ARHS - Arhaus Continues Footprint Expansion (Rating Upgrade)

2023-12-19 16:54:13 ET

Summary

- Arhaus, Inc. is an omni-channel retailer of premium quality home furnishings.

- The global furniture market is expected to reach $785 billion by 2027, driving growth opportunities for Arhaus.

- Arhaus' recent financial trends show growing revenue but a drop in earnings due to startup costs from new showroom openings.

- My outlook on Arhaus, Inc. stock is a Buy.

A Quick Take On Arhaus

Arhaus, Inc. ( ARHS ) is an omni-channel retailer of premium quality home furnishings.

I previously wrote about Arhaus in July 2023 with a Hold outlook on expected slowing revenue growth.

Given the company's continued expansion efforts, strong balance sheet , cash flow and a discounted cash flow calculation that suggests the stock is undervalued, my outlook on ARHS is a Buy.

Arhaus Overview And Market

Ohio-based Arhaus sells "heirloom quality, artisan-made furniture and decor" products via an omnichannel approach.

The firm is led by co-founder and CEO John Reed, who has been with the firm since inception and had previously stepped out of the CEO role only to have to step back in when new CEO Adrian Mitchell resigned in 2019 after only one year on the job.

The company’s primary offerings include:

-

Furniture

-

Accessories

-

In-Home Design Services

-

Digital Tools.

Arhaus pursues an omni-channel business model, with over 75 retail stores and an online direct-to-consumer website and ordering capabilities.

Management has said it intends to open "between five and seven new stores per year for the foreseeable future."

Per a 2021 market research report by Global Market Insights, the global market for furniture was an estimated $546 billion in 2020 and is expected to reach $785 billion by 2027.

This represents a forecast CAGR of 5.4% from 2021 to 2027.

The primary reasons for this expected growth are a continued growth in the development of new residential projects and "ongoing smart city developments."

Also, below is a chart showing the global furniture market at a glance:

Global Market Insights

The U.S. furniture market is highly fragmented, with over 23,000 retail furniture establishments.

The company competes with a wide variety of national and regional retailers, department showrooms, mail-order catalogs, interior design trade showrooms and others.

Arhaus’ Recent Financial Trends

Total revenue by quarter (blue columns) has continued to grow year-over-year due to growing showroom volume; Operating income by quarter (red line) has dropped in the most recent quarter because of higher SG&A expenses and lower gross margin from its expanded showroom footprint.

Seeking Alpha

Gross profit margin by quarter (green line) has proceeded with no discernible trend in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have risen in Q3 2023 due to a $10 million donation to the Nature Conservancy and higher selling expenses related to new showroom openings.

Seeking Alpha

Earnings per share (Diluted) have dropped materially in the most recent quarter, as the chart shows below:

Seeking Alpha

(All data in the above charts is GAAP.)

