VCISF - ASGI: Buy This Infrastructure CEF To Make Money Even In The Absence Of Growth

2023-05-01 17:44:53 ET

Summary

- The money supply is shrinking and the Federal government is gobbling up an ever-growing percentage, starving private businesses of growth capital.

- abrdn Global Infrastructure Income Fund invests in infrastructure companies that should be able to deliver an acceptable return even in the absence of growth.

- The ASGI closed-end fund has much better international diversification than most other global closed-end funds, which brings certain advantages to a portfolio.

- The CEF is relying a great deal on capital gains to fund its distributions, which could be a problem.

- The ASGI fund is currently trading at an incredibly attractive discount to net asset value.

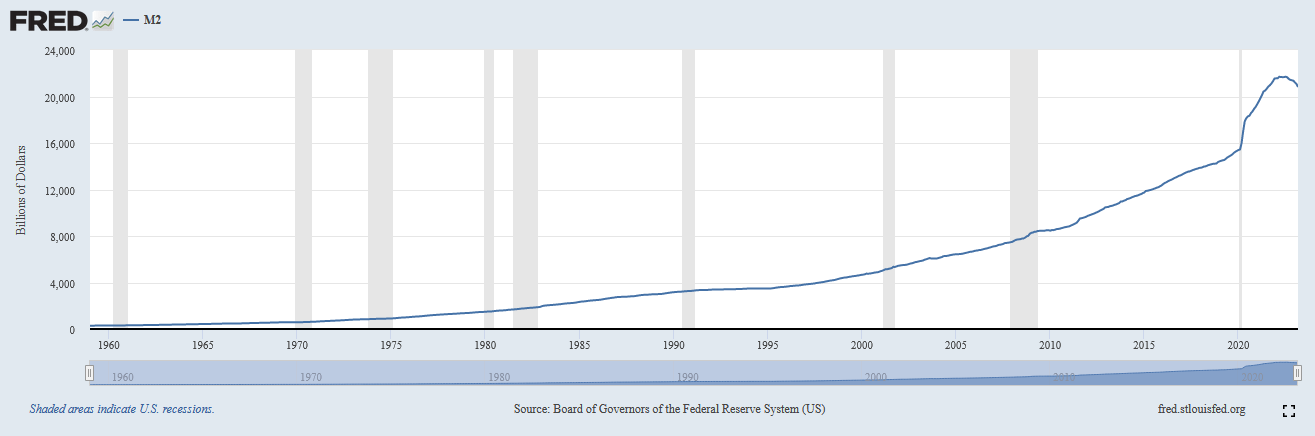

We are certainly living in interesting times, as the current rate of inflation in the United States is running at a four-decade high, although there are some signs that it is slowing down. However, there is a very real possibility that the inflation rate may soon take off again , which will force the Federal Reserve to continue to raise rates well beyond what the market currently expects. In addition to this, the money supply has declined for the first time since the United States abandoned the gold standard:

{kind=link}

Despite this, the Federal Government refuses to cut spending. Since the Federal Government will always get the funding that it needs, the government is basically using up a greater and greater proportion of the money that exists in the economy. This forces us to question where the growth that the stock market is currently expecting will come from as private companies are starved of the capital that they need to generate that growth. It is uncertain how this could play out, but it could very easily result in a stock market crash once investors realize these realities. As such, it may be a good idea to move some money into reasonably safe havens that will continue to earn a return regardless of anything that happens.

One possible safe haven is infrastructure. Infrastructure consists of things like railroads, cellular towers, roads, pipelines, and other things that are necessary for modern society to function. These things can provide an effective safe haven because they will be used by consumers and businesses and earn money regardless of anything that happens in the economy. After all, will a cash-strapped retiree spend the last pennies of his Social Security check on paying his electric bill or buying one of Apple's ( AAPL ) iPhones? The latter is rather useless without cellular towers and electricity. As such, we can count on the companies that provide infrastructure to be steady earners for us going forward.

This is evident when we consider that most of these companies enjoy remarkably stable cash flows from year to year and pay out very high distribution yields. For example, the Alerian MLP Index ( AMLP ), which includes most companies that operate energy pipelines, currently yields 7.85%. That yield certainly provides an acceptable yield in an environment in which growth is hard to come by. However, there are things out there with even more attractive yields.

