APLT - ARISE-HF Phase 3 Trial Likely To Disappoint Due To Multiple Red Flags

2024-01-04 11:37:10 ET

Summary

- Applied Therapeutics has encountered significant valuation challenges since its IPO, primarily due to the limited efficacy of its Aldose Reductase Inhibitors (ARI) franchise.

- The company is expected to release topline data from ARISE-HF, a phase 3 trial examining AT-001 efficacy in DbCM in Q4 2023.

- Several red flags and the possibility of a disappointing data readout do not inspire confidence.

- Failure of many ARIs in the past led to our lack of confidence in AT-001 success.

Introduction

Applied Therapeutics, Inc. (APLT), a Delaware-based small clinical-stage biotech company established in January 2016 under the leadership of CEO Shoshana Shendelman, has encountered significant valuation challenges since its initial public offering on May 13th, 2019. To date, the company's value has diminished by approximately 70%, a downturn primarily linked to the limited efficacy of its Aldose Reductase Inhibitors ((ARI)) franchise. Applied Therapeutics' strategy was to refine previously tested small molecules, leveraging advancements in drug design to enhance efficacy while reducing side effects and toxicity. The focus remains predominantly on ARIs, although noteworthy success in their targeted areas remains elusive.

Particularly telling is the case of AT-007, an inhibitor that did not demonstrate significant results in a phase 3 study for Galactosemia, leading to expressed frustrations over the FDA's requirement for clinical outcomes data in addition to biomarker changes for potential approval. Despite these hurdles, the company has resolved to pursue New Drug Application (NDA) filings in both the US and Europe.

Our analysis, however, pivots away from the Galactosemia case to concentrate on the impending release of topline data from the phase 3 ARISE-HF study. ARISE-HF, examining Diabetic Cardiomyopathy (DbCM) - a condition affecting a considerably larger demographic than Galactosemia - offers a more substantial market potential. The study evaluates AT-001 (Caficrestat), a carboxylic acid aldose reductase inhibitor structurally similar to AT-007, against a placebo control. While Applied Therapeutics' leadership exhibits optimism, citing improvements in primary endpoints for a third of the patients in blinded data, our analysis adopts a more cautious stance. We aim to elucidate potential pitfalls that could culminate in an unfavorable outcome for the phase 3 trial. Prior to delving into these complexities, we will provide a brief overview of the drug's mechanism of action and the design of the trial.

AT-001 and DbCM

Applied Therapeutics touts AT-001 as a significant advancement over conventional Aldose Reductase Inhibitors such as Zapolrestat, Ponalrestat, Epalrestat, and Tolrestat . The company highlights AT-001's enhanced selectivity and affinity , paired with its diminished penetration into the central nervous system. This inhibitor is designed to target the binding pocket of aldose reductase, a key enzyme in the polyol pathway, which is believed to be excessively active in diabetic patients under hyperglycemic conditions. This overactivity is linked to increased sorbitol concentrations and reactive oxygen species (ROS) production , both implicated in cellular damage.

Several preclinical studies have shown that ARIs, AT-001 included, can effectively inhibit aldose reductase, thereby reducing serum sorbitol levels in a dose-responsive manner. Similar outcomes were observed in earlier human clinical trials involving first-generation ARIs. While the underlying mechanism of AT-001 is clear and aligns with theoretical expectations, the real question remains: Can such biochemical activity translate into clinically meaningful outcomes?

DbCM represents a complex cardiac disorder in diabetic individuals , marked by a series of pathophysiological changes such as ventricular dilation, heart cell enlargement, significant interstitial fibrosis, and altered systolic function amidst diastolic dysfunction. Over time, DbCM can progress to heart failure ((HF)), a debilitating state where the heart struggles to effectively circulate blood. Applied Therapeutics posits that by mitigating myocyte stress triggered by the overactive polyol pathway, AT-001 could enhance cardiac function. This hypothesis is supported by observed improvements in cardiac energetics and a decrease in mitochondrial ROS in animal models. The phase 3 trial, ARISE-HF, is the company's initiative to determine if AT-001 can replicate these effects in humans, potentially offering a new therapeutic avenue for DbCM management.

