ASHTF - Ashtead: Guidance Indicates Price Upside (Rating Upgrade)

2023-12-06 04:07:16 ET

Summary

- Ashtead Group's just-released earnings report shows a cooling off in revenue and operating profit growth, but they remain healthy nevertheless.

- Temporary factors such as a quiet hurricane season and strikes in the entertainment industry have impacted the company's performance and also affected guidance.

- Despite Ashtead's reduced outlook, however, a recent price correction and its market multiples indicate a fair price upside ahead.

When I last wrote about the construction equipment rental company Ashtead Group (ASHTF) in September, I had given it a Hold rating despite a 10% upside to the stock. This was based on the likelihood of a further softening in the company’s financials going forward after some cooling off was observed in the first quarter (Q1 2024) and there was weakness in the US construction sector, its biggest market.

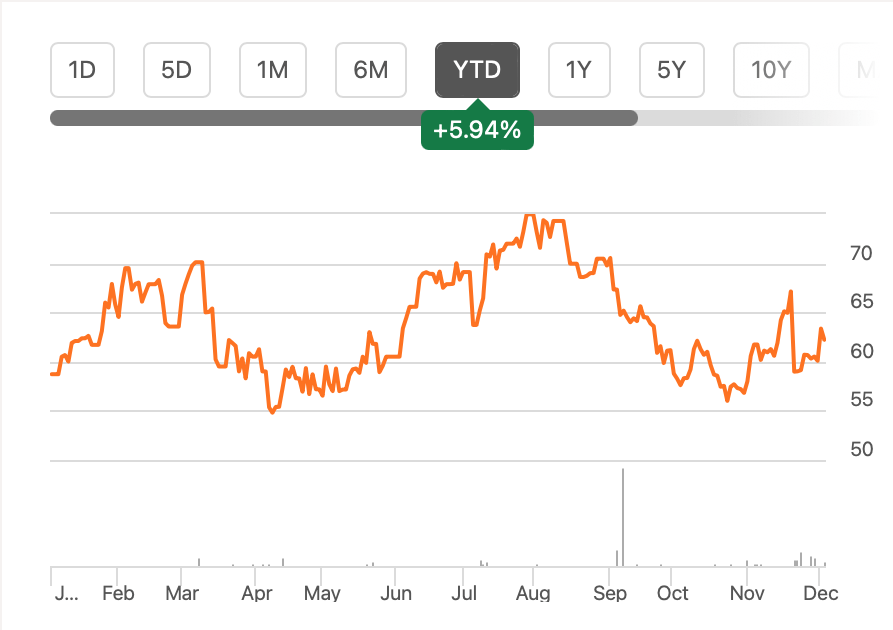

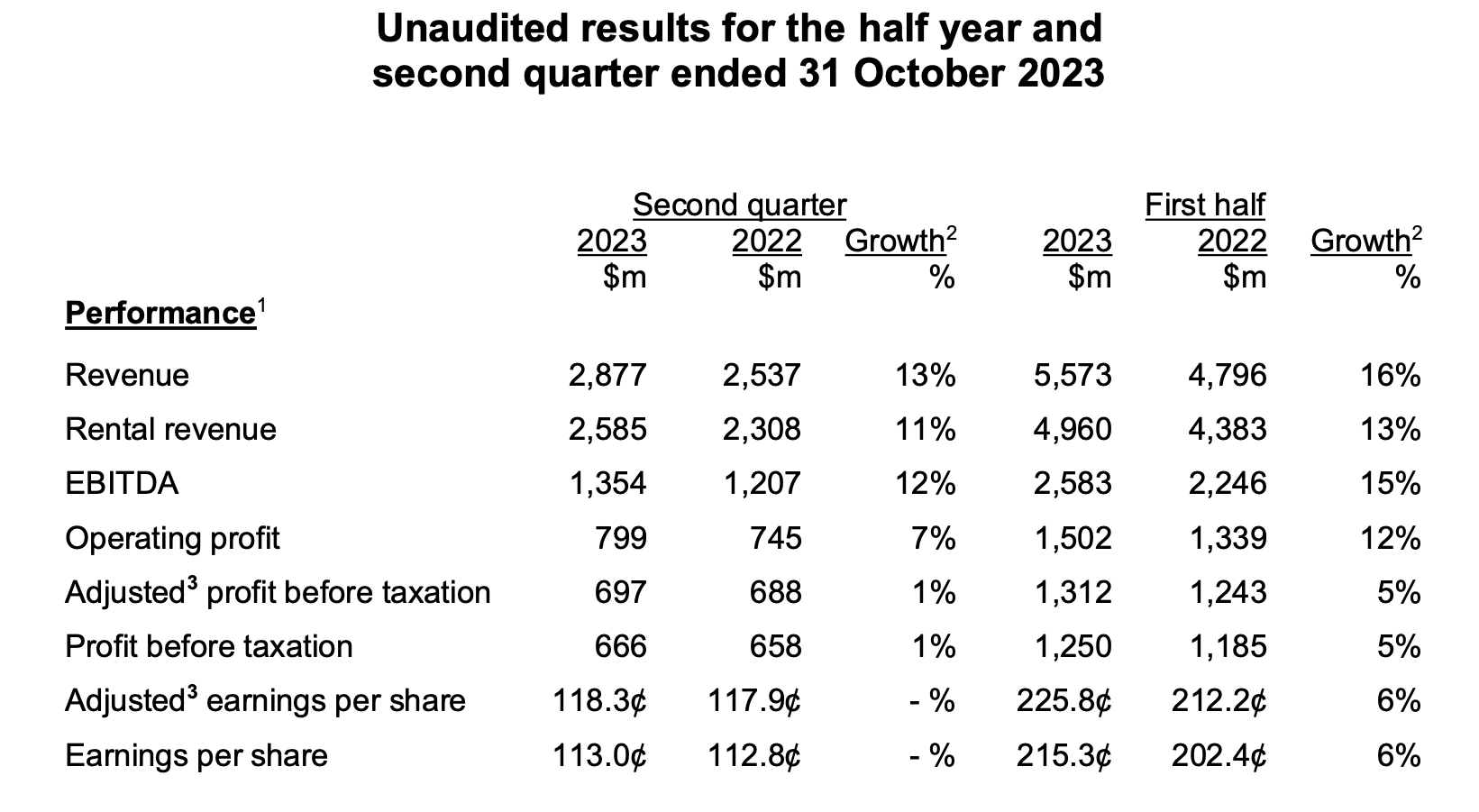

The company’s second quarter (Q2 2023) and first half (H1 2023) ending October 31, 2023, released today , confirm the slowing down. But here’s the catch. In the interim, its price has declined by 3.5% instead of seeing an uptick, making for an underwhelming price change year-to-date [YTD] (see chart below).

{kind=link}

The key focus of this discussion then is to figure out whether the price and earnings developments point towards a Buy rating again for Ashtead or not.

Some cooling off, but largely healthy financials

