SHLRF - Ascending The Market With Otis: Financial Strengths Market Trends And Long-Term Outlook

2023-12-05 05:01:55 ET

Summary

- Otis showcases resilience in its service-centric model, navigating challenges in elevator industry markets.

- Financially stable Q3 results reveal steady growth in sales, increased service orders, and strategic dividend policies.

- In this article, we go over the latest financials while addressing critical issues such as China and Otis' negative equity.

Introduction

Otis ( OTIS ) has caught my attention since Terry Smith started buying it , after having ditched its Finnish competitor KONE ( KNYJF ). Elevator and escalator manufacturers belong to an incredibly interesting niche within the industrials sector and the industrial machinery industry. In fact, this is a very consolidated market, with a few main players: Otis being the largest, followed by Kone, the Swiss Schindler ( SHLAF ) and the German thyssenkrupp ( TYEKF ).

These companies all have resilient business model amidst industry cyclicality. In fact, not only do they install new equipment, but a large part of their revenue comes from service. In particular, these companies have maintenance contracts and modernization services. Otis, for example, generates around 57% of sales from services, which contribute by 83% to the overall operating profits. In other words, these companies sell their equipment almost at cost, knowing that throughout their lifecycle they will generate a high-margin recurring revenue. So, what becomes key for success is customer retention and, if possible, customer conversions. What made me choose Otis over Kone and its other peers is its lower exposure to China, where currently the housing market is going through any turmoil, with an impact on elevator and escalator sales as well.

Recently, Otis has started to feel the impact of high interest rates, with slowing new equipment orders. On the other side, it has proven resilient because this was counteracted by a consistent surge in modernization orders. Once I shared my last analysis back in the summer, I had a buy rating with a fair value estimated to be around $90 per share. That is when I bought my first small position. In October, as the stock was dipping, I actually took advantage of that weakness and bought more shares around $75.

My confidence lies in Otis's resilience, driven by its service-centric business model and steady financial performance, positioning it as a relatively safer investment within the manufacturing sector.

It is now time to see how the company performed in Q3 and how it is positioning itself for 2024.

An overlook on its markets

During the Morgan Stanley 11th Annual Laguna Conference , Judy Marks, Otis CEO, gave a nice overview on the company's business worldwide. She was clear about the strongest market the company has today:

As we look around the world and the market today, our strongest market is actually Asia Pacific. We're seeing really strong growth in new equipment there, double-digit in India, but really kind of mid-single digit the rest of Asia Pacific, which includes the mature Asia, Japan, Korea, Australia as well as the emerging Asia in Southeast Asia. And as I said, India is just really growing nicely at double-digit in terms of the market segment and units.

We should spot right away how China wasn't mentioned, since it is a market on its own, on which we will spend a few important words in a moment.

Europe, on the other hand, is seeing a high-single digits decrease this year. But the picture is mixed. Southern Europe (Spain and Italy) are performing really well, while Germany, France and the UK aren't.

China

Miss Marks, in the same conference, was asked several questions about China. After all, it is the largest market for elevators and Otis has been lagging behind its peers. However, the outlook doesn't look that bright. In fact, Otis CEO explained how this year the market will be down 10%. On the other hand, since its spin-off, Otis has increased by 75% its service portfolio to 350,000 units before a million installed base. Of those 8 million units, 75% are still serviced by independent providers. This means Otis only has 4% market share and it still has room to grow. In fact, in terms of service revenue, Otis has grown revenues at double-digits for two years in a row. How does Otis plan on acquiring more and more service contracts? By creating an ecosystem - Otis ONE - which can't be easily serviced by external providers.

Moreover, in China, Otis' conversion rate is the lowest anywhere in the world. After the spin-off it was about 40%. At the end of 2022 it was up to 48% and Otis has set its target to be about 60% in the medium-term.

Though the residential housing market has been severely hit in China, spending in infrastructure has increased, making Otis state there currently are larger bids making infrastructure a strong segment for elevators and escalators.

Overall, the outlook on China keeps on being rather gloomy in terms of new equipment sales, but the fact Otis can grow substantially in service still leaves room to forecast both top-line and bottom-line growth in that market.

Modernization

A part of service which sometimes is overlooked is modernization. Currently, there Otis has around 20 million units in the world. According to what Judy Marks said during the Laguna Conference, around 7 million are over 20 years old. This means they are eligible for modernization. China is part of this too because it saw a big surge between 2005 and 2015. This means that in the next few years we will see the need to start modernizing the elevators and escalators installed at the beginning of that strong cycle.

Modernization is not as high-margin as maintenance. However, it plays a key role in customer retention. As Miss Marks explained: "our conversion rates after a modernization are in the high 90% everywhere in the world".

