WLK - Ascent Industries: Impressive Early Innings Turnaround

Summary

- Ascent Industries, formerly Synalloy Corporation, is an under the radar Small-Cap industrial in the midst of a major turnaround.

- ACNT has two different business lines. First being a metal tubular business, think infrastructure piping and stainless steel piping, and secondly specialty chemical, think outsourced chemical manufacturing for blue chips.

- The company had been poorly run for years leading to below peer margins, inconsistent growth, low on-time delivery metrics, and unsafe working environments.

- Following a proxy fight in the summer of 2020, new management was brought in to turn the ship. An impressive turnaround has since unfolded led by new executive chair of the board Ben Rosenzweig and new CEO Chris Hutter.

- ACNT is in a very interesting spot as new management has proven their execution ability, but a 3Q hiccup in the metals business has sent the stock down. We believe this opens a great buying opportunity.

Introduction

Ascent Industries ( ACNT ) is an industrial manufacturing company that has undergone an extensive and complete rebuild. This change was initiated when the largest shareholder , the hedge fund Privet Funds, won control of the board via a proxy fight in the summer of 2020. Since then, ACNT has undergone a vast array of significant changes that we will both lay out and reason why we believe those changes implemented now make ACNT a compelling investment case.

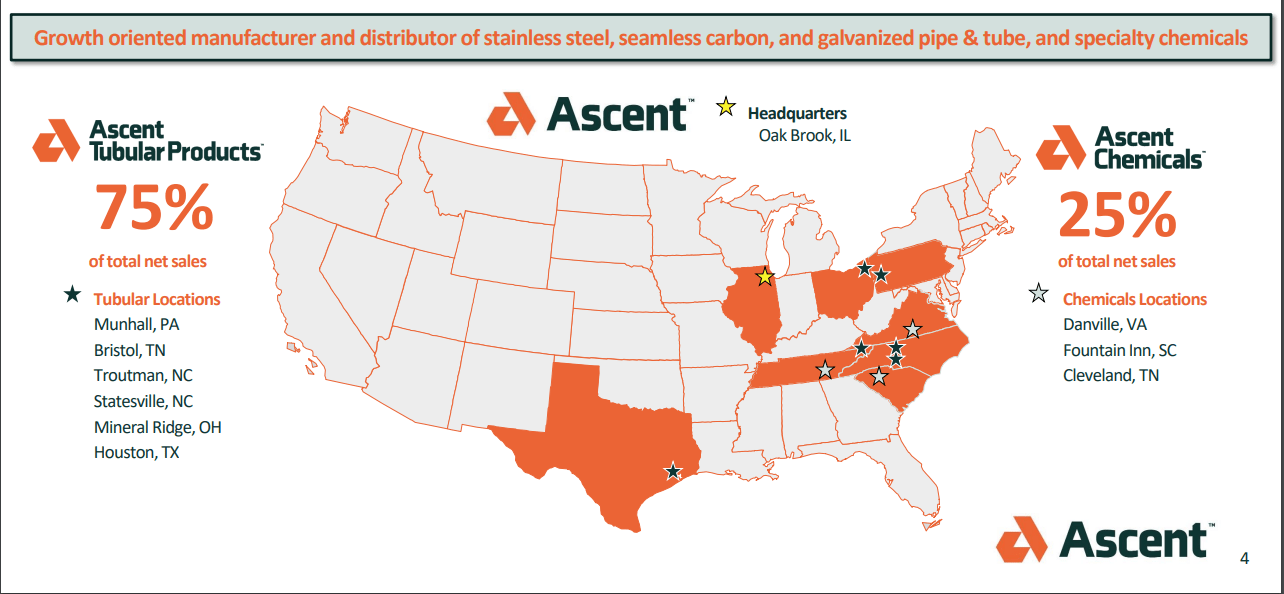

ACNT has two distinctive business lines, Ascent Tubular and Ascent Chemical. The company was founded in 1967 under the previous name Synalloy Corporation and previously traded under the ticker SYNL. The rebrand of the Synalloy to Ascent came this past August after the changes implemented by new management made the company of the past barely recognizable. Therefore, a complete rebrand felt in-line with the other initiatives. The company is headquartered in Oak Brook, IL and has 6 locations for the tubular business and 3 for the chemical business with over 750 employees.

{kind=link}

ACNT Footprint Snapshot (ACNT Investor Slides)

We believe that the transformation ACNT has undergone over the past two years has fundamentally changed the future business prospects for the better. We see above peer top-line growth, market share gains, accretive and synergistic M&A opportunities, and strong margin expansion all in the coming years. A messy 3Q report has opened, in our eyes, the best entry-opportunity into ACNT since the execution of new management has been validated. For all these reasons, we believe the small and under the radar ACNT merits the attention of investors.

Thesis

Overview

Our thesis on ACNT can be bucketed into three core concepts:

- New management

- Inflecting financials with strong margin expansion

- Continued M&A opportunities in specialty chemicals

While these buckets are broad, this is because there are many factors within each that we will weave into our overall thesis. We also want to highlight that the, in our eyes, depressed valuation plays into our thesis, but we will speak to the valuation in its own section.

Management Change

The set-up

The entire story of ACNT starts with new management stepping into the picture in 2020. This change of management was spurred by the largest shareholder of ACNT, the hedge fund Privet Funds, launching a proxy contest for multiple board seats. Privet argued that years of mismanagement had led to both significant operational deficiencies and poor shareholder returns. ACNT's old management vehemently fought against this change, putting out several releases over that timeframe claiming Privet was acting irrationally and was not equipped to successfully run the business. Ultimately, Privet won the proxy battle in June 2020 gaining three board seats and effectively gaining control of ACNT.

