ARNGF - Argonaut Gold: Substantial Improvements In Costs During Q2 Compared To Q1

2023-08-11 15:38:32 ET

Summary

- Q2-23 result: Production and cost are in line with guidance.

- The valuation continues to be compelling without the Mexican assets, which might now produce longer than earlier communicated.

- Argonaut Gold is a compelling gold miner with growing production and lower costs in 2024.

Investment Thesis

Argonaut Gold ( ARNGF ) released its Q2 results on August 11. This article covers the Q2 result and some general thoughts about the company. I have written many articles about Argonaut Gold over the last three years, which can be found here .

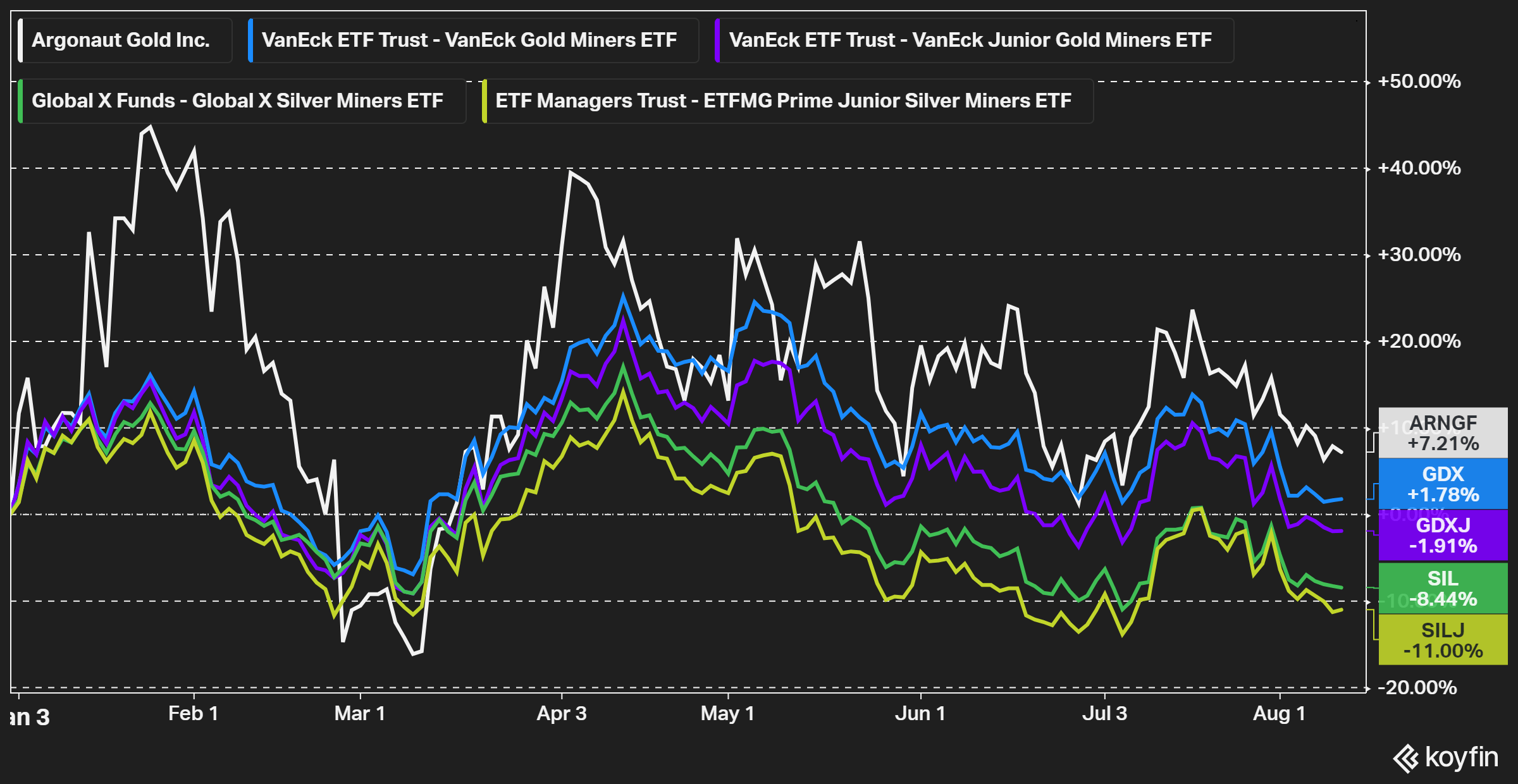

Following a horrible 2022, with multiple cost overruns for Magino and a very large bought deal at an extremely depressed stock price, 2023 has been much less turbulent for the company. Argonaut has had a positive performance and has outperformed the regular precious metals ETFs during the year, even if there is likely a lot more upside remaining if the company achieves commercial production in Q3, as expected following the first gold pour in mid-June.

