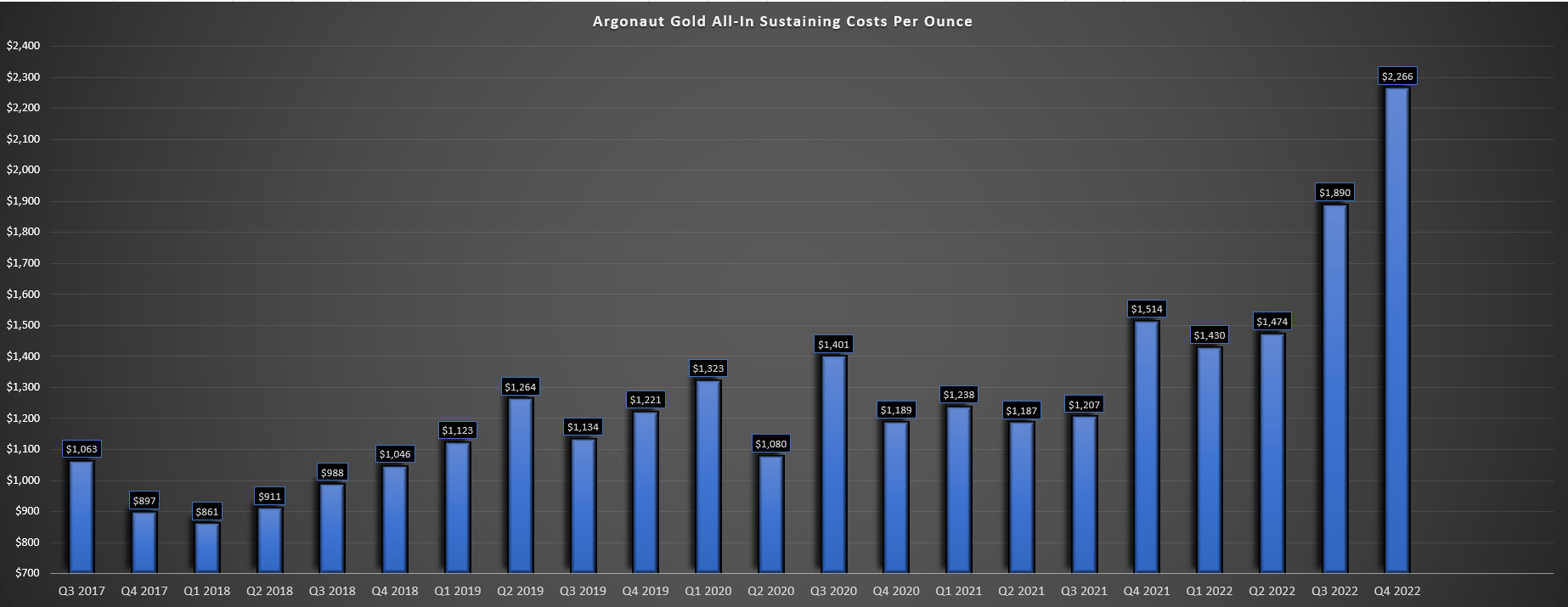

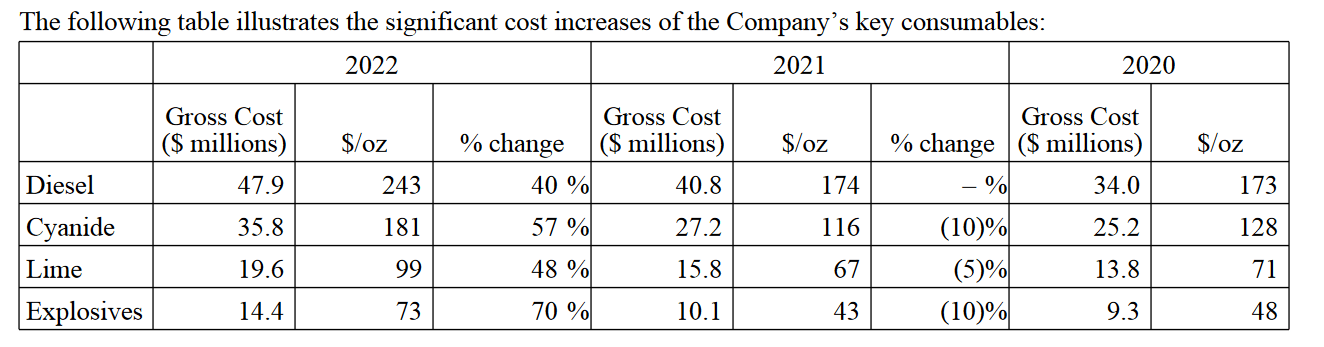

This certainly turned out to be the case for Argonaut's high-volume and low-grade Mexican operations that have limited profitability with an average rock value below $35/tonne. As shown in the below chart, AISC soared to $2,266/oz in Q4 and came in just shy of $1,800/oz for the year. The inflated costs were partially due to an inventory write-down, but even adjusting for this, costs came in well above the industry average of ~$1,300/oz and have trended higher at an accelerated pace since 2021. The culprit for this is rising diesel, cyanide, lime, and explosives costs, and a stronger Mexican Peso certainly didn't help matters in 2022. The result is that cash costs alone were up over 45% from FY2020 to FY2022 ($1,443/oz vs. $946/oz).

{kind=link}

Argonaut - Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

Argonaut - Consumables Costs (Company Filings)

Although costs will dip year-over-year based on 2023 guidance, they're still expected to remain 30% above FY2020 levels even with lower-cost contribution from Magino, setting up a sluggish 2023 at best at current metals prices. The good news is that with the CFE power line connection in 2023, we will see a dip in diesel consumption at San Agustin (savings of 300,000 liters per month), and industry-wide commentary from some producers suggests we saw peak inflation in Q3/Q4 2022 with costs normalizing a little. That said, the one negative was that Magino's upfront capex increased to ~$755 million ($730 million previously), placing a further strain on the NPV (5%) at this asset which previously sat well north of $600 million before the capex blowouts.

So, why go long the stock in Q4?

Following another 85% haircut in the stock into November 2022 and after valuing Argonaut's operating/development portfolio (ex-Magino) at just $350 million, I went long Argonaut at US$0.265 at a ~$230 million market cap under the belief that investors were getting Magino for free based on the value of the operating portfolio (or the operating portfolio for free if they valued the stock on Magino). However, following material write-downs and much worse cost creep than I expected, I have revised my fair value for its operating/development portfolio (ex-Magino) to just $210 million to be conservative, shaving significant value off Argonaut and reducing my fair value to US$0.54.