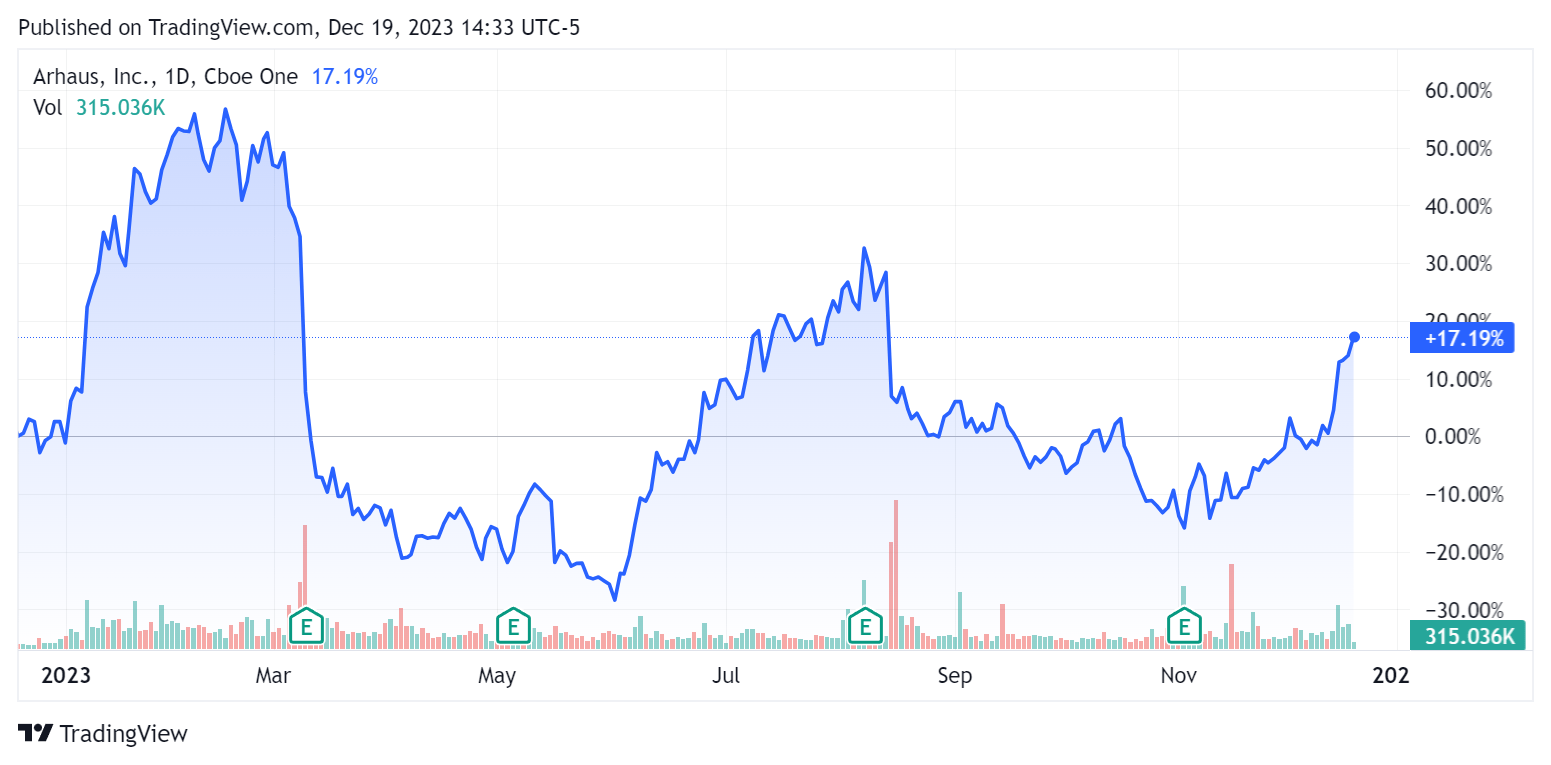

In the past 12 months, ARHS’s stock price has shown high volatility and has risen by a net of 17.19%:

{kind=link}

For balance sheet results, the firm ended the quarter with $236.9 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $89.6 million, during which capital expenditures were $58.0 million. The company paid $7.4 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Arhaus

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 1.3 |

| Enterprise Value / EBITDA |

| 8.0 |

| Price / Sales |

| 1.2 |

| Revenue Growth Rate |

| 17.0% |

| Net Income Margin |

| 10.9% |

| EBITDA % |

| 16.6% |

| Market Capitalization |

| $1,510,000,000 |

| Enterprise Value |

| $1,730,000,000 |

| Operating Cash Flow |

| $147,580,000 |

| Earnings Per Share (Fully Diluted) |

| $1.01 |

| 2023 FWD EPS Estimate |

| $0.84 |

| Free Cash Flow Per Share |

| $0.64 |

| SA Quant Score |

| Buy - 4.05 |

(Source - Seeking Alpha.)

