ARKAY - Arkema: French Powerhouse Trading At Just 4x The 2024 EBITDA

Summary

- Arkema is a French company active in the chemical sector.

- The company's 2022 will be exceptionally strong but the earnings and FCF result should not be extrapolated to 2023.

- Instead, I prefer to focus on the 2024 guidance. Based on that guidance, the stock is cheap.

- It's a volatile sector, and I don't think there's any rush to get in. But seeing how Arkema is trading at a 15% FCF yield for 2024, I am getting interested in picking up stock.

Introduction

Arkema ( ARKAF ) ( ARKAY ) is a French chemical company operating with adhesive solutions (sealants, flooring solutions), advanced materials (high performance polymers and performance additives) and coating solutions (paints, 3D printing,…) as its three most important pillars.

2022 will be a banner year for the company and 2023 will very likely be worse than this year's performance. But that's okay, as Arkema should be judged on its 2024 plans and realisations, as the company has set out very clear revenue and EBITDA targets. And based on that 'normalized' performance, Arkema is quite attractive.

{kind=link}

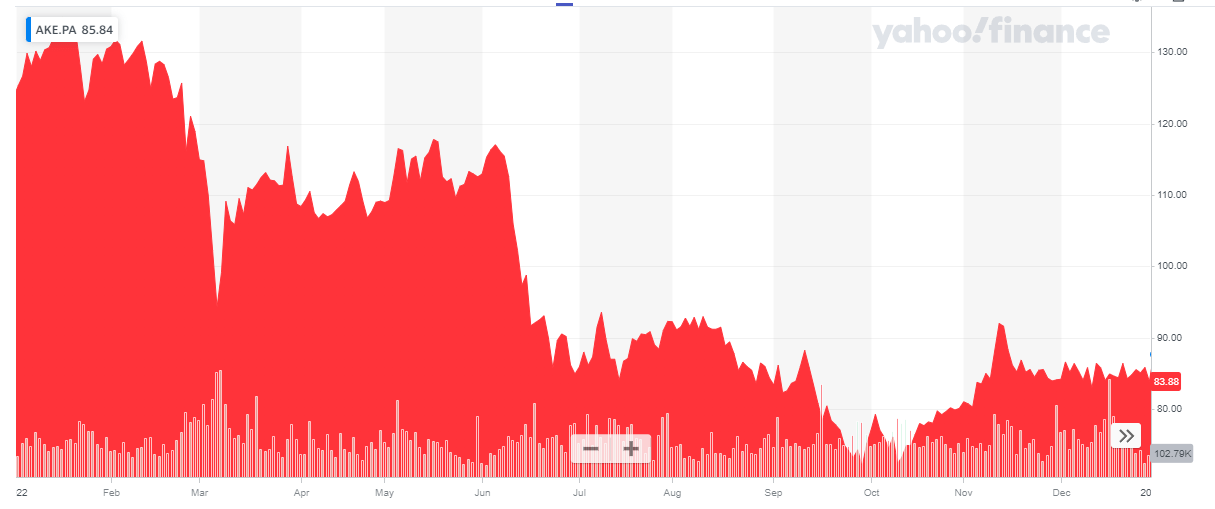

Arkema's primary listing is on Euronext Paris where the company is trading with AKE as its ticker symbol . The average daily volume in Paris is approximately 180,000 shares (for a monetary value of just over $17M). The company currently has approximately 75M shares outstanding after its recent offering to its employees , resulting in a market capitalization of approximately 6.6B EUR. I will use the Euro as base currency throughout this article.

2022 will be an excellent year

I will be relatively brief about the 2022 results for Arkema as those are not exactly representative as last year will prove to be an excellent year for Arkema.