ARISE-HF

Applied Therapeutics initiated a substantial study ( NCT04083339 ) involving around 700 patients in a stratified, blinded, randomized, and placebo-controlled trial. This 1:1:1 trial design compares a placebo with two dosages of AT-001 (1000mg and 1500mg, administered twice daily). The principal metric for evaluation is peak functional oxygen capacity, gauged by the change in peak VO2 measured during a Cardiopulmonary Exercise Test ((CPET)) from baseline to the 15-month mark. Supplementary endpoints encompass the progression to stage C heart failure, alterations in NT-proBNP levels, and variations in the Kansas City Cardiomyopathy Questionnaire ((KCCQ)) scores. The study's objective is to identify a minimum of a 6% difference between the treatment groups and the placebo, a benchmark informed by prior research correlating such a change with reduced progression risk to heart failure.

The foundation for this trial is predominantly built on pre-clinical data, including biomarker studies and insights from Pfizer's previous development of an ARI, Zapolrestat. To critically evaluate Applied Therapeutics' optimism, it is imperative to comprehend the intricacies of the primary outcome-its nature, influencing factors, and the potential impact of AT-001's mechanism of action on it. Peak VO2 , often misconstrued as max VO2, is essentially the maximum volume of oxygen utilized during a specific type of intense physical activity, like that measured in CPET for ARISE-HF. This parameter can be broken down via Fick's equation: peak VO2 = Cardiac Output (Heart Rate x Stroke Volume) x Arteriovenous Oxygen Difference (?-AVO2). The equation underscores the factors impacting peak VO2; increases in heart rate, stroke volume, or ?-AVO2 (the muscle's capacity to extract and utilize oxygen) will escalate the peak VO2.

While preclinical studies cited by Applied Therapeutics show promising improvements in cardiac energetics, reduced cardiac tissue fibrosis, and decreased cellular oxidative stress, the translation of these outcomes from animal models to human clinical trials is not straightforward. We do not anticipate these improvements to significantly influence ?-AVO2 or heart rate. There's a possibility of enhanced stroke volume, indicated in part by Zopolrestat studies, which might result from alleviating high sorbitol concentrations and the reductive intracellular environment, thereby potentially enhancing the overall contractility of cardiac tissue. Notably, heart rate is unlikely to be impacted by AT-001's mechanism and typically decreases with age-a factor contributing to the natural decline in peak VO2.

Initially, Applied Therapeutics posited that AT-001 would primarily decelerate or halt the regression of peak VO2, rather than reverse it. However, as the trial progressed and the company analyzed the blinded data, their expectations appeared to grow. Amidst the uncertainties, one clear aspect emerges: the initially anticipated modest efficacy reflects the complexity and variability inherent in the disease's progression and its cellular dynamics.

Red Flags

In this section, we scrutinize various aspects that bear upon the potential success of Applied Therapeutics' ARISE-HF trial. The company, in numerous presentations, has asserted that AT-001 either maintains or elevates the pharmacological efficacy of traditional ARIs, while simultaneously diminishing adverse, non-target effects. This renewed interest in ARIs, a class of drugs explored previously in the 80s and 90s, is predicated on the premise set by Pfizer's Zopolrestat.

AT-001 and Zapolrestat Structure (APLT Sep 2023 IP)

Presumably, although Zopolrestat demonstrated efficacy, it suffered from a suboptimal safety profile. Currently, Epalrestat stands as the sole clinically utilized ARI, approved in Japan for diabetic neuropathy nearly four decades ago. Pfizer's decision to discontinue Zopolrestat's development in the US, citing inadequate data and high levels of hepatotoxicity (as claimed by Applied Therapeutics), adds another layer of complexity. Some early 2000s studies indicate Zopolrestat's failure was also due to insufficient efficacy , a point partially conceded by Applied Therapeutics, which highlights AT-001's enhanced activity based on preclinical in-vitro enzyme inhibition data.