Of those three new members, two have been the primary drivers for change at ACNT, Ben Rosenzweig and Chris Hutter . The first major change implemented after gaining control of ACNT was replacing the past CEO with Mr. Hutter in the fall of 2020. Before diving further into the change, below we profile the professional histories of Mr. Rosenzweig and Mr. Hutter.

Ben Rosenzweig - Serves as Executive Chairman of the board for ACNT. Along with his duties for ACNT he is a partner at ACNT's largest shareholder Privet Fund. He joined Privet in 2008 after working as an investment banker at Alvarez and Marsal. Mr. Rosenzweig has extensive experience as a board member, currently on four and previously on another three. We point out that of the seven total boards positions Mr. Rosenzweig has served on, five have seen positive stock appreciation. Mr. Rosenzweig graduated magna cum laude with degrees in Finance and Economics from Emory University.

Chris Hutter - Serves as a board member and as the president and CEO of ACNT. Previous to joining ACNT, Mr. Hutter cofounded UPG Enterprises which is a privately held diversified industrial company focusing on steel fabrication. Mr. Hutter grew UPG to over $1.6B in sales with 3,000 employees across 9 manufacturing sites. Key to note, for a later thesis point, during his time UPG successfully executed over a dozen acquisitions of smaller steel fabrication companies. Mr. Hutter graduated from University of Illinois Urbana-Champaign with a Finance degree and gained an MBA in Finance from Lewis University.

2021 - Setting the foundation

The company that Mr. Hutter took over was plagued by inefficiencies, disorganization, late deliveries, disjointed business lines, unsafe working environments, and bloated costs to name a few of the inherited problems. Faced with wide-spanning problems, Mr. Hutter initially focused on the low hanging fruit and laying a foundation for an aligned organization functioning as a unified team. Just one example of the low hanging fruit was the decision to terminate the private jet previous management acquired. As for creating an aligned organization, Mr. Hutter visited all of ACNT's facilities speaking with employees to truly gain a fundamental understanding of what needed to change to create a unified company. Mr. Hutter also made it clear that the plan was not to cost-cut to prosperity but rather rebuild, retool, and realign a company that had lost any sense of direction.

These initial measures were immediately reflected in 1Q 2021 which was ACNT's first GAAP profitable quarter since 4Q 2018. What made this profitable quarter even more impressive was that it came even though sales were slightly down on a Y/y basis. We believe that this quarter was the first instance, on their first opportunity, of new management proving their ability to execute margin expansion goals. During the 1Q earnings call Mr. Hutter continued to emphasize that there were still amble opportunities to drive further efficiencies in the business. The focus on incentivizing employees properly and bringing in the right people also remained a top priority. This focus on people was highlighted by the hiring of a new head of the Ascent Tubular, Tim Lynch, who brought in over 20 years' experience from large-cap steel companies. Another key point called out during the 1Q report was that the Safe Drinking Water Act would be a significant tailwind for Ascent Chemical.

The execution of the turnaround plans continued into 2Q and through 3Q financial metrics across the board continued to improve drastically. This was accompanied with robust revenue growth as well. These were then the second and third quarter in a row of proven execution by new management. The changes that Mr. Hutter had implemented had begun to take shape. Some of the standout operational improvements through these quarters were:

- On time deliveries through the first three quarters of 2021 improving by 184%.

- Refining the supply chain process within the tubular business in order to lower the number of SKUs on hand, leading to a significant reduction in inventory days

- Implementation of a safety summit to increase worker safety and employee retention

- Addition of new CFO, Aaron Tam whose expertise is in establishing culture of metrics based analysis, cash conversion, margin enhancement processes

- Shifting the tubular business from a stocking distributer to a producer of made-to-order products

However, most notably during 3Q ACNT acquired the specialty chemical manufacture DanChem . ACNT purchase DC for $32.95M. At the time of the acquisition, DC was projected to see $30M in revenues at an 18% EBITDA margin for 2021. This than implies ACNT paid a ~6x EBITDA multiple for DC. ACNT financed this purchase through its existing credit facility. This acquisition significantly expanded the capabilities of ACNT specialty chemical unit in all capacities. For example, DC has the largest fleet of horizontal reactors in the contract specialty chemical manufacturing industry. Horizontal reactors are used for various products such as petrochemicals, pharmaceuticals, food and beverage, and plastics. The acquisition of DC also led to the hiring of a head for Ascent Chemicals, John Zuppo, who was previously the CEO of DC. The acquisition of DC was expected to accelerate product development, provide entrance into new end markets, expand the production capabilities, and deepen current customers relationships with cross selling opportunities. Also key to note, Mr. Zuppo sits on the board of governors for SOCMA . We believe this gives Ascent Chemicals two major edges. First Mr. Zuppo's role with SOCMA (Society of Chemical Manufacturers and Affiliates) gives Ascent Chemicals essentially a major stamp of approval having the head sit on the major trade organization. Secondly, it gives Mr. Zuppo access to inbound sales opportunities from companies who reach out to SOCMA in search of a partner to producer chemicals for them.

The theme of operational improvements continued through 4Q with another major improvement in the financials. While the numbers were eye-popping, management did iterate that the incredible financial metrics in 2021 were influenced by one of the strongest pricing environments ever. Mr. Rosenzweig explicitly stated this on the 4Q call...

We're keenly aware that we operate in a very dynamic market environment from where we sit today we expect pricing to begin normalizing sometime in the second quarter. As a result, continuing to proactively ensure we can earn competitive margins and any pricing environment remains one of our top priorities this year (2022).

