ARNGF - Argonaut Gold: Further Weakness Should Present A Buying Opportunity

2023-05-29 06:36:08 ET

Summary

- Argonaut Gold's Q1 results showed a 30% decline in production and negative all-in sustaining cost margins.

- The company is expected to transform into a lower-cost miner with a Tier-1 jurisdiction focus, capable of producing over 200,000 ounces per annum.

- With a new CEO, Argonaut Gold is becoming a more investable company, and I would view pullbacks below US$0.37 as buying opportunities.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) is finally over and one of the most recent companies to report its results is Argonaut Gold ( OTCPK:ARNGF ). Unfortunately, this was another rough quarter for the small-cap gold miner from a headline standpoint, with gold-equivalent production down 30% year-over-year to ~38,600 ounces, and all-in sustaining costs remaining near their highest levels on record at $1,947/oz. That said, the Q1 results don't accurately reflect how this business will look over the long-run. In fact, with a new CEO at the helm, arguably a conservative mine plan at Magino and a pivot away from high-volume and high-cost Mexican operations, Argonaut's evolution into a more investable company has finally begun. Let's take a closer look below:

Q1 Production & Costs

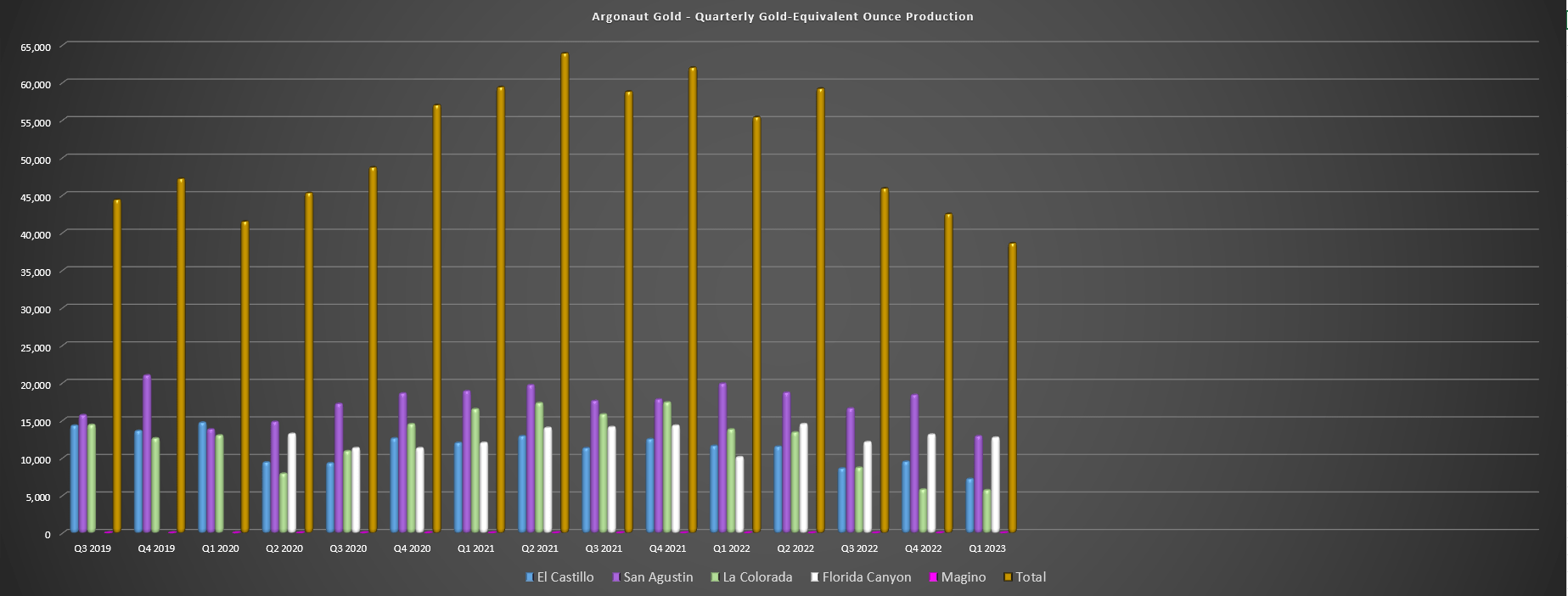

Argonaut Gold released its Q1 results earlier this month, reporting quarterly production of ~38,600 gold-equivalent ounces [GEOs], a 30% decline from the year-ago period. This was related to lower tonnes mined and lower grades at its Mexican operations, with its El Castillo Mine busy with residual leaching after mining activities were halted in Q4 of last year (~7,200 GEOs produced in Q1 2023 vs. ~11,600 GEOs in Q1 2022). Meanwhile, Argonaut is winding down its other two operations in Mexico (San Agustin and La Colorada), but will look at organic growth opportunities for La Colorada where high-grade mineralization was encountered below the El Creston Pit. The result of the lower grades and tonnes mined at these operations and a soft start to 2023 at Florida Canyon (Nevada) was a significant decline in revenue and operating cash flow to $69.0 million and $10.5 million, respectively.