However, the possibility that advanced neuropathic stages in Zopolrestat's trials were beyond reversal, and thus unresponsive to treatment, raises concerns about AT-001's efficacy in Diabetic Cardiomyopathy (DbCM). With the targeted DbCM population exhibiting a median peak VO2 of ~15 mL/kg/min, indicative of low physical activity levels, and a high likelihood of advancing to stage C heart failure, there is apprehension that the pathologic alterations might be too advanced for an aldose reductase inhibitor to yield clinical benefits. Furthermore, the validity of the data supporting AT-001's testing in DbCM, derived from a distinct population and methodology with smaller sample sizes, could be questioned. The phase 2 Zopolrestat trial, involving approximately 70 participants notably younger than those in ARISE-HF, showed cardiac output stabilization over a year, contrasting with declines in the placebo group, primarily attributed to increased stroke volume - aligning with AT-001's proposed MOA. Despite these promising signs, the disparity in methodology, the imbalance in participant demographics between treatment and placebo groups, and the small scale of the trial, suggest caution in interpreting these findings as definitive predictors of ARISE-HF's outcomes.

Moreover, the differences in ARISE-HF from Pfizer's phase 2 trial are double-edged, offering both potential benefits and concerns. The uniqueness of ARISE-HF, compared to prior studies, might be seen optimistically by Applied Therapeutics but also raises cautionary flags from a more conservative viewpoint. Adding to this is the discontinuation of Ponalrestat , an ARI structurally akin to AT-001, due to its lack of efficacy. The decision to invest substantially in a phase 3 trial based on dated and inconclusive phase 2 data and an abandoned drug does not inherently inspire confidence.

In a recent address , the CEO's description of the blinded data as "exciting," showing an equal distribution of improvement, stabilization, and decline in primary outcomes mirroring the trial's arm structure, could suggest drug efficacy. Yet, the true allocation of these responses remains concealed. The possibility that any recipients could exhibit improvements in VO2peak is not to be overlooked, especially given the differing characteristics of the ARISE-HF population from those in long-term decline studies . Additionally, the potential influence of other medications, taken by a significant subset of participants, on peak VO2 needs careful consideration. One study identified improvements in peak VO 2 related to Dapagliflozin (SGLT2) administration, theorized to arise from improved cellular iron availability. Such scenarios, coupled with the blind nature of the trial, might contribute to the observed outcomes, warranting a meticulous analysis of the trial data upon unblinding.

Furthermore, there are critical considerations regarding the decline rates in peak VO2, previously extrapolated from disparate population studies. The cohort in ARISE-HF, classified as pre-type B heart failure, does not align well with most cross-sectional studies that have historically tracked peak VO2 reductions over extended periods. This discrepancy raises questions about the applicability of these decline rates to the ARISE-HF population. It is important to note that the multitude of medications administered to participants could potentially impact the three components of Fick's equation, which governs peak VO2. Additionally, the influence of physical fitness levels on peak VO2 cannot be overlooked.

Applied Therapeutics' assertion that peak VO2 is an appropriate endpoint, ostensibly unaffected by exercise levels, invites scrutiny. Evidence suggests that while exercise may not alter the rate of decline in max VO2, it can certainly affect its absolute value. Such nuances are particularly relevant in a study spanning 15 months, where even slight variations can be significant. The company's reference to a 6% change in peak VO2, based on an unblinded, randomized trial , further complicates the analysis. This cited difference, although statistically significant, was presented without elaborating on its clinical impact. Each observed 6% reduction in peak VO2 correlated to a 4% decrease in risk of cardiovascular mortality or cardiovascular hospitalization, presenting a delicate balance between potential efficacy and the likelihood of adverse effects (AT-001 was considered safe in a prior study, but the phase 3 data could report new trends). This complexity does not lend itself to straightforward FDA approval or a clear-cut decision-making process for clinicians.

Moreover, the reliance on a single phase 3 study, despite its potential success and anticipated efficacy levels, may fall short of the FDA's stringent approval criteria. Typically, the agency requires either two phase 3 studies with p-values below 0.05 or one study with a more robust p-value below 0.0025. The regulatory response, even in the face of positive results, will likely hinge on the robustness of the data, potentially necessitating further costly investigations for a trial of this magnitude.

A pivotal concern with AT-001 is its reliance on biomarker-driven data and the seemingly tenuous link between the drug's mechanism of action and tangible clinical outcomes. When considering the array of inconsistencies and limitations in previous data, there is a palpable risk of an underwhelming outcome from the ARISE-HF trial. This analysis, aggregating various elements of past and current research, suggests a cautious approach to anticipating the trial's results.