Even with the incredible pricing environment taken into account, the financial results for the first full year under new management clearly exemplified their ability to execute on their goals. Below we summarized some of the several key financial improvements.

| Metric |

| 2019 |

| 2020 |

| 2021 |

| Y/y Improvement |

| 2021 vs 2019 |

| Revenue |

| $305.20 |

| $256.00 |

| $334.70 |

| 31% |

| 10% |

| Gross Profit |

| $30.80 |

| $22.70 |

| $60.80 |

| 168% |

| 97% |

| Gross Margins |

| 10% |

| 9% |

| 18% |

| 900 bps |

| 800 bps |

| Net Income |

| $3.00 |

| $27.30 |

| $20.20 |

| 4,750 bps |

| 2,320 bps |

| EBITDA |

| $9.20 |

| $4.50 |

| $41.00 |

| 811% |

| 346% |

In 2021, Mr. Hutter, Mr. Rosenzweig, and team proved their ability to implement successful change at ACNT. While they did benefit from an incredibly robust demand environment, the mere fact they were able to capitalize on it also speaks to their execution abilities. During this process, ACNT gained the operational foundation for a multi-year turnaround by cutting bloated costs, bringing in more experienced management, and building an overall cohesive company that was all working toward the same goal. We view 2021 as an excellent first step in the turnaround story of ACNT and the results of it gave us the utmost confidence in management in continuing to execute their plans for improvements.

2022 - Continued execution but not without hiccups

While the focuses in 2021 were centered around capitalizing on the robust demand environment, aligning the organization, and improving on time deliveries, 2022 has been focused around identifying low margin revenue to eliminate, cutting unnecessary costs, and implementing successful business strategies. The momentum ACNT exhibited in their business has continued into 2022 but the momentum in the stock has fallen.

Progress is never a linear journey and we note that management has echoed this same thought during their conference calls. Most notably on the 4Q 21' call with Mr. Rosenzweig stating...

What I will say is that we don’t anticipate our growth this year being as linear as it has been over the past several quarters. We remain committed to executing on our strategy, excelling in the areas that we can control and trying to build value brick-by-brick.

Through the first half of 2022 ACNT's financials continued to benefit from the same robust demand environment that it saw in 2021. With revenues, EPS, EBITDA all up on a y/y through the first half of 2022 by 52%, 380%, and 200% respectively.