{kind=link}

Q2-23 Result

Argonaut did in the second quarter of the year report $83.1M in revenues, a net income of $21.2M, and adjusted operating cash flow of $17.4M. These figures were substantially better than the Q1 numbers of 2023.

Figure 2 - Source: Argonaut Q2-23 Earnings Release

In the end of Q2, the company had $71.8M in cash and a net debt position of $151.6M. Given the constructive gold price above $1,900/oz now and Magino ramping up production, the net debt position is likely to improve during the second half of the year. One of the main near-term priorities will, apart from ramping up Magino, be to deleverage over the coming years.

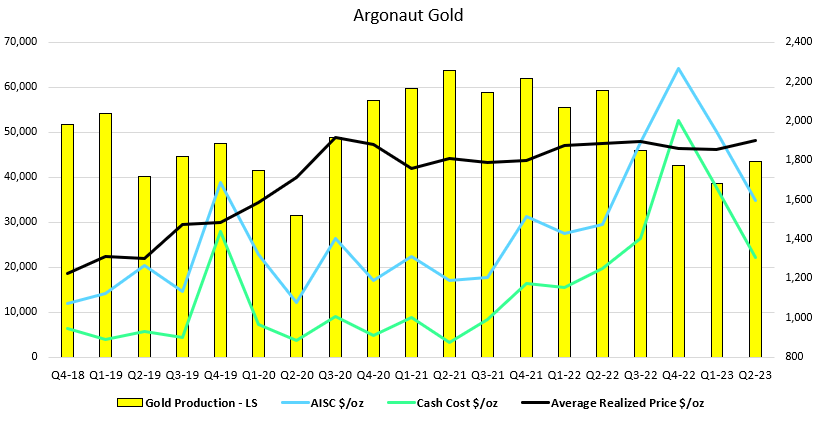

We can in the chart below see that the production volume, of 43,492 gold equivalent ounces, increased slightly compared to Q1. While both the cash cost of $1,304/oz and AISC $1,594/oz are down substantially compared to Q1.

Figure 3 - Source: Argonaut Gold Quarterly Reports

{kind=link}

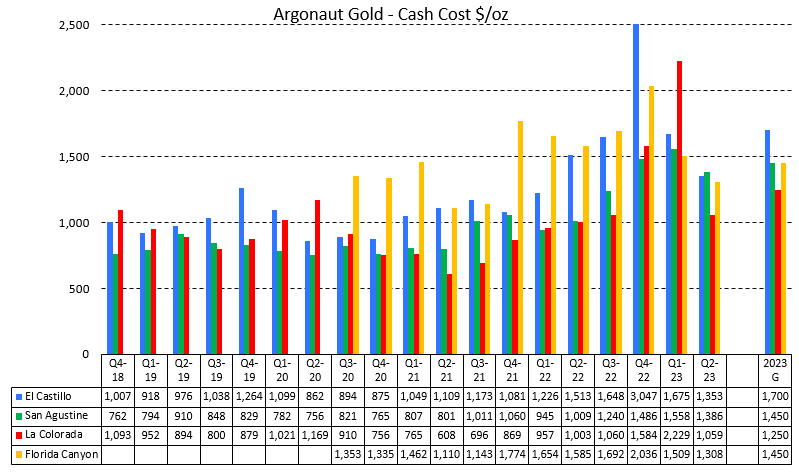

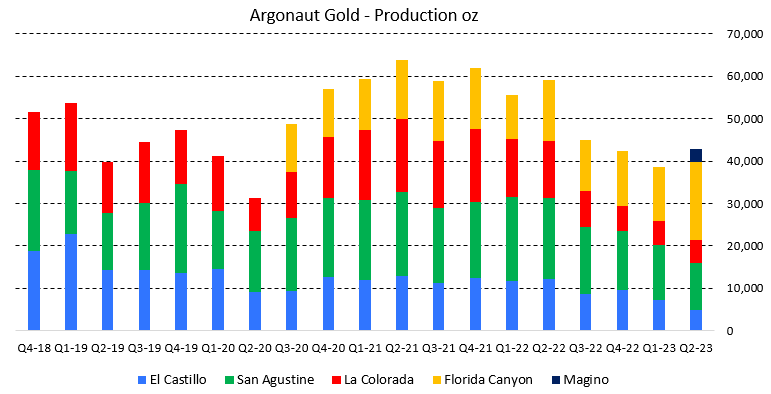

Among the various mines, we have seen quarter-over-quarter improvements with regards to costs for all the mines, which is of course very positive. The production figures are a somewhat mixed where Florida Canyon is tracking guidance, while La Colorada has had weaker production numbers, even if that is partly to be expected due to more stripping in the first half of the year. Both San Agustin and El Castillo are at this point tracking production numbers above the guidance range.

