AHKSF - Asahi Kasei: Not A Bad Proposition

2023-08-03 09:14:44 ET

Summary

- Asahi Kasei in typical Japanese-stock fashion does several totally unrelated things, but has some good positioning in each segment.

- In materials there is an emerging exposure to renewables. In homes, there are more vigorous overseas markets. In medical to new in-licensed meds and acute care equipment there is resilience.

- Results are affected by commodity fluctuations, the end of the pandemic and some less resilient segments, but the outlook isn't bad longer-term.

- At 13x PE, it's actually a pretty interesting proposition.

Asahi Kasei Corporation ( OTCPK:AHKSY ) is a company we haven't looked at in some years. While some things are the same, the quality of the disclosure has markedly improved and the story has changed to focus more on emerging and more secular trends. They make order-built homes and do building in foreign markets, a segment that hasn't changed much. They have a chemicals and materials segment which is quite commodified but has some more specialty exposures in renewable energy, car interiors and textiles. Then there's the life science division, which used to be a pretty dull pharma business and then some well-placed acute care products used in the pandemic like ventilators. Now that business is becoming more interesting as they invest for growth and innovation. While Asahi Kasei earnings quality suffers due to commodified exposures and volatility, the increment looks good for the business, and actually seems compelling considering secular trends and rebounds incoming at a forward 13x PE multiple for FY 2023.

