ARKAF - Arkema: Anticipate A 15% EBITDA Increase In 2024

2023-09-04 04:30:00 ET

Summary

- Arkema will remain profitable and free cash flowing this year, but all eyes are on 2024.

- The company's Q2 2023 revenue decreased by 23% compared to Q2 2022, but the EBITDA margin remained at the projected 17.1%.

- Arkema's free cash flow performance is strong, with a net debt of just under 2.7B EUR and a debt ratio below 2 times the EBITDA.

Introduction

In an article published in January, I explained why I was bullish on Arkema ( ARKAF ) ( ARKAY ), a large French company in the chemical sector, focusing on adhesive solutions, coating solutions and advanced materials. While I realized 2023 would be a weaker year than the very strong 2022, I was charmed by the company’s projection for 2024 as the revenue and margin projections were pretty impressive. The share price is already up by about 17% while the company also paid a dividend of 3.4 EUR, representing just over 4% of the share price when the previous article was published. The total return of 21% is pretty decent in these markets.

{kind=link}

Arkema's primary listing is on Euronext Paris where the company is trading with AKE as its ticker symbol . The average daily volume in Paris is roughly 150,000 shares (for a monetary value of around 15M EUR). The company currently has approximately 74.7M shares outstanding resulting in a market cap of approximately 7.3B EUR. I will use the Euro as base currency throughout this article as Arkema trades in Euro and reports its financial results in Euro as well.

The margins are recovering

As stated in the introduction, I didn’t have particularly high hopes for 2023 and I mainly care about Arkema remaining on track to meet its guidance for 2024.

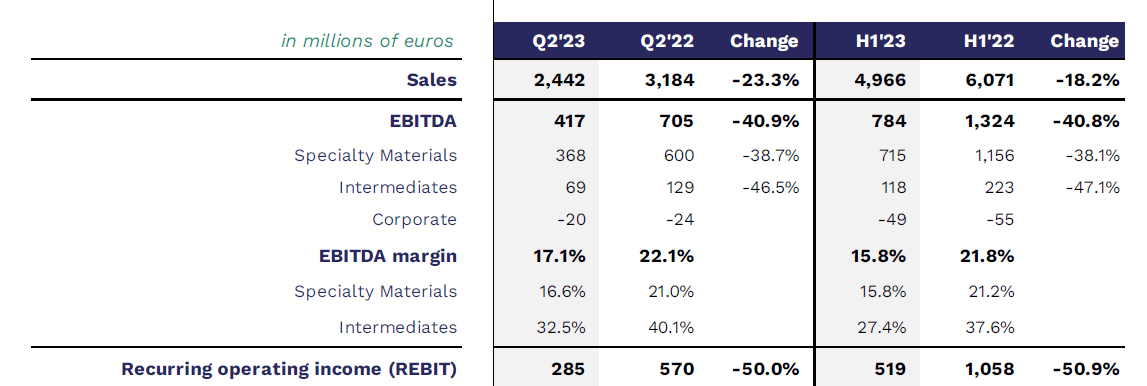

The total revenue in the second quarter decreased by approximately 23% from the Q2 2022 revenue, but this was widely expected as 2022 was a banner year for the company. Arkema is pointing towards weak demand and continuous destocking on the level of its end customers. And of course, as the revenue decreases, the EBITDA result is the first hit: the total EBITDA fell by about 40% from the (again, exceptionally high) result of 705M EUR in Q2 2022. But more importantly, the EBITDA margin came in at 17.1% which is the margin the company has been guiding to for its 2024 results. So margins are still more than okay. As you can see below, the Q2 EBITDA margin helped to compensate for the weaker margin in the first quarter of the year and the average EBITDA margin in the first semester was approximately 15.8%. Still below the 17% EBITDA margin guidance for 2024, but the first semester of this year also hasn’t been the most efficient period for the company due to the lower demand.