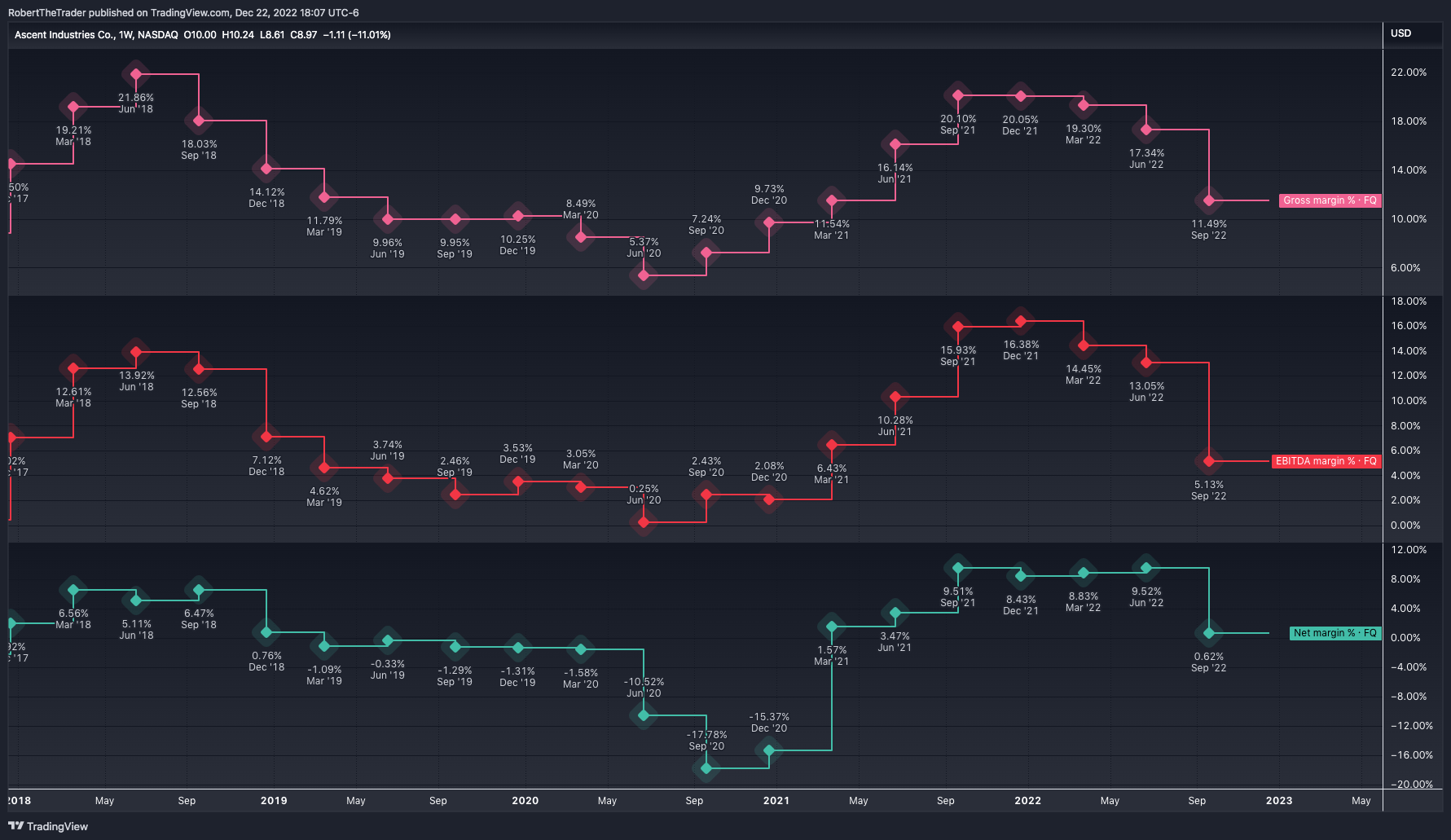

However, the robust demand environment began to cool during 3Q. Additionally during 3Q, ACNT built up certain high cost tubular products for one certain long-time customer, which ACNT has not disclosed who specifically the customer was. This however proved to be a misstep, as the company's CEO passed away and the new CEO decided to move into a different direction. This left ACNT with a large sum of high-cost inventory left unsold negatively impacting margins. Important to note however, no one single customer accounts for more than 10% of revenues of any ACNT’s business segments. The strong US dollar also hurt ACNT most specifically in its small diameter tubular business. This is because that market saw a major influx from international suppliers taking advantage of the strong USD. These headwinds also were combined with increased expenses by ACNT towards growth and improvement initiatives for the business which further negatively affected ACNT's margins. What resulted from these was a serious deterioration in the margins that investors had come to expect from ACNT under the new management.

{kind=link}

ACNT Quarterly Margins (TradingView)

On a q/q basis gross, EBITDA, and net margins fell 585, 792, and 890 basis points respectively. This erosion of margins is what we believe has been the major driver of the stocks ~40% fall since reporting 3Q earnings. What also has likely put downside pressure on the stock is that management called out that the margin issues would bleed into 4Q results as well. While there is no doubt the 3Q report was ugly, it has not shaken our confidence in management's ability to execute their long-term turn around plans. This is because this management's first misstep in the 7 quarters since taking control. While 7/7 is the hope, 6/7 is still excellent.

During our conversations with management since the 3Q report, we gained the feeling that they have a firm understanding of what went wrong and how to fix it. While we also walked away with the feeling that likely 1Q of 2023 will also be a messy quarter. This is because, in alignment with their goals of eliminating low margin revenue, there are a few low-margin revenue contracts that are set to expire at the end of 2022 where management thinks those customers will likely not renew at the new prices.

With all this in mind, we believe the fall in ACNT preceding the 3Q report has opened an excellent entry into the stock for long-term investors. We call out that Mr. Hutter, Mr. Rosenzweig also hold this opinion, as they purchased over $50,000 and $25,000 of stock in the open market two days following the earnings drop respectively.