Argonaut Gold - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

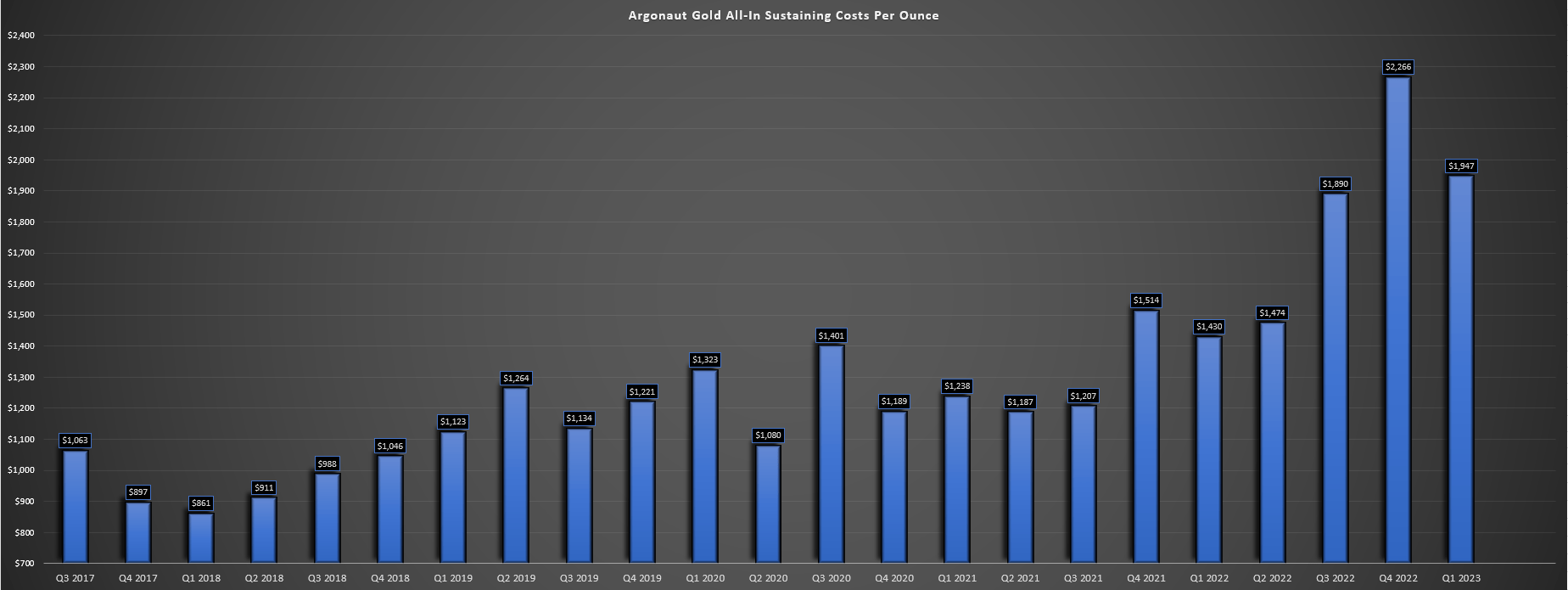

Looking at the operations from a cost standpoint, there wasn't anything to write home about here either, with cash costs soaring to $1,660/oz (+44% year-over-year) and all-in sustaining costs [AISC] increasing to $1,947/oz, making Argonaut one of the highest-cost gold producers sector-wide. And while Florida Canyon will remain in production while Argonaut pivots away from Mexico temporarily, this mine didn't provide any help from a margin standpoint with ~12,700 GEOs produced at all-in sustaining costs of $1,794/oz. Argonaut did note that this was a weaker Q1 than planned and that operational improvements have led to higher production in March, with what should be better performance as the year progresses, but even if Florida Canyon meets guidance, it's expected to produce just 60,000 ounces at $1,750/oz AISC at the midpoint.

Argonaut Gold - All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

Given the lower average realized gold price of $1,858/oz and significant increase in AISC, Argonaut's AISC margins came in at [-] $89/oz, down from $444/oz in the year-ago period. And while these headline results certainly don't make Argonaut Gold look investable, the company has a much better asset in the wings that's expected to pour first gold within the next week and begin commercial production by Q4 of this year. This is the Magino Mine in Ontario, Canada, which is expected to produce ~142,000 ounces of gold for its first five years, with FY2023 production likely to come in near ~70,000 ounces at $1,225/oz AISC in a partial year of production for the asset. And while investors had to deal with significant uncertainty this time last year with another cost blowout, Magino is fully funded with Argonaut having ~$160 million in liquidity at quarter-end and ~$100 million left to spend at Magino.

{kind=link}

