ASG - ASG: Growth That Is Less Dependent On The Magnificent 7

2024-01-15 23:41:53 ET

Summary

- The multi-cap Liberty All-Star Growth Fund is positioned to do well if a soft landing broadens stock performance beyond the Magnificent 7.

- ASG trades at over a 6% discount to NAV, which provides a tailwind if it goes to a premium as it has in other cycles.

- The more active management and better discount make ASG a better pick than its bigger brother USA.

The Little Brother With More Potential

Liberty All-Star Funds is a family of two closed-end funds sponsored by ALPS Advisors. The "All-Star" in the name refers to the management structure of the funds. Fund assets are allocated among a handful of different independent investment management firms. These managers focus on different styles (value/growth) and market caps (small/mid/large).

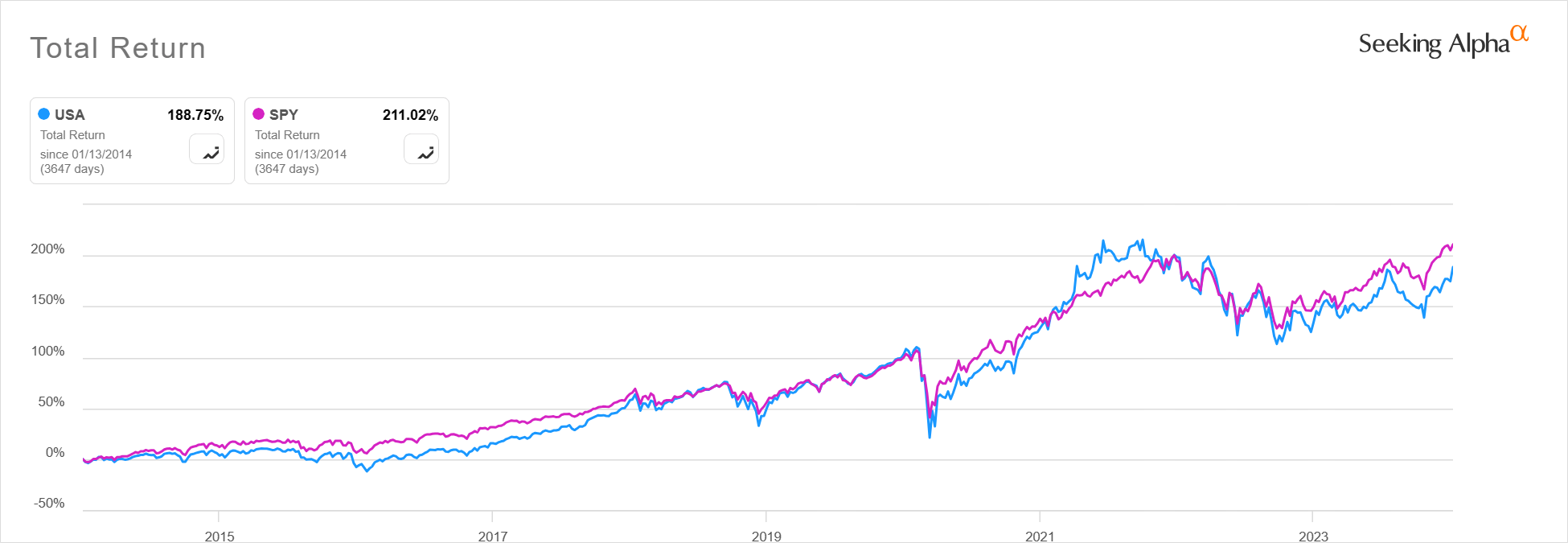

The larger of the two funds is the Liberty All-Star Equity Fund ( USA ) with $1.8 billion in assets under management. USA gets plenty of focus here on Seeking Alpha, especially by income-focused analysts because of the fund's policy of paying out 10% of net asset value each year. While most authors and commenters refer to these distributions as "dividends", only a small part comes from dividend income of the fund's holdings. The rest comes from capital gains if the fund's assets have appreciated in value or return of capital if they have not.