The latest release shows revenue growth softened from 19% year-on-year (YoY) in Q1 2023 to 13% in Q2. Operating profit growth, too, slowed down to 12% (Q1 2023: 18%). It might be a slowing down from earlier, but on their own, the numbers still look rather healthy. In fact, the operating profit margin of 26.9% for H1 2023, is actually an improvement over the 26.1% levels seen in Q1.

{kind=link}

It's also essential to note here, that Ashtead attributes the recent financial outcomes to two temporary developments:

- A quiet hurricane season and other natural occurrences like wildfires in Q3 2023 compared to past years meant lower emergency response requirements.

- The Canadian business has been impacted by writers' and actors' strikes in the entertainment industry. These have spilled over into business from other markets that rent the space as well. However, the extent of impact from the industrial action has been limited since Canada is a relatively small market for Ashtead, with a 6% revenue share as of H1 2023. Further, despite the disruption, growth in the market still has been good at 15% in CAD terms.

I am, however, somewhat concerned after looking at the latest earnings per share [EPS] figure, which has remained nearly unchanged from Q2 2022 compared to a 14% increase in Q1. Mostly higher interest expenses, but also higher taxes explain the latest EPS.

It's far from the worst situation, though, considering that the interest coverage ratio is at a healthy 6x. Also, with interest rates expected to start coming off next year, the company can be better placed sooner rather than later.