Unfortunately, moving this asset into production has come at a cost, with capex blowouts due to inflationary pressures hurting multiple producers and developers. In Iamgold's ( IAG ) case, this meant having to sell off half of its portfolio and giving up additional interest in Cote temporarily to avoid share dilution, including the sale of its Boto, Karita, and Diakha-Sirabaya Projects in Senegal, Guinea, and Mali, and its Rosebel Mine in Suriname. In Argonaut's case, the company didn't have $500+ million in assets to sell to help address its funding gap at Magino, and the result is that its weighted average share count has soared by ~170% year-over-year to ~838 million shares, and should end the year above 860 million shares following the closing of its recent financing. And in addition to this equity dilution, a 2.0% NSR was sold to Franco-Nevada, slightly reducing Argonaut's exposure to this asset.

While this is certainly disappointing, Argonaut is finally just steps away from the finish line (albeit behind its May 15th production target at Magino). And while the recent mining law reforms in Mexico are not positive, the start of production at Magino will come just in time to pivot away from this less favorable Tier-2 jurisdiction without seeing any significant impact to overall production. So, while there's lots to be negative about and shareholders have been put through the wringer here, new management is in place to clean up, and Argonaut remains a promising turnaround story with well over 50% upside to fair value if Magino is able to perform as expected, and assuming Florida Canyon can be optimized.

Recent Developments

Starting with the negatives, Argonaut noted that labor continues to be a challenge and stockpiling of ore is occurring at a slower rate than planned, with just ~103,000 tonnes stacked as of quarter-end and closer to ~200,000 tonnes stacked as of mid-May. These are negative developments, as is the fact that while fuel prices have cooled off a little, one theme we're seeing industry-wide is persistent labor/contractor inflation, and inflationary pressures on some consumables, even if freight and fuel costs are minor offsets. This suggests that the expected all-in sustaining costs of $1,000/oz over the mine life (Q1 2022 TR) may not end up being conservative enough, meaning all-in sustaining costs could come in closer to $1,100/oz, reflecting significant inflationary pressures experienced in 2022, and the mid single-digit inflation expected by some producers in 2023.