Figure 4 - Source: Argonaut Gold Quarterly Reports Figure 5 - Source: Argonaut Gold Quarterly Reports

{kind=link}

{kind=link}

We will likely have to wait until Q3 at least until Magino has sufficient production, for us to judge it against guidance. However, it is fair to say Magino has had a very welcomed contribution of 3,296 gold equivalent ounces in Q2. Keep in mind that the first gold pour was as recently as mid-June.

Valuation

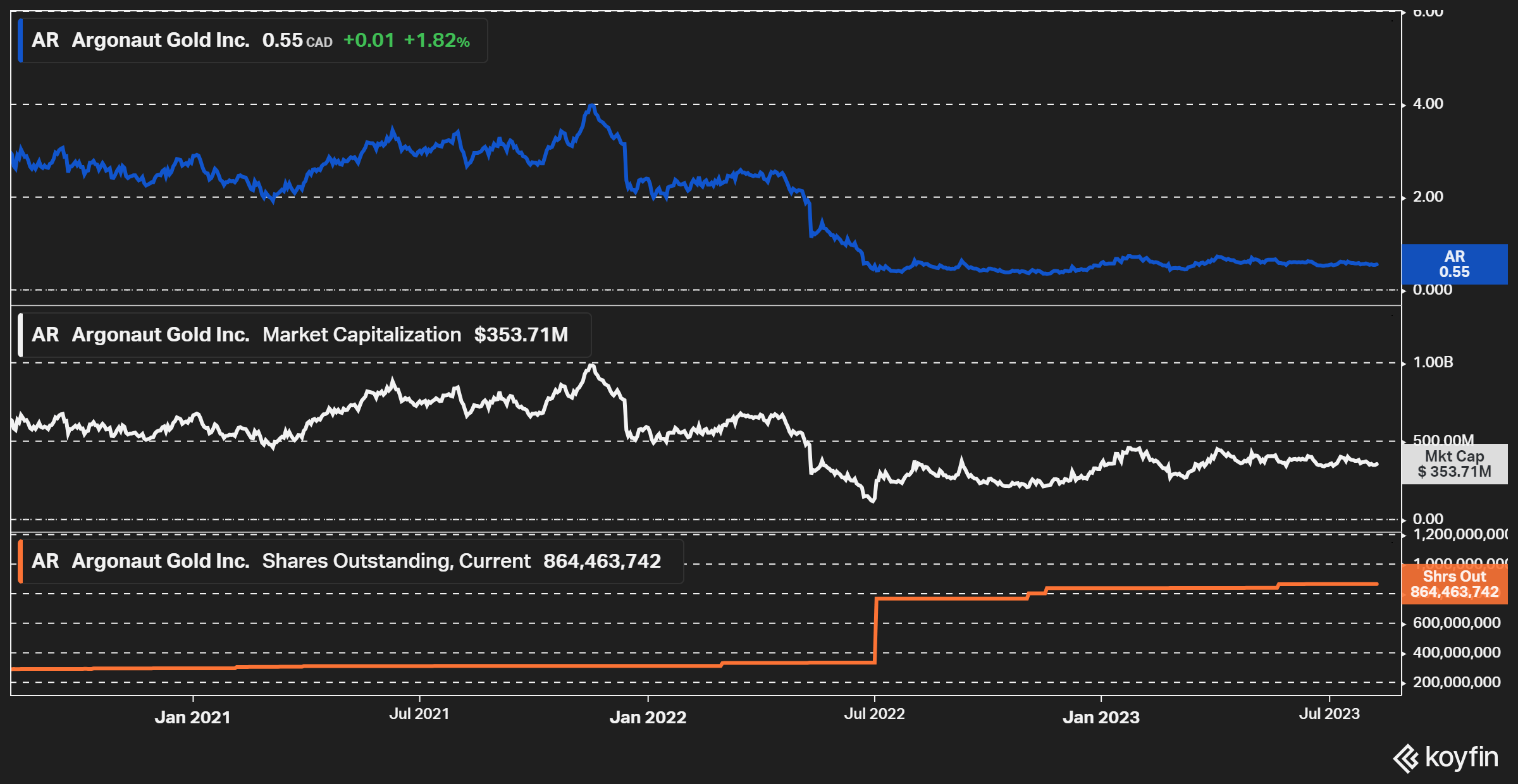

Argonaut Gold does, with the latest share price and the financials as of Q2, have a market cap of $353M and an enterprise value of $555M. Where I have added the convertibles to the net debt position here.