Reduced outlook

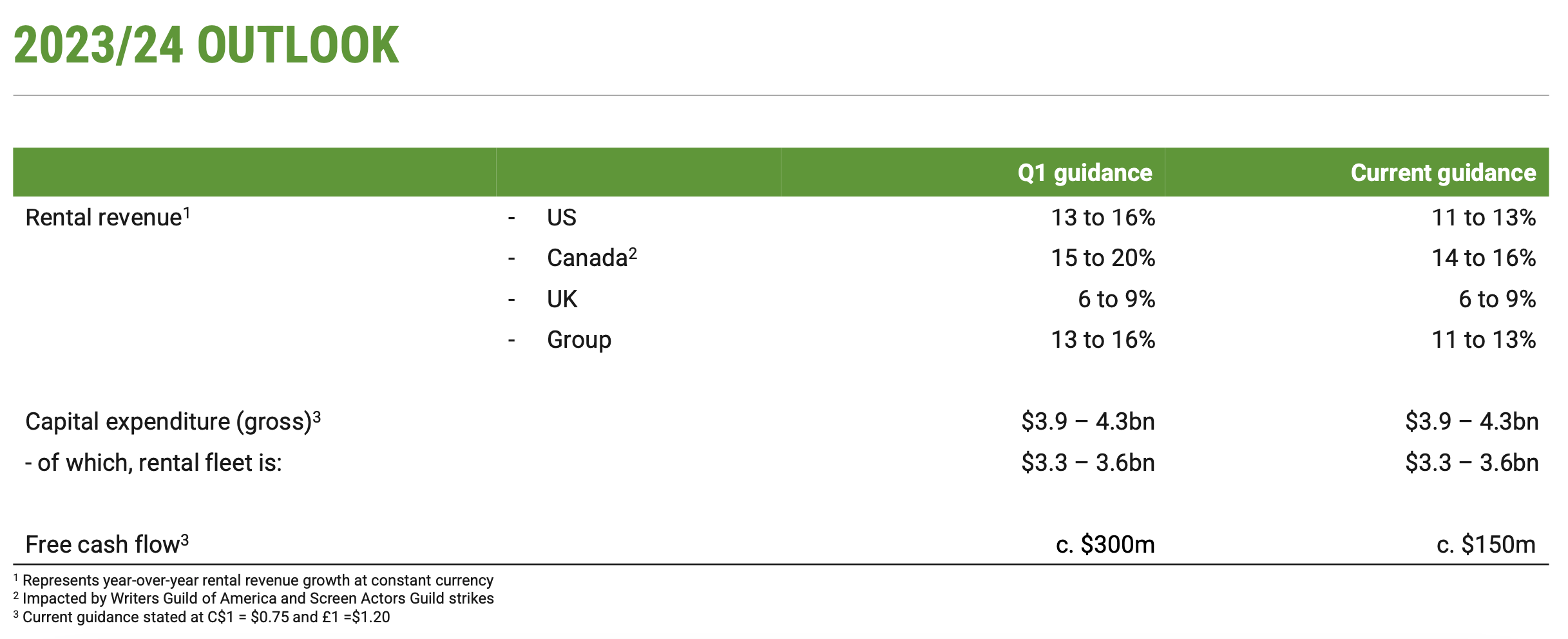

For now, though, Ashtead has reduced its outlook for its full financial year 2023 (ending April 30, 2024). It now expects rental revenue to grow by 11-13% compared to the earlier forecast of 13-16%. For context, rental revenue accounted for 89% of the company's H1 2023 revenues, and the remainder comes from the sale of new and used equipment.

{kind=link}

There are still encouraging trends forecast in the country-level guidance though. At the midpoint, the company now expects Canadian revenue to grow by 15%, which is a decline from the 17.5% expected earlier. But it is still the same as the growth seen so far. The UK market is seen rising at 7.5% in 2023, compared to a 3% increase seen in H1 2023, indicating an expected acceleration in H2 2023.

The US market, however, is something of a concern, with rental growth now expected to slow down to 12%, slower than the 14% rise seen so far. This also ties in with the general state of the construction industry in the US. The industry's leading index, the Dodge Momentum Index, which Ashtead likes to refer to, has declined by 8% YoY in October. It has seen some improvement on a month-on-month basis in the past couple of months, but it was declining for months before that, so it's not enough to rule out further weakness going forward.

Estimating full-year numbers

Based on the guidance for the group, I've estimated the potential revenue and earnings for the current financial year. Assuming that the rental revenue comes in at the midpoint of the guidance range and the revenues from the sale of equipment continue to grow at 48.4%, the same as in H1 2023, the group revenue would grow at 15.6% for the current financial year. This is around the same as the growth seen so far.

Next, assuming its net profit margin remains at 16.9%, the same as in H1 2023, the net profit figure would come in at USD 1.9 billion. This is a 16.8% YoY increase and bodes well for an EPS increase too.

The market multiples

This results in a forward GAAP price-to-earnings (P/E) ratio of 14.4x, which is more optimistic than the average of analysts' projections, which yields a forward P/E of 16.1x. Further, even my estimate is lower than the stock's five-year average of 20.7x .

Next, the TTM P/E at 16.4x has declined from the 17.1x level it was at the last I checked. Further, it's now also lower than the stock's median P/E for the past 10 years at 17.5x .

Essentially, the historical average for both the TTM and forward P/Es indicates that there's an upside for Ashtead. On average around a 25% increase in price is due. This is a significant improvement from the 10% upside indicated the last time around.

What next?

This is enough reason to make the stock and its ADRs a Buy for me now. To answer the question I intend to answer in this discussion, the balance of price and performance has tilted in Ashtead's favour again.

It's not as if there aren't risks ahead. The US construction industry, in particular, needs to be watched for further developments. Recent external events have also worked against the company. But historically, Ashtead has been on point with its guidance. Even this time, it had reduced forecasts in its trading update in November, which played out in the latest numbers.

Going by this guidance, the company is still expected to see healthy performance for the current financial year. This in turn indicates a good uptick for the stock. There can be some dips ahead if investor outlook on the industry weakens, but I see these as buying opportunities. I'm upgrading Ashtead to Buy again.

For further details see:

Ashtead: Guidance Indicates Price Upside (Rating Upgrade)