{kind=link}

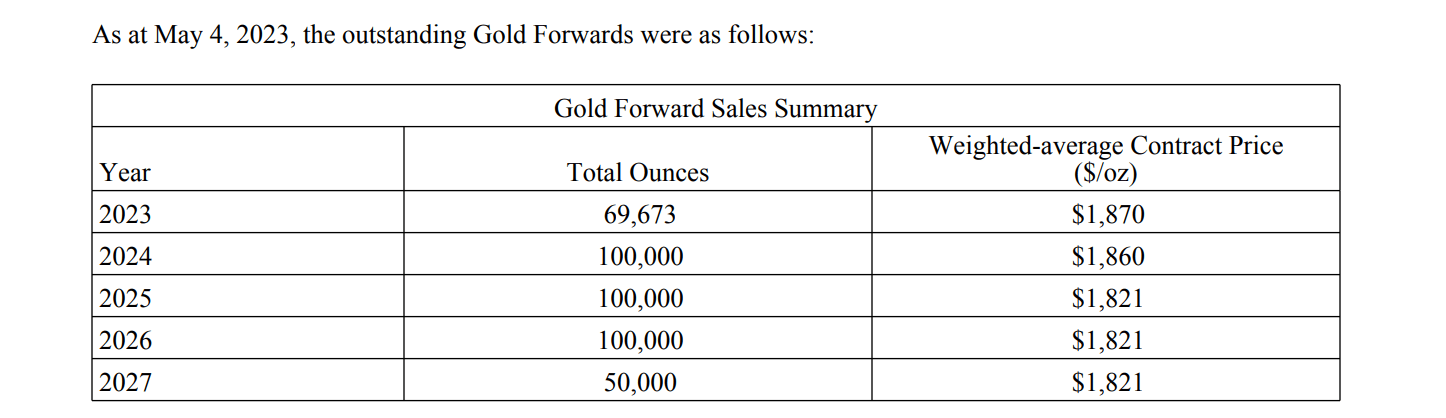

The other negative development is that Argonaut Gold has over 40% of 2024-2026 gold production sold forward at an average price of ~$1,830/oz, meaning it's not benefiting nearly as much from the higher gold prices as some of its peers. So, while Magino will be transformative from a margin standpoint, it won't benefit nearly as much as peers, with an average realized gold price closer to $1,930/oz even if the spot price heads back above $2,000/oz. Finally, while Florida Canyon is a work in progress, it continues to be a very high-cost mine. So, between elevated costs at Florida Canyon and what I would argue to be more conservative assumptions of $1,050/oz AISC from 2024 to 2028 at Magino, Argonaut's consolidated costs are likely to be closer to $1,275/oz, only marginally below the industry average.

That said, there are some positives worth discussing. For starters, Argonaut is working to convert open pit resources to reserves, with ongoing work to potentially look at mill optimization and expansion down the road. At a 15,000 tonne per day throughput rate, production would increase to 190,000+ ounces per annum. And with Argonaut remaining excited about the underground opportunity, there is the potential to lift production to ~230,000 ounces per annum end of this decade even at a 15,000 tonne per day processing rate by displacing a small portion of open pit feed with higher-grade underground feed. This is a similar (albeit a much smaller scale) opportunity to what Agnico Eagle ( AEM ) is looking at with Detour Lake, with upside from a throughput standpoint vs. permitted capacity (32.8 million tonnes vs. 27.0 million tonnes) and the potential for Detour Underground to increase head grades.

{kind=link}

If successful, this could certainly help to offset the impact of inflationary pressures and help Magino operate at sub $950/oz all-in sustaining costs, which would be well below the industry average of ~$1,300/oz. And while these improvements won't happen overnight and significant work has to be completed in the interim, I would argue that these optimizations aren't a stretch. Plus, unlike the disastrous capex blowout that has torpedoed shareholder value because of non-stop share dilution (near-tripling of the share count vs. Q4 2021 levels), they could pursue these opportunities with free cash flow, helping Argonaut to improve its production growth per share metrics which remain among the worst industry-wide due currently.