One of the best ways to invest in infrastructure companies is by purchasing a closed-end fund that invests in these companies. These funds are capable of employing certain strategies that can boost their effective yields well beyond that of any of the underlying companies, which is a feature that exchange-traded and open-ended funds cannot accomplish. In this article, we will discuss the abrdn Global Infrastructure Income Fund ( ASGI ), which is one fund that clearly falls into this category, as its 8.04% yield is higher than most of the things that can be found in the market today. I have discussed this fund before, but as a significant amount of time has passed since then a great many things have changed. This article will, therefore, focus specifically on those changes as well as provide an updated analysis of the fund's finances. Let us investigate and see if this fund could be a worthy addition to a portfolio today.

About The Fund

According to the fund's webpage , the abrdn Global Infrastructure Income Fund has the stated objective of providing its investors with a high level of total return with an emphasis on current income. This is hardly surprising for an infrastructure fund, even one that invests in common equities. As we can clearly see here, this fund is a common equity fund as nearly all of its assets are invested in that security type:

CEF Connect

As I have pointed out in various previous articles, common equity is by its nature a total return vehicle. After all, investors generally purchase common equities in order to receive an income from the distributions and dividends that they pay out, as well as benefit from capital gains as the issuing company grows and prospers. In the case of infrastructure companies, there is much greater weight put on the distributions. This is because infrastructure companies tend to have fairly low growth rates, so they make up for this by distributing a substantial percentage of their cash flows to the investors. After all, they do not usually have places to invest the money internally. We only need so many roads or electric lines running down the street, after all! The nice thing about this strategy versus a high-growth company is that the investors can receive a return in flat markets that would likely not reward a company that depends on constant growth or capital appreciation to deliver a return. As I discussed in the introduction, this is an appealing characteristic today because it is questionable how strong the growth will be in the economy with the government demanding an ever-greater share of the money supply.

As my long-time readers are likely well aware, I have devoted a considerable amount of time and effort to discussing infrastructure companies such as pipelines, utilities, and telecommunications companies on this site and elsewhere on the Internet. As such, many of the largest positions in the fund's portfolio will probably be familiar to most readers. Here they are:

abrdn

I have published articles on NextEra Energy ( NEE ), Kinder Morgan ( KMI ), The Williams Companies ( WMB ), and Enbridge ( ENB ) on this site in the past. Three of these are crude oil and natural gas pipeline operators, while NextEra Energy is the largest electric utility in the United States. Admittedly, I have normally discussed more than four companies listed in the top holdings of most infrastructure funds, so this one clearly offers different holdings than many other infrastructure funds. The fact that it is managed by abrdn offers a partial explanation for this, as abrdn is a foreign company. The fund manager is based in the United Kingdom, so its funds tend to offer much more international exposure than funds managed by American companies. We can see this in the fact that only 38.0% of the securities in this fund come from American issuers:

abrdn

Normally, we see a 60%+ weighting to the United States in any global closed-end fund, so the fact that this one offers much more international diversity is nice to see. The reason for this is the protection that international investments provide us against regime risk. Regime risk is the risk that some government or other authority will impose some law or take another action that has an adverse impact on a company in which we are invested. The only realistic way to protect ourselves against this risk is to ensure that only a relatively small percentage of our assets is invested in any single country. As we can see, this fund is certainly doing this as its American exposure is less than most funds. As such, including it in your portfolio could help reduce your overall exposure to the United States and improve your diversification.

