ASHTF - Ashtead Group: Mega Projects Driving Mega Growth Ahead

2023-09-20 12:02:28 ET

Summary

- Ashtead Group's rental revenue has shown strong growth, making it well-positioned to benefit from large mega projects in the US.

- The company's revenue increased by 19% in 1Q24, with notable growth in the US market.

- Ashtead's prospects in the Mega Projects business are expected to be a major growth driver, with the company doubling its market share over the past quarter.

Summary

Following my coverage of Ashtead Group ( ASHTY ), I recommended a buy rating as the business has demonstrated strong growth in rental revenue, and I expected it to be well-positioned to benefit from the acceleration of large mega projects in the United States. This post is to provide an update on my thoughts on the business and stock. I reiterated my buy rating for ASHTY as I became more bullish about ASHTY's ability to continue finding more deals in Mega Projects, which I expect to be a long-term growth driver for the business.

Investment thesis

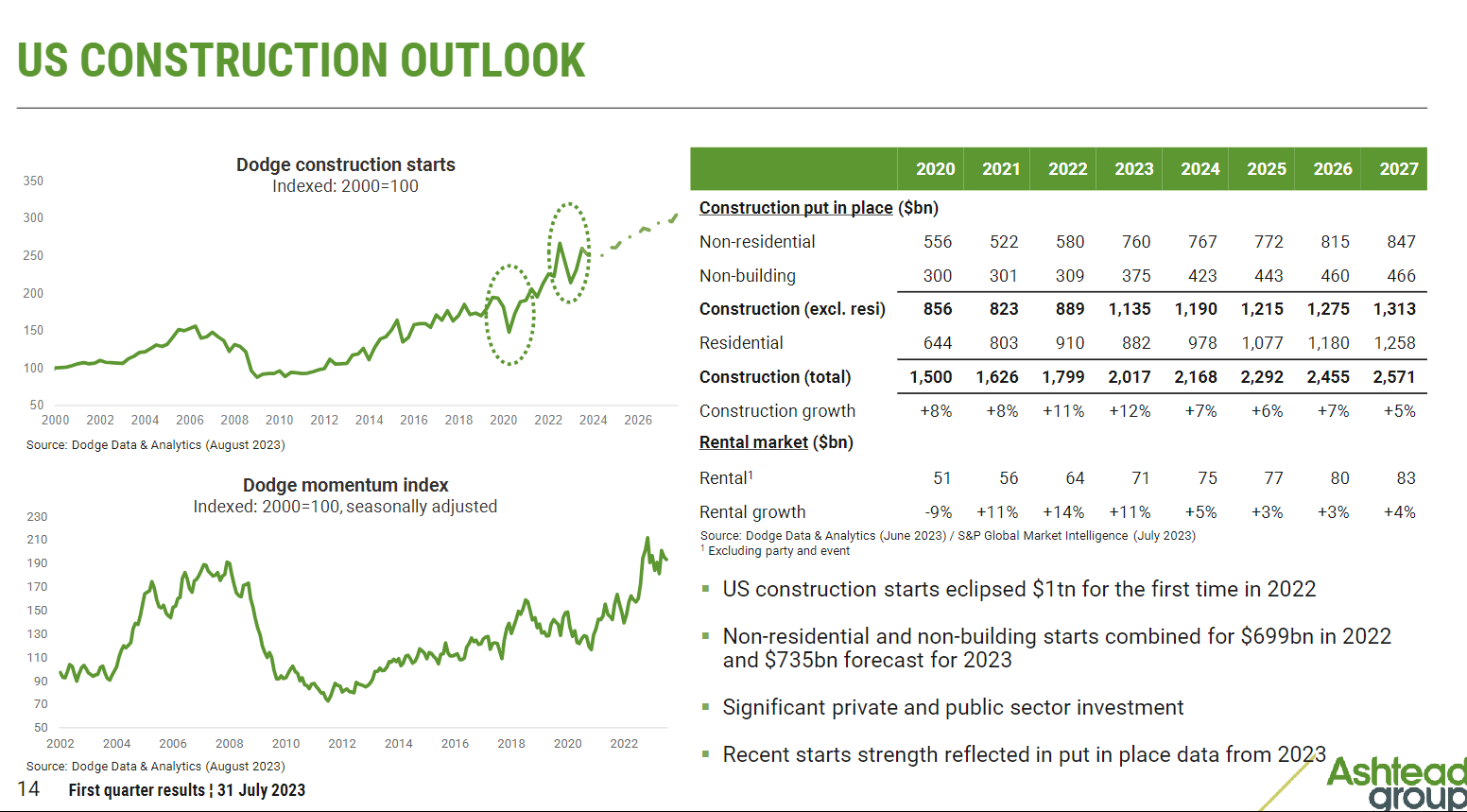

Group revenue for ASHTY increased by 19% year over year in 1Q24, which was better than expected. This was helped along by the group bringing forward some previously scheduled disposals, most notably the sale of used equipment. The most notable growth occurred in the United States, where rental-only sales increased by 16%, general tool sales increased by 14%, and specialty sales increased by 17%. Growth in rental income has been supported by an improving rate and volume environment.

Despite the fact that ASHTY is a London-listed company, the vast majority (95%) of its EBITDA comes from the United States. That's why I'm concentrating on the USA. The company achieved a 53% US drop-through rate in Q1 and projects that it will remain above 50% for the remainder of the year, though this is contingent on the pace of bolt-on M&A. Newcomers should know that M&A is dilutive at first because it takes about three years for the combined company to reach the average of the group. Margin pressure in the United States was exacerbated by the pull forward of used equipment sales, but management emphasized an improvement in same-store EBITDA margins compared to the prior year. As such, I expect margins to recover eventually. I continue to have a positive outlook on the future of the US construction industry as a whole due to the robust state of the end market, robust demand, and clear indicators of progress in finding more deals in Mega Projects. According to management, they are continuously improving their understanding by assessing current demand, customer feedback on demand, order backlogs, and future project expectations. This ongoing process reinforces management's belief in sustained structural growth in a robust market, extending into 2024 and beyond.