Valuation & Technical Picture

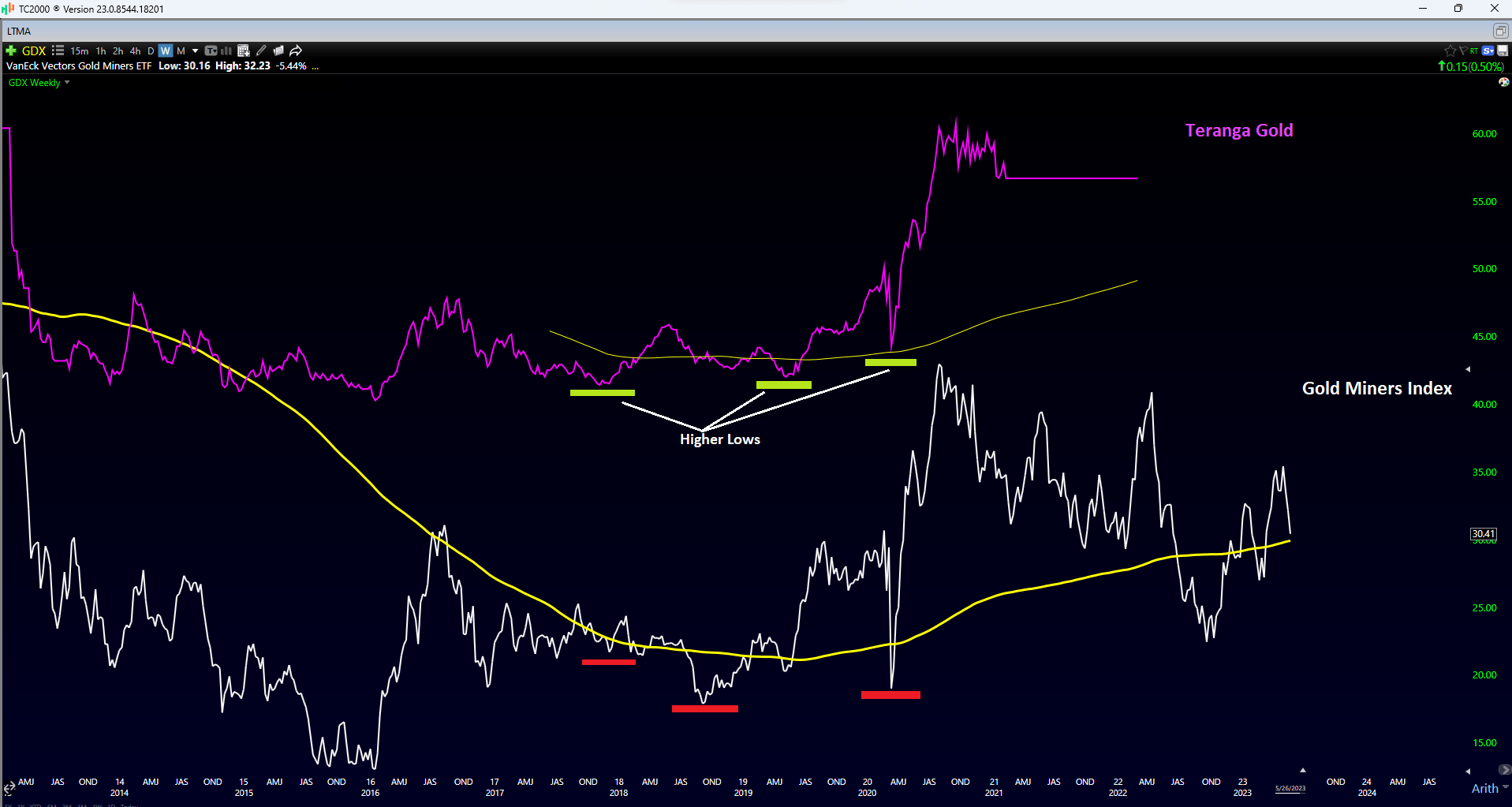

Based on ~900 million fully diluted shares and a share price of US$0.42 (which includes convertible debentures and the recently closed financing in April) Argonaut trades at a market cap of US$378 million (~$550 million enterprise value), making it one of the cheapest ~200,000-ounce producers in the market today. And while this might look justified with the company reporting negative AISC margins in its Q1 results, Magino is a transformative asset that will dramatically improve its margin profile. In addition, its winding down of its Mexican operations is a positive from a jurisdictional standpoint, similar to Kinross ( KGC ) exiting a business that led to a discounted multiple when it sold its Chirano and Kupol/Dvoinoye mines last year, and its Udinsk Project, in Ghana and Russia, respectively.

Given this significant improvement in the business outlook with a large low-cost mine in a Tier-1 jurisdiction set to come online, which will offset elevated costs at its smaller Florida Canyon Mine, some investors might believe that a return to US$2.00 level is warranted. However, it's important to note that Argonaut's share count has nearly tripled from year-ago levels, meaning that anchoring one's price target to the stock's previous highs makes little sense from a valuation standpoint. And while I believe a fair multiple for Argonaut is 1.0x P/NAV vs. 0.80x P/NAV previously, this still translates to a fair value of just US$0.67 based on an estimated net asset value of ~$600 million, which includes exploration upside at Magino and adjusts for its net debt estimated corporate G&A.

Plus, Argonaut has hamstrung itself a little relative to peers with a significant portion of forward gold sales at prices ranging from $1,821/oz to $1,860/oz over the next several years (2024-2027), meaning it won't receive the same benefit from a higher gold price as its peers. And while there is material upside to an estimated fair value of US$0.67, I am looking for a minimum 45% discount to fair value for sub $500 million market cap names in the gold sector, and especially those where we're in the ramp-up of phase of production when it's not entirely clear if the mine will perform as efficiently as expected. After adjusting for this required margin of safety level for smaller-cap producers, the ideal buy zone for Argonaut comes in at US$0.37 or lower.