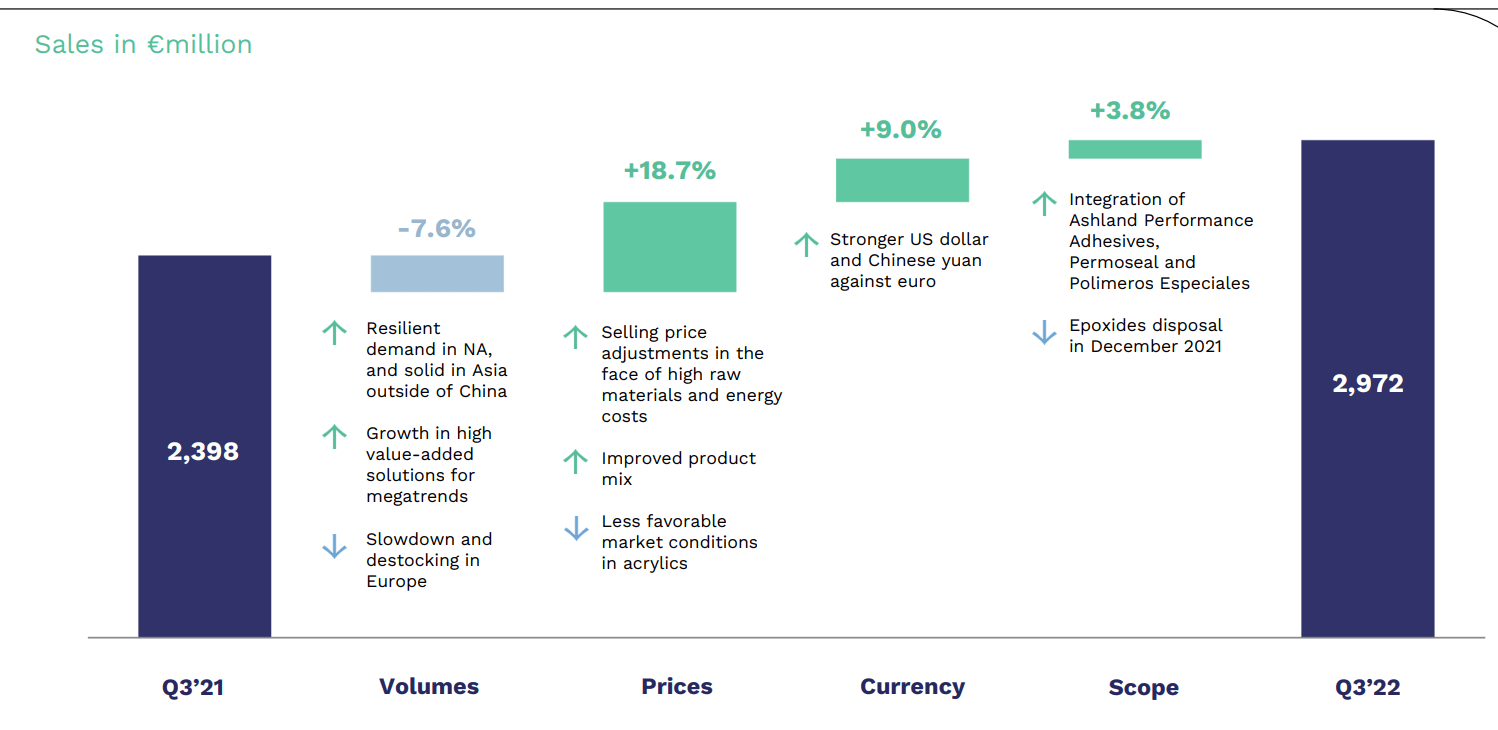

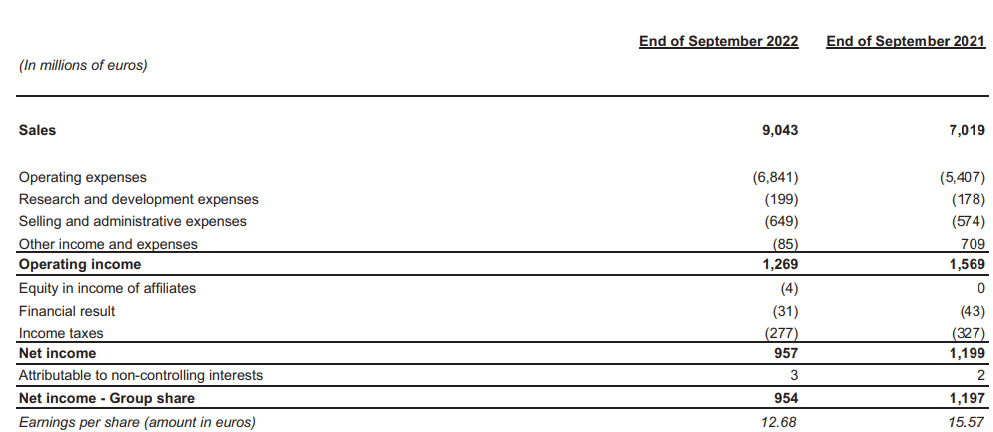

In the first nine months of the year, the company reported a total revenue of just over 9B EUR , resulting in an operating income of 1.27B EUR . That's lower than in the first nine months of 2021, mainly due to the 'other income and expenses' which really boosted the 2021 results.