Q1 Breakdown

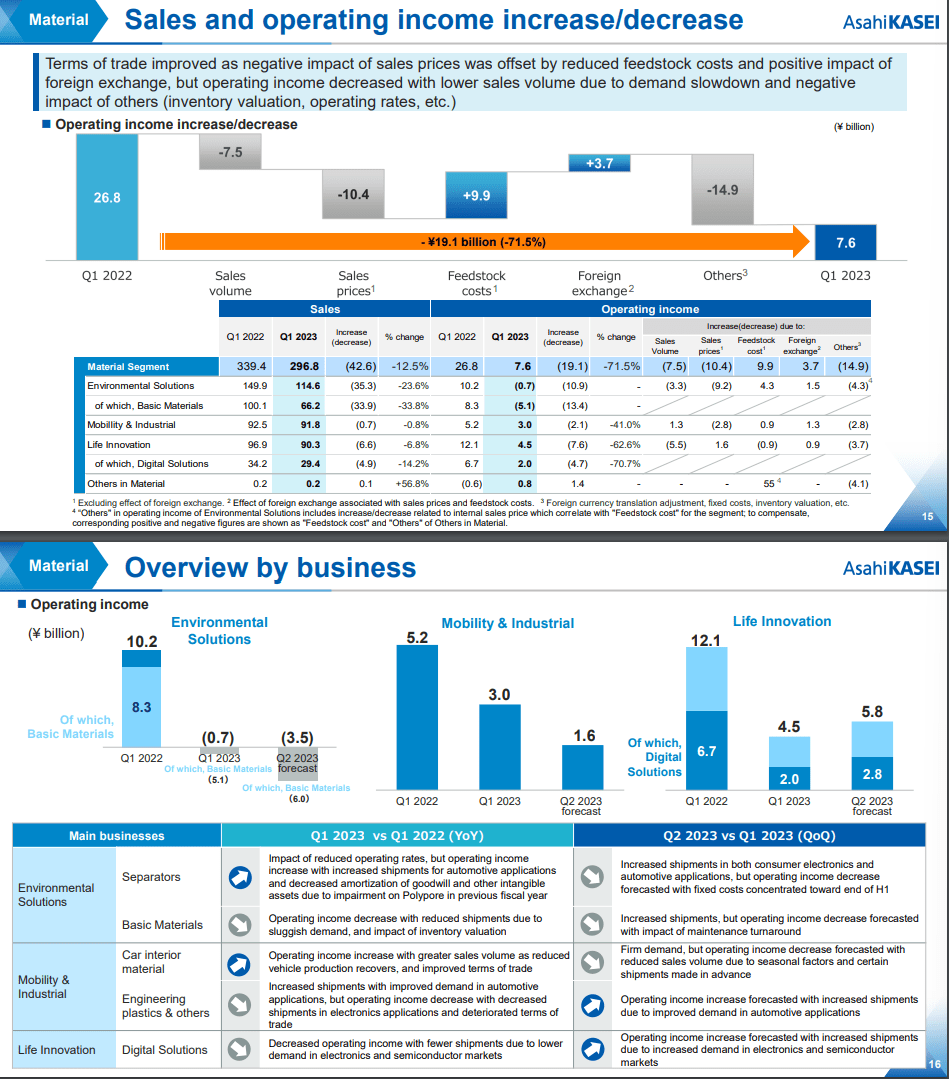

The materials business got stomped by commodity volatility and economic uncertainty that affected their commodified exposures. In particular, Asahi Kasei is exposed to markets like automotive and electronics which were the first to appear weak in the global rate hiking regime being carried out.

Automotive was actually less affected by rate hiking, but continued to be affected by overhang from slow supply of vehicles that has persisted since the semiconductor shortage in FY 2022 . In Q1 automotive is a positive increment in the chemical end markets while electronics is not. Lost volumes in electronics hurt the mobility and industrial segment as industrial scale was lost. Asahi Kasei does chemicals for producing car interiors and other parts, so these exposures to mobility have done well. Environmental solutions contains basic materials which was hit by some inventory revaluation effects and weak margins on commodified chemical products that are more sensitive to economic change - there was deflation here as with the rest of commodity markets. Some of these products are exposed longer-term to hydrogen economy and other decarbonization technologies, but their dynamics are still dictated by commodity forces in general industry. But this segment is also exposed to separators used in battery technology, and automotive and EV pickup actually helped this business despite pressure from a weak Chinese economy, which does account for 10% of the company's overall sales. The profit here is growing nicely. The major delta in life and innovation was in the digital solutions business, which is affected by the situation in semiconductor markets which has been slow and caused scale to be lost, but also other exposures for clothes and textiles saw pressure as margins remain somewhat compressed.

{kind=link}

Overall, pressure in terms of sales volume but also greater caution in broader industry had almost equal and large effects on overall operating profit. The materials segment is altogether pretty commodified and the effects of deflation on commodity and commodity level products was felt as the global economy slows down.