{kind=link}

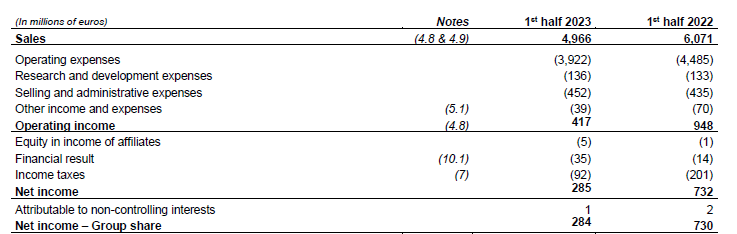

As shown in the image above, the total revenue in the first half of 2023 came in at just under 5B EUR, and this resulted in an operating income of 417M EUR, which is a decrease of more than 50% compared to the first half of 2022 (which, again, does not necessarily provide a fair comparison basis). And despite the substantial decrease in operating income, the company obviously remained profitable: the net income was approximately 285M EUR of which 284M EUR was attributable to the shareholders of Arkema.

{kind=link}

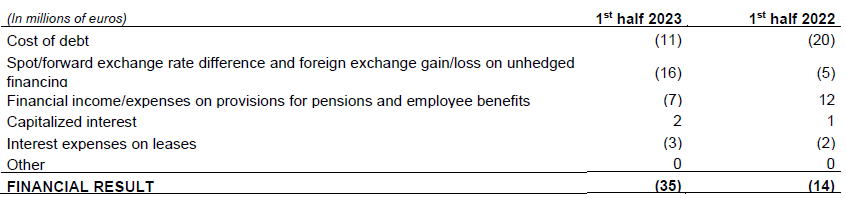

This represented an EPS of 3.73 EUR per share. Not brilliant, but as 2023 was generally seen as a transition year, it’s a decent result. Also keep in mind the net finance expenses of 35M EUR are substantially higher than the 14M EUR in H1 2022. That was perhaps somewhat surprising as the total interest expenses decreased, but as you can see below, there was a 19M EUR delta in the provisions for pensions and employee benefits while there was an additional 11M EUR ‘hit’ due to FX changes. This means the underlying earnings would have exceeded 4 EUR per share.

{kind=link}

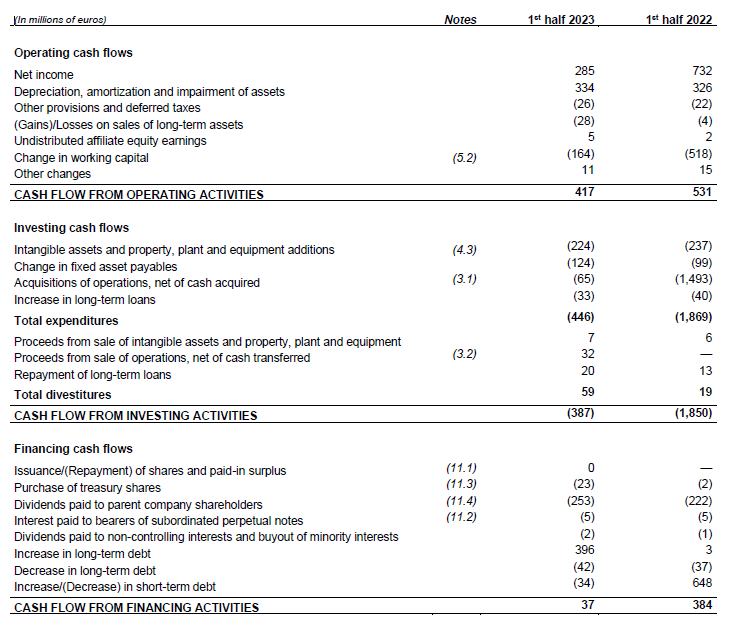

Those additional finance expenses are also non-cash items. The cash flow statement below indicates the operating cash flow was approximately 417M EUR, but this includes a 164M EUR investment in working capital items and excludes the 5M EUR in interest paid to the perpetuals and 2M EUR paid to non-controlling interests. This means that on an adjusted basis, the operating cash flow was approximately 574M EUR.