{kind=link}

{kind=link}

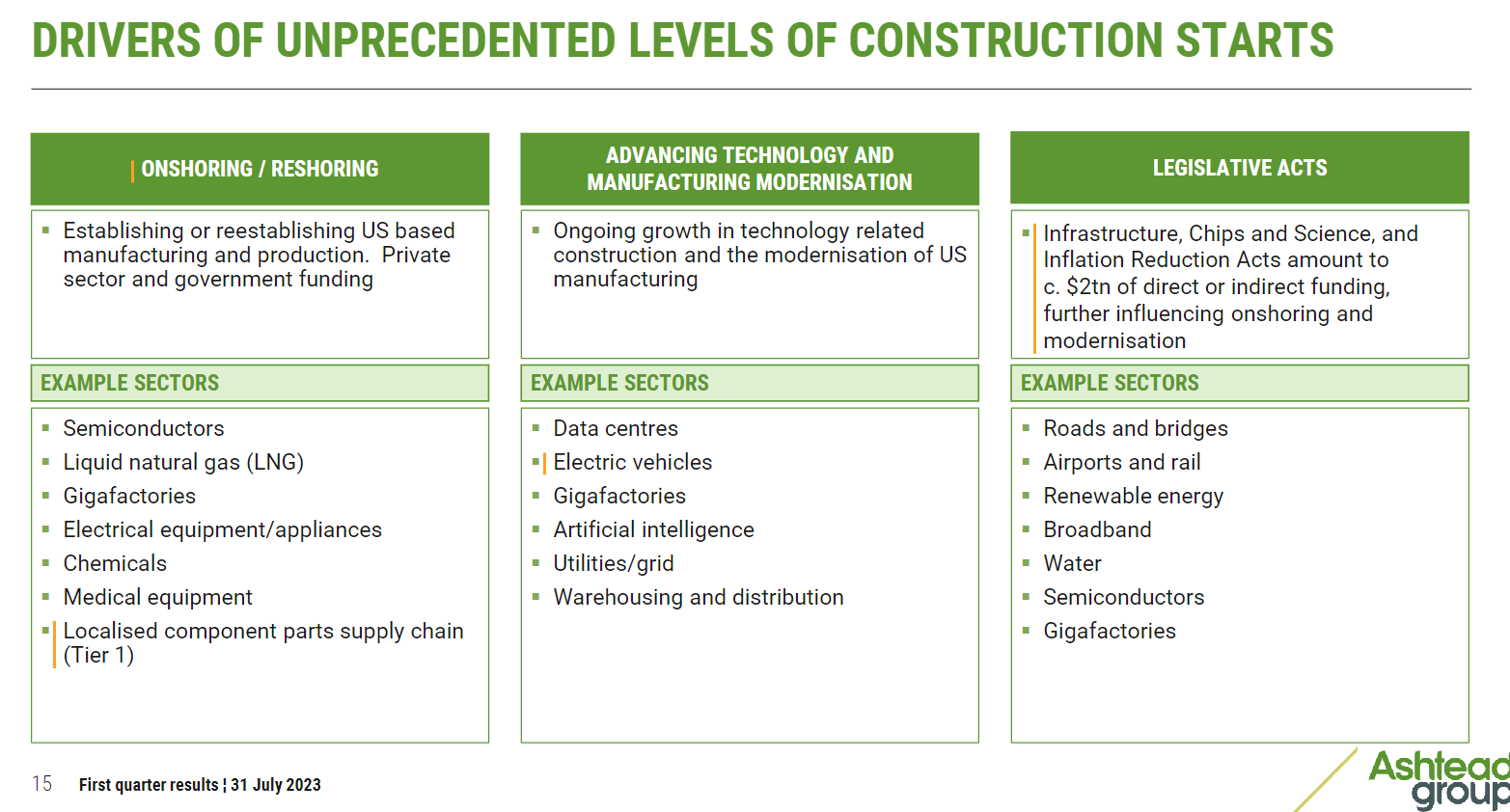

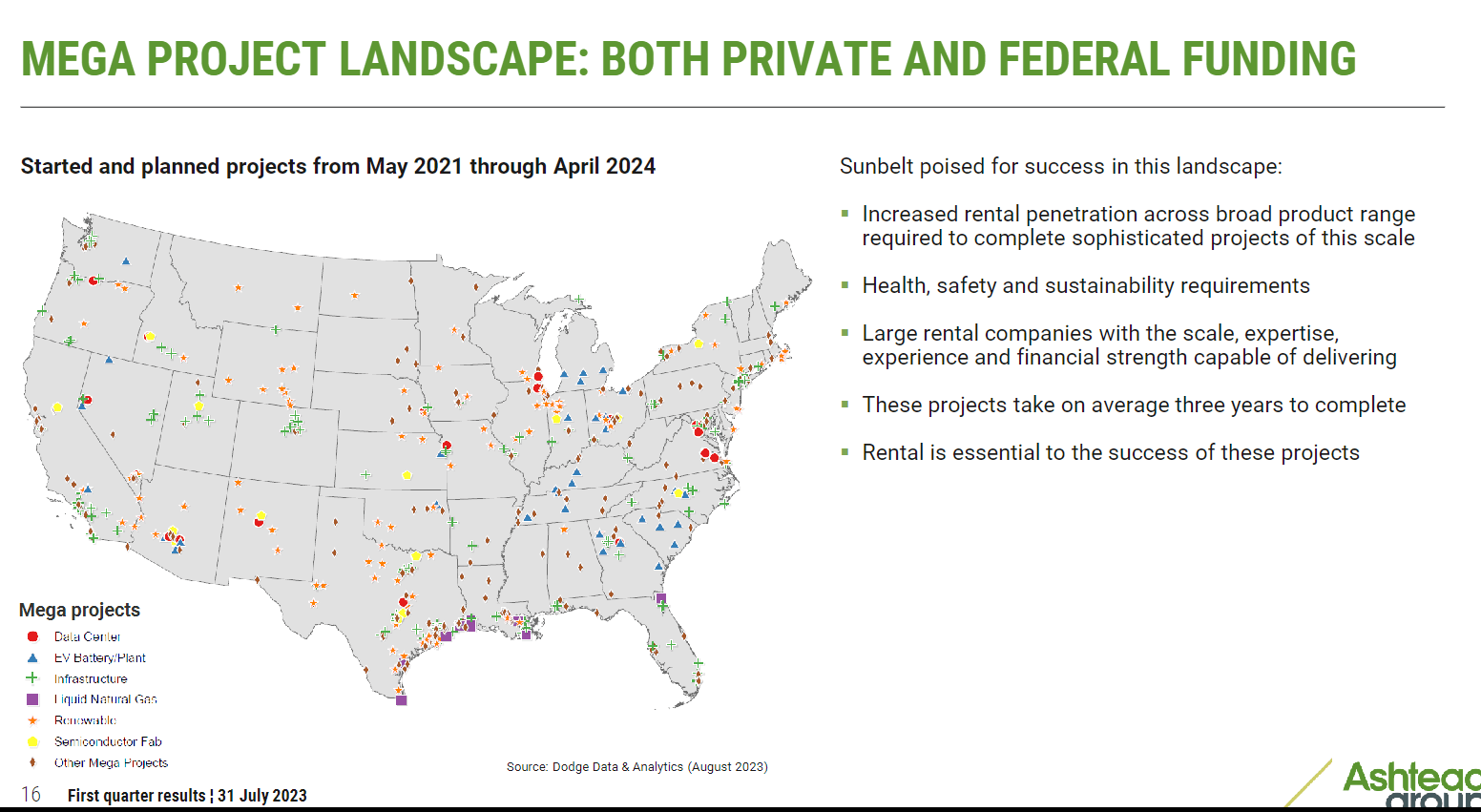

The major growth driver, which I have mentioned previously, is ASHTY's prospects in growing its Mega Projects business. The 1Q24 update further increased my outlook for this part of the business, which I expect to increasingly become a bigger growth catalyst. I believe that the next decade will be fruitful for ASHTY thanks to the growth of megaprojects, which are intrinsically linked to legislative acts in the United States. The direct implication is that there will be more requirements in terms of the number of pieces of equipment for such Mega Projects. This also means that the contractor would need to have a very strong balance sheet. As such, this Mega Project trend is likely to benefit larger players like ASHTY, United Rentals, Herc, and Home Depot. The bearish argument is that such Mega Projects might not be developed given the lack of funding (especially in the rising rate environment). I would argue that these larger projects fit into the overall direction of the nation’s development, and as such, they are less likely to be canceled because of a lack of funding.

Fundamentally, the group stated that its market share in Mega Projects has doubled and that Mega Projects now account for 10+% of the group's revenue. Quantitatively, the group notes that there are currently 500 Mega Projects either already underway or scheduled to begin before April 2024, and that this number is only growing. Given that a project must cost more than $400 million to be considered a Mega Project, 501 Mega Projects would imply at least $200 billion in sales. If spread out over 15 years, this would generate $13 billion in annual revenue, which is more than ASHTY's current total revenue.