Valuation and Cash Burn

The valuation of AT-001 presents a complex challenge, primarily due to uncertainties around its reception by clinicians and payers, notwithstanding Applied Therapeutics' optimistic stance. The company's projection of pricing AT-001 on par with medications like Entresto and SGLT2 inhibitors, at an annual cost of approximately $4000 to $5000, serves as a basis for our financial modeling.

Our valuation approach employs a Discounted Cash Flow ((DCF)) model, grounded in cautious assumptions, with a sales projection extending to the expiration of the primary patents. This conservative methodology reflects the potential limitations of AT-001's clinical benefits, which could subsequently impact sales trajectories. A crucial factor in our model is the estimated target population. The prevalence of Diabetic Cardiomyopathy among individuals with Type 2 Diabetes is subject to variation, as indicated by diverse studies. Consequently, our model adopts a more restrained estimate, targeting a U.S. population that constitutes 33% of the company's projected figure, roughly equating to 2 million individuals.

Incorporating a modest market penetration rate of 3%, a discount rate of 10%, and a gross margin of 40%, our analysis extends to the primary patent's expiration in 2031. Under these parameters, we approximate the value of AT-001 to be ~$500M. This valuation not only factors in the direct financial aspects but also cautiously weighs the potential market dynamics and the drug's clinical positioning in the evolving landscape of DbCM treatment.

| Year |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| 2031 |

| 2032 |

| 2033 |

| 2034 |

| Revenue |

| 100 |

| 200 |

| 230 |

| 232 |

| 235 |

| 237 |

| 239 |

| 242 |

| 12 |

| 1 |

| 0 |

| COGS |

| 40 |

| 80 |

| 92 |

| 93 |

| 94 |

| 95 |

| 96 |

| 97 |

| 5 |

| 0 |

| 0 |

| Gross Profit |

| 60 |

| 120 |

| 138 |

| 139 |

| 141 |

| 142 |

| 144 |

| 145 |

| 7 |

| 0 |

| 0 |

| Tax |

| 11 |

| 23 |

| 26 |

| 26 |

| 27 |

| 27 |

| 27 |

| 28 |

| 1 |

| 0 |

| 0 |

| Net Income |

| 49 |

| 97 |

| 112 |

| 113 |

| 114 |

| 115 |

| 116 |

| 117 |

| 6 |

| 0 |

| 0 |

Applied Therapeutics, with a current market capitalization slightly above $250M, presents a nuanced financial picture when considering the potential exercise of outstanding warrants. The exercise of these warrants could significantly inflate the total share count, potentially elevating the market capitalization to around $300M. This hints at a market sentiment factoring in a 50-60% likelihood of AT-001's success. This probability encompasses the drug's prospects for regulatory approval and commercial viability, as inferred from the company's current market valuation and available data. Historically, phase 3 trials succeed about ~60% of the time. This, however, is partially due to the less successful (about 30-40%) phase 2 data, which proceeds the trials. When accounting for the lack of previous phase 2 study and confidence based on Pfizer's failed Zopolrestat and biomarkers, we believe the likelihood of success is below the current market's anticipated range.

As of Q3 2023 , Applied Therapeutics reports a net cash reserve of approximately $37M. The company's funding strategy, primarily through public offerings, has led to a notable level of share dilution. With the completion of the ARISE-HF trial, there may be a reduction in associated expenses. Nonetheless, upcoming costs related to data analysis, potential regulatory meetings, and other preparatory activities are expected to rise. Predicting the company's operating expenses for 2024 poses a challenge, but the existing cash reserves are unlikely to sustain operations beyond the next year. Consequently, it seems highly probable that Applied Therapeutics will seek additional funding avenues to secure the necessary capital.

The company's current stance, with 77M outstanding shares and the issuance of 32M pre-funded warrants and 30M common warrants between 2022 and 2023, sets the stage for a substantial increase in share count. While ownership percentage limits on warrant exercises are a factor, even a partial exercise of these warrants in the near term could push the number of outstanding shares well beyond the present 77M.

When reporting its net loss per share, Applied Therapeutics used a base of 90M shares, accounting for both the outstanding warrants and option contracts. Utilizing this adjusted share count for market capitalization calculations produces an approximate value of $300M. This recalibrated figure more accurately reflects the company's market value, considering the dilutive impact of the warrants and options, thereby providing a more holistic understanding of its financial standing.