Inflection Financials

Margins

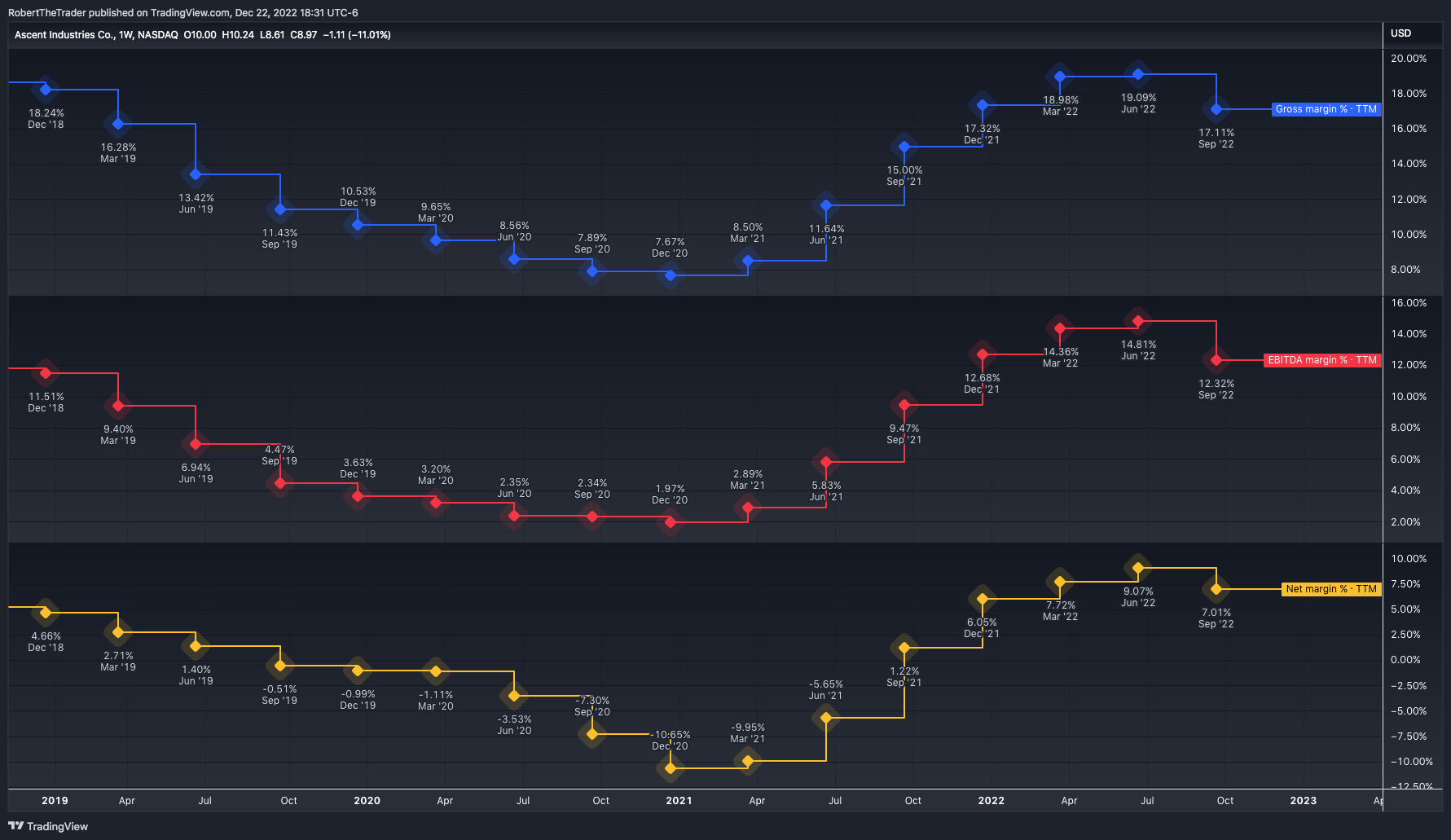

Since the new management has stepped into ACNT, there has been a clear and robust inflection across all financial metrics. While the 3Q report was a step back, we urge investors to step back and look at the bigger picture. This bigger picture being the TTM metrics. Why we highlight the TTM statistics is because the historically the tubular business ACNT operates in can be very volatile. This was obviously observed through parts of both 2021 and 2022. With this in mind, looking at TTM metrics allows one to drown out the noise or messiness of any specific quarter and really gain a better sense of how the business is operating.

{kind=link}

ACNT TTM Margins (Tradingview)

Looking at the TTM margin profile of ACNT truly puts into perspective how much improvements management have already implemented into the business. Even with the expected depressed margins in 4Q and slightly impacted margins in 1Q, we anticipate these TTM margins to remain trending upwards. While the work that has been done is impressive, what is most important for investors is what work will be done in the future to continue to improve margins.

Through both our conversations with management and their public statements, our view is that future margin expansion will be fueled by four main sources.

- The inherently higher margin Chemical business becoming a larger contributor

- Eliminating lower margin tubular revenue and backfilling that capacity with higher margin jobs

- Automation of the production floor

- Acquisitions of higher margin chemical plants

We believe that these four objectives for margin expansion are achievable and view the likelihood of it being very high. Management has made it clear that their goal over the next 24 months is to shift the revenue split between the tubular and chemical business from 75/25 to 50/50. This initiative in itself would raise the overall margin profile of ACNT as the chemical business carries a higher margin profile. For perspective, on an EBITDA margin run-rate basis, management is aiming for the tubular business to see 10-15% margins and the chemical business for 13-20% margins.

The elimination of low margin revenue should also provide a tailwind for margins in 2023. A leftover from past management, ACNT currently has certain tubular contracts that receive low single digit EBITDA margins. While revenues likely see a decline in the 1H of 2023 due to these contract not renewing, we would still view it as a net positive. This is because it will open up production capacity for ACNT to fulfill higher margin jobs, aligning with the long-term goals for ACNT.

While management has already significantly improved worker safety on the production floor of their facilities, going from >7 accidents a year to a touch above 3, they have yet to implement much of theirs plans for automation. These plans of automation will initially hit margins because the spending on automation is not offset by more demand such as marketing or sales spend does. However, the negative impact on margins will be transitory and once the automaton is in place ACNT's will greatly benefit from less labor costs, quicker production times, and expanded volume ability.

Lastly, we believe that ACNT has developed a robust pipeline of potential M&A targets within the specialty chemical space. We will flesh out this concept more in the acquisition section of our thesis, but these acquisition targets will be immediately accretive to margins as the DM acquisition was.