Coupled with this strategy, Otis has another one: acquiring every year small independent service providers, spending around $50-$70 million a year on this. In this way, Otis acquires customers and their need for services, while up-skilling these providers so that they can maintain and service correctly Otis equipment withing the Otis ecosystem.

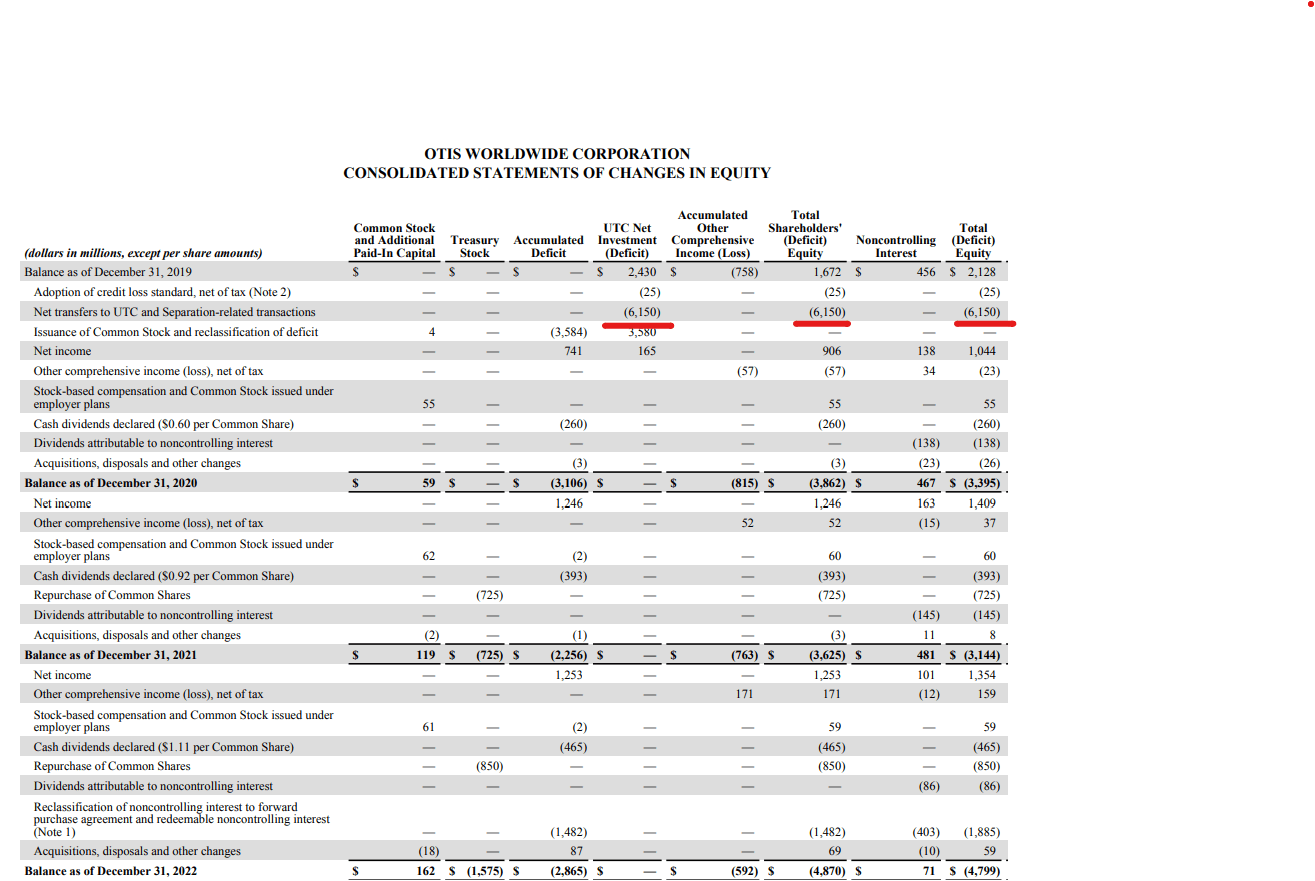

The issue of negative equity

In my past article, some readers asked me about an issue. Otis financials look fine, but if we look at Otis' balance sheet we find an issue with total common equity being negative by around $4.8 billion. Now, come countries would not allow this per their accounting rules. However, as far as I understand what lead to this negative number, I think the issue is not that big.

By reading the last annual reports, in particular the 2020 Annual Report and the 2022 Annual Report we find Otis explaining why it is recording in its balance sheet negative retained earnings (accumulated deficit) of about $2.2 billion:

As a result of the Tender Offer approval, the issued and outstanding shares of Zardoya Otis owned by Euro Syns, S.A. ("Euro Syns") were reclassified to current liabilities as Forward purchase agreement, and the remaining shares not owned by the Company were deemed redeemable at the option of the other shareholders and were reclassified from Noncontrolling interest to Redeemable noncontrolling interest on our Consolidated Financial Statements. The difference between the historical noncontrolling interest carrying value in the balance sheet and the fair value of the Tender Offer was recorded to Accumulated deficit.