Verdict

Navigating the potential challenges for ARISE-HF to serve as a pivotal success for Applied Therapeutics is fraught with complexities. A primary concern is the modest efficacy historically associated with first-generation Aldose Reductase Inhibitors. Despite claims of improved binding affinity and selectivity for AT-001, there remains a degree of uncertainty about whether such enhancements will translate into significant clinical benefits. While past studies have indicated some efficacy of ARIs, they frequently fell short of achieving meaningful endpoints. The Zopolrestat phase 2 study, which the company informally uses as a reference point, differs considerably in its design, raising the possibility that the more extensive and better-stratified AT-001 phase 3 study may show less efficacy due to regression to the mean.

Furthermore, the real-world significance of the study's endpoints, even if met, is subject to debate. Improvements in conditions like severe diabetes and myocardial dysfunction are undeniably valuable, yet these advancements must be weighed against factors such as drug pricing and any safety concerns. Additionally, success in the phase 3 trial does not guarantee FDA approval; the agency may demand more extensive evidence, particularly if the effects observed are not sufficiently pronounced.

Applied Therapeutics faces a precarious financial situation. To sustain operations, the company will likely need to secure additional funding, a task that could prove challenging if the ARISE-HF study does not meet expectations. The company's stock price has experienced a notable surge, increasing over 50% in the past month, a rise likely fueled by heightened investor interest in anticipation of the forthcoming catalyst. The current market capitalization, standing at approximately $300 million, reflects strong confidence in the phase 3 outcomes. This optimism may be influenced by the company's encouraging perspective on blinded data and prior biomarker research. Nonetheless, this optimism must be tempered with caution, as the distribution of responses in the blinded data does not have to align with the study's arms, and the predictive value of biomarkers has been historically overestimated in many clinical trials. Additionally, there has been no mention of the magnitude of the effect in the blinded data set, which is another key part of the study.

Our analysis, considering the breadth of available data, suggests that significant improvements in peak VO2 between the treatment and placebo groups are unlikely. The market's current valuation of Applied Therapeutics appears overly optimistic, leading us to a bearish stance on the stock. While a favorable study outcome holds potential for substantial upside, realizing AT-001's market potential likely involves hurdles beyond the ARISE-HF trial, casting doubt on the likelihood of the company's market capitalization surpassing $500M. Conversely, negative trial results could drastically impact the stock price. The company's broader pipeline, still in the exploratory phase and lacking imminent revenue generation, combined with the impending need for funding, could result in a significant reduction in market capitalization, potentially falling to or below $100M.