Revenue

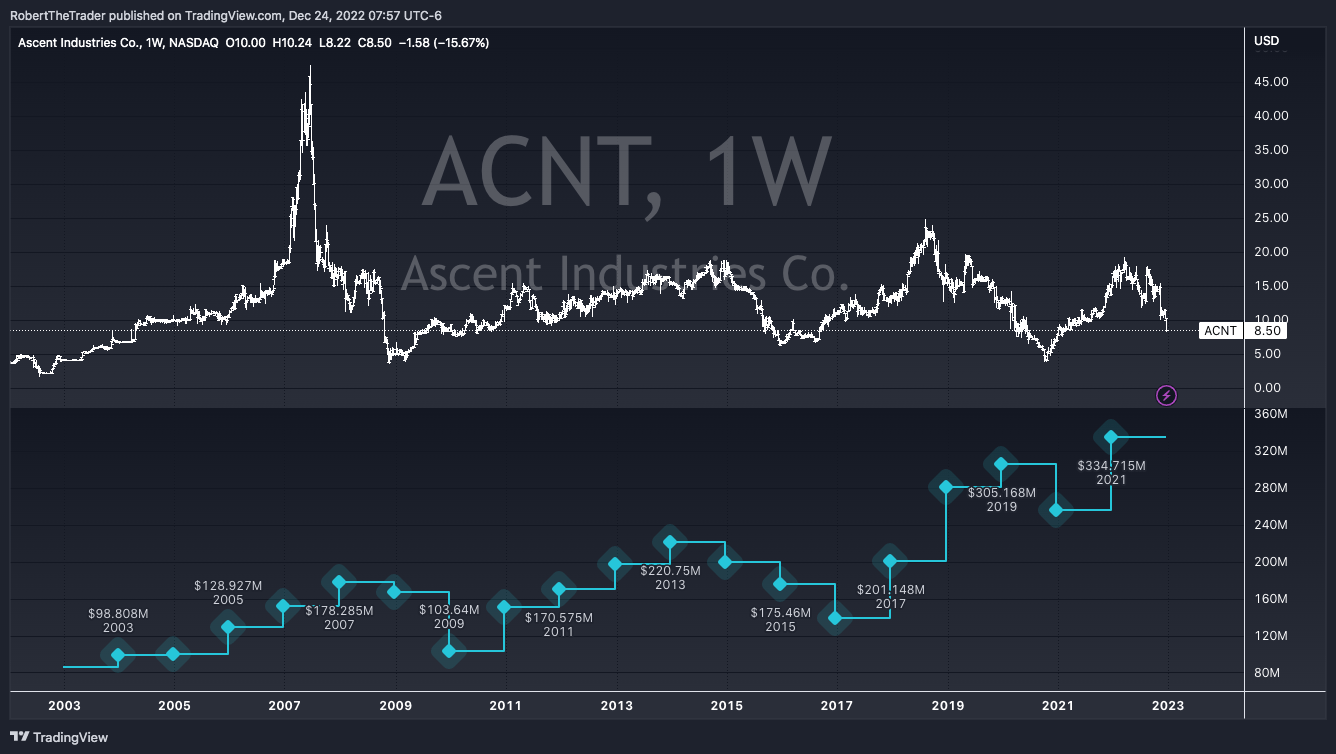

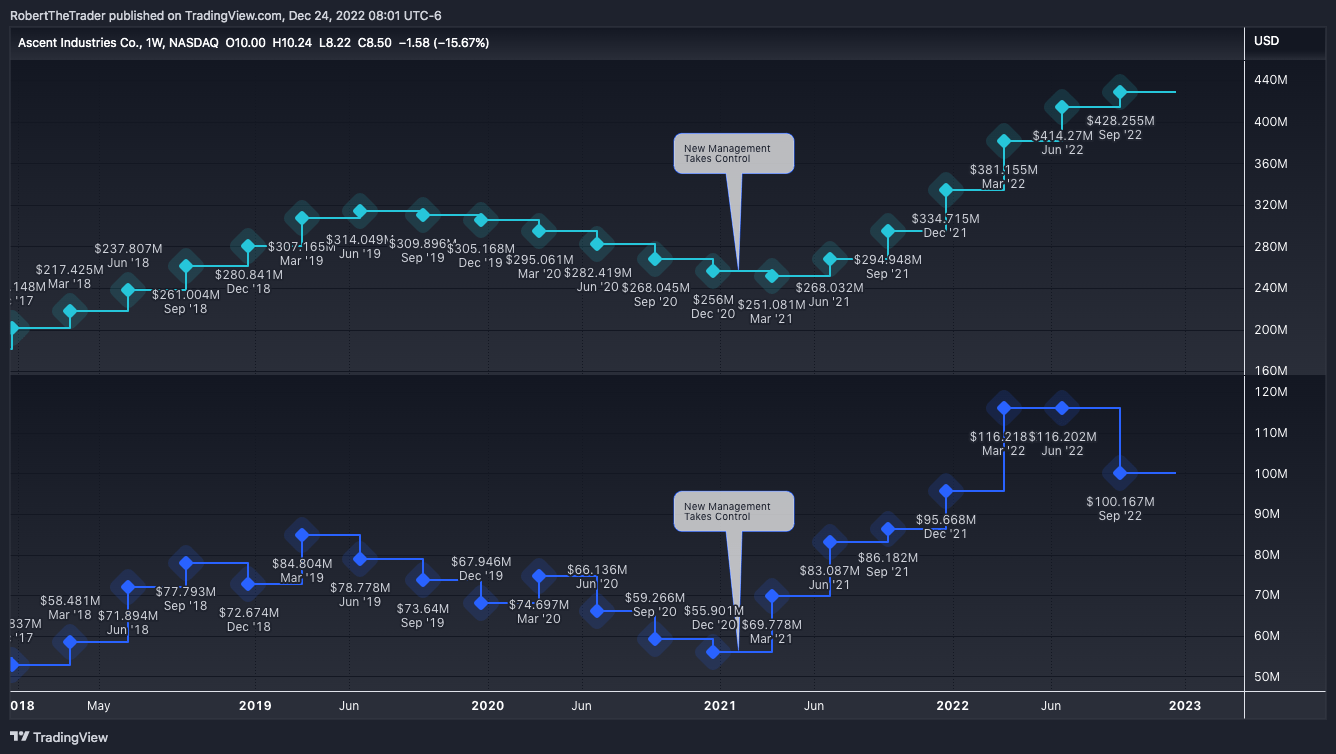

Along with an inflection in margins, ACNT has also experienced a major inflection in their revenue. As we have previously noted, revenues did benefit from a major spur in demand through parts of 21 and 22 but even with that accounted for the revenue growth ACNT has seen under new management has been impressive. We first point out that the $334M in revenues for 2021 was a record for ACNT, 10% above the previous high. Equally impressive, in all seven quarters since new management stepped in, ACNT has seen TTM revenues increase. In addition to this, five of the seven quarters individually saw q/q growth and six have seen y/y growth.

{kind=link}

ACNT Yearly Revenue (TradingView)

{kind=link}

ACNT Quarterly/TTM Revenues (TradingView)

We model ACNT exiting 2022 revenues with north of $420M in revenues, representing 25% growth. While we do forecast revenues down 8% in 2023 to account for likely lost contracts, we see a return to growth and record revenues in 2024 and beyond. We believe the growth ACNT will realize in the future will be spurred by:

- Newly implemented "One Team" approach

- Operational efficiencies

- Cross Selling

Previously, ACNT was an extremely disjointed and disconnected organization before new management stepped in. Two examples to highlight this were first sales teams would often, unknowingly during the fact, be fighting against one another for the same business. This lead to those low margin contracts we mentioned earlier, as sales personnel were incentivized to bring in any type of revenue regardless of the margin profile. So aligning with their economic incentives, sales teams would low ball bids on project to get that revenue unknowingly taking a higher margin job away from another team within ACNT. Secondly, ACNT's 9 manufacturing plants previously would only store products made within that facility. This was extremely inefficient especially for a small company whose facilities have the ability to store outside made products. The 9 plants are across 8 different states so there is a good geographic footprint ACNT inherently had, but this edge was essentially neutralized under old management. As customers would still have to pay for individual shipping from the different plants, wait for the product, and deal with a completely other team.