But, more importantly, a big chunk of Otis negative equity comes from a big dividend paid by Otis to its parent company UTC. Even in the last annual report linked above, we can find on the consolidated statements of changes in equity due to net transfers to UTC related to the separation of $6.3 billion during 2020. These were primarily funded by the net proceeds from issuance of long-term debt of $6.3 billion during 2020. In red, I highlighted how the UTC related deficit leads to total shareholders' deficit.

{kind=link}

In other words, UTC took advantage of the spin-off to receive a hefty dividend, leaving Otis with the task of retaining a part of its yearly earnings. Therefore, the negative equity Otis has is the result of payments of large dividends as a consequence of a decision made by the parent company about distributions from the affiliate.

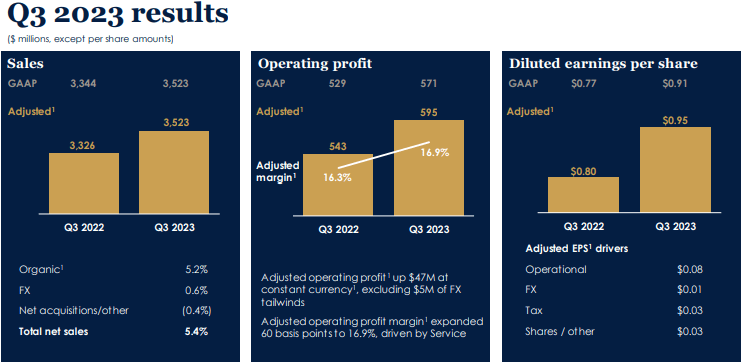

Financial highlights

Now, let's look at Otis' Q3 financial highlights Otis reported:

{kind=link}

- Net sales went up 5.4% and organic sales up 5.2%. Service net sales were up 10.1% with organic sales up 8.4%;

- Maintenance portfolio units increased 4.2%

- GAAP EPS up 18.2% and adjusted EPS up 18.8%

- Service GAAP operating profit margin expansion of 80 basis points and adjusted Service operating profit margin expansion of 90 basis points

- New Equipment orders down 10%;

- backlog up 3%, up 2% at constant currency

- Modernization orders up 13%, backlog up 17%

- GAAP cash flow from operations of $306 million; free cash flow of $272 million

- Updated full-year outlook with organic sales up ~5.5%, adjusted EPS of ~$3.52 and free cash flow of ~$1.5 billion

Overall, these results show a healthy company. In particular, it is clear how Otis is resilient during economic weakness and can navigate through turmoiled waters. In fact, while global new equipment bookings were down 10% YoY, in service, the company expects to grow its installed base by 5%. As was explained during the earnings call : "This will put the global service installed base somewhere between 21 million units to 22 million units by year end of which we currently maintain approximately 2.2 million and expect to end the year around 2.3 million units in our maintenance portfolio".

Further resilience can be seen by looking at the backlog and at the orders the company reported, which are visualized below.

Otis Q3 Results Presentation

As said above, modernization shows its strength and there are reasons to believe we will see strong tailwinds for this business segment over the next few years.

What matters a lot is that Otis' higher margins segments, those generating and printing cash, are growing. Since these streams of revenue are highly predictable, Otis can afford to be rather generous with its shareholders. Since going public, the company has already increased by 70% its dividends, keeping its payout ratio around 40%. A buyback program has been initiated, with the target of returning $800 million to the shareholders.

The company also said it doesn't feel it needs to pay-down debt anymore, considering its balance sheet healthy, with a net debt of $6 billion and an EBITDA of $2.4 billion Otis has a ND/EBITDA ratio at 2.5x which is fine for a business whose operations are rather predictable and stable.

Conclusion

Since my last article, Otis's stock price is flat. Considering its recent results confirm the resilience of this business, I still see the company fairly priced at $90. This means it can be bought at current levels, though perhaps with caution, in order to take advantage of further drops into the $70s as we saw happening a few months ago. So far, Otis has proven a stock with very little paper-hand investors. It trades at a premium compared to the market because of its predictability. This is why a 25 PE, though to many may seem expensive, prices correctly a business to hold for many years to come. Yet, investors should also use prudence and step into this holding a little bit at a time, dollar cost averaging in, while reinvesting the dividends received.

For further details see:

Ascending The Market With Otis: Financial Strengths, Market Trends, And Long-Term Outlook