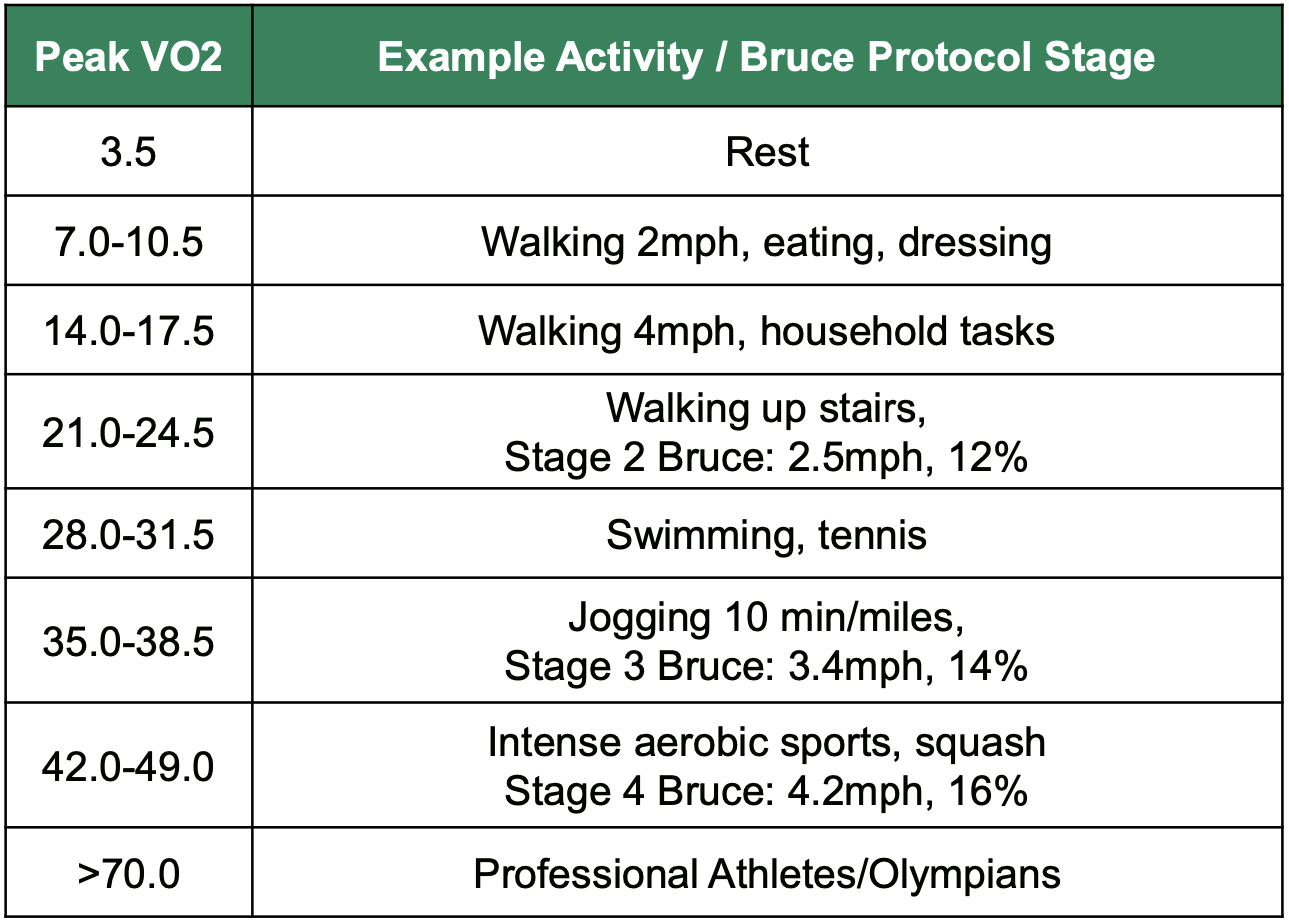

What would positive data mean for the stock? If the company reports strong topline data, with a highly statistically significant result, the market is likely to de-risk some of the drug value. Based on our assumptions, the company could reach valuations close to $500M. Strong statistical significance could make a case for the company to not require another phase 3 study to push for approval, however, the endpoint still remains questionable in terms of impact and QOL changes. The detectable change that the company often mentions is 6%, which in the case of the baseline data corresponds to ~1 mL/kg/min. To put this in real-life context, this would mean that even after improving 6%, the average patient would still stay in the "Walking 4mph/Household tasks" range.

peak VO2 Activity Levels (APLT Diabetic Cardiomyopathy forum presentation)

{kind=link}

Investment Strategy

We believe that buying derivative contracts offers a better risk-to-reward ratio. Short-term put options seem to be the most cost-effective, as the topline data is expected to be published soon (Q4 2023). January 19th $2.50 Put contracts are currently offered for a price of 40c/option, and in case of a significant drop, as anticipated in case of weak ARISE-HF data, could return up to 200% of the invested amount (~50-60% drop in stock value before expiry). IV crush could impact the profit level, however, if the stock were to drop significantly below the exercise price, the investor should still expect >100% gain and the drop is not certain, as the financial instability that might be fueled by weak data could warrant further volatility. In case of positive data, the contracts would likely expire worthless, but as opposed to opening a short position, the loss would not exceed 100%, and the owner would not be required to maintain a margin nor cover the costs of borrowing. While we do not expect the stock to gain over 100% in case of a "positive" readout, it is possible to approach levels close to that threshold, depending on the market sentiment and further guidance from the company. Our upside thesis could also be underestimated, as it is primarily based on our conservative and rational estimates.

For further details see:

ARISE-HF Phase 3 Trial Likely To Disappoint Due To Multiple Red Flags