Despite the active management structure of USA, fund performance over time tracks very closely with S&P 500 index ETFs ( SPY ) ( VOO ) ( IVV ) but usually trails slightly thanks to the 1% expense ratio of the fund.

{kind=link}

I have often stated in article comments that investors can save most of the 1% management fee by owning an S&P 500 ETF and selling a portion of it quarterly to generate similar distribution levels as USA. This thesis was also outlined in a recent article .

Nevertheless, many investors do not want to be bothered with selling and are willing to pay the higher management fee for that service. I'm not going to try to dissuade anyone from doing that in this article even though I think differently. Instead, I would like to raise awareness of the other fund in the Liberty All-Star family, the Liberty All-Star Growth Fund ( ASG ). This fund is much smaller, with just $328 million under management. ASG shares many of the characteristics of USA, including the use of multiple asset managers and the distribution policy. In the case of ASG, the three fund managers are chosen for their focus on small-, mid-, or large-cap growth. The distribution policy targets 8% of NAV, or 2% quarterly. Unlike USA however, ASG appears to be more willing to deviate from the benchmark, resulting in more variable performance over time. The fund also has a bit more deviation in its premium or discount to NAV. Both of these characteristics create more trading opportunities to add alpha. Both of these characteristics are currently in favorable positions.

More Variability In Holdings

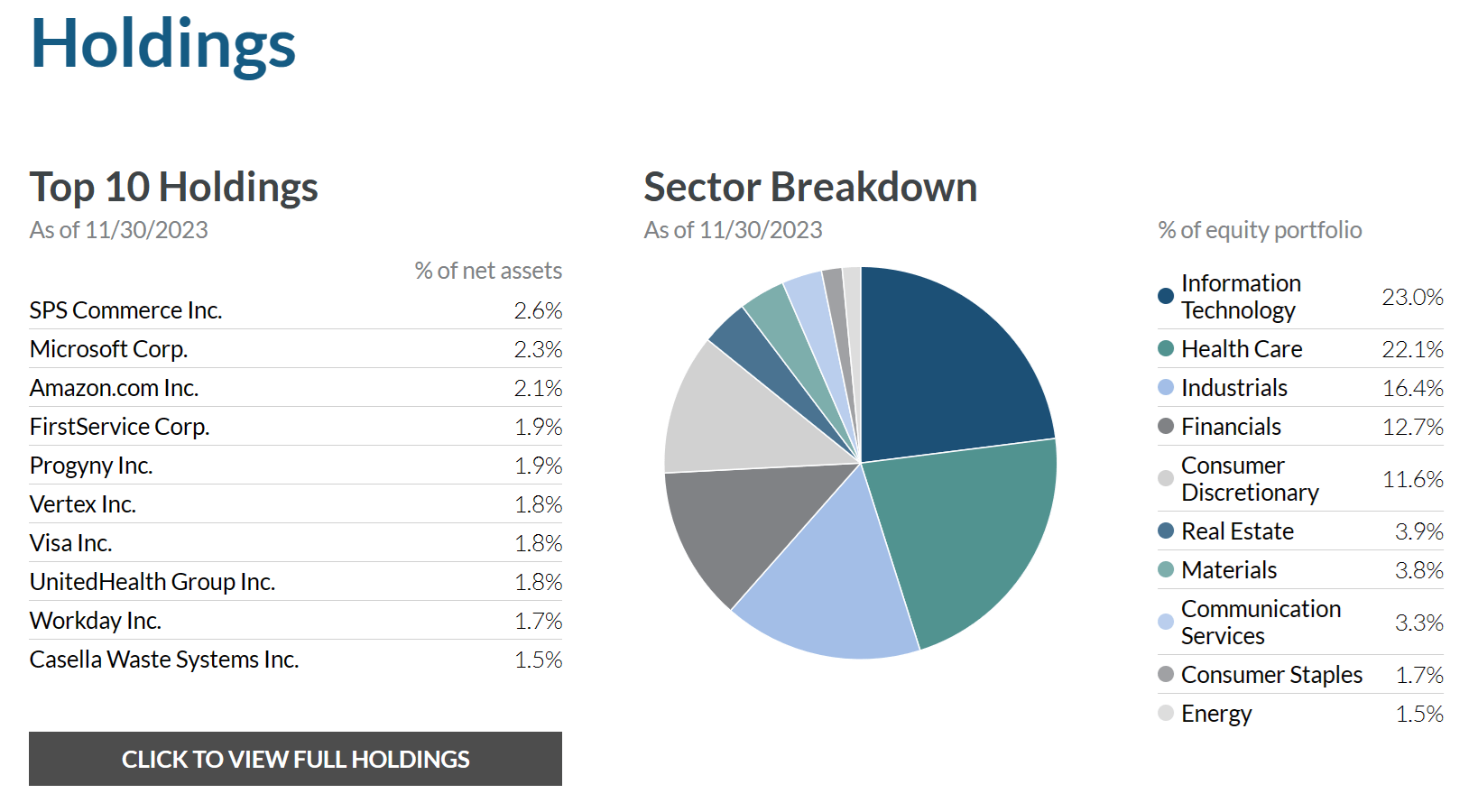

ASG is a true multi-cap fund as we see from its top holdings. While Magnificent 7 members Microsoft ( MSFT ) and Amazon ( AMZN ) are in the top 10, they only make up 4.4% of the fund, and the rest of the top 10 contain positions across the market cap spectrum.

{kind=link}

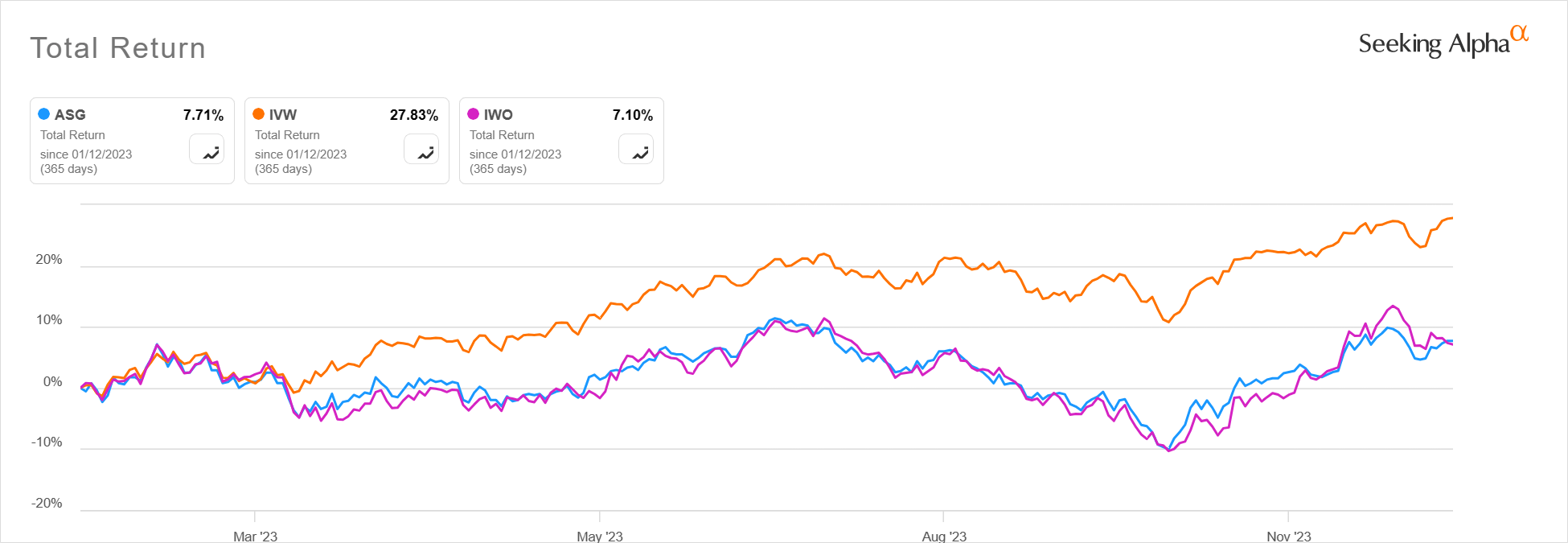

This positioning has hurt the performance of ASG recently. Over the past year, we see that the fund tracked closely with the small-cap iShares Russell 2000 Growth ETF ( IWO ) and lagged considerably behind the large-cap iShares S&P 500 Growth ETF ( IVW ).