{kind=link}

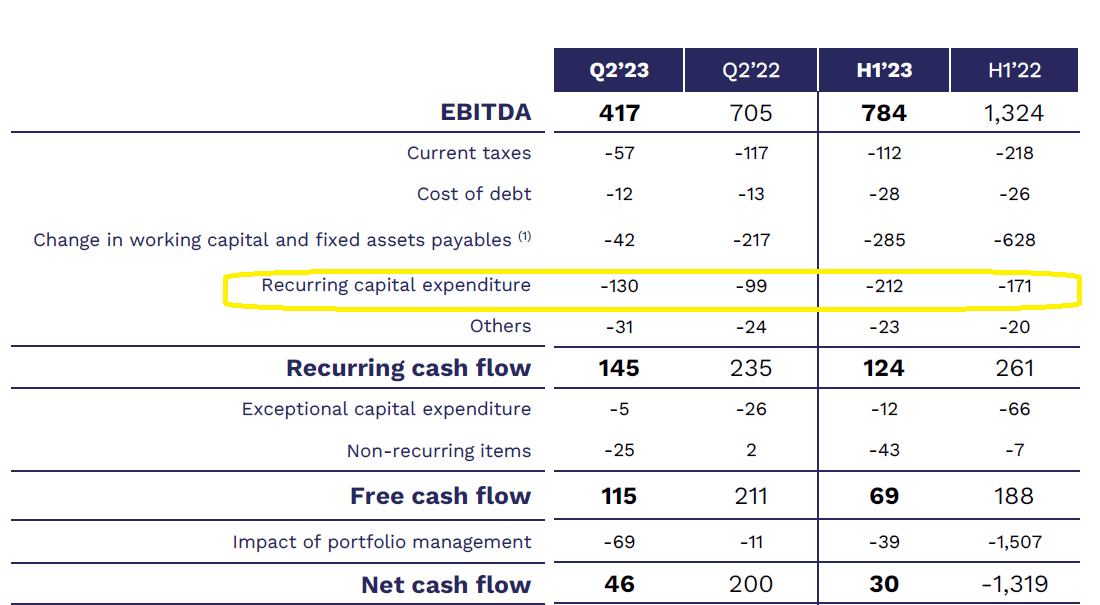

The total capex was approximately 348M EUR (including the increase in payables on fixed assets), resulting in a net free cash flow of 226M EUR. The image below shows the recurring capex was just 212M EUR, which means the underlying free cash flow result was quite a bit higher than the reported cash flow. Arkema continues to invest in growth with, amongst others, investments to supply anhydrous hydrogen fluoride to Nutrien ( NTR ) in the United States.

{kind=link}

Arkema’s free cash flow performance remains strong and as of the end of June, the balance sheet contained 1.67B EUR in cash and about 3.6B EUR in gross financial liabilities. The net debt was just under 2B EUR. And while that is an increase compared to the first half of 2022, this is related to A) the investment in working capital items and B) the payment of just over a quarter of a billion Euro in dividends in the first half of the year. Including the impact of equity-like deeply subordinated debt, the net debt level is 2.6-2.7B EUR.

Investment thesis

Considering Arkema anticipates a full-year EBITDA of 1.5-1.6B EUR, the debt ratio will remain firmly below 2 times the EBITDA, so there doesn’t appear to be a balance sheet risk here. Meanwhile, the stock is still trading at an EBITDA multiple of around 6.5 times on an enterprise value basis. And based on the 2024 projections, the EBITDA should increase by approximately 15% from the midpoint of this year’s guidance.

Using an EBITDA of 1.55B EUR for this year and considering the full-year depreciation expenses will be around 675M EUR, we can expect an EBIT of around 900M EUR. The net finance expenses will likely remain low as Arkema should start generating interest income on its cash pile while the vast majority of its financial debt consists of fixed rate bonds so the interest expenses will only increase very slowly. And the long-term debt on the secondary markets has a yield to maturity of less than 4% so the financial markets seem to be very happy with the credit risk of Arkema. I anticipate a pre-tax profit of 850M EUR and a net income of 640-675M EUR for an EPS of around 8-8.5 EUR per share. This should increase towards 10 EUR per share in 2024 as the company meets its mid-term targets.

I have been writing out of the money put options on Arkema and I will likely continue to do so. I currently have no position but could write additional options on any weakness in the share price.

For further details see:

Arkema: Anticipate A 15% EBITDA Increase In 2024