{kind=link}

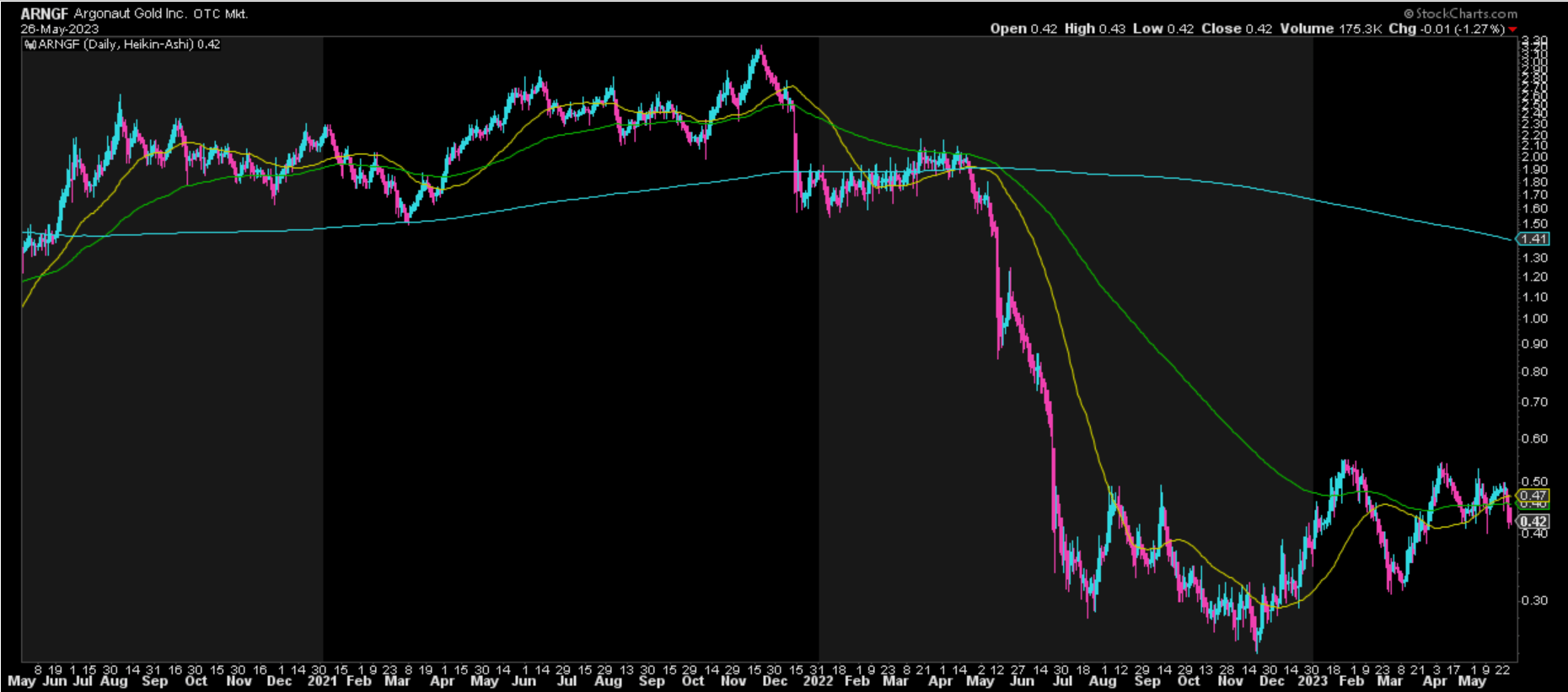

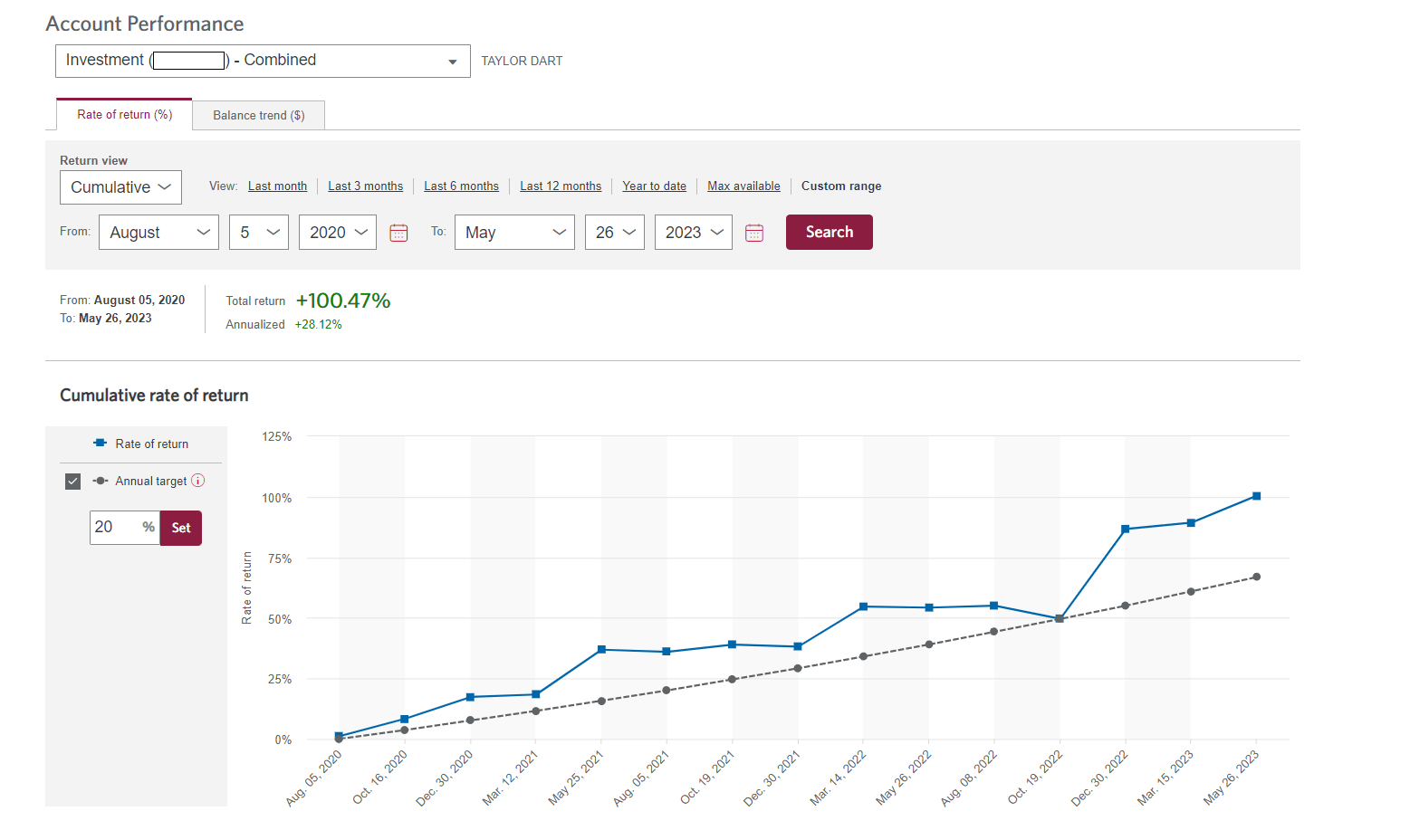

Finally, if we look at the technical picture, Argonaut may be well off its previous highs, but it remains in the upper portion of its support/resistance range, with clear resistance at US$0.52 and no meaningful support until US$0.31. This doesn't mean that the stock must pull all the way back to support, but I prefer to buy in the lower portion of a stock's support/resistance range, and especially for turnaround stories. So, while I think Argonaut is one of the more interesting names from a value standpoint, I would need a pullback to US$0.37 to become more interested. Waiting for a pullback of this magnitude could result in a missed opportunity. However, I don't believe in cheating on entries and letting emotions override rules-based systems, and this rigid approach has helped me to outperform the GDX since its August 2020 peak, with it down 30% in the same period.

Portfolio Returns - August 5th, 2020 to May 26th, 2023 (Personal Portfolio Returns)

{kind=link}

Summary

Argonaut Gold's Q1 results were anything but pretty, with production down 30% year-over-year and it being one of the few producers to report negative all-in sustaining cost margins, even with some help from the gold price as a tailwind. That said, the Q1 results do not accurately represent what this business will look like post-2023, which is a much lower-cost miner with a Tier-1 jurisdiction focus capable of producing 200,000+ ounces per annum at sub $1,300/oz all-in sustaining costs, and 240,000+ ounces if higher processing rates are explored, with the mill already permitted to operate at significantly higher levels, and underground opportunities also being explored which could spike feed grades.

{kind=link}

Plus, while Magino is nearing the finish line and all the heavy lifting is complete, investors can have much more confidence in the management team here, which is arguably the most important attribute when investing in small-caps, and one reason I have avoided Argonaut from 2016-2022. However, former Teranga Gold CEO Richard Young is a massive upgrade from pre-2021 Argonaut leadership, with Young being a company-builder that transformed Teranga into a sector leader before its eventual sale at a premium valuation. So, with a new CEO with a track record of building shareholder value in a disciplined manner, we can finally look Argonaut at as a potential investment, and not just a swing-trading vehicle. To summarize, if we were to see further weakness in the stock below US$0.37, I would view this as a buying opportunity.

For further details see:

Argonaut Gold: Further Weakness Should Present A Buying Opportunity