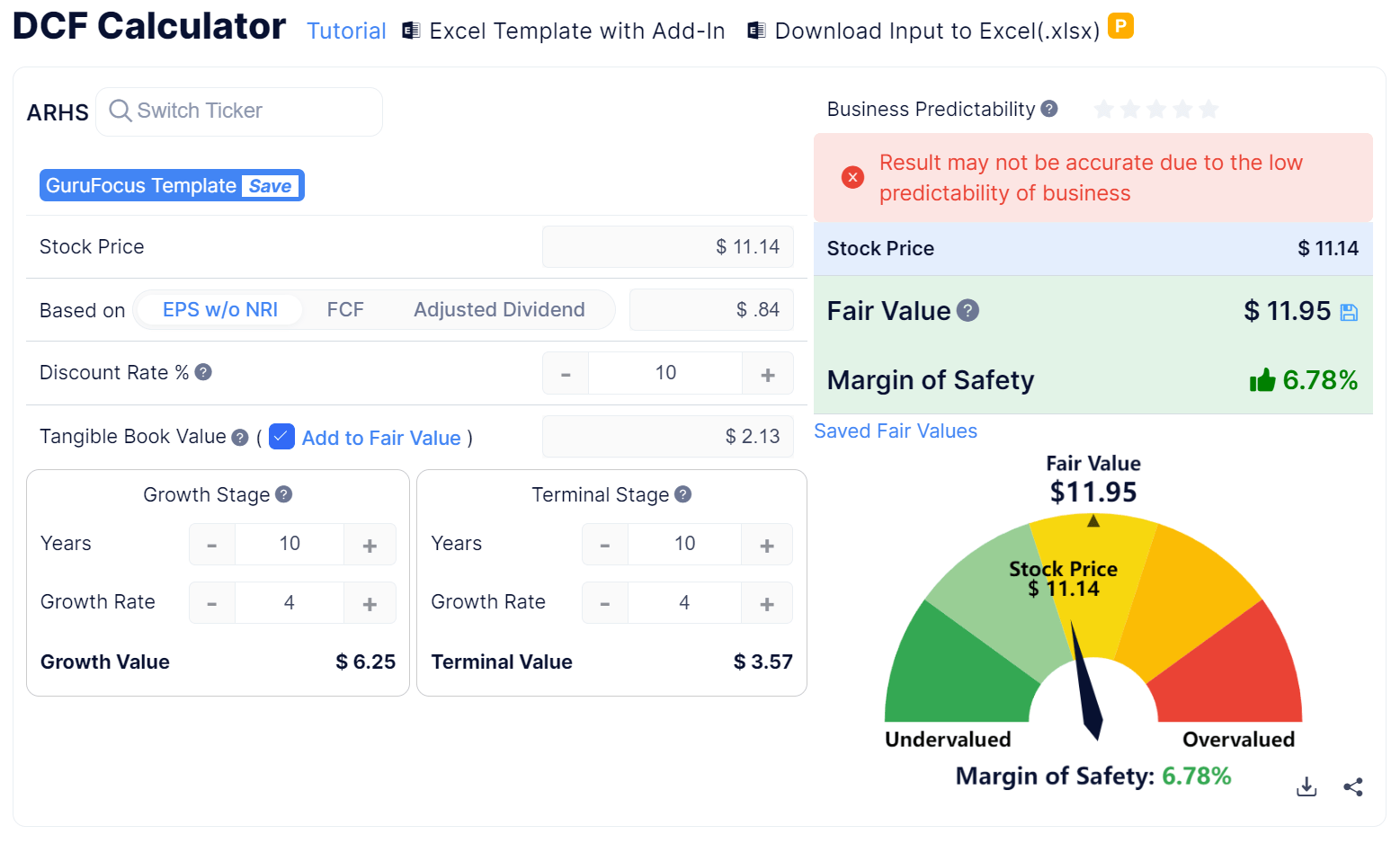

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Based on the DCF, using a discount rate of 10% (10-year Treasury (US10Y) at 4% plus 6% equity risk premium) and forward earnings per share assumption of $0.84, the firm’s shares would be valued at approximately $11.95 versus the current price of $11.14, indicating they are potentially currently undervalued by about 6.8%.

Commentary On Arhaus

In its most recent earnings call (Source - Seeking Alpha ), management’s prepared remarks highlighted its revenue growth but also noted a YoY reduction in earnings due to the costs from its new showroom openings.

Year to date, the company has opened eight new showrooms located in premium demographic locations.

In 2024, the firm is expecting to add 6 - 8 new full showrooms, 2 - 3 outlet locations and ten relocations, expansions or renovation projects.

Analysts questioned the leadership about backlog action, new store performance and margin impacts.

Management said that it expects to work through its product backlog by the end of 2023.

Leadership also said it was happy with 2023’s new store performance, which has been equal to or above their expectations. It expects the same from its 2024 new store cohort.

Margin impacts were due to greater sales from "price action" products, but management believes its brand awareness is growing due to its broader showroom footprint.

For the quarter’s results, total revenue rose 1.9% year-over-year, while gross profit margin slid 0.8%.

Selling and G&A expenses as a percentage of revenue increased by 6.6% YoY and operating profit fell by 49.3% due to the aforementioned gross profit compression and greater SG&A costs from store openings and higher sales expenses.

The company's financial position is quite strong, with plenty of liquidity, no debt and strong positive cash flow.

Looking ahead, 2024 full-year revenue growth is expected to be around 4.2% from consensus estimates.

In the past twelve months, the firm's EV/EBITDA valuation multiple has fallen by about 25%, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include improved revenue growth from new showroom openings and reduced expense recognition from backlog sell-through.

Given the company's strong balance sheet, cash flow and a discounted cash flow calculation that suggests the stock is undervalued, my outlook on ARHS is a Buy.

For further details see:

Arhaus Continues Footprint Expansion (Rating Upgrade)