As I've said before, this all makes clear that the non-residential cycle has been considerably delinked from the residential cycle as a result of years of change in construction composition and the more recent reshoring or U.S. de-globalization and larger-than-ever-before seen federal government spending acts, all contributing to the rise of an era of mega projects. 2Q23 earnings results call

{kind=link}

Valuation

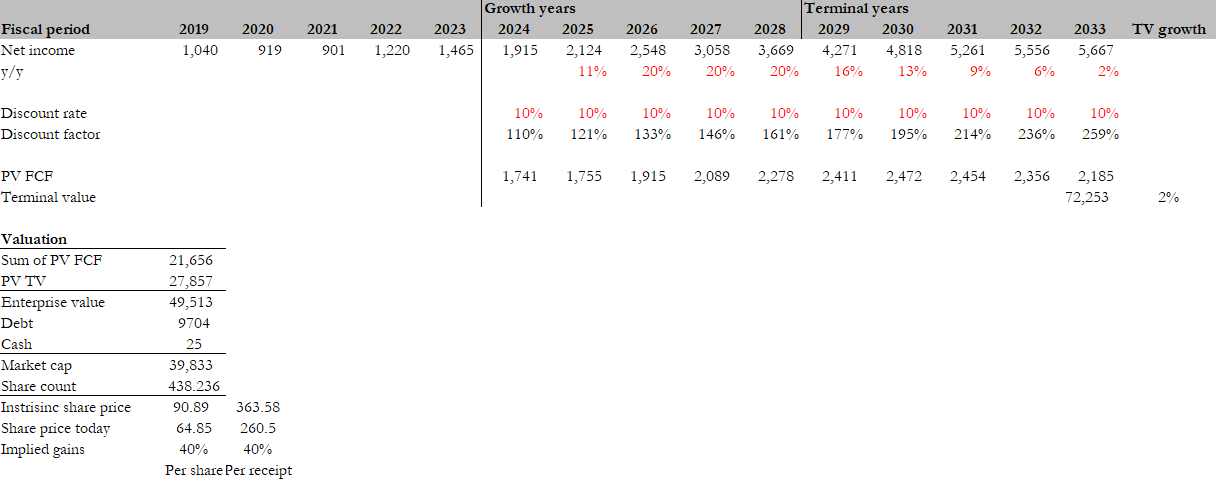

I believe the fair value for ASHTY based on my DCF model is $91. My model assumptions are that:

- Earnings to inflect in FY25 when growth normalizes

- Earnings to grow 20% as topline growth reverts to historical range, supported by further Mega Projects penetration

- Earnings growth to taper down to inflation rate over the long-term

Since my last write-up, ASHTY valuation has revised downwards to 14x, closer to comps (CAT, URI, FINGF) level. However, it is still trading at a premium which I continue to see as justified given ASHTY is growing faster and has higher profit margins.

- CAT trades at 13.7x forward PE and is expected to grow at 3% next year with 17% EBITDA margin

- URI trades at 11x forward PE and is expected to grow at 11% with 49% EBITDA margin

- FINGF trades at 11x forward PE is expected to see revenue decline 5% with 12% EBITDA margin.

{kind=link}

Risk

My thoughts on risk are the same as prior, although there have been substantial changes in ASHTY's business model and the rental market, the company still retains some characteristics of cyclicality due to the industry's inherent nature. I anticipate that ASHTY will better withstand a recession compared to its performance in the past. Nevertheless, there could still be short-term effects on earnings and market sentiment during economic downturns.

Conclusion

My bullish outlook on ASHTY remains intact, reinforced by the company's strong performance and its growing presence in Mega Projects. ASHTY's impressive 19% year-over-year revenue growth in 1Q24, particularly in the United States, highlights its resilience and growth potential in the rental market. The Mega Projects segment is emerging as a significant growth driver, with ASHTY doubling its market share in this sector. With over 500 Mega Projects underway or scheduled to begin by April 2024, ASHTY's position as a major player in this market is solidified. The company's robust balance sheet and its alignment with national development initiatives bode well for its future in Mega Projects.

For further details see:

Ashtead Group: Mega Projects Driving Mega Growth Ahead