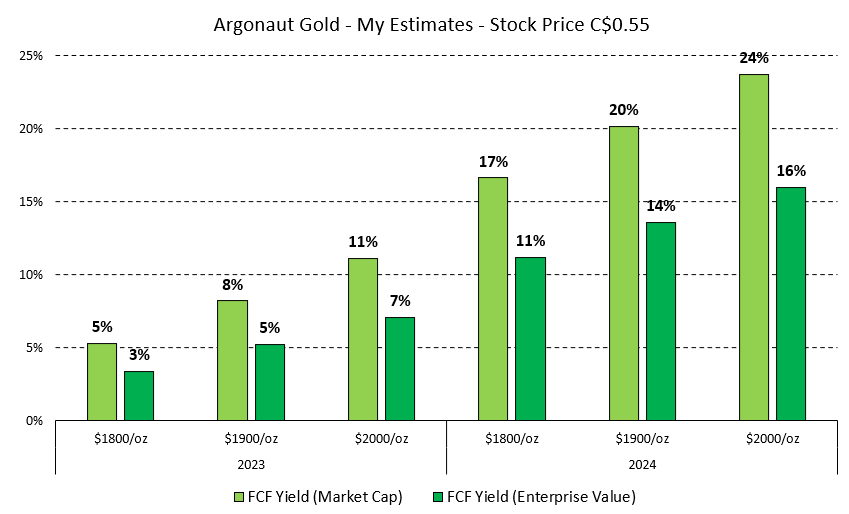

The 2023 guidance remains unchanged, with the exception of $10M more in CAPEX for 2023, I haven't had to make any other material changes to my estimates. If we disregard the construction capital in 2023 at Magino, Argonaut does today trade with a free cash flow yield of 8% using the market cap and a $1,900/oz gold price.

However, things get far more interesting in 2024, when we will have a full year of production from Magino, where the free cash flow yield is likely to more than double, to around 20% using the market cap and a $1,900/oz gold price.

Figure 6 - Source: My Estimates

{kind=link}

Do note that I am only assuming 20,000 gold ounces from residual leaching in 2024 from the Mexican assets, while it now looks more likely that production will continue into 2024, at least at San Agustin.

Figure 7 - Source: Argonaut Gold Earnings Release

{kind=link}

Risks & Conclusion

Many long-term shareholders of Argonaut have suffered following some poor management decisions over the years and I do not think we are likely to see the highs of 2021 around C$4 any time soon, given the large increase in the number of shares lately.

Having said that, I do think a market cap around $1B, which we saw in 2021 is a realistic target in a few years. That would imply a substantial upside to shareholders from current levels, which is of course dependent on a successful ramp-up of Magino and some deleveraging, as the financial leverage is presently a bit too high for comfort.

{kind=link}

It is relatively common to see delays for new mines to reach their nameplate capacity. If that were to happen for Magino, it would at the very least force Argonaut to operate with a high financial leverage for longer than what at least I would prefer. Where the company in Q2 already had to obtain a waiver on certain financial covenants on its financing package. At this point, I think the risk of a more substantial delay is relatively low, but it is still a risk to consider.

Another possible risk would be more of a general disruption to operations at either Magino or Florida Canyon, which is also a relatively low-probability event. However, the problem of now having its production more concentrated and at least in the near term operating with a high financial leverage, means the impact of such an event could be far more severe that what we saw when in the spring of 2020, when Argonaut halted mining at stacking at its Mexican operations for about a month. Such an event could force the sale of assets at distressed values, a very large equity financing, and/or default.

As a mining company, the commodity price risk is always worth considering as well, but a lower gold price would partly be offset by the hedges which were required to get the financing package approved.

Figure 9 - Source: Argonaut Gold Q2-23 MDA

All-in-all, an investment in Argonaut is not without risk at this point, but given the very attractive valuation together with how far along Magino is at this point, I view the risk reward as very favorable.

For further details see:

Argonaut Gold: Substantial Improvements In Costs During Q2 Compared To Q1