{kind=link}

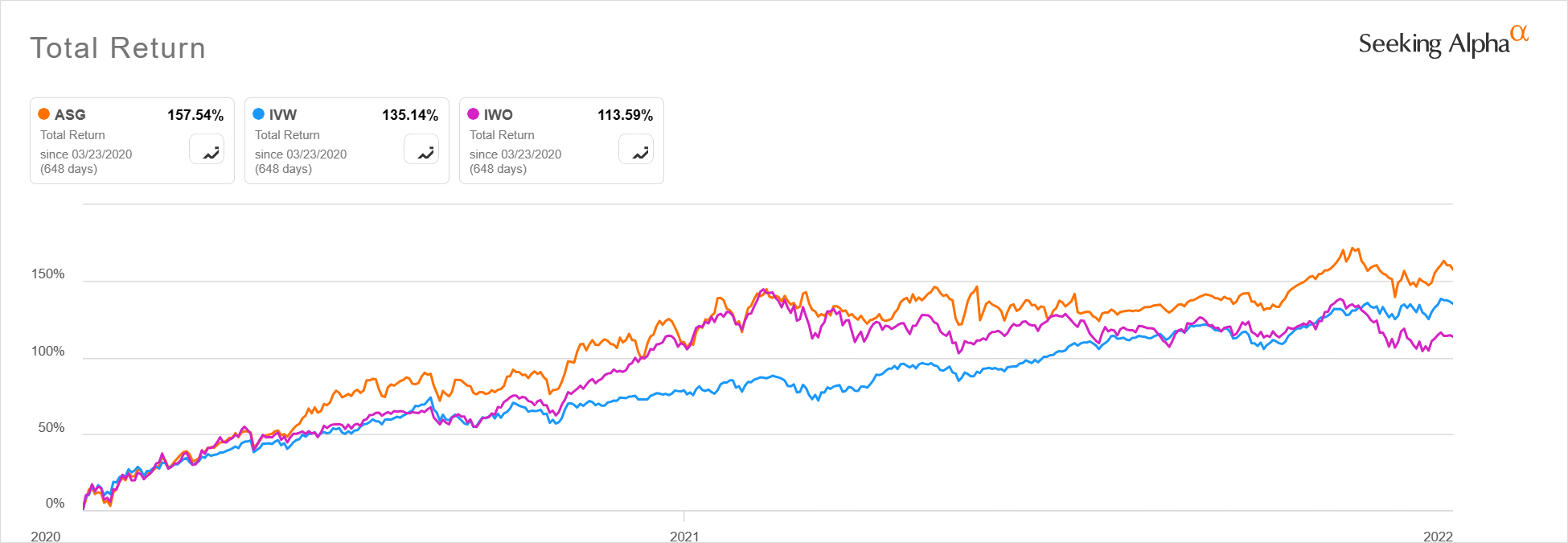

If you believe as I do that the Magnificent 7 are ready to take a breather and performance will broaden out to a wider set of stocks this year, then ASG could become an outperformer, as it was during the pandemic bull market of March 2020 to December 2021.