{kind=link}

The bottom line for 9M 2022 showed a net income attributable to the shareholders of Arkema of 954M EUR, representing an EPS of 12.68 EUR per share.

{kind=link}

I'm mainly interested in a company's free cash flow potential, and Arkema isn't any different as my 2021 article was also zooming in on cash flows.

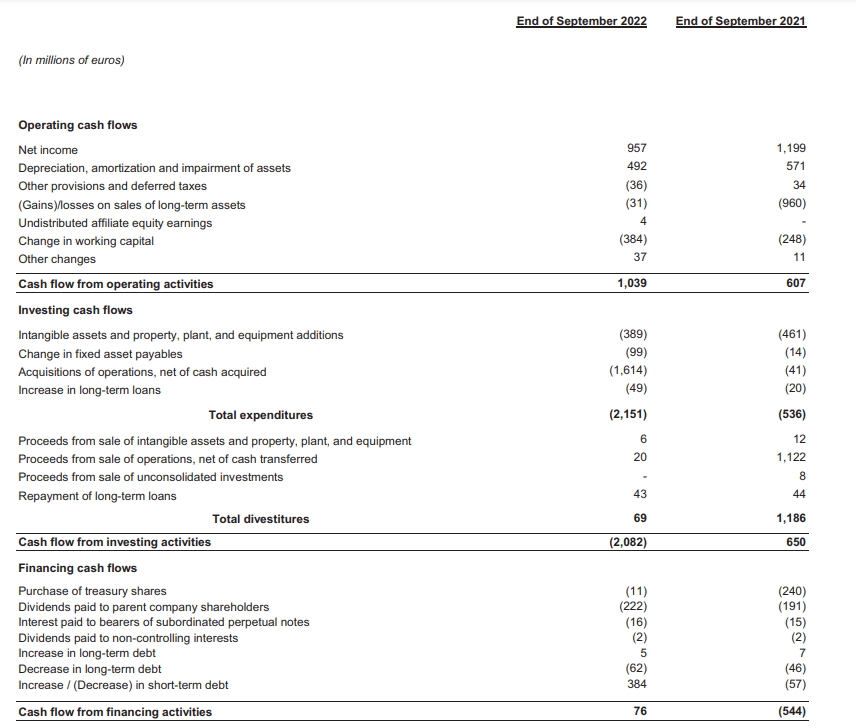

In the first nine months of the year, Arkema reported a total operating cash flow of 1.04B EUR, which included about 384M EUR in working capital investments and excluded the 18M EUR in dividends to non-controlling interests and the payment of interest on the subordinated perpetual debt.

{kind=link}

We see the total capex was 389M EUR, which results in an adjusted free cash flow of 1.02B EUR for a free cash flow result of approximately 13.6 EUR per share.

While Arkema doesn't provide a detailed sustaining capex, we know the company aims to spend 5.5% of its revenue on 'recurring capex'. Despite using 'recurring', this total capex also includes growth, and the company has guided for about 60% of its recurring capex to be spent on sustaining capex. This means that in normalized circumstances, about 3.3% of its revenue is related to sustaining capex. Assuming Arkema will generate 11B EUR in revenue in 2024 (see later), it's probably safe to assume the sustaining capex is approximately 400M EUR per year.

This means the sustaining capex in the first nine months of the year was approximately 300M EUR, resulting in an underlying free cash flow result of 1.1B EUR or almost 15 EUR per share.

It's unlikely 2023 will be as good, but that doesn't make Arkema a bad investment

2022 turned out to be a great year for companies in the chemical sector, but there's little doubt most companies will have to take a step back in 2023. The average analyst consensus calls for an EBITDA of 1.58B EUR in 2023 which would not only be about 25% below the anticipated 2022 result, it would also be almost 10% below the 2021 EBITDA result.