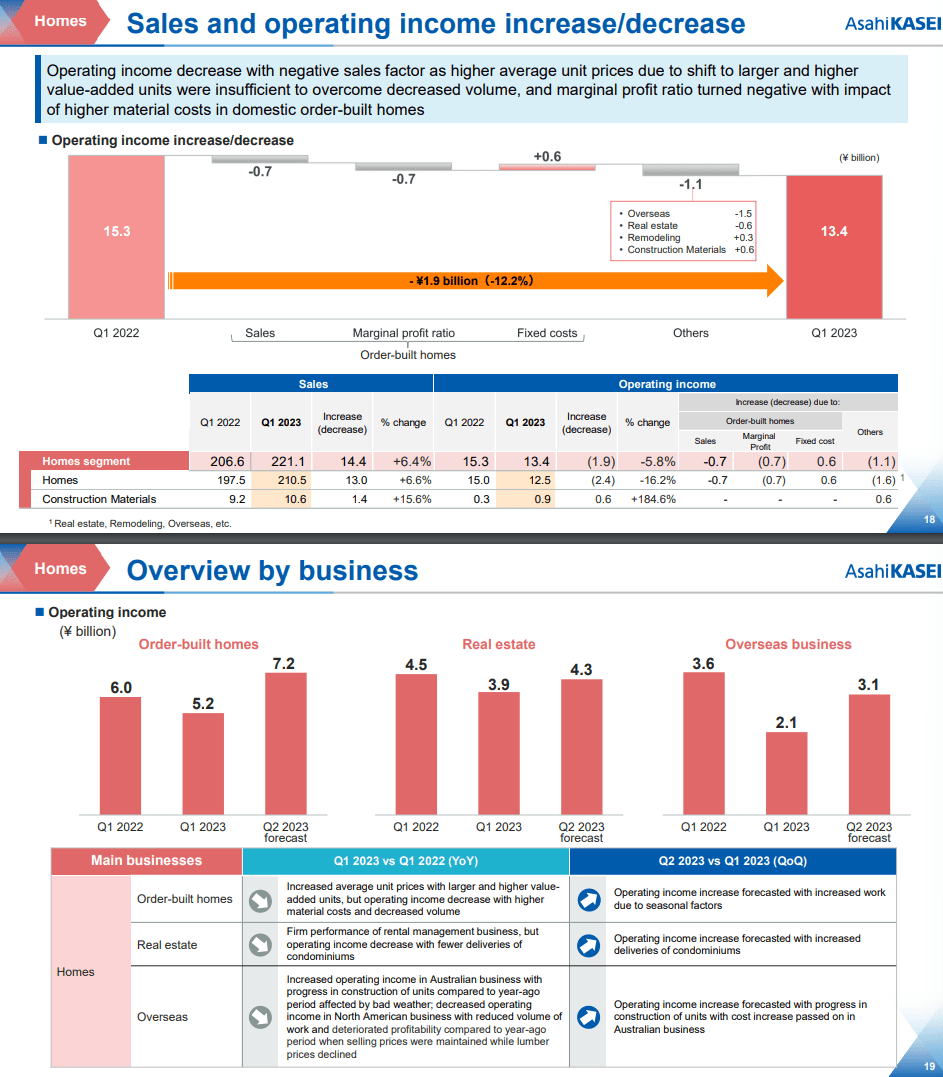

The homes segment suffers from belligerent inflation in materials, which is consistent with reporting we've seen from other companies, but primarily those in Japan due to imported inflation from the weak Yen. Orders have been falling for order built homes, and while there have been positive mix effects, weakness is showing in their order built exposure in Japan due to material inflation. Their real estate management business is solid and mostly unremarkable, but the overseas business is suffering since part of their market is in Australia, which has an elevated real estate market and has been sensitive to the rate hiking regime. While the overseas expansion is a welcome evolution, besides North America, they are exposed to markets feeling the pain of higher rates. Comps were also quite weak due to weather effects early in the prior year.