{kind=link}

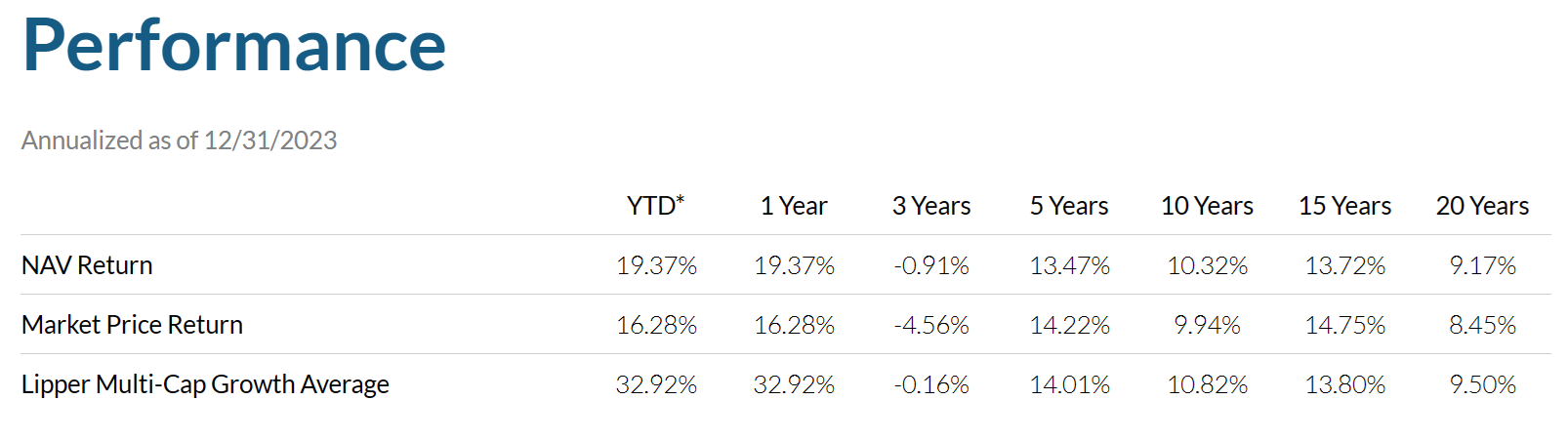

Over longer periods, ASG has done better compared to the multi-cap benchmark than it has recently.

{kind=link}

The NAV performance has matched the benchmark better than the market price performance. The funds discount to NAV provides another current trading opportunity.