Now, under the "One Team" approach management has implemented, sales personnel are unified either under Ascent Tubular or Ascent Chemical, so each sales team has full awareness of what ACNT as a whole is bidding on and avoid cannibalizing margins. Also to increase efficiency, each plant will store high-demand items specific towards that region regardless of what plant produced it. This initiative has been one of the proponents of on-time deliveries rising from sub 30% under previous management to better than 80% now. We also believe that the more unified organization will lead to amble cross-selling opportunities. Further amplifying the cross-selling opportunities are the industry connections that new management, specifically Mr. Hutter, Lynch, and Zuppo, bring to ACNT. We believe their expansive industry networks through decades of experience and board positions they hold on trade organizations within their respective industry will provide both new relationships and amble cross selling opportunities.

Deleveraging

Under the guidance of new management ACNT has also seen an impressive improvement of its balance sheet and leverage ratios. These improvement have been driven by all of the previous initiatives we have mentioned. In addition, a fully subscribed rights offering in December of 2021 for $10M also improved the liquidity of ACNT. The offering ended with 785K shares priced at $12.75, important to note was the offering was done exclusively to existing shareholders. Even though this did happen over a year ago, we still feel it highlights a strong shareholder base for ACNT.

Improving the balance sheet and deleveraging the business had been a top priority for new management upon gaining control of ACNT. This is because they knew this was needed in order to execute on the M&A strategy they intended to pursue.

ACNT Leverage Ratio (ACNT Investor Slides)

As shown above, ACNT has significantly reduced its net leverage ratio from over 8x to a very reasonable 1.4x. Again, we want to note that we expect this ratio to tick higher over the next two quarters. This is due to the headwinds we've previously called out that ACNT will face during that time, but with no debt covenants investors should not fret over this.

M&A

The M&A roadmap for ACNT is robust and we believe will play a major factor in the bull case for the stock. We believe that ACNT has developed a pipeline of accretive acquisitions worth over $350M in revenues seeing EBITDA margins in the high teens. The overwhelming majority of this targets are within the specialty chemical space. This is because management has specifically focused on acquisitions in the space due to their high margin profile, low capex, and the fact that the specialty chemical is extremely fragmented.

This fragmentation of the market begun to occur in the 1980s when larger businesses who owned these chemical plants begun to spin these "dirty assets" off their books. In most cases, these spin-offs were sold to the head of the plant and have continued to be ran, owned, and operated by that same person or their family. Another reason for the fragmentation of the market is that each type of chemical facility is usually only equipped to produce certain products, this then leads into the fact that many large blue-chip customers have only one sole source for certain mission critical chemicals. Keeping in mind the owners of these plants and the lack of supply chain diversity their customers have, the industry is ripe for M&A. Many of these owners and operators of prospective plants are in their late 60s or 70s and are looking for a liquidity event to cash out. We think ACNT can provide that. Many of the blue chip customers want diversity in their supply chain of chemical products, and we believe ACNT can provide that.

Management has already shown their ability to execute successful acquisitions at reasonable prices through the DC acquisition. We also not that during 2022, ACNT has noticed other bidders entering the market and rather than paying a modest 6x EBITDA which ACNT looks to do, they are offering 10-12X EBITDA. This is why ACNT has not had any acquisitions in 2022. However, during our discussions with management they did highlight that many of those deals that were happening at 10-12x EBITDA are now coming back to market as the buyer was unable to find financing. We think this patience and value oriented mindset is a major positive moving forward, as ACNT has shown they will not overpay for an asset even if the market is. While ACNT has seen debt grow under new management, it has been so sustainably and prudently. Going forward, we expect any acquisitions will be underwritten in the same way. As for funding future acquisitions, ACNT will fund those through the existing $36.7M of borrowing capacity to go along with the $40M in additional borrowing capacity through a committed accordion feature. Management has noted that they are hesitant to raise capital through an equity round due to the stocks poor 2022 performance, but would be open to that type of funding when the stock returns the teens.

We also note that Mr. Hutter grew his previous business, UPG, through more than a dozen acquisitions of smaller industrial steel players. Ultimately scaling the business to over $1.6B in yearly revenues by the time he left. There has been a clear demonstrated ability by management and ACNT as a whole to successfully identify acquisition targets, pay the correct price for those targets, and integrate them into the business smoothly. In sum, we believe this $350M pipeline of specialty chemical acquisition targets that ACNT has developed will provide tremendous upside to the stock. ACNT would benefit from increased revenues, higher margins, and more cross selling opportunities.

Valuation

We believe that ACNT shares are currently undervalued when comparing them to both their specialty chemical peers and tubular peers. Conglomerate businesses do often trade at discounted valuations to its peers but we believe ACNT stands to close that valuation gap through the futures initiatives we have laid out.