There have been several changes to the fund's largest positions since the last time that we discussed it. In fact, the only five companies currently on the list that were still on it back in November are Kinder Morgan, The Williams Companies, Enbridge, Vinci SA ( VCISF ), and Ferrovial, S.A. ( FRRVF ). The remaining companies were all added to the list over the past six months or so. This could imply that this fund does a significant amount of trading, but its 25.00% annual turnover says differently. In fact, that is a very low annual turnover for an equity closed-end fund, or CEF. The reason that this is important is that it costs money to trade stocks or other assets, which is billed directly to the shareholders. This creates a drag on the fund's performance and makes management's jobs more difficult. This is because the fund's managers need to generate sufficient returns to cover the additional expenses and still deliver a return that is acceptable to the investors. There are very few management teams that manage to accomplish this on a consistent basis, which is one reason why most actively-managed funds underperform their benchmark indices. This fund is an exception to this rule, though, as it has usually outperformed the S&P Global Infrastructure Index ( IGF ):

abrdn

Thus, it appears that the management of this fund has certainly proven to be quite competent, although the fund does not have nearly as long of a track record as the index. In addition, past performance is no evidence of future results. However, the fund has performed reasonably well so far, and it certainly has a much greater yield than the paltry 2.12% offered by the index. As such, it could prove to be a very reasonable alternative option for the index for any investor.

Distribution Analysis

One of the attractive things about infrastructure companies is that they typically have very high yields. This comes from the fact that these companies do not generally grow very quickly, so they make up for it by paying out a high percentage of their cash flows to investors. This results in many of these companies having very high dividend yields. For example, here are the dividend yields from the largest companies in the fund:

| Company |

| Dividend Yield |

| Aena ( ANNSF ) |

| 0.00% |

| Ferrovial ( FRRVF ) |

| 2.34% |

| Cellnex Telecom ( CLNXF ) |

| 0.00% |

| Vinci |

| 3.51% |

| NextEra Energy |

| 2.44% |

| Kinder Morgan |

| 6.59% |

| The Williams Companies |

| 5.92% |

| Engie ( ENGIY ) |

| 5.18% |

| Enbridge |

| 6.64% |

| American Tower ( AMT ) |

| 3.05% |

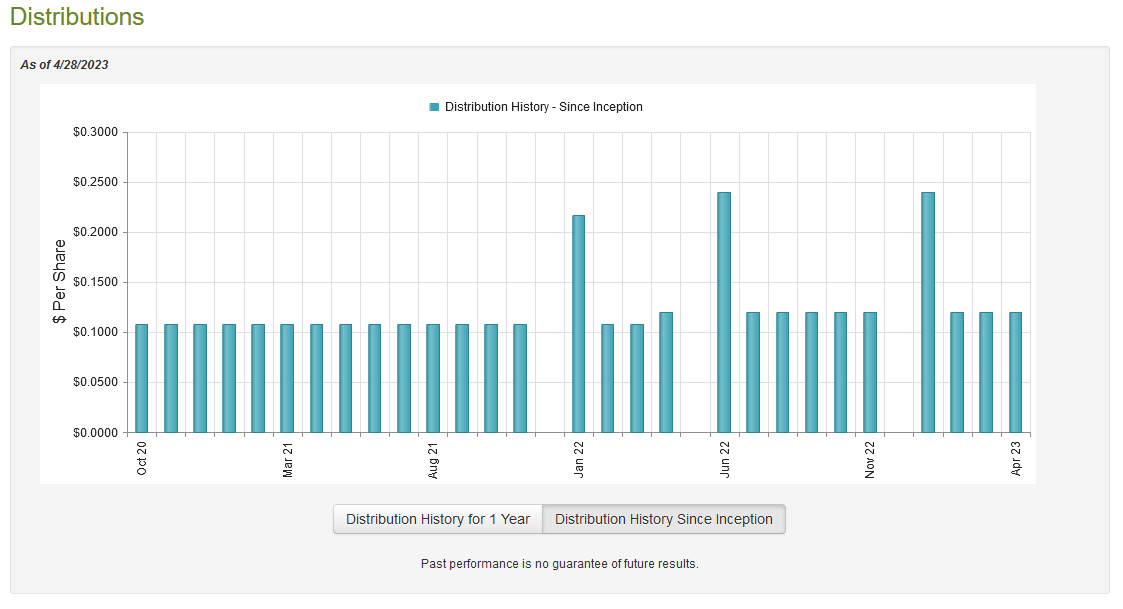

The abrdn Global Infrastructure Income Fund specifically states that it expects to deliver most of its returns to investors in the form of the distributions that it pays out. These distributions will consist of both the income that it receives from the infrastructure companies in the portfolio as well as any capital gains. As many of these companies have fairly high yields, we can assume that the fund's portfolio probably has a very high yield overall and combined with capital gains, it should be able to pay out a remarkably high yield. This is certainly the case as the fund pays a monthly distribution of $0.12 per share ($1.44 per share annually), which gives it an 8.04% yield at the current price. The fund has been remarkably consistent about its distribution over the years as it has never reduced the payout but did increase it back in the middle of 2022 at a time when many other closed-end funds were struggling:

{kind=link}

This distribution history will undoubtedly appeal to any investor that is seeking a stable and secure source of income with which to pay their bills and support their lifestyles. It also demonstrates the strength that infrastructure companies have in challenging market conditions, as most of these companies tend to enjoy remarkably stable cash flows and reasonable valuations that allow them to weather conditions that are devastating for other assets. As is always the case though, it is important that we ensure that the fund can actually afford the distributions that it pays out. After all, we do not want to be the victims of a distribution cut that reduces our incomes and almost certainly causes the fund's share price to decline.

Unfortunately, we do not have a particularly recent document that we can consult for our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on September 30, 2022. As such, it will not include any information about the fund's performance over the past seven months. However, this is still a more recent report than the one that we had available to us the last time that we discussed this fund and as such it should give us a better idea of how well the fund handled the turbulent markets of 2022. During the full-year period, the abrdn Global Infrastructure Income Fund received a total of $3,733,779 in dividends and $144,206 in interest from the assets in its portfolio. When combined with a small amount of income from other sources, the fund reported a total investment income of $4,289,635 over the period. It paid its expenses out of this amount, which left it with $388,849 available for the shareholders. As can probably be guessed, this was nowhere close to enough to cover the $12,129,579 that the fund actually paid out in distributions during the period. At first glance, this is likely to be quite concerning as the fund did not have sufficient net investment income to afford its distributions.

However, the fund does have other ways through which it can obtain the money that it needs to cover the distribution. For example, it might have capital gains that it can pay out. The market in 2022 was actually reasonably good for infrastructure companies, at least when compared to most other assets. The fund thus had some success at earning capital gains, as it reported net realized gains of $12,007,742 but this was more than offset by $29,807,104 in net unrealized losses. Overall, the fund's assets declined by $29,540,092 after accounting for all inflows and outflows during the period. This is likely to be concerning at first glance; however, the fund did have sufficient net investment income and net realized gains to cover the distributions. Thus, it did manage to cover the distributions despite the fact that its assets declined.

The abrdn Global Infrastructure Income Fund's ability to sustain the distribution going forward is questionable, particularly since the net investment income was a lot less than expected given the yields of the assets in the portfolio. The smaller its asset base, the more difficult it will be to get the capital gains that are needed to cover the distribution. I am cautiously optimistic, but we will want to look very closely at the fund's semi-annual report when it is released in a few weeks for more insight.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the abrdn Global Infrastructure Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the money that the investors would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a closed-end fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 28, 2023 (the most recent date for which data is available as of the time of writing), the abrdn Global Infrastructure Income Fund had a net asset value of $21.44 per share but the shares only traded for $17.93 each. This gives the fund's shares a 16.37% discount on the net asset value. This is an enormous discount for any fund and is significantly better than the 14.60% discount that the shares have had on average over the past month. As such, the current price certainly looks like a good entry point.

Conclusion

In conclusion, it will be interesting to see the long-term direction of the market. As the Federal Government consumes an ever-greater amount of the wealth in the economy, the private sector will probably struggle to deliver the growth that many of us have become accustomed to. Fortunately, infrastructure investors are not really worried about growth, since the yields of many of these companies deliver an acceptable return even in the absence of growth. This fund likewise delivers a distribution that is quite acceptable even if the share price remains flat.

Unfortunately, the abrdn Global Infrastructure Income Fund is depending more on capital gains to fund its distribution than I would really like, which may prove problematic in the absence of economic growth. Fortunately, the valuation is incredibly attractive today, and the abrdn Global Infrastructure Income Fund may still prove to be a better investment than many other things in the market.

For further details see:

ASGI: Buy This Infrastructure CEF To Make Money Even In The Absence Of Growth