Discount Presents A Buying Opportunity

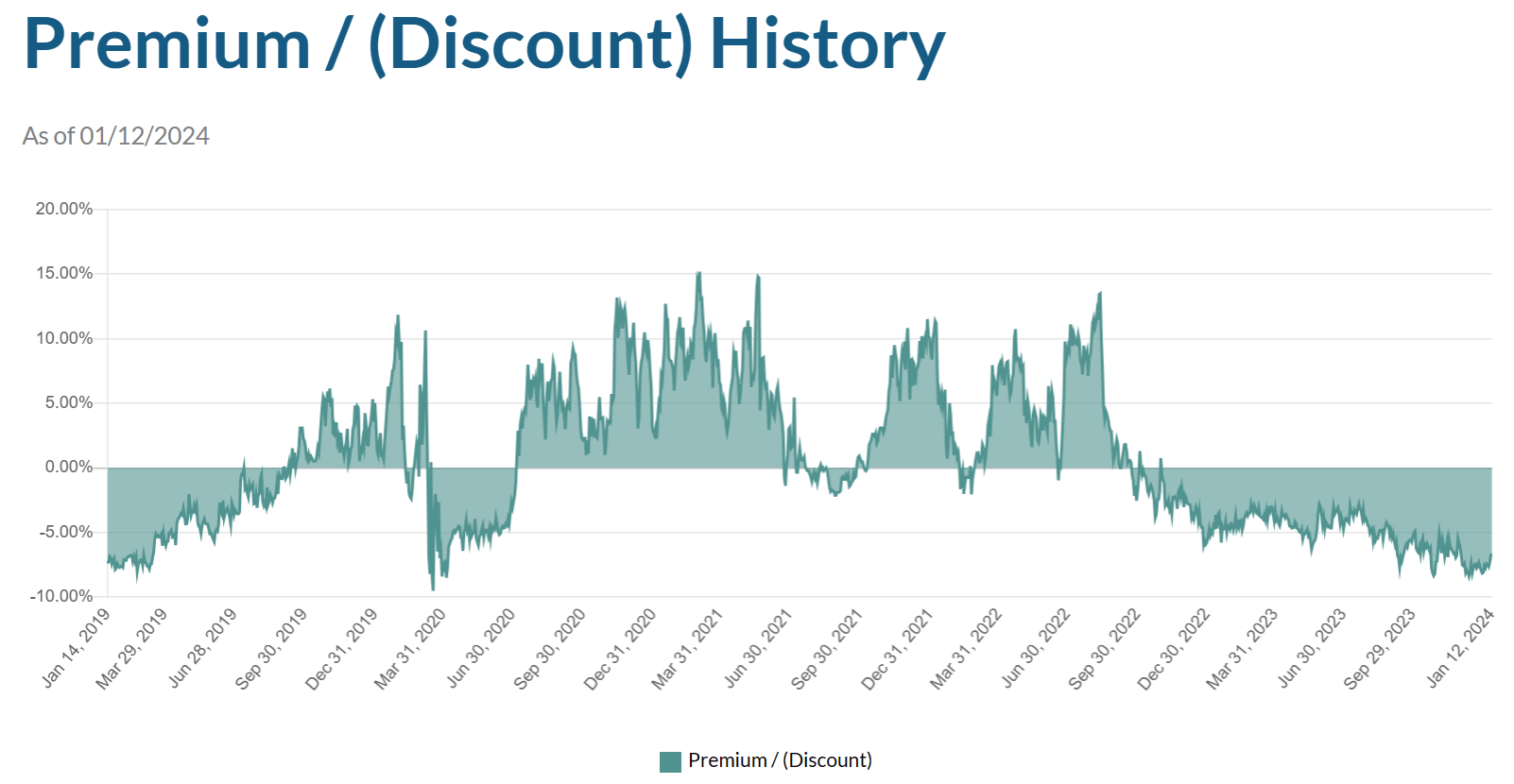

ASG in the past 5 years has traded anywhere between a discount of around 8% to NAV to a premium of almost 15%. From the pandemic lows in March 2020 to the top of that bull market at the end of 2021, the fund went from a deep discount to a high premium. This was a contributor to the fund's outperformance over index ETFs during that period.

Looking at recent data, ASG was back near 5-year low discounts in December and is still 6.7% below NAV as of 1/12/24.

{kind=link}

USA has exhibited a narrower variation in premium/discount over the last couple years and currently trades at just a 1.5% discount to NAV.

More Sustainable Distribution

Many investors buy the All-Star funds because of their high distributions relative to index ETFs. Although ASG at 8% of NAV is lower than USA's distribution at 10% on NAV, ASG looks more sustainable. ASG payout in 2022 came 100% from long-term capital gains. The fund has not paid return of capital since 2012. In contrast, USA's distributions have included return of capital in about half the years since 2012. The funds have not yet released distribution classifications for 2023, but I expect neither one to have return of capital due to the strong market performance last year.

Risks

ASG looks ready to rebound based on regression to the mean of smaller cap growth after a year of much stronger performance from the mega-cap Magnificent 7. This is more likely in the event of a soft landing in the economy where companies of all sizes can perform well. If we get a more significant slowdown in the economy, the mega caps may outperform due to their perceived relative safety. In case of a recession, value stocks may be the leader with all growth stock indexes lower.

Active management is also a risk with ASG's 1.1% expense ratio, even higher than USA. Along with fees cutting into investment income, the greater flexibility of the active managers provides more opportunities for poor stock selection or asset allocation.

Conclusion

Liberty All-Star Funds provide a way for investors to get broad equity market exposure while collecting distributions of 8%-10% per year. While it can be more efficient to own index ETFs yourself and sell shares as needed for income, many investors do not mind paying a higher management fee to outsource this activity. Of the two funds in this family, I prefer ASG, the Growth Fund. Unlike USA, the management actually appears "active", judging by the greater variability of returns compared to the growth fund benchmark. While ASG has underperformed in the last two years, it could be ready to outperform again as it did in 2020 and 2021. A soft landing with performance broadening out beyond the Magnificent 7 provides the best chance for ASG to do well. ASG also recently bottomed in terms of its discount to net asset value, so the cycle looks ready to provide a tailwind with market price swinging to a premium.

For further details see:

ASG: Growth That Is Less Dependent On The Magnificent 7