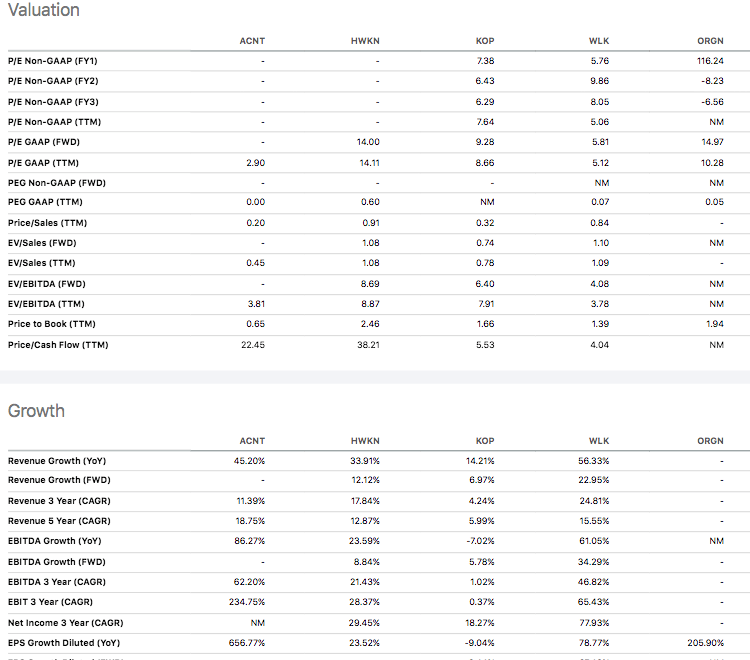

First, comparing ACNT to similar tubular/metal comps it trades at a discounted valuation even though ACNT has the strongest revenue and EPS growth. We used Seeking Alpha's peer group in to find proper comps of Universal Stainless & Alloy Products Inc. ( USAP ), Olympic Steel ( ZEUS ), and Haynes International ( HAYN ). ACNT's 2.9 TTM PE ratio is still nearly a full turn lower than the lowest comp ZEUS's.

{kind=link}

ACNT Tubular/Metals Comps (Seeking Alpha)

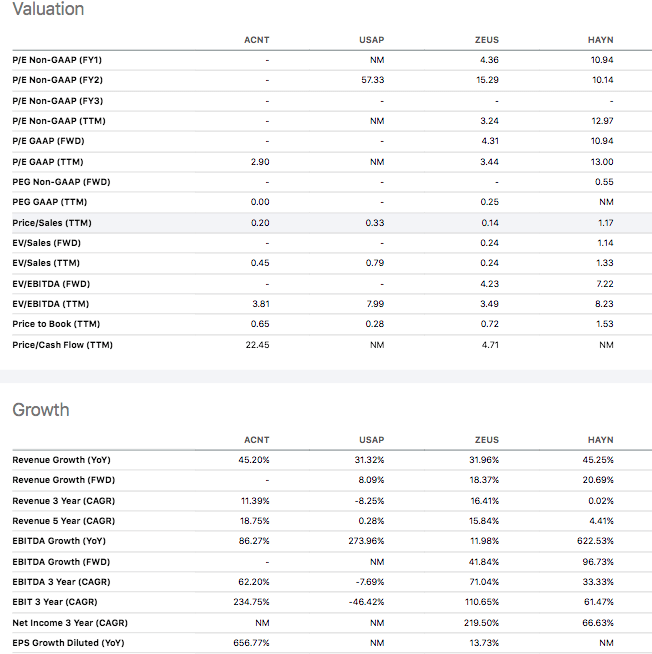

We found our chemical comps of Hawkins ( HWKN ), Koppers Holdings ( KOP ), Westlake Chemical Partners (WLKP) and Origin Materials ( ORGN ) using both Seeking Alpha's industry feature along with SEC EDGAR's SIC feature to. When comparing ACNT to chemical peers, the same discounted valuation occurs but only at a more drastic rate. Where ACNT's PE of 2.9 stands far below the average comp PE multiple of 9.54. This discounted valuation is again despite ACNT showing stronger growth statistics across Revenue, EBITDA, and EPS growth.

{kind=link}

ACNT Chemical Comps (Seeking Alpha)

We also note to readers that, ACNT is pivoting to have a larger focus on the chemical business going forward. We believe that this pivot in business focus should be followed by a higher multiple as chemical peers have a much higher multiple than the metals/tubular comps.

We believe it is important to note that ACNT's 3Q EPS of $0.06 is a sharp fall from the previous three quarters. As we have highlighted, we do see increased expenses over the next two quarters along with a likely a drop in revenue, which we anticipate will push earnings down during that time, in consequence raising the PE ratio. Investors should expect the PE ratio of ACNT to climb higher through the first half of 2023, but ultimately we see ACNT exiting 2023 with quarterly EPS back in the range $0.60-$0.90 range and steadily climbing through 2024.

Risks

We believe investing in ACNT incurs the following risks

- Commodity pricing and inflation - A large part of ACNT's COGs involve commodities. If they are unable to insulate themselves from inflation in those goods their margins will erode and the stock will suffer.

- Inability to replace low margin jobs - A major part of our thesis revolves around the fact ACNT plans to replace low margin jobs. If the company is unable to refill that production capacity with higher margin jobs or any jobs at all, the stock will suffer.

- Management leaving - The new management that leads ACNT now is a major reason for our bullishness. If any were to leave the company, that would negatively affect our view on ACNT's ability to execute its future plans and we believe the stock would suffer.

- Acquisitions - If ACNT is unable to successfully find acquisition targets, the financials will likely hit a ceiling. If future acquisitions are not successfully integrated into the business, that would also negatively affect the stock.

- Insider Selling - Another reason for our bullishness is how well aligned management and insiders are with the overall shareholder base. If insiders begin to sell before the changes we see in the future take place or after unexpected road bumps occur, we would view this as a negative and believe the stock would suffer.

Summary

In summary, we believe ACNT provides an excellent opportunity for long-term orientated investors who have the patience to wait through two likely rocky quarters. We believe that new management have already created significant change within a previously sleepy small company. Management and insiders are also very well aligned with shareholders, being that fact that insiders owning over 23% of the stock. We see amble opportunities to execute future margin expansion as well as a very accretive acquisition roadmap in the future. For all these reasons along with others previously stated, we believe ACNT stands out as a top micro-cap pick heading into 2023.

For further details see:

Ascent Industries: Impressive Early Innings Turnaround