AANNF - Aroundtown Is Now Too Cheap To Ignore

2023-05-31 06:54:48 ET

Summary

- Aroundtown's Q1 2023 earnings show resilient operating performance despite weak investor sentiment and high debt load.

- The company has improved its liquidity position and reduced leverage through asset disposals and debt repurchases.

- Trading at a depressed valuation, Aroundtown's risk-reward proposition is attractive for long-term investors with limited downside and potential high upside when market conditions improve.

Aroundtown ( OTCPK:AANNF ) is currently trading at a very depressed valuation, making its risk-reward proposition quite interesting for long-term investors.

As I’ve analyzed in previous articles , Aroundtown currently has a depressed valuation due to very weak investor sentiment and a high debt load, but its operating performance has been resilient in recent quarters, and in this article I analyze its Q1 2023 earnings announced 30 May and update its investment case.

Earnings Analysis

Despite a falling share price, Aroundtown’s operating momentum has been resilient in recent quarters, showing that investors may be punishing the company too hard even though its leverage position is higher than compared to some of its peers and its business is skewed to offices and hotels (representing more than 60% of its portfolio), two segments of the real estate sector that are more cyclical, compared to residential properties for instance.

Since my last article on Aroundtown , its share price has declined by some 39%, and its currently trading near all-time lows. Its drop since its peak achieved in 2020 is about 89%, showing that a lot of fundamental issues are already priced-in.

Article performance (Seeking Alpha)

This bad performance is also explained by a rising interest rate environment in Europe, which is negative for property valuations, and also has increased funding costs for real estate companies. Moreover, the credit markets have been shut for these companies, making refinancing of upcoming loans and bond issues more difficult to achieve.

Despite this tough operating backdrop, Aroundtown reported today somewhat positive Q1 2023 earnings , which were mixed compared to expectations (beat on revenues and miss on FFO), but the market reacted positively as shown in the next graph.

Earnings Surprise (Bloomberg)

Its net rental income amounted to €297 million in Q1, a decrease of 4% YoY, due to asset disposals compared to the same quarter of last year, while on a like-for-like basis rental growth was 3.5%. While disposals are negative for its top-line, as I’ve analyzed in previous articles, due to the current challenging market conditions in the real estate market, the company’s strategy has clearly shifted from growth to cash preservation.

This happens because Aroundtown’s balance sheet is not particularly solid, as the company has a high leverage position, and needs to retain cash both for liquidity purposes and to reduce leverage. This profile also explains why the company decided to suspend its annual dividend a few months ago, to save about €250 million of cash outflow.

Indeed, one of Aroundtown’s main weaknesses is its debt position, measured by its loan-to-value (LTV) ratio. While before the current market downturn, investors would treat hybrid bonds as equity, this has changed in recent quarters when call options were skipped by issuers, including Aroundtown, and the market started to treat perpetual notes (also called hybrid debt) as debt. While for some real estate companies this treatment doesn’t affect much the reported and ‘adjusted’ LTV ratios, in Aroundtown’s case the difference is significant.

At the end of last March, its LTV ratio was 40% when accounting only for its senior debt, a ratio that increases to 55% when also including hybrid bonds. This ratio is above the sector’s average and also higher than compared to its closest peers, which usually have LTVs ratios between 40-45%, which is another factor explaining why investor sentiment toward Aroundtown has been weak in recent months.

Leverage (Aroundtown)

To reduce its leverage position, Aroundtown has been a net seller of properties, performing disposals of €460 million during Q1 (booking a profit of about €29 million) and has signed further disposals amounting to some €320 million since the beginning of the year, at values around book value.

While these disposals will reduce its rental income and earnings going forward, it increases the company’s cash position and reduces leverage, which are critical factors to manage in the current challenging market environment.

Its liquidity position improved to €3 billion at the end of March, an increase of €300 million during the quarter, which is positive to reduce the company’s need to raise debt in the capital markets over the next few years. Moreover, Aroundtown has been able to raise some €450 million bank debt (secured) since the beginning of the year, at a reasonable cost of Euribor plus 130 basis points.

This is a much lower funding cost than currently issuing unsecured bonds in the capital markets, explaining why the company also decided to repurchase some outstanding bonds with maturities in the range 2024-26. Aroundtown repurchased about €710 million of bonds at an average discount of 17% to par value, reducing net debt and booking a profit of about €120 million.

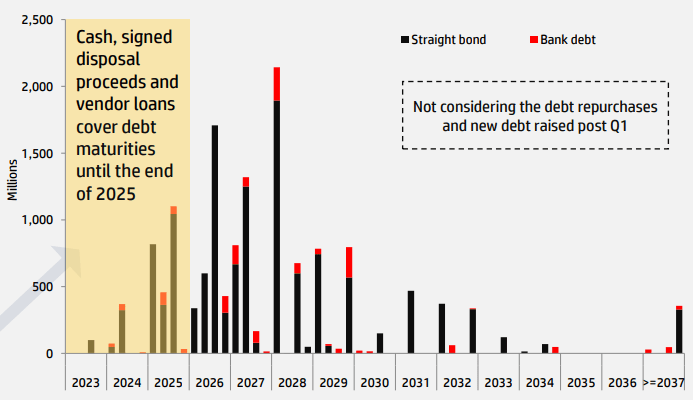

Taking into account all measures performed in recent months, Aroundtown has enough resources to cover its debt maturities until the end of 2025, which seems to be a comfortable position to properly manage the current downturn. Additionally, the vast majority of its properties are unencumbered and Aroundtown has plenty of room to raise mortgage loans if needed, thus the prospects of a liquidity crunch in the short term seem to be rather low.

{kind=link}

Considering its debt repurchases performed post Q1, its signed disposals and vendor loans, the company’s pro-forma LTV ratio drops to 37%. This is a very acceptable level, showing that Aroundtown used too much perpetual notes during the boom years, being the main reason of its current relatively high leverage financial position when considering other metrics, such as the net debt-to-EBITDA at close to 12x.

Debt ratios (Aroundtown)

Regarding its operating performance, its property portfolio was valued at €27.8 billion at the end of March, a stable value compared to the end of 2022, and its vacancy rate was 7.7% (vs. 7.6% in 2022). Its total revenue in Q1 was €402 million (+2.3% YoY), while a loss of €130 million in property revaluations and capital gains led to an operating profit of €86 million in the quarter (-72% YoY). On the other hand, its FFO was €84.6 million representing a decline of only 4.5% YoY.

By segment, the office and residential segments continue to report some positive rental growth, due in part by inflation indexation, while the hotels segment continues to be a laggard even though the collection rate is expected to improve this year and fully recover next year, compared to levels achieved before the pandemic.

Going forward, Aroundtown reaffirmed its previous FFO range of €300-330 million for the full year, compared to €363 million achieved in 2022, a drop that is justified by higher financing costs and the negative effect of disposals.

Conclusion

Aroundtown has reported another decent financial performance taking into account the current downturn in the European real estate market, showing that its business has good fundamentals. The company has improved its liquidity position and I don’t see any potential liquidity issues in the next couple of years, which is supportive of its investment case.

Due to a weak share price, Aroundtown is currently trading at a very depressed valuation of 0.10x net asset value, which seems to be too harsh and already reflects much of the company’s woes. Therefore, I see Aroundtown’s current investment proposition quite interesting, as the potential downside seems limited at current prices, while the upside potential can be quite high when market conditions improve, considering that historically Aroundtown traded at about 0.6x net asset value over the past five years.

For further details see:

Aroundtown Is Now Too Cheap To Ignore