{kind=link}

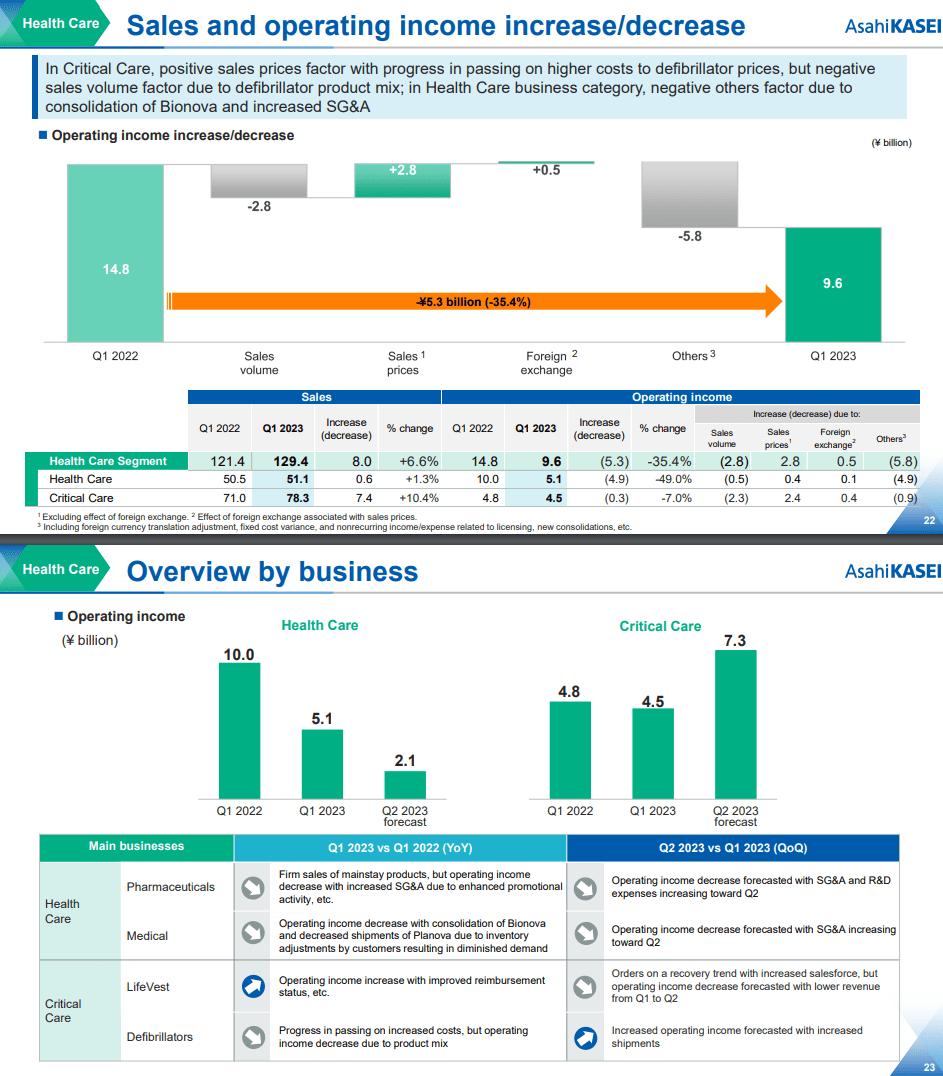

The health care segment is undergoing quite a lot of change. Critical care has mostly digested the impact of the end of the pandemic on results, and products that weren't directly exposed are being marketed and sold well by the company. Defibrillators are still under inflation pressure and are undergoing pricing action. In the coming quarter more pricing action is expected, and more solid performance all around is expected to contribute positively. The healthcare exposures have undergone major change as R&D and promotional expenses have gone up due to some recent new in-licensing and greater levels of activity in this segment as the company looks to make it a more relevant contributor. They want to become a more relevant specialty pharma player, also through their US subsidiary Veloxis. Profits will be depressed for a while from this segment as Asahi Kasei tries to create a more innovative pharma business, but sales are growing as their healthcare platform scales.

{kind=link}

Bottom Line

The main issue for Asahi Kasei's earnings is the basic materials segment, overshadowing some positive exposure to renewables, and generally good exposure to an automotive recovery. The semiconductor and electronics slowdown is hitting them quite hard for now in chemicals too, but it's quite natural to have a glut after a shortage. Homes is suffering in Australian markets mostly, with domestic Hebel deliveries expected to be pretty good despite slowdown in domestic ordering. They are good at the moment too as revenues are rising YoY, there's just margin compression going on. Healthcare is under pressure but the pressure is discretionary on earnings. Revenues are growing in healthcare.

The longer-term growth expectations are pretty good for the business in terms of profits. We like what we're seeing, and since March 2023 the forecasts have pegged forward PEs at 13x despite the growth investment going on and some temporary headwinds like inflation issues in homes. With a growing pharma platform, resilience in medical equipment and homes, as well as a growing renewable and battery exposure in environmental solutions, the picture can be expected to improve for Asahi Kasei. But it's still relatively early to call since short-term economic headwinds are still quite meaningful. A watchlist pick.

For further details see:

Asahi Kasei: Not A Bad Proposition