Taking a more conservative valuation approach to these operating assets that have seen material cost creep and are suffering from permitting challenges has put a dent in my fair value and with a less ebullient 2023 outlook, another cost increase at Magino (albeit a minor one) and worsening sentiment sector wide, it's no surprise that the stock took a beating this week. Given the deterioration in the technical outlook with Argonaut slicing below a key support area, I exited the rest of my position after taking some profits at US$0.47 as the stock became overbought in mid January. Let's take a look at the valuation after the drop:

Valuation

Based on ~850 million fully diluted shares and a share price of US$0.33, Argonaut trades at a market cap of ~$280 million, a very reasonable valuation for a company with one Tier-1 jurisdiction asset nearing production, another small-scale Tier-1 jurisdiction asset (Florida Canyon), and several Tier-2 jurisdiction operations/development projects. However, as discussed earlier, it's tough to place much value on the portfolio outside of Magino because of the cost profile, especially if one takes a conservative view on the gold price and assumes a base case of $1,800/oz, which I think is wise given that it is quite volatile even if there is certainly a fundamental case for higher prices later this decade.

{kind=link}

Argonaut - Annual Financial Results (Company Filings)

If we assume an estimated fair value of $450 million for Magino, $100 million in exploration upside across the portfolio, and $210 million in value for the rest of the portfolio (Florida Canyon, La Colorada, San Agustin plus development assets), I see a fair value for Argonaut of $760 million. Using a P/NAV multiple of 0.90x to reflect the mostly Tier-1 jurisdictional profile (assuming it divests or winds down its Mexican operations) and after subtracting out $220 million in net debt and corporate G&A, I see a fair value for Argonaut of $475 million or US$0.54 per share. Although this represents 64% upside from current levels, I'm looking for a much larger margin of safety for sub $500 million market cap companies, like was present when I bought in November 2022.

With sector laggards and sub $500 million market cap names, I want a minimum 50% discount to fair value to justify starting new positions, and Argonaut would need to trade back below US$0.275 to meet this criterion. Obviously, there's no guarantee that the stock declines by this magnitude after it's already suffered a sharp decline. However, for high-risk and more volatile names like Argonaut, I want to be compensated with considerable upside to fair value for taking on that risk and I don't see enough margin of safety just yet.