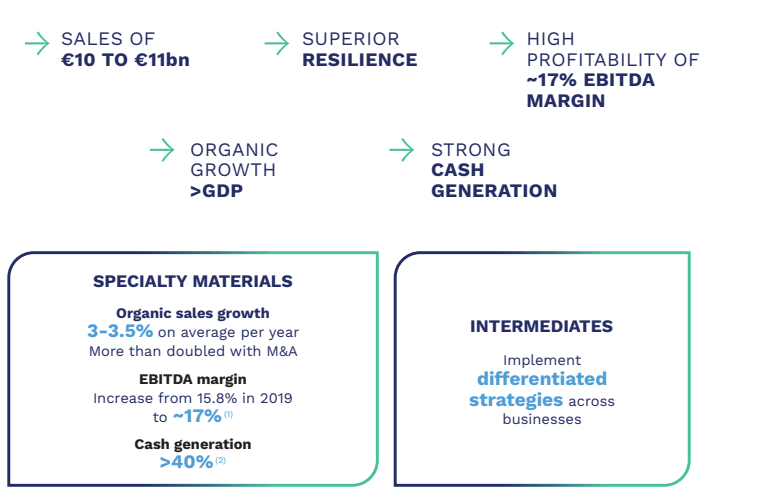

While that may sound disappointing, we should actually look at 2022 as an exceptional year, and Arkema will move back to a 'normalized' performance. The company is sticking with its 2024 guidance to generate 10-11B EUR in revenue and report a 17% EBITDA margin.

{kind=link}

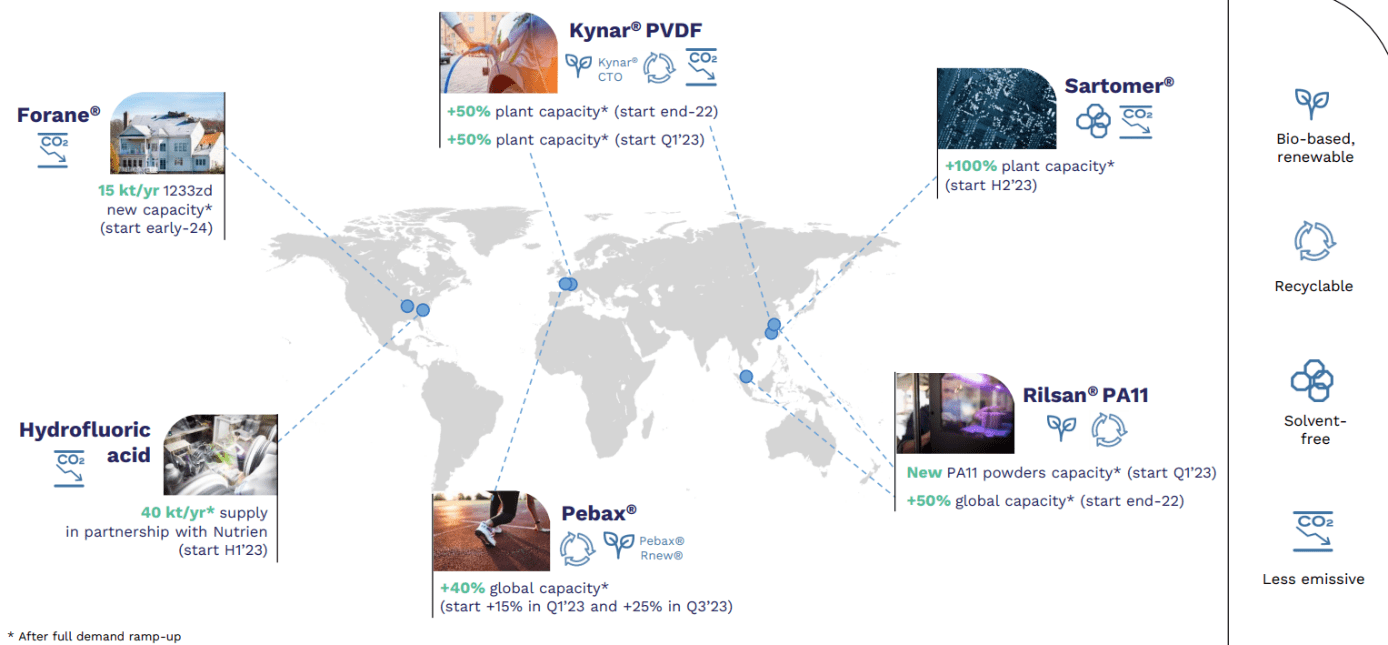

The revenue and EBITDA increase will be fueled by the completion and start-up of the growth projects Arkema has been invested in over the past few years as 2023 will be a pivotal year. Several new plants (or expansion programs) will come online and ramp up during the year, which makes the 2024 targets achievable.