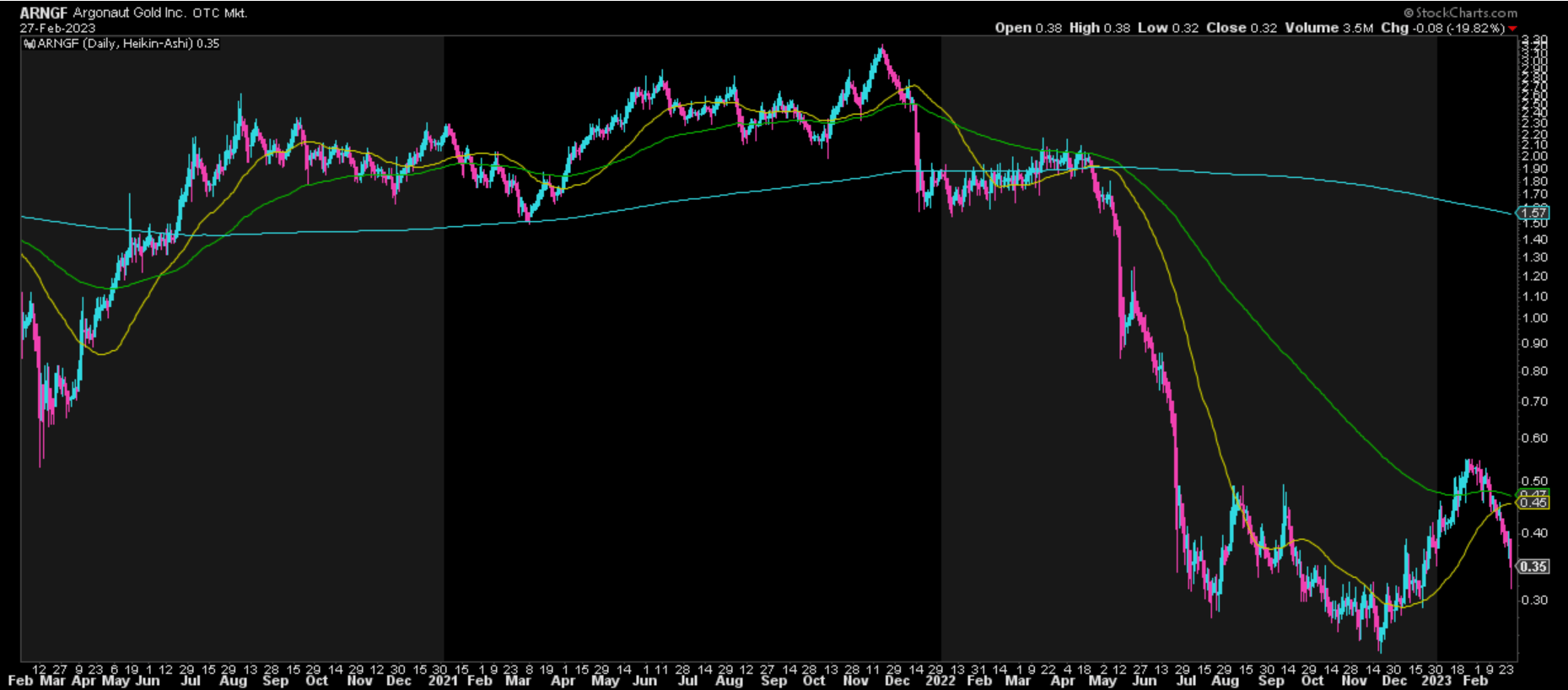

{kind=link}

ARNGF Daily Chart (StockCharts.com)

If the stock bottoms at this level and it takes off without me hopping back on board, that's perfectly fine. I was looking for a quick 35%-40% gain on Argonaut when I bought in November and achieved that, and I'm ahead of most that are still underwater on the position after trying to catch a falling knife above US$1.50 per share. I think the key to long-term success is not being married to positions and only getting aggressive when the odds are stacked massively in one's favor, and while that was the case at US$0.265 in November, it's less so with a significant impairment, a less favorable outlook at all assets (Magino is on track but we've seen minor cost creep) at a 20% higher share price.

Summary

Assuming Magino can perform as planned and given its significant permitted capacity and potential for upside from Magino Underground, Argonaut has a bright future under its new CEO Richard Young, who did an incredible job at Teranga Gold before its eventual sale. That said, the FY2023 outlook is less favorable than expected and I did not expect an impairment of this magnitude. Meanwhile, the stock has broken below a key technical level at US$0.35, which has killed short-term momentum, suggesting that while a return to the lows at US $0.25 is unlikely, it can't be ruled out. So, while I will be watching the stock for a potential bottoming setup, I remain on the sidelines for now.

For further details see:

Argonaut: A Kitchen-Sink Quarter