{kind=link}

This allows us to calculate the potential EPS and free cash flow.

Starting with an EBITDA result of 1.75B EUR (just below the midpoint of the EBITDA based on the 10-11B EUR revenue guidance) and knowing the annual depreciation charges will be approximately 675M EUR per year (a small increase from the current 655M EUR per year), the EBITDA will be approximately 1.08B EUR.

The interest expenses should not increase by too much. I will apply a 60M EUR net interest cost (and that's quite generous as Arkema's strong free cash flow result should enable the company to reduce its gross debt), resulting in a 1.02B EUR pre-tax income. Applying an average tax rate of 25% would result in a net income of 765M EUR or just over 10 EUR per share.

We also know the sustaining capex is approximately 3.3% of the revenue. Even when I'm conservative and apply a 4% sustaining capex on the 10.5B EUR revenue, the 420M EUR in annual sustaining capex is substantially lower than the 675M EUR in annualized depreciation expenses.

This means the free cash flow result excluding growth investments will likely be 200-250M EUR per year higher than the net income. This could easily add an additional 3 EUR per share and the annual sustaining free cash flow could easily be 12.5-13 EUR per share. Please note we will likely not see this in the annual results as I expect Arkema to continue to invest in growth (at a moderate pace).

Investment thesis

2022 will be a great year, but the market realizes 2023 clearly won't be a strong and Arkema's share price has lost about 25% since the summer. I think this creates an opportunity for investors with a longer-term investment horizon. The 2024 guidance implies the stock is currently trading at 9 times earnings and at a free cash flow yield of 15% if you would exclude the growth capex.

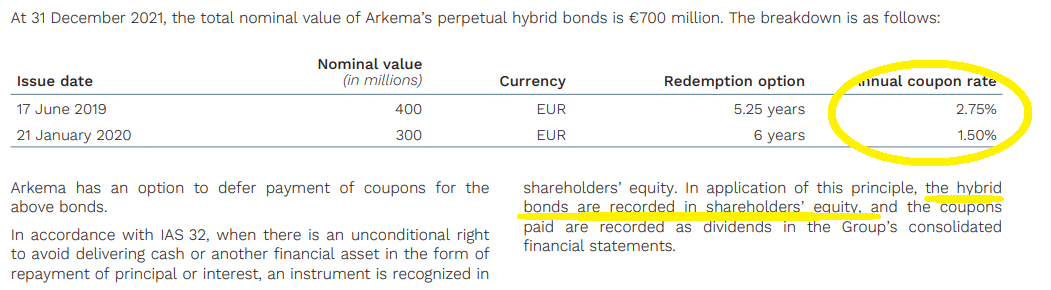

The net debt (excluding the hybrid bonds) is just 1.5B EUR (including the hybrid bonds the net debt exceeds 2B EUR but considering these bonds are costing Arkema just 1.5% and 2.25% which is ultra-cheap capital for equity-like perpetual debt, I don't expect those bonds to be called and they are considered equity). There's no way Arkema will (or should) call these bonds as the cost of capital is just a fraction of the 'normal' cost of capital for equity so I will just use the net financial debt excluding these securities.

{kind=link}

This means the company is currently trading at an EV/EBITDA of approximately 4.5 using the 2024 EBITDA, and if we would assume the net debt to decrease to 500M EUR by the end of 2024, the forward EV/EBITDA is actually just 4.

Applying a P/E of 10 would result in a fair value of 100 EUR. Applying a forward EV/EBITDA of 6 would result in a fair value of 133 EUR per share. Applying a sustaining FCF yield of 7.5% would result in a fair value of 173 EUR per share. The weighted average of these three potential value calculations is 135 EUR per share, and I think that's a realistic near-term (12-18 months) target. The market could be disappointed with the 2023 guidance (although it should be fully prepared) and that could create an opportunity to pick up stock.

I currently have no position in Arkema, but I will likely initiate a position in the next few months in anticipation of the 2024 guidance being met.

For further details see:

Arkema: French Powerhouse Trading At Just